|

市場調查報告書

商品編碼

1998733

化合物半導體市場機會、成長要素、產業趨勢分析及2026-2035年預測。Compound Semiconductor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

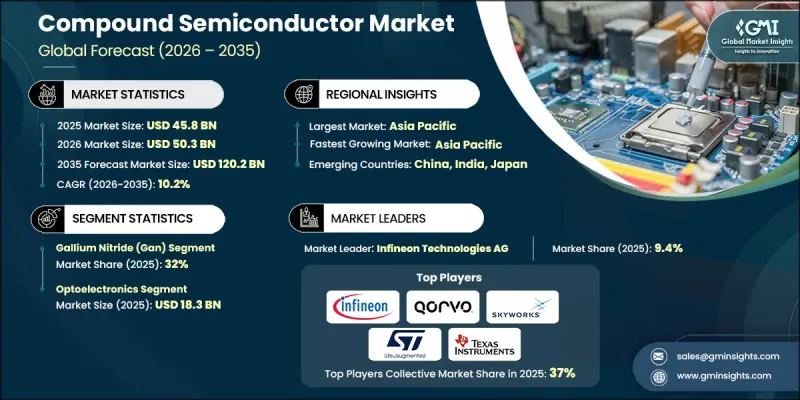

預計到 2025 年,全球化合物半導體市場價值將達到 458 億美元,並預計以 10.2% 的複合年成長率成長,到 2035 年達到 1202 億美元。

市場擴張的驅動力在於對電動車、可再生能源系統以及節能高性能組件日益成長的需求。朝向更小更緊湊的電子設計轉變、5G網路的快速部署以及對先進雷達系統的需求,都在加速化合物半導體的應用。此外,對光電和光電子產品日益成長的需求也推動了各領域的研發。這些材料在高頻和高功率應用中表現出色,因此對現代基礎設施、通訊、汽車和工業能源解決方案至關重要。技術進步、電氣化和網路複雜性的提升,共同促進了全球投資和市場的持續成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 458億美元 |

| 預計金額 | 1202億美元 |

| 複合年成長率 | 10.2% |

預計2026年至2035年間,碳化矽(SiC)市場將以11.1%的複合年成長率成長。碳化矽因其卓越的功率效率、導熱性和高壓性能而備受青睞,使其成為電動車、可再生能源系統和工業電力電子的理想材料。其在高溫高頻環境下的優異性能,進一步鞏固了其作為次世代應用程式關鍵材料的地位。

電力電子領域是成長最快的應用領域,預計2026年至2035年將以12.6%的複合年成長率成長。這一成長主要得益於電動車、工業系統和可再生能源裝置對節能型功率轉換器、逆變器和馬達驅動裝置的需求不斷成長。氮化鎵(GaN)和碳化矽(SiC)半導體能夠提供高功率密度、優異的熱性能和效率,滿足這些對能源效率要求極高的產業永續運作的需求。

預計到2025年,北美化合物半導體市場佔有率將達到22.1%。該地區正快速擴張,主要受通訊、汽車和可再生能源產業的強勁需求驅動。對5G基礎設施的投資、電動車的普及以及清潔能源計畫的推進,都刺激了對高性能半導體的需求。政府支持技術創新的政策,以及主要產業參與者的存在,持續推動市場成長。這些先進材料在能源、交通和連接解決方案中的應用,正使北美成為全球化合物半導體應用的重要貢獻者。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率分析

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 電動汽車和可再生能源

- 小型化和緊湊設計的要求

- 5G網路快速發展

- 對高效雷達解決方案的需求

- 對光電和光電子學的需求不斷成長

- 產業潛在風險與挑戰

- 高昂的生產成本

- 材料供應與供應鏈風險

- 市場機遇

- 航太和國防領域的需求不斷成長

- 可再生能源系統的快速成長

- 促進因素

- 成長潛力分析

- 監理情勢

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 新興經營模式

- 合規要求

- 地緣政治和貿易趨勢

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 主要企業的競爭標竿分析

- 財務績效比較

- 銷售量

- 利潤率

- 研究與發展(R&D)

- 產品系列比較

- 產品線寬度

- 科技

- 創新

- 區域擴張比較

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 小眾玩家

- 財務績效比較

- 主要進展

- 併購

- 夥伴關係和聯盟

- 技術進步

- 業務拓展與投資策略

- 數位轉型計劃

- 新興競爭對手和Start-Ups競爭對手的發展趨勢

第5章 市場估算與預測:依材料類型分類,2022-2035年

- 氮化鎵(GaN)

- 砷化鎵(GaAs)

- 碳化矽(SiC)

- 磷化銦(InP)

- 矽鍺(SiGe)

- 其他

第6章 市場估算與預測:依產品類型分類,2022-2035年

- 電力電子

- 分立元件

- 電源模組

- 裸晶

- 射頻設備

- 功率放大器

- 分立電晶體

- 整合式射頻組件

- 射頻積體電路

- 光電子學

- LED

- 雷射二極體

- 檢測器

- 其他

- 其他

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 溝通

- 車

- 航太/國防

- 工業和電力供應

- 家用電子電器

- 可再生能源

- 資料中心計算

- 其他

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- 主要企業

- Infineon Technologies AG

- Qorvo, Inc.

