|

市場調查報告書

商品編碼

1998734

全地形車(ATV)市場機會、成長要素、產業趨勢分析及2026-2035年預測All-Terrain Vehicle (ATV) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

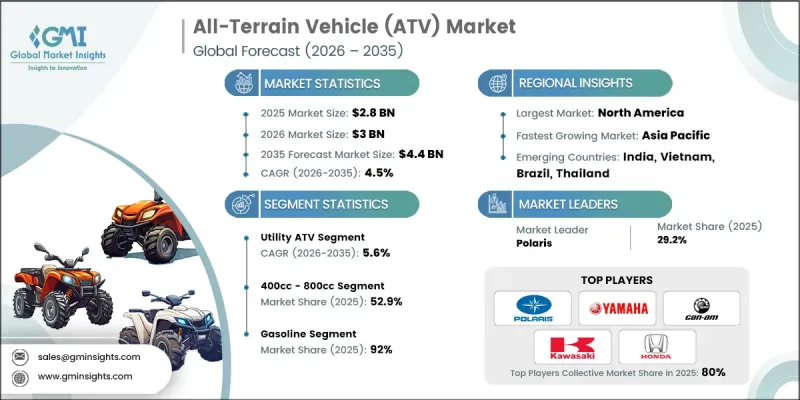

全球全地形車(ATV)市場預計到 2025 年價值 28 億美元,預計到 2035 年將以 4.5% 的複合年成長率成長至 44 億美元。

全地形車市場的成長主要得益於戶外活動參與度的提高以及對能夠穿越複雜地形的車輛需求的不斷成長。隨著人們對戶外休閒的興趣持續高漲,消費者越來越傾向於選擇具備可靠越野性能並能進入偏遠地區的車輛。同時,在惡劣環境下營運的產業也推動了對耐用且用途廣泛的運輸解決方案的需求。全地形車在農業和土地管理等商業領域的廣泛應用也促進了市場的發展。這些車輛在傳統交通工具難以通行的地區提供了運輸和營運效率。法律規範和土地管理政策也影響市場走向,促使製造商設計符合環境標準和使用指南的車輛。為此,各公司正在推出以提升性能、耐用性和永續性為重點的創新車輛設計。此外,隨著工業和休閒用戶尋求更環保的替代方案,電動全地形車的逐步推廣正成為一大趨勢。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 28億美元 |

| 預測金額 | 44億美元 |

| 複合年成長率 | 4.5% |

預計到2025年,多用途全地形車(ATV)市佔率將達到56%,並在2026年至2035年間以5.6%的複合年成長率成長。這類車輛的需求主要源自於各行業在崎嶇地形上可靠運輸的實際應用。多用途全地形車廣泛應用於需要在戶外環境中進行機動性和設備運輸的商業活動。其多功能性和耐用性使其適用於物料運輸、日常巡檢和一般野外作業。隨著工業領域對戶外作業效率的持續關注,對能夠支援這些功能的車輛的需求預計將保持強勁。土地管理和農業作業機械化的不斷提高也促進了專為多用途應用而設計的全地形車的穩步普及。

到2025年,汽油車市佔率將達到92%。汽油車憑藉著可靠的性能和便利的加油設施,依然廣受歡迎。這些車輛繼續為各種商業和休閒應用提供支持,在這些應用中,可靠的能源供應至關重要。許多地區加油站的廣泛分佈確保了燃料供應的穩定性,從而推動了汽油動力全地形車的持續普及。其強勁的引擎性能和長續航里程使其適用於偏遠地區等對車輛穩定性要求極高的嚴苛應用場景。

美國全地形車(ATV)市場佔85%的市場佔有率,預計2025年市場規模將達到17億美元。美國全地形車市場發展成熟,並在一個系統化的法規環境下運作,該環境強調安全、土地使用準則和車輛標準。在農村地區,越野出行在日常營運中扮演著至關重要的角色,因此對全地形車的需求尤其旺盛。這些車輛在農業和土地休閒活動中的廣泛應用,以支撐穩定的市場需求。用於農業和畜牧業的大片土地,使得人們持續需要可靠的交通工具來跨越廣闊的區域。此外,休閒越野活動仍然是市場需求的重要驅動力,而指定的越野路線和便利的戶外空間也鼓勵人們負責任地使用車輛。

