|

市場調查報告書

商品編碼

1998687

電池溫度控管系統市場機會、成長要素、產業趨勢分析及2026-2035年預測Battery Thermal Management System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

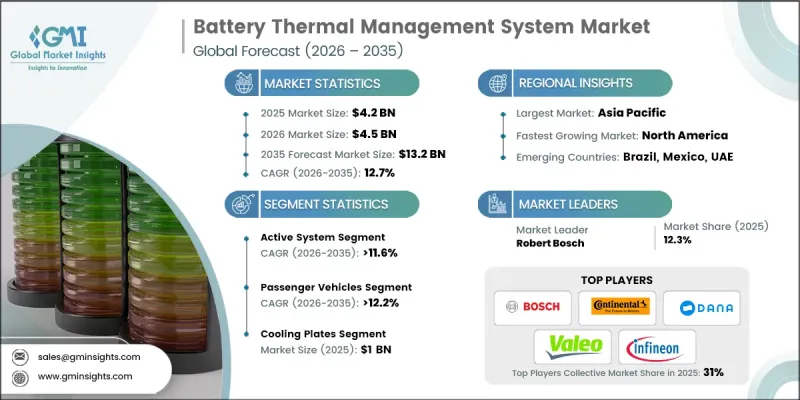

全球電池溫度控管系統市場預計到 2025 年將價值 42 億美元,預計到 2035 年將以 12.7% 的複合年成長率成長至 132 億美元。

受電動車普及率不斷提高、對先進電池儲能技術的需求日益成長、電池運行安全標準日益嚴格以及可再生能源基礎設施快速發展的推動,電池溫度控管系統行業正在蓬勃發展。汽車製造商、電池開發商和儲能供應商正大力投資先進的溫度控管解決方案,以提升電池性能、延長運作並確保安全運作。電動車的快速普及、大規模電池儲能設施的部署以及高容量電池組的廣泛應用,進一步提升了對高效溫度控管技術的需求。隨著電池容量和功率密度的提升,維持穩定的動作溫度對於防止電池劣化和確保可靠的能量輸出至關重要。因此,先進的電池溫度控管系統正成為現代儲能和電動車生態系統中不可或缺的一部分。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 42億美元 |

| 預計金額 | 132億美元 |

| 複合年成長率 | 12.7% |

高性能電池系統對溫度穩定性的需求日益成長,推動了各行各業對更先進的溫度控管技術的應用。製造商和系統整合商越來越關注能夠有效散熱、降低過熱風險並提高能源效率的解決方案。現代電池溫度控管系統融合了即時溫度監控、智慧冷卻機制和先進材料等功能,旨在控制熱環境。改進的冷卻架構、智慧監控平台和整合電池控制技術等最新趨勢正在革新傳統的電池管理方法,同時提升運作安全性和可靠性。

到2025年,主動冷卻系統市佔率將達到47%,預計2026年至2035年將以11.6%的複合年成長率成長。該細分市場在主動維持電池最佳溫度方面發揮著至關重要的作用,而電池溫度直接影響電池的安全性、效率和運作。隨著高容量鋰離子電池和新一代電池技術在電動車和能源儲存系統中的日益普及,主動冷卻技術對於維持電池性能的穩定性至關重要。這些系統能夠持續控制溫度並提高能源效率,這對於確保電池在全球各種應用中的穩定運作至關重要。

預計到2025年,乘用車市佔率將達到76%,並有望在2026年至2035年間以12.2%的複合年成長率成長。該細分市場的強勁表現主要得益於全球電動和混合動力乘用車產量和普及率的不斷提高。消費者和製造商都將提升電池效率、延長電池壽命、增強熱穩定性以及確保車輛性能的穩定性作為首要目標。因此,先進的電池溫度控管技術正被廣泛應用於乘用車,以維持電池的最佳工作狀態並確保車輛的可靠運作。各類車輛整合電池溫度控管系統的日益標準化,進一步鞏固了該細分市場在全球市場的主導地位。

