|

市場調查報告書

商品編碼

1998697

PCR塑膠包裝市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測PCR Plastic Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

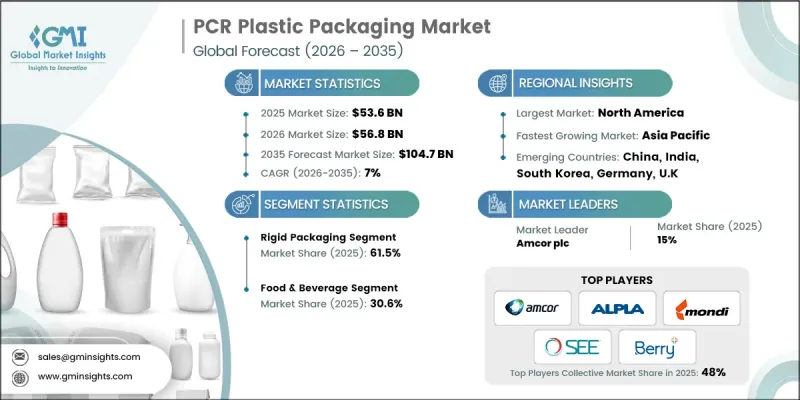

全球消費後回收塑膠包裝市場預計到 2025 年將達到 536 億美元,年複合成長率為 7%,到 2035 年將達到 1,047 億美元。

市場擴張的主要驅動力來自企業對使用再生材料的日益重視、消費者對永續包裝的偏好不斷增強,以及政府對再生材料使用標準制定的強制性法規。對回收基礎設施的投資正在提高消費後再生材料(PCR)的供應量和質量,從而支持全球供應鏈。各大品牌正採用更輕的PCR包裝形式,以在實現永續性目標的同時減少材料消耗。預計這一趨勢將從2021年左右開始加速,並持續到2032年。這種轉變不僅將提高包裝效率並減少運輸過程中的排放,還將強化循環包裝策略,使企業能夠實現其環境目標,並吸引具有環保意識的消費者。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 536億美元 |

| 預測金額 | 1047億美元 |

| 複合年成長率 | 7% |

到2025年,硬質包裝市佔率將達到61.5%。硬質包裝之所以佔據市場主導地位,是因為其廣泛應用於食品、飲料、個人護理和家居用品的瓶、罐、容器和瓶蓋等領域。其結構強度和耐用性使其成為使用再生塑膠(如rPET和rHDPE)的理想選擇。快速消費品品牌的高需求以及其易於操作和填充的特性,也鞏固了該細分市場的主導地位。

預計2026年至2035年間,再生聚丙烯(rPP)市場將以9.3%的複合年成長率成長。推動市場需求成長的主要因素是容器、瓶蓋、封口和化妝品等產品中對永續包裝的需求不斷成長。 rPP具有優異的耐化學性和耐熱性,使其適用於廣泛的應用領域。分類和回收製程的進步正在提高rPP的品質和供應量,從而鼓勵製造商在其包裝解決方案中擴大rPP的使用範圍。

預計到2025年,北美消費後回收塑膠(PCR)包裝市佔率將達38.3%。該地區市場成長的驅動力主要來自對再生材料使用的嚴格監管、企業永續發展計畫以及對循環經濟的承諾。政府政策和與品牌回收商的合作確保了高品質再生塑膠的穩定供應。先進的回收基礎設施、消費者對永續包裝日益增強的意識以及對創新回收技術的持續投資,進一步推動了食品、飲料和消費品行業市場的穩步擴張。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 快速消費品品牌關於使用回收材料的舉措

- 政府對再生塑膠含量最低標準的強制性規定。

- 消費者對永續包裝材料的偏好日益成長

- 擴大先進塑膠回收再利用基礎設施

- 食品、個人護理和家居包裝需求成長

- 產業潛在風險與挑戰

- 供不應求

- 加工成本高於原生塑膠

- 市場機遇

- 利用化學回收法製備高純度PCR樹脂

- 品牌與回收商之間的閉合迴路回收合作關係

- 促進因素

- 成長潛力分析

- 監理情勢

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 定價策略

- 新興經營模式

- 合規要求

- 專利和智慧財產權分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 市場集中度分析

- 主要企業的競爭標竿分析

- 財務績效比較

- 銷售量

- 利潤率

- 研究與發展(R&D)