目錄

第1章:調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率分析

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 戶外休閒參與者增加

- 精密農業實踐的擴展

- 增加對農村地區基礎設施和土地管理的投入

- 動力傳動系統和懸吊系統的產品創新

- 產業潛在風險與挑戰

- 安全問題和事故率

- 關於越野通行環境法規

- 市場機遇

- 越野車的電氣化

- 在國防和邊境監控領域不斷擴展的應用

- 售後配件和性能增強產品

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 美國全地形車(ATV)安全法規和消費品安全委員會(CPSC)指南

- 聯邦土地使用權與越野車輛管理條例

- 非道路火花點火引擎的排放氣體法規

- 加拿大越野車的安全和省級註冊要求

- 歐洲

- 歐盟四輪與越野車輛型式認證框架

- ECE車輛安全與煞車系統法規

- 各國特定的類型認證和道路使用限制

- 環境和噪音排放法規

- 亞太地區

- 中國越野車製造排放氣體標準

- 印度四輪車輛與非公路用車輛型式認證標準

- 日本車輛安全與小型越野機動性指南

- 澳洲越野車設計和安全要求

- 東協區域汽車認證框架

- 拉丁美洲

- 巴西針對越野車輛的安全與環境法規

- 阿根廷車輛登記和使用法規

- 符合墨西哥製造和安全標準

- 區域越野車法規結構

- 中東和非洲

- 阿拉伯聯合大公國關於在沙漠中駕駛和運營越野車輛的許可和法規。

- 沙烏地阿拉伯的汽車安全標準與檢驗標準

- 南非越野車登記和安全要求

- 北美洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格分析(基於初步調查)

- 對過去價格趨勢的分析

- 按玩家類型分類的定價策略

- 交易數據分析(基於付費資料庫)

- 進出口量及進口額趨勢

- 主要貿易路線及關稅的影響

- 生產能力和生產趨勢(基於初步調查)

- 按地區和主要生產商分類的安裝能力

- 運轉率和擴張計劃

- 成本細分分析

- 專利分析(基於初步研究)

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 關於碳足跡的考量

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 針對特定領域的生成式人工智慧應用案例和實施藍圖

- 風險、限制和監管考量

- 預測假設和情境分析(基於初步研究)

- 基本案例-驅動複合年成長率的關鍵宏觀經濟與產業變量

- 樂觀情境-宏觀經濟與產業利好因素

- 悲觀情景-宏觀經濟放緩或產業逆風

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲(MEA)

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃及資金籌措

第5章 市場估價與預測:依車輛類型分類,2022-2035年

- 多用途全地形車

- 運動型全地形車

- 休閒車

- 青少年全地形車

第6章 市場估算與預測:依引擎排氣量分類,2022-2035年

- 排氣量低於400cc

- 400cc~800cc

- 超過800cc

第7章 市場估算與預測:依燃料類型分類,2022-2035年

- 汽油

- 電

第8章 市場估算與預測:依驅動系統分類,2022-2035年

- 兩輪驅動(2WD)

- 四輪驅動(4WD)

- 全輪驅動(AWD)

第9章 市場估計與預測:依應用領域分類,2022-2035年

- 農業/耕作

- 林業

- 軍事/國防

- 運動賽車

- 休閒與旅遊

- 工業和公共產業

- 其他

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 挪威

- 荷蘭

- 瑞典

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 新加坡

- 泰國

- 印尼

- 越南

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲(MEA)

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

第11章:公司簡介

- 世界公司

- BRP

- Honda

- Kawasaki

- Polaris

- Suzuki

- Textron

- Yamaha

- 本地球員

- Arctic Cat

- Italika

- John Deere

- Kubota

- Kymco

- TGB

- 新興企業/顛覆者

- Apollo

- Bashan

- CFMoto

- Coolster

- Hisun

- Linhai

- Taotao

The Global All-Terrain Vehicle (ATV) Market was valued at USD 2.8 billion in 2025 and is estimated to grow at a CAGR of 4.5% to reach USD 4.4 billion by 2035.