中國電池溫度控管系統市場佔55%的全球佔有率,預計2025年市場規模將達到11.088億美元。憑藉強大的電動車製造生態系統和完善的電池供應鏈基礎設施,中國在電池溫度控管系統產業中扮演著至關重要的角色。主要汽車製造商和電池供應商的存在,正在加速該地區先進溫度控管解決方案的開發和應用。汽車製造商與技術供應商之間的緊密合作,確保了電池安全性、運作效率和長期性能的持續提升,同時滿足嚴格的能源效率和安全法規要求。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 電動車的廣泛普及

- 高容量電池組

- 法規和安全標準

- 技術進步

- 產業潛在風險與挑戰

- 初始成本高

- 整合的複雜性

- 市場機遇

- 商用電動車和車隊電氣化

- 儲能與可再生能源的融合

- 下一代電池技術

- 與人工智慧和物聯網的整合

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 美國:EPA、CARB、NHTSA 標準

- 加拿大:加拿大運輸部,CMVSS 305

- 歐洲

- 德國:BMDV,歐洲 6/7

- 法國:運輸部,6/7歐元

- 英國:運輸部,Euro 6/7

- 義大利:基礎設施和運輸部關於電動車電池合規性

- 亞太地區

- 中國:工信部、中國 6/7 標準

- 日本:國土交通省,JIS標準

- 韓國:國土交通省制定KS排放標準

- 印度:MoRTH,BS6標準

- 拉丁美洲

- 巴西:DENATRAN、CONAMA 標準

- 墨西哥:通訊與運輸部

- 中東和非洲

- 阿拉伯聯合大公國:RTA 和 ESMA 法規

- 沙烏地阿拉伯:運輸部,SASO

- 北美洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格分析(基於初步調查)

- 對過去價格趨勢的分析

- 按球員類型分類的定價策略(高階/超值/成本加成)

- 區域價格波動分析

- 成本細分分析

- 專利趨勢(基於初步調查)

- 人工智慧(AI)的影響

- 利用人工智慧改造現有經營模式

- 人工智慧在預測性維護和車隊電池管理的應用

- BTMS設計的自動化最佳化

- 用於零件需求預測的供應鏈人工智慧

- GenAI 各細分市場的應用案例與實施藍圖

- 熱模組設計生成

- 電池效能最佳化

- 客戶服務聊天機器人和技術支援

- 行銷內容創作

- 風險、限制和監管考量

- 物聯網賦能的BTMS中的資料隱私

- 人工智慧演算法的透明度要求

- 人工智慧驅動的產品故障責任

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 碳足跡考量

- 使用案例場景

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃及資金籌措

第5章 市場估價與預測:依冷卻方式分類,2022-2035年

- 主動系統

- 液冷系統

- 冷媒冷卻系統

- 熱電冷卻系統

- 被動系統

- 空氣冷卻系統

- 基於散熱器的系統

- 自然對流系統

- 混合系統

- 活性液體和被動相變材料的整合

- 空氣+液體混合系統

- 多模態自適應系統

第6章 市場估計與預測:依組件分類,2022-2035年

- 冷卻板

- 熱交換器

- 泵浦和壓縮機

- 風扇和鼓風機

- 溫度感測器

- 熱界面材料

- 其他

第7章 市場估價與預測:依車輛類型分類,2022-2035年

- 搭乘用車

- 掀背車

- 轎車

- SUV

- 商用車輛

- 輕型商用車(LCV)

- 中型商用車(MCV)

- 重型商用車(HCV)

第8章 市場估計與預測:依電池類型分類,2022-2035年

- 鋰離子電池

- 鎳氫(NiMH)電池

- 鉛酸電池

- 全固態電池

第9章 市場估計與預測:依促進因素分類,2022-2035年

- 電池式電動車(BEV)

- 插電式混合動力汽車(PHEV)

- 混合動力電動車(HEV)

第10章 市場估價與預測:依電池容量分類,2022-2035年

- 小於100度

- 100~200kWh

- 200~500kWh

- 超過500度

第11章 市場估價與預測:按地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 比利時

- 荷蘭

- 瑞典

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 新加坡

- 韓國

- 越南

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲(MEA)