- Skyworks Solutions, Inc.

- STMicroelectronics NV

- Texas Instruments Incorporated

- Wolfspeed, Inc.

- ams-OSRAM AG

- MACOM Technology Solutions

- 按地區分類的主要企業

- 北美洲

- Navitas Semiconductor

- Power Integrations, Inc.

- Microchip Technology Inc.

- 歐洲

- Renesas Electronics Corporation

- Freiberger Compound Materials GmbH

- Nexperia BV

- 亞太地區

- AXT, Inc.

- Samsung Electronics Co., Ltd.

- Innoscience(Suzhou)Technology Holding Co., Ltd.

- Sumitomo Electric Industries

- 北美洲

- 小眾/顛覆者

- Coherent Corp.

The Global Compound Semiconductor Market was valued at USD 45.8 billion in 2025 and is estimated to grow at a CAGR of 10.2% to reach USD 120.2 billion by 2035.

The market's expansion is driven by rising demand for electric vehicles, renewable energy systems, and energy-efficient high-performance components. The push for smaller, more compact electronic designs, rapid deployment of 5G networks, and the need for advanced radar systems are accelerating the adoption of compound semiconductors. In addition, the growing demand for photonics and optoelectronics products is supporting research and innovation across sectors. These materials provide superior performance in high-frequency and high-power applications, making them essential for modern infrastructure, telecommunications, automotive, and industrial energy solutions. The convergence of technological development, increased electrification, and network densification fuels continued investment and market growth globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $45.8 Billion |

| Forecast Value | $120.2 Billion |

| CAGR | 10.2% |

The silicon carbide (SiC) segment is expected to grow at a CAGR of 11.1% during 2026-2035. SiC is favored for its exceptional power efficiency, thermal conductivity, and high-voltage performance, making it ideal for electric vehicles, renewable energy systems, and industrial power electronics. Its ability to operate under high temperatures and frequencies strengthens its role as a critical material in next-generation applications.

The power electronics segment is the fastest-growing application, growing at a CAGR of 12.6% from 2026 to 2035. This growth is driven by the rising need for energy-efficient power converters, inverters, and electric motor drives in electric vehicles, industrial systems, and renewable energy setups. GaN and SiC semiconductors provide high power density, superior thermal performance, and efficiency required for sustainable operation in these energy-sensitive sectors.

North America Compound Semiconductor Market held 22.1% share in 2025. The region is expanding rapidly due to strong demand from telecommunications, automotive, and renewable energy sectors. Investments in 5G infrastructure, electric vehicle adoption, and clean energy initiatives are fueling the need for high-performance semiconductors. Government programs supporting technology innovation, coupled with the presence of leading industry players, continue to drive market growth. The integration of these advanced materials across energy, mobility, and connectivity solutions positions North America as a major contributor to global compound semiconductor adoption.

Prominent players operating in the Global Compound Semiconductor Market include Wolfspeed, Inc., Infineon Technologies AG, Qorvo, Inc., Skyworks Solutions, Inc., STMicroelectronics N.V., Texas Instruments Incorporated, ams-OSRAM AG, MACOM Technology Solutions, Coherent Corp., Microchip Technology Inc., Renesas Electronics Corporation, Samsung Electronics Co., Ltd., Innoscience (Suzhou) Technology Holding Co., Ltd., Sumitomo Electric Industries, Navitas Semiconductor, Power Integrations, Inc., Nexperia B.V., and Freiberger Compound Materials GmbH. Key strategies adopted by companies in the Global Compound Semiconductor Market focus on strengthening their competitive positioning and global footprint. Firms are heavily investing in R&D to develop next-generation GaN and SiC solutions for high-efficiency power management and high-frequency applications. Strategic partnerships and collaborations with electric vehicle manufacturers, renewable energy companies, and telecom providers enable faster product adoption and tailored solutions. Companies are expanding regional manufacturing capabilities to reduce lead times, improve supply security, and meet growing global demand. They are also emphasizing sustainability by developing energy-efficient, low-loss semiconductor solutions. Targeted marketing, intellectual property protection, and advanced quality assurance protocols are employed to enhance brand reliability, establish long-term client relationships, and maintain a strong market presence.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Material type trends

- 2.2.2 Product type trends

- 2.2.3 Application trends

- 2.2.4 Regional trends

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Electric vehicles and renewable energy

- 3.2.1.2 Miniaturization and compact design requirements

- 3.2.1.3 Rapid development of 5G networks

- 3.2.1.4 Demand for high-efficiency radar solutions

- 3.2.1.5 Growing photonics and optoelectronics demand

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production costs

- 3.2.2.2 Material availability and supply chain risks

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand in aerospace and defense

- 3.2.3.2 Surge in renewable energy systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging Business Models

