|

市場調查報告書

商品編碼

1998763

退磁系統市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測Degaussing System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

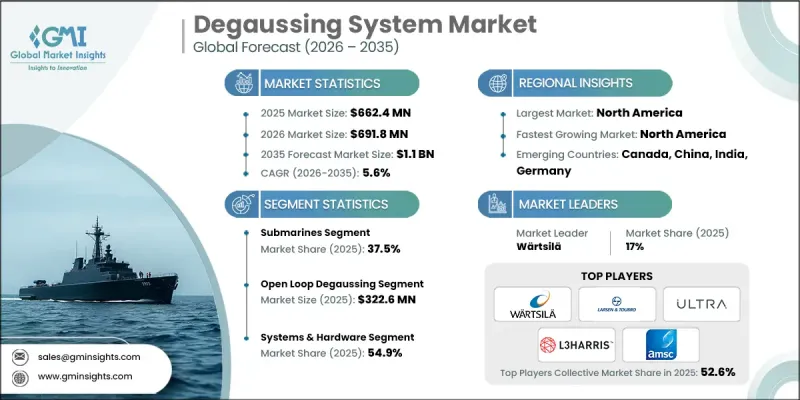

全球退磁系統市場預計到 2025 年將達到 6.624 億美元,年複合成長率為 5.6%,到 2035 年將達到 11 億美元。

市場擴張的驅動力來自海軍現代化項目的進展、艦隊規模的擴大以及應對磁性水雷和水下侵入性武器威脅日益成長的需求。世界各國海軍正在整合先進的數位監視技術,以增強艦隊的生存能力和防護能力,同時優先考慮艦艇的隱身性能和磁性特徵管理。地緣政治緊張局勢和海上安全問題正在加速消磁系統的部署,而對節能和低維護技術的日益重視也推動了市場需求。軍艦現代化和反水雷戰計畫進一步提升了磁性特徵控制系統的重要性,尤其是在潛艦和先進作戰艦艇上。預計艦隊對數位監視的持續投入以及降低營運成本的努力將使市場保持成長勢頭直至2035年。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 6.624億美元 |

| 預測金額 | 11億美元 |

| 複合年成長率 | 5.6% |

由於降低磁特徵對隱身作戰至關重要,預計到2025年,潛艦領域將佔據37.5%的市場佔有率。潛水艇在高度隱密且充滿敵意的水下環境中作業,極易受到探測和磁性水雷的威脅。世界主要海軍持續部署常規潛艦和核能,將確保對先進消磁系統(旨在維護作戰安全並增強隱身能力)的穩定需求。

預計2025年,開放回路型消磁系統市場規模將達3.226億美元,為海軍艦艇提供可靠的磁場抑制方案。這些系統利用預設電流等級消除艦艇內部的永磁和感應磁,在降低複雜性的同時提高了運作效率。其久經考驗的可靠性、易於整合以及對各種海軍平台的適應性,使其成為長期磁場管理和艦隊安全的關鍵。

受持續推進的海軍現代化舉措的推動,預計到2025年,北美消磁系統市佔率將達到36.5%。該地區擁有先進的海軍艦隊,並聚集了許多專注於磁性特徵管理解決方案的領先國防承包商。各國政府正大力投資水雷對抗措施、艦隊生存技術和數位化艦艇監視平台。在充足的國防預算和技術進步的支持下,加上持續的升級和艦隊維護計劃,預計北美將在2035年之前繼續保持消磁系統部署的主要貢獻者地位。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 海軍現代化和艦隊擴充計畫的擴展

- 磁性水雷和魚雷構成的威脅日益加劇。

- 人們越來越關注艦船的隱身性和生存能力

- 自動去磁技術進步

- 資料中心和安全資料擦除要求

- 產業潛在風險與挑戰

- 對固態儲存設備的影響有限。

- 透過替代消防技術展開競爭

- 市場機遇

- 與無人船平台整合

- 與數位監控/物聯網系統整合

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 定價策略

- 新興經營模式

- 合規要求

- 專利和智慧財產權分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 市場集中度分析

- 按地區

- 主要企業的競爭標竿分析

- 財務績效比較

- 銷售量

- 利潤率

- 研究與開發

- 產品系列比較

- 產品線寬度

- 科技

- 創新

- 區域擴張比較

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 小眾玩家

- 戰略展望矩陣

- 財務績效比較

- 主要進展

- 併購

- 夥伴關係與合作

- 技術進步

- 擴張和投資策略

- 數位轉型計劃

- 新興競爭對手和Start-Ups競爭對手的發展趨勢

第5章 市場估算與預測:依船舶類型分類,2022-2035年

- 水面作戰艦艇

- 巡防艦

- 驅逐艦

- 克爾維特

- 巡洋艦

- 航空母艦和兩棲攻擊艦

- 直升機登陸艦(LHD)

- 登陸平台船塢(LPD)

- 兩棲運輸艦(LST)