- 阿拉伯聯合大公國

- 南非

- 沙烏地阿拉伯

第12章:公司簡介

- Global Player

- BorgWarner

- Continental

- Dana

- Denso

- Hanon Systems

- Hitachi Astemo

- Infineon Technologies

- MAHLE

- Robert Bosch

- Valeo

- Regional Player

- Aisin Seiki

- Borgers

- Calsonic Kansei(KKC)

- GKN Automotive

- Inalfa Roof Systems

- Magna International

- Modine Manufacturing

- Nidec

- Thermo King

- Webasto

The Global Battery Thermal Management System Market was valued at USD 4.2 billion in 2025 and is estimated to grow at a CAGR of 12.7% to reach USD 13.2 billion by 2035.

Expansion within the battery thermal management system industry is supported by the growing adoption of electric vehicles, increasing demand for advanced battery storage technologies, strict safety standards for battery operation, and the rapid development of renewable energy infrastructure. Automotive manufacturers, battery developers, and energy storage providers are investing heavily in advanced thermal management solutions to improve battery performance, extend operational lifespan, and ensure safe functionality. The rapid expansion of electric mobility, large-scale battery storage installations, and high-capacity battery packs is further strengthening demand for efficient thermal management technologies. As battery capacity increases and power density rises, maintaining stable operating temperatures becomes critical for preventing degradation and ensuring reliable energy output. Consequently, advanced battery thermal management systems are becoming essential components in modern energy storage and electric mobility ecosystems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.2 Billion |

| Forecast Value | $13.2 Billion |

| CAGR | 12.7% |

The growing need to maintain temperature stability in high-performance battery systems is encouraging the deployment of more advanced thermal management technologies across multiple industries. Manufacturers and system integrators are increasingly focusing on solutions that enable efficient heat dissipation, reduce overheating risks, and enhance energy efficiency. Modern battery thermal management systems incorporate features such as real-time temperature monitoring, intelligent cooling mechanisms, and advanced materials designed to regulate thermal conditions. Recent technological developments, including improved cooling architectures, intelligent monitoring platforms, and integrated battery control technologies, are reshaping conventional battery management approaches while enhancing operational safety and reliability.

The active system segment held a 47% share in 2025, and it is expected to grow at a CAGR of 11.6% between 2026 and 2035. This segment plays a vital role in actively maintaining optimal battery temperatures, which directly influences battery safety, efficiency, and operational lifespan. With the increasing use of high-capacity lithium-ion and next-generation battery technologies in electric mobility and energy storage systems, active cooling approaches have become essential for maintaining consistent performance. These systems provide continuous temperature regulation and improve energy efficiency, which is critical for ensuring stable battery operation across various applications worldwide.

The passenger vehicles segment held 76% share in 2025, and it is estimated to grow at a CAGR of 12.2% during 2026-2035. The strong performance of this segment is largely attributed to the increasing production and adoption of electric and hybrid passenger vehicles globally. Consumers and manufacturers are prioritizing improved battery efficiency, longer battery lifespan, enhanced thermal stability, and consistent vehicle performance. As a result, advanced battery thermal management technologies are being widely integrated into passenger vehicles to maintain optimal battery operating conditions and support reliable vehicle operation. Increasing standardization of integrated battery thermal management systems across different vehicle categories is further strengthening the leadership of this segment across global markets.

China Battery Thermal Management System Market held a 55% share, generating USD 1,108.8 million in 2025. The country plays a significant role in the battery thermal management system industry due to its strong electric vehicle manufacturing ecosystem and well-established battery supply chain infrastructure. The presence of major automotive manufacturers and battery suppliers has accelerated the development and deployment of advanced thermal management solutions within the region. Close collaboration between automotive companies and technology providers continues to support improvements in battery safety, operational efficiency, and long-term performance while ensuring compliance with strict energy efficiency and safety regulations.