- 產品系列比較

- 產品線寬度

- 科技

- 創新

- 區域擴張比較

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 小眾玩家

- 戰略展望矩陣

- 財務績效比較

- 主要進展

- 併購

- 夥伴關係與合作

- 技術進步

- 業務拓展與投資策略

- 數位轉型計劃

- 新興/Start-Ups競爭對手的發展趨勢

第5章 市場估價與預測:依包裝產品類型分類,2022-2035年

- 硬包裝

- 瓶子

- 容器/瓶子

- 托盤泡殼

- 蓋子和閉合部件

- 其他

- 軟包裝

- 薄膜包裝

- 收納袋

- 其他

第6章 市場估算與預測:依材料類型分類,2022-2035年

- 再生聚對苯二甲酸乙二酯(rPET)

- 再生高密度聚苯乙烯(rHDPE)

- 再生聚丙烯(rPP)

- 再生低密度聚乙烯(rLDPE)

- 其他

第7章 市場估計與預測:依最終用途產業分類,2022-2035年

- 食品/飲料

- 個人護理和化妝品

- 醫療保健和製藥

- 家居用品

- 工業/消費品

- 其他

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- 主要企業

- Amcor plc

- Berry Global Inc.

- Sealed Air Corporation

- ALPLA Group

- Mondi

- 按地區分類的主要企業

- 北美洲

- Glenroy, Inc

- Evergreen Resources

- Prompac

- Winpak LTD

- 亞太地區

- Cambrian Packaging

- PTT Global Chemical Public Company Limited

- Sanle Plastic

- Udinc

- 歐洲

- Longdapac

- RED PACK

- Regent Plast Private Limited

- 北美洲

- 特殊玩家/干擾者

- 3plastics

The Global PCR Plastic Packaging Market was valued at USD 53.6 billion in 2025 and is estimated to grow at a CAGR of 7% to reach USD 104.7 billion in 2035.

Market expansion is primarily driven by increasing corporate commitments to incorporate recycled content, rising consumer preference for sustainable packaging, and government regulations mandating minimum recycled content usage. Investments in recycling infrastructure are enhancing the availability and quality of PCR materials, supporting supply chains globally. Brands are adopting lightweight PCR packaging formats to reduce material consumption while maintaining sustainability goals, a trend that accelerated around 2021 and is expected to continue through 2032. This shift not only improves packaging efficiency and lowers transportation emissions but also strengthens circular packaging strategies, enabling companies to meet environmental targets and appeal to eco-conscious consumers.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $53.6 Billion |

| Forecast Value | $104.7 Billion |

| CAGR | 7% |

The rigid packaging segment held a 61.5% share in 2025. Rigid formats dominate due to their extensive use in bottles, jars, containers, and caps across food, beverage, personal care, and household products. Their structural strength and durability make them ideal for integrating recycled plastics such as rPET and rHDPE. High demand from FMCG brands and the convenience of handling and filling contribute to the segment's market leadership.

The recycled polypropylene (rPP) segment is anticipated to grow at a CAGR of 9.3% during 2026-2035. Rising adoption of sustainable packaging in containers, caps, closures, and cosmetics is boosting demand. rPP offers excellent chemical resistance and heat tolerance, making it suitable for diverse applications. Advances in sorting and recycling processes are improving the quality and availability of rPP, encouraging manufacturers to expand its use across packaging solutions.

North America PCR Plastic Packaging Market held a 38.3% share in 2025. Market growth in the region is fueled by strong regulatory mandates on recycled content, corporate sustainability programs, and circular economy initiatives. Government policies, coupled with brand-recycler collaborations, ensure a reliable supply of high-quality recycled resins. Advanced recycling infrastructure, increasing consumer awareness of sustainable packaging, and ongoing investment in innovative recycling technologies further support the market's steady expansion across food, beverage, and consumer goods sectors.

Key players in the Global PCR Plastic Packaging Market include 3plastics, ALPLA Group, Amcor plc, Berry Global Inc., Cambrian Packaging, Evergreen Resources, Glenroy, Inc., Longdapac, Mondi, PTT Global Chemical Public Company Limited, Prompac, RED PACK, Regent Plast Private Limited, Sanle Plastic, Sealed Air Corporation, Udinc, and Winpak LTD.