- 潛水艇

- 攻擊型潛水艇

- 彈道導彈潛艦

- 巡弋飛彈潛艦

- 巡邏和支援船隻

- 近海巡邏艦(OPV)

- 掃雷(MCMV)

- 高速攻擊艇(FAC)

- 輔助/支援船

第6章 市場估計與預測:依系統類型分類,2022-2035年

- 開放回路退磁

- 陀螺儀/地磁地圖控制

- 手動模式系統

- 舊式船舶系統

- 封閉回路型退磁

- 基於磁力計的控制

- 簽章預測系統

- 一種降低距離依賴性的系統。

- 混合系統

- 多模系統

- 可升級平台

- 模組化系統

第7章 市場估算與預測:依產品/服務分類,2022-2035年

- 系統硬體

- 退磁線圈組件

- 電源單元

- 控制面板

- 磁力計和感測器

- 雙極放大器和導體

- 嵌入式控制軟體

- 服務

- 安裝和試運行

- 預防性保養

- 維修和故障排除

- 系統現代化

- 校準與檢驗

- 技術支援和培訓

第8章 市場估算與預測:依安裝類型分類,2022-2035年

- 新安裝(OEM整合)

- 維修/現代化

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- 主要企業

- Wartsila

- L3Harris Technologies Inc.

- Larsen &Toubro Limited

- Ultra Electronics Holdings Plc

- 按地區分類的主要企業

- 北美洲

- American Superconductor Corporation

- Magnetics International

- 亞太地區

- Surma Ltd.

- Dayatech Merin

- 歐洲

- Polyamp

- Hitzinger GmbH

- STL Systems AG

- 北美洲

- 特殊玩家/干擾者

- IFEN

- K&G Marine

- Meriton Industries

- DA-Group

- HAELOG

The Global Degaussing System Market was valued at USD 662.4 million in 2025 and is estimated to grow at a CAGR of 5.6% to reach USD 1.1 billion in 2035.

The market expansion is driven by growing naval modernization programs, increasing fleet expansions, and the rising need to counter threats from magnetic mines and influence-based underwater weapons. Navies worldwide emphasize vessel stealth and magnetic signature management while integrating advanced digital monitoring technologies to enhance fleet survivability and protection. Geopolitical tensions and maritime security concerns are accelerating the adoption of degaussing systems, while the increasing focus on energy-efficient and low-maintenance technologies reinforce demand. The modernization of warships and mine countermeasure programs has elevated the significance of magnetic signature control systems, particularly in submarines and advanced combat vessels. Rising investment in digital monitoring and operational cost reduction across fleets is expected to sustain market momentum through 2035.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $662.4 Million |

| Forecast Value | $1.1 Billion |

| CAGR | 5.6% |

The submarines segment held a 37.5% share in 2025, due to the critical requirement for magnetic signature reduction in stealth operations. Submarines operate in sensitive and hostile underwater environments, making them highly vulnerable to detection and magnetic mines. The continuous deployment of conventional and nuclear-powered submarines by major navies globally ensures consistent demand for advanced degaussing systems designed to maintain operational security and enhance stealth capabilities.

The open-loop degaussing systems segment generated USD 322.6 million in 2025, as they provide reliable magnetic reduction for naval vessels. These systems use predetermined electrical current levels to neutralize permanent and induced magnetism in ships, offering operational efficiency with reduced complexity. Their proven reliability, straightforward integration, and adaptability across a range of naval platforms make them essential for long-term magnetic management and fleet safety.

North America Degaussing System Market held 36.5% share in 2025, driven by continuous naval modernization initiatives. The region benefits from advanced naval fleets and the presence of leading defense contractors specializing in magnetic signature management solutions. Governments are investing heavily in mine countermeasure systems, fleet survivability technologies, and digital vessel monitoring platforms. Continuous upgrades and fleet sustainment programs are expected to maintain North America as a key contributor to degaussing system adoption through 2035, underpinned by strong defense budgets and technological advancements.

Leading companies operating in the Global Degaussing System Market include Ultra Electronics Holdings Plc, Polyamp, American Superconductor Corporation, Larsen & Toubro Limited, HAELOG, Hitzinger GmbH, L3Harris Technologies Inc., DA-Group, Dayatech Merin, STL Systems AG, K&G Marine, Surma Ltd., Wartsila, IFEN, and Magnetics International. Key players in the Global Degaussing System Market are employing strategies to strengthen their foothold and expand their market presence. Companies are investing in R&D to develop energy-efficient, low-maintenance, and digitally integrated degaussing solutions suitable for modern naval fleets. Strategic partnerships with defense contractors, governments, and shipbuilding companies enhance technology adoption and global reach. Firms are also focusing on modular and scalable systems to address different vessel classes, including submarines and surface combatants. Expanding into emerging maritime markets and offering maintenance, training, and lifecycle support services further improves customer retention.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Vessel type trends

- 2.2.2 System type trends

- 2.2.3 Offering trends

- 2.2.4 Installation type trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising naval modernization and fleet expansion programs