- 3.9 Compliance Requirements

- 3.10 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Material Type, 2022 - 2035 (USD Billion & Units)

- 5.1 Key trends

- 5.2 Gallium nitride (GaN)

- 5.3 Gallium arsenide (GaAs)

- 5.4 Silicon carbide (SiC)

- 5.5 Indium phosphide (InP)

- 5.6 Silicon germanium (SiGe)

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Billion & Units)

- 6.1 Key trends

- 6.2 Power electronics

- 6.2.1 Discrete devices

- 6.2.2 Power modules

- 6.2.3 Bare die

- 6.3 RF devices

- 6.3.1 Power amplifiers

- 6.3.2 Discrete transistors

- 6.3.3 Integrated RF components

- 6.3.4 RF integrated circuits

- 6.4 Optoelectronics

- 6.4.1 LEDs

- 6.4.2 Laser diodes

- 6.4.3 Photodetectors

- 6.4.4 Others

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion & Units)

- 7.1 Key trends

- 7.2 Telecommunications

- 7.3 Automotive

- 7.4 Aerospace & defense

- 7.5 Industrial & power supply

- 7.6 Consumer electronics

- 7.7 Renewable energy

- 7.8 Data centers & computing

- 7.9 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion & Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Key Players

- 9.1.1 Infineon Technologies AG

- 9.1.2 Qorvo, Inc.

- 9.1.3 Skyworks Solutions, Inc.

- 9.1.4 STMicroelectronics N.V.

- 9.1.5 Texas Instruments Incorporated

- 9.1.6 Wolfspeed, Inc.

- 9.1.7 ams-OSRAM AG

- 9.1.8 MACOM Technology Solutions

- 9.2 Regional Key Players

- 9.2.1 North America

- 9.2.1.1 Navitas Semiconductor

- 9.2.1.2 Power Integrations, Inc.

- 9.2.1.3 Microchip Technology Inc.

- 9.2.2 Europe

- 9.2.2.1 Renesas Electronics Corporation

- 9.2.2.2 Freiberger Compound Materials GmbH

- 9.2.2.3 Nexperia B.V.

- 9.2.3 Asia Pacific

- 9.2.3.1 AXT, Inc.

- 9.2.3.2 Samsung Electronics Co., Ltd.

- 9.2.3.3 Innoscience (Suzhou) Technology Holding Co., Ltd.

- 9.2.3.4 Sumitomo Electric Industries

- 9.2.1 North America

- 9.3 Niche / Disruptors

- 9.3.1 Coherent Corp.

化合物半導體市場-2026-2032年全球市場預測

化合物半導體市場-2026-2032年全球市場預測 磷酸銦化合物半導體市場規模、佔有率和成長分析:按產品類型、晶圓尺寸、裝置類型、應用、最終用戶和地區分類-2026-2033年產業預測

磷酸銦化合物半導體市場規模、佔有率和成長分析:按產品類型、晶圓尺寸、裝置類型、應用、最終用戶和地區分類-2026-2033年產業預測 全球 III-V 族半導體市場預測至 2034 年:按材料類型、產品、沉積技術、晶圓尺寸、應用、最終用戶和地區分類全球化合物半導體市場預測至2034年:依材料、產品類型、晶圓尺寸、製造技術、應用、最終用戶及地區分類碳化矽 (SiC) 半導體裝置市場預測至 2034 年—按裝置類型、晶圓尺寸、電壓範圍、應用、最終用戶和地區分類的全球分析

全球 III-V 族半導體市場預測至 2034 年:按材料類型、產品、沉積技術、晶圓尺寸、應用、最終用戶和地區分類全球化合物半導體市場預測至2034年:依材料、產品類型、晶圓尺寸、製造技術、應用、最終用戶及地區分類碳化矽 (SiC) 半導體裝置市場預測至 2034 年—按裝置類型、晶圓尺寸、電壓範圍、應用、最終用戶和地區分類的全球分析 化合物半導體市場:依產品類型、材料、最終用戶和地區分類。碳化矽組件市場預測至2034年-全球分析(按組件類型、元件類型、電壓範圍、額定功率、應用、最終用戶、通路和地區分類)

化合物半導體市場:依產品類型、材料、最終用戶和地區分類。碳化矽組件市場預測至2034年-全球分析(按組件類型、元件類型、電壓範圍、額定功率、應用、最終用戶、通路和地區分類) 化合物半導體市場規模、佔有率、趨勢和預測:按類型、產品類型、沉積技術、應用和地區分類,2026-2034年系統半導體市場:2026年至2032年全球預測(依產品類型、材料類型、技術、外形規格、連接方式、應用和最終用途產業分類)

化合物半導體市場規模、佔有率、趨勢和預測:按類型、產品類型、沉積技術、應用和地區分類,2026-2034年系統半導體市場:2026年至2032年全球預測(依產品類型、材料類型、技術、外形規格、連接方式、應用和最終用途產業分類) 2026年全球化合物半導體市場報告

2026年全球化合物半導體市場報告