Growth in the all-terrain vehicle market is largely supported by increasing participation in outdoor activities and the growing need for vehicles capable of navigating challenging landscapes. As interest in outdoor recreation continues to rise, consumers are increasingly seeking vehicles designed for reliable off-road mobility and access to remote areas. At the same time, industries that operate in rugged environments are contributing to the demand for durable and versatile transportation solutions. The expanding use of all-terrain vehicles in professional applications such as agriculture and land management is also strengthening market development. These vehicles provide mobility and operational efficiency in areas where conventional transportation options are less practical. Regulatory frameworks and land management policies are also influencing the direction of the market, encouraging manufacturers to design vehicles that comply with environmental standards and usage guidelines. In response, companies are introducing innovative vehicle designs that focus on improved performance, durability, and sustainability. The gradual adoption of electric all-terrain vehicles is also emerging as an important trend as industries and recreational users look for environmentally responsible alternatives.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.8 Billion |

| Forecast Value | $4.4 Billion |

| CAGR | 4.5% |

The utility ATV segment held 56% share in 2025 and is projected to grow at a CAGR of 5.6% between 2026 and 2035. Demand for these vehicles is largely supported by their practical applications in sectors that require reliable transportation across uneven or difficult terrain. Utility all-terrain vehicles are widely utilized for operational activities that require mobility and equipment handling in outdoor environments. Their versatility and durability make them suitable for tasks that involve the transportation of materials, routine inspections, and general field operations. As industries continue to prioritize efficiency in outdoor work environments, the demand for vehicles that can support these functions is expected to remain strong. The increasing mechanization of land management and agricultural operations also contributes to the consistent adoption of utility-focused all-terrain vehicles.

The gasoline segment held a share of 92% in 2025. Gasoline-powered vehicles remain widely preferred due to their dependable performance and the convenience of refueling infrastructure. These vehicles continue to support a broad range of operational and recreational uses where a reliable energy supply is essential. The extensive availability of gasoline refueling points across many regions ensures consistent access to fuel, which strengthens the continued adoption of gasoline-powered all-terrain vehicles. Their strong engine performance and long operational range make them suitable for demanding applications in remote environments where consistent vehicle performance is critical.

United States All-Terrain Vehicle (ATV) Market accounted for 85% share, generating USD 1.7 billion in 2025. The market in the country is well established and operates within a structured regulatory environment that emphasizes safety, land usage guidelines, and vehicle standards. Demand for all-terrain vehicles is particularly strong in rural areas where off-road mobility plays a key role in daily operations. The widespread use of these vehicles in agricultural and land management activities supports steady market demand. Large land areas used for farming and ranching create consistent requirements for reliable transportation across extensive properties. In addition, recreational off-road activities remain an important contributor to market demand, supported by designated trails and accessible outdoor spaces that encourage responsible vehicle use.

Key companies participating in the Global All-Terrain Vehicle (ATV) Market include Polaris, Yamaha, Honda, Kawasaki, Suzuki, Arctic Cat, BRP, Textron, CFMoto, and Kymco. Companies operating in the Global All-Terrain Vehicle (ATV) Market are focusing on several strategic initiatives to strengthen their competitive position and expand their market reach. Product innovation remains a primary strategy, with manufacturers investing in advanced vehicle technologies that enhance durability, performance, and user safety. Many companies are also developing electric and environmentally friendly vehicle options to align with evolving environmental regulations and sustainability goals. Strategic partnerships with distributors and regional dealers are helping manufacturers expand their presence across key geographic markets. Additionally, firms are increasing investments in research and development to improve vehicle efficiency and introduce new features that enhance user experience. Expanding production capacity and strengthening supply chain networks are also helping companies respond effectively to growing global demand for all-terrain vehicles.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Displacement

- 2.2.4 Fuel

- 2.2.5 Drive

- 2.2.6 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growth in outdoor recreation participation

- 3.2.1.2 Expansion of precision agriculture practices

- 3.2.1.3 Rising rural infrastructure and land management spending

- 3.2.1.4 Product innovation in powertrain and suspension systems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Safety concerns and accident rates