Companies in the PCR Plastic Packaging Market are pursuing strategies to solidify their presence and expand market share. They are investing in advanced recycling and material processing technologies to ensure high-quality PCR content. Product innovation, such as lightweight packaging and customizable formats, allows brands to meet both sustainability goals and consumer expectations. Strategic partnerships with FMCG brands and recyclers strengthen supply chains, ensuring consistent PCR availability. Market expansion into emerging regions, coupled with capacity upgrades and automation, enhances production efficiency. Firms are also leveraging branding and marketing campaigns to highlight sustainable credentials, supporting premium positioning while complying with global regulations on recycled content.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Packaging product type trends

- 2.2.2 Material type trends

- 2.2.3 End-use industry trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Corporate recycled-content commitments by FMCG brands

- 3.2.1.2 Government mandates on minimum recycled plastic content

- 3.2.1.3 Rising consumer preference for sustainable packaging materials

- 3.2.1.4 Expansion of advanced plastic recycling infrastructure

- 3.2.1.5 Growth in food, personal care, and household packaging demand

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited supply of food-grade PCR resins

- 3.2.2.2 Higher processing costs than virgin plastics

- 3.2.3 Market opportunities

- 3.2.3.1 Chemical recycling enabling high-purity PCR resins

- 3.2.3.2 Closed-loop recycling partnerships between brands and recyclers

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Packaging Product Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Rigid packaging

- 5.2.1 Bottles

- 5.2.2 Containers & jars

- 5.2.3 Trays & clamshells

- 5.2.4 Caps & closures

- 5.2.5 Others

- 5.3 Flexible packaging

- 5.3.1 Films & wraps

- 5.3.2 Pouches & bags

- 5.3.3 Others

Chapter 6 Market Estimates and Forecast, By Material Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Recycled polyethylene terephthalate (rPET)

- 6.3 Recycled high-density polyethylene (rHDPE)

- 6.4 Recycled polypropylene (rPP)

- 6.5 Recycled low-density polyethylene (rLDPE)

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By End-Use Industry, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Food & beverage

- 7.3 Personal care & cosmetics

- 7.4 Healthcare & pharmaceuticals

- 7.5 Household products

- 7.6 Industrial & consumer goods

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Key Players

- 9.1.1 Amcor plc

- 9.1.2 Berry Global Inc.

- 9.1.3 Sealed Air Corporation

- 9.1.4 ALPLA Group

- 9.1.5 Mondi

- 9.2 Regional key players

- 9.2.1 North America

- 9.2.1.1 Glenroy, Inc

- 9.2.1.2 Evergreen Resources

- 9.2.1.3 Prompac

- 9.2.1.4 Winpak LTD

- 9.2.2 Asia Pacific

- 9.2.2.1 Cambrian Packaging

- 9.2.2.2 PTT Global Chemical Public Company Limited

- 9.2.2.3 Sanle Plastic

- 9.2.2.4 Udinc

- 9.2.3 Europe

- 9.2.3.1 Longdapac

- 9.2.3.2 RED PACK

- 9.2.3.3 Regent Plast Private Limited

- 9.2.1 North America

- 9.3 Niche Players/Disruptors

- 9.3.1 3plastics

塑膠包裝市場:2026-2032年全球市場預測(按包裝類型、包裝材料、製造技術、包裝形式和最終用途行業分類)

塑膠包裝市場:2026-2032年全球市場預測(按包裝類型、包裝材料、製造技術、包裝形式和最終用途行業分類) 2026年全球塑膠包裝市場報告2026年全球瓦楞塑膠包裝市場報告

2026年全球塑膠包裝市場報告2026年全球瓦楞塑膠包裝市場報告 再生塑膠(PCR)包裝市場預測至2034年-按產品、材料、最終用戶和地區分類的全球分析塑膠瓦楞包裝市場預測至2034年-按包裝類型、材料類型、最終用戶和地區分類的全球分析

再生塑膠(PCR)包裝市場預測至2034年-按產品、材料、最終用戶和地區分類的全球分析塑膠瓦楞包裝市場預測至2034年-按包裝類型、材料類型、最終用戶和地區分類的全球分析 塑膠包裝市場:按產品類型、最終用途行業和地區分類

塑膠包裝市場:按產品類型、最終用途行業和地區分類 醫療設備和植入用高純度塑膠市場規模、佔有率和成長分析:按產品、應用和地區分類-產業預測(2026-2033 年)

醫療設備和植入用高純度塑膠市場規模、佔有率和成長分析:按產品、應用和地區分類-產業預測(2026-2033 年) 塑膠包裝市場規模、佔有率和趨勢分析報告:按材料、產品、技術、應用、地區和細分市場分類(2026-2033 年)散裝聚苯乙烯包裝市場:按應用和地區分類

塑膠包裝市場規模、佔有率和趨勢分析報告:按材料、產品、技術、應用、地區和細分市場分類(2026-2033 年)散裝聚苯乙烯包裝市場:按應用和地區分類 塑膠包裝市場分析及預測(至2035年):依類型、產品類型、應用、材料類型、技術、最終用戶、功能及工藝分類

塑膠包裝市場分析及預測(至2035年):依類型、產品類型、應用、材料類型、技術、最終用戶、功能及工藝分類