Major companies operating in the Global Battery Thermal Management System Market include Robert Bosch, Continental, BorgWarner, Denso, Valeo, Dana, MAHLE, Hanon Systems, Infineon Technologies, and Hitachi Astemo. Companies participating in the Global Battery Thermal Management System Market are implementing a range of strategic initiatives to strengthen their competitive position and expand their market presence. Leading manufacturers are investing significantly in research and development to introduce advanced thermal management technologies that improve energy efficiency and battery performance. Many companies are also forming strategic partnerships with automotive manufacturers and energy storage providers to accelerate the development of integrated battery solutions. Expanding production capacity and strengthening global supply chains are key priorities to meet growing demand from the electric mobility sector. Additionally, organizations are focusing on integrating intelligent monitoring systems and advanced cooling technologies into their product portfolios. Continuous innovation, strategic collaborations, and the development of next-generation battery management technologies are helping companies reinforce their foothold in the global battery thermal management system market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Cooling method

- 2.2.3 Component

- 2.2.4 Vehicle

- 2.2.5 Battery

- 2.2.6 Propulsion

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising EV Adoption

- 3.2.1.2 High-Capacity Battery Packs

- 3.2.1.3 Regulatory & Safety Standards

- 3.2.1.4 Technological Advancements

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Initial Cost

- 3.2.2.2 Integration Complexity

- 3.2.3 Market opportunities

- 3.2.3.1 Commercial EV & Fleet Electrification

- 3.2.3.2 Energy Storage & Renewable Integration

- 3.2.3.3 Next-Generation Battery Technologies

- 3.2.3.4 Integration with AI and IoT

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S.: EPA, CARB, NHTSA Standards

- 3.4.1.2 Canada: Transport Canada, CMVSS 305

- 3.4.2 Europe

- 3.4.2.1 Germany: BMDV, Euro 6/7

- 3.4.2.2 France: Ministry of Transport, Euro 6/7

- 3.4.2.3 UK: Department for Transport, Euro 6/7

- 3.4.2.4 Italy: Ministry of Infrastructure & Transport, EV Battery Compliance

- 3.4.3 Asia Pacific

- 3.4.3.1 China: MIIT, China 6/7 Standards

- 3.4.3.2 Japan: MLIT, JIS Regulations

- 3.4.3.3 South Korea: MOLIT, KS Emission Standards

- 3.4.3.4 India: MoRTH, BS6 Norms

- 3.4.4 Latin America

- 3.4.4.1 Brazil: DENATRAN, CONAMA Standards

- 3.4.4.2 Mexico: Ministry of Communications & Transport

- 3.4.5 Middle East and Africa

- 3.4.5.1 UAE: RTA, ESMA Regulations

- 3.4.5.2 Saudi Arabia: Ministry of Transport, SASO

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation Landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Pricing analysis (Driven by Primary Research)

- 3.8.1 Historical Price Trend Analysis

- 3.8.2 Pricing Strategy by Player Type (Premium / Value / Cost-Plus)

- 3.8.3 Regional Price Variation Analysis

- 3.9 Cost breakdown analysis

- 3.10 Patent landscape (Driven by Primary Research)

- 3.11 Impact of Artificial Intelligence (AI)

- 3.11.1 AI-driven disruption of existing business models

- 3.11.2 Predictive maintenance & fleet battery management AI

- 3.11.3 Automated BTMS design optimization

- 3.11.4 Supply chain AI for component demand forecasting

- 3.11.5 GenAI use cases & adoption roadmap by segment

- 3.11.5.1 Thermal module design generation

- 3.11.5.2 Battery performance optimization

- 3.11.5.3 Customer service chatbots & technical support

- 3.11.5.4 Marketing content creation

- 3.11.6 Risks, limitations & regulatory considerations

- 3.11.6.1 Data privacy in IoT-enabled BTMS

- 3.11.6.2 AI algorithm transparency requirements

- 3.11.6.3 Liability in AI-driven product failures

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Use case scenarios

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Cooling Method, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Active system