- 3.2.2.2 Environmental restrictions on off road access

- 3.2.3 Market opportunities

- 3.2.3.1 Electrification of off-road vehicles

- 3.2.3.2 Growth in defense and border surveillance applications

- 3.2.3.3 Aftermarket accessories and performance upgrades

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 United States all terrain vehicle safety regulations and Consumer Product Safety Commission guidelines

- 3.4.1.2 Federal land access and off road vehicle management rules

- 3.4.1.3 Emission standards for off road spark ignition engines

- 3.4.1.4 Canada off road vehicle safety and provincial registration requirements

- 3.4.2 Europe

- 3.4.2.1 European Union type approval framework for quadricycles and off road vehicles

- 3.4.2.2 ECE vehicle safety and braking system regulations

- 3.4.2.3 Country level homologation and road use restrictions

- 3.4.2.4 Environmental and noise emission compliance standards

- 3.4.3 Asia Pacific

- 3.4.3.1 China off road vehicle manufacturing and emission standards

- 3.4.3.2 India quadricycle and off highway vehicle homologation norms

- 3.4.3.3 Japan vehicle safety and small off road mobility guidelines

- 3.4.3.4 Australia off road vehicle design and safety requirements

- 3.4.3.5 ASEAN regional vehicle certification frameworks

- 3.4.4 Latin America

- 3.4.4.1 Brazil off road vehicle safety and environmental compliance rules

- 3.4.4.2 Argentina vehicle registration and usage regulations

- 3.4.4.3 Mexico manufacturing standards and safety compliance

- 3.4.4.4 Regional off road vehicle regulatory frameworks

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE off road vehicle licensing and desert operation rules

- 3.4.5.2 Saudi Arabia vehicle safety and inspection standards

- 3.4.5.3 South Africa off road vehicle registration and safety requirements

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Pricing Analysis (Driven by primary research)

- 3.8.1 Historical Price Trend Analysis

- 3.8.2 Pricing Strategy by Player Type

- 3.9 Trade Data Analysis (Driven by paid database)

- 3.9.1 Import/export volume & value trends

- 3.9.2 Key trade corridors & tariff impact

- 3.10 Capacity & Production Landscape (Driven by primary research)

- 3.10.1 Installed Capacity by Region & Key Producer

- 3.10.2 Capacity Utilization Rates & Expansion Pipelines

- 3.11 Cost breakdown analysis

- 3.12 Patent analysis (Driven by primary research)

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly Initiatives

- 3.13.5 Carbon footprint considerations

- 3.14 Impact of AI and Generative AI on the Market

- 3.14.1 AI Driven Disruption of Existing Business Models

- 3.14.2 GenAI Use Cases and Adoption Roadmap by Segment

- 3.14.3 Risks Limitations and Regulatory Considerations

- 3.15 Forecast assumptions & scenario analysis (Driven by primary research)

- 3.15.1 Base Case- Key Macro & Industry Variables Driving CAGR

- 3.15.2 Optimistic Scenarios- Favorable macro and industry tailwinds

- 3.15.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicle, 2022 - 2035 (USD Mn, Units)

- 5.1 Key trends

- 5.2 Utility ATV

- 5.3 Sport ATV

- 5.4 Recreational ATV

- 5.5 Youth ATV

Chapter 6 Market Estimates & Forecast, By Displacement, 2022 - 2035 (USD Mn, Units)

- 6.1 Key trends

- 6.2 Below 400cc

- 6.3 400cc - 800cc

- 6.4 Above 800cc

Chapter 7 Market Estimates & Forecast, By Fuel, 2022 - 2035 (USD Mn, Units)

- 7.1 Key trends

- 7.2 Gasoline

- 7.3 Electric

Chapter 8 Market Estimates & Forecast, By Drive, 2022 - 2035 (USD Mn, Units)

- 8.1 Key trends

- 8.2 2-Wheel Drive (2WD)

- 8.3 4-Wheel Drive (4WD)

- 8.4 All-Wheel Drive (AWD)