- 3.2.1.2 Growing threats from magnetic mines/torpedoes

- 3.2.1.3 Increased focus on vessel stealth and survivability

- 3.2.1.4 Technological advances in degaussing automation

- 3.2.1.5 Data center and secure data destruction requirements

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited impact on solid-state storage devices

- 3.2.2.2 Competition from alternative suppression technologies

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with unmanned vessel platforms

- 3.2.3.2 Integration with digital monitoring/IoT systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Vessel Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Surface combatants

- 5.2.1 Frigates

- 5.2.2 Destroyers

- 5.2.3 Corvettes

- 5.2.4 Cruisers

- 5.3 Aircraft carriers & amphibious vessels

- 5.3.1 Landing helicopter dock (LHD)

- 5.3.2 Landing platform dock (LPD)

- 5.3.3 Landing ship tank (LST)

- 5.4 Submarines

- 5.4.1 Attack submarines

- 5.4.2 Ballistic missile submarines

- 5.4.3 Cruise missile submarines

- 5.5 Patrol & support vessels

- 5.5.1 Offshore patrol vessels (OPV)

- 5.5.2 Mine countermeasure vessels (MCMV)

- 5.5.3 Fast attack craft (FAC)

- 5.5.4 Auxiliary & support ships

Chapter 6 Market Estimates and Forecast, By System Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Open loop degaussing

- 6.2.1 Gyro / geomagnetic map control

- 6.2.2 Manual mode systems

- 6.2.3 Legacy fleet systems

- 6.3 Closed loop degaussing

- 6.3.1 Magnetometer-based control

- 6.3.2 Signature prediction systems

- 6.3.3 Reduced range dependency systems

- 6.4 Hybrid systems

- 6.4.1 Multi-mode systems

- 6.4.2 Upgrade-ready platforms

- 6.4.3 Modular systems

Chapter 7 Market Estimates and Forecast, By Offering, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Systems & hardware

- 7.2.1 Degaussing coil assemblies

- 7.2.2 Power supply units

- 7.2.3 Control cabinets

- 7.2.4 Magnetometers & sensors

- 7.2.5 Bipolar amplifiers & conductors

- 7.2.6 Embedded control software

- 7.3 Services

- 7.3.1 Installation & commissioning

- 7.3.2 Preventive maintenance

- 7.3.3 Repairs & troubleshooting

- 7.3.4 System modernization

- 7.3.5 Calibration & verification

- 7.3.6 Technical support & training

Chapter 8 Market Estimates and Forecast, By Installation Type, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 New build (OEM integration)

- 8.3 Retrofit / modernization

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Wartsila

- 10.1.2 L3Harris Technologies Inc.

- 10.1.3 Larsen & Toubro Limited

- 10.1.4 Ultra Electronics Holdings Plc

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 American Superconductor Corporation

- 10.2.1.2 Magnetics International

- 10.2.2 Asia Pacific

- 10.2.2.1 Surma Ltd.

- 10.2.2.2 Dayatech Merin

- 10.2.3 Europe

- 10.2.3.1 Polyamp

- 10.2.3.2 Hitzinger GmbH

- 10.2.3.3 STL Systems AG

- 10.2.1 North America

- 10.3 Niche Players/Disruptors

- 10.3.1 IFEN

- 10.3.2 K&G Marine

- 10.3.3 Meriton Industries

- 10.3.4 DA-Group

- 10.3.5 HAELOG

退磁系統市場:全球市場預測,2026-2032年

退磁系統市場:全球市場預測,2026-2032年 消磁系統市場分析及預測(至2035年):類型、產品類型、服務、技術、組件、應用、部署狀態、最終用戶、功能

消磁系統市場分析及預測(至2035年):類型、產品類型、服務、技術、組件、應用、部署狀態、最終用戶、功能 消磁系統:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

消磁系統:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 2034年全球退磁系統市場預測-依產品類型、容器類型、最終用戶和地區分類的分析

2034年全球退磁系統市場預測-依產品類型、容器類型、最終用戶和地區分類的分析 消磁系統市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測海軍艦艇消磁系統市場:按艦艇類型、組件、安裝類型、技術和最終用途分類的全球預測,2026-2032年

消磁系統市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測海軍艦艇消磁系統市場:按艦艇類型、組件、安裝類型、技術和最終用途分類的全球預測,2026-2032年 退磁系統市場 - 全球產業規模、佔有率、趨勢、機會、預測:按船舶類型、解決方案、地區和競爭對手分類,2021-2031年

退磁系統市場 - 全球產業規模、佔有率、趨勢、機會、預測:按船舶類型、解決方案、地區和競爭對手分類,2021-2031年 船舶類型、解決方案、最終用戶和地區分類的退磁系統市場規模、佔有率和成長分析 - 2026-2033 年產業預測

船舶類型、解決方案、最終用戶和地區分類的退磁系統市場規模、佔有率和成長分析 - 2026-2033 年產業預測