Chapter 9 Market Estimates & Forecast, By Application, 2022 - 2035 (USD Mn, Units)

- 9.1 Key trends

- 9.2 Agriculture & Farming

- 9.3 Forestry

- 9.4 Military & Defense

- 9.5 Sports & Racing

- 9.6 Recreation & Tourism

- 9.7 Industrial & Utility Services

- 9.8 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 (USD Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Norway

- 10.3.8 Netherlands

- 10.3.9 Sweden

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Singapore

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Turkey

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 BRP

- 11.1.2 Honda

- 11.1.3 Kawasaki

- 11.1.4 Polaris

- 11.1.5 Suzuki

- 11.1.6 Textron

- 11.1.7 Yamaha

- 11.2 Regional Players

- 11.2.1 Arctic Cat

- 11.2.2 Italika

- 11.2.3 John Deere

- 11.2.4 Kubota

- 11.2.5 Kymco

- 11.2.6 TGB

- 11.3 Emerging Players / Disruptors

- 11.3.1 Apollo

- 11.3.2 Bashan

- 11.3.3 CFMoto

- 11.3.4 Coolster

- 11.3.5 Hisun

- 11.3.6 Linhai

- 11.3.7 Taotao

全地形車引擎市場-全球產業規模、佔有率、趨勢、機會及預測(2021-2031):依類型、需求類別、功率、地區及競爭格局分類電動全地形車市場-全球產業規模、佔有率、趨勢、機會與預測:按應用、驅動類型、地區和競爭格局分類,2021-2031年

全地形車引擎市場-全球產業規模、佔有率、趨勢、機會及預測(2021-2031):依類型、需求類別、功率、地區及競爭格局分類電動全地形車市場-全球產業規模、佔有率、趨勢、機會與預測:按應用、驅動類型、地區和競爭格局分類,2021-2031年 全地形車(ATV)市場報告:按類型、應用、引擎類型、車輪數量、驅動系統、燃料類型、乘客容量和地區分類(2026-2034 年)

全地形車(ATV)市場報告:按類型、應用、引擎類型、車輪數量、驅動系統、燃料類型、乘客容量和地區分類(2026-2034 年) 全地形車(ATV)市場:按類型、驅動方式、動力來源、引擎排氣量、乘客容量、變速箱類型、銷售管道和應用分類-2026-2032年全球市場預測

全地形車(ATV)市場:按類型、驅動方式、動力來源、引擎排氣量、乘客容量、變速箱類型、銷售管道和應用分類-2026-2032年全球市場預測 全球全地形車(ATV)市場:按類型、驅動方式、燃料類型、電池容量、引擎排氣量、乘客容量、車輪數量、應用和地區分類-預測至2035年

全球全地形車(ATV)市場:按類型、驅動方式、燃料類型、電池容量、引擎排氣量、乘客容量、車輪數量、應用和地區分類-預測至2035年 全球全地形車(ATV)市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全地形車(ATV)市場規模、佔有率、成長及全球產業分析:按類型、應用和地區的洞察,2026-2034年的預測全地形防洪車輛市場按推進系統、車輛類型、應用、終端用戶產業和分銷管道分類,全球預測(2026-2032年)全球全地形車和多用途車市場(按車輪配置、推進方式、車輛類型、引擎排氣量、應用、配銷通路和最終用戶分類)預測,2026-2032年數位驅動系統市場(按馬達類型、齒輪類型、分銷管道、終端用戶產業和車輛類型分類)-全球預測(2026-2032年)

全球全地形車(ATV)市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全地形車(ATV)市場規模、佔有率、成長及全球產業分析:按類型、應用和地區的洞察,2026-2034年的預測全地形防洪車輛市場按推進系統、車輛類型、應用、終端用戶產業和分銷管道分類,全球預測(2026-2032年)全球全地形車和多用途車市場(按車輪配置、推進方式、車輛類型、引擎排氣量、應用、配銷通路和最終用戶分類)預測,2026-2032年數位驅動系統市場(按馬達類型、齒輪類型、分銷管道、終端用戶產業和車輛類型分類)-全球預測(2026-2032年)