- 5.2.1 Liquid Cooling Systems

- 5.2.2 Refrigerant-Based Cooling Systems

- 5.2.3 Thermoelectric Cooling Systems

- 5.3 Passive system

- 5.3.1 Air Cooling Systems

- 5.3.2 Heat Sink-Based Systems

- 5.3.3 Natural Convection Systems

- 5.4 Hybrid system

- 5.4.1 Active Liquid + Passive PCM Integration

- 5.4.2 Air + Liquid Hybrid Systems

- 5.4.3 Multi-Mode Adaptive Systems

Chapter 6 Market Estimates & Forecast, By Component, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Cooling Plates

- 6.3 Heat Exchangers

- 6.4 Pumps & Compressors

- 6.5 Fans & Blowers

- 6.6 Thermal Sensors

- 6.7 Thermal Interface Materials

- 6.8 Others

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger vehicles

- 7.2.1 Hatchbacks

- 7.2.2 Sedans

- 7.2.3 SUV

- 7.3 Commercial vehicles

- 7.3.1 Light commercial vehicles (LCV)

- 7.3.2 Medium commercial vehicles (MCV)

- 7.3.3 Heavy commercial vehicles (HCV)

Chapter 8 Market Estimates & Forecast, By Battery, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Lithium-ion battery

- 8.3 Nickel-Metal Hydride (NiMH) battery

- 8.4 Lead-acid battery

- 8.5 Solid-state battery

Chapter 9 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 Battery Electric Vehicles (BEVs)

- 9.3 Plug-in Hybrid Electric Vehicles (PHEVs)

- 9.4 Hybrid Electric Vehicles (HEVs)

Chapter 10 Market Estimates & Forecast, By Battery Capacity, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 <100 KWH

- 10.3 100-200 KWH

- 10.4 200-500 KWH

- 10.5 >500 KWH

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Belgium

- 11.3.7 Netherlands

- 11.3.8 Sweden

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 Singapore

- 11.4.6 South Korea

- 11.4.7 Vietnam

- 11.4.8 Indonesia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 South Africa

- 11.6.3 Saudi Arabia

Chapter 12 Company Profiles

- 12.1 Global Player

- 12.1.1 BorgWarner

- 12.1.2 Continental

- 12.1.3 Dana

- 12.1.4 Denso

- 12.1.5 Hanon Systems

- 12.1.6 Hitachi Astemo

- 12.1.7 Infineon Technologies

- 12.1.8 MAHLE

- 12.1.9 Robert Bosch

- 12.1.10 Valeo

- 12.2 Regional Player

- 12.2.1 Aisin Seiki

- 12.2.2 Borgers

- 12.2.3 Calsonic Kansei (KKC)

- 12.2.4 GKN Automotive

- 12.2.5 Inalfa Roof Systems

- 12.2.6 Magna International

- 12.2.7 Modine Manufacturing

- 12.2.8 Nidec

- 12.2.9 Thermo King

- 12.2.10 Webasto

電池機殼及溫度控管材料市場預測至2034年-按電池類型、材料類型、功能、應用、最終用戶和地區分類的全球分析

電池機殼及溫度控管材料市場預測至2034年-按電池類型、材料類型、功能、應用、最終用戶和地區分類的全球分析 汽車電池溫度控管系統市場:依產品類型、冷卻方式、安裝等級及最終用戶分類-2026-2032年全球市場預測

汽車電池溫度控管系統市場:依產品類型、冷卻方式、安裝等級及最終用戶分類-2026-2032年全球市場預測 汽車電池溫度控管系統市場分析及至2035年的預測:按類型、產品、技術、組件、應用、材料類型、最終用戶、功能和安裝類型分類電池溫度控管市場預測至2034年—按系統類型、組件、技術、應用、最終用戶和地區分類的全球分析

汽車電池溫度控管系統市場分析及至2035年的預測:按類型、產品、技術、組件、應用、材料類型、最終用戶、功能和安裝類型分類電池溫度控管市場預測至2034年—按系統類型、組件、技術、應用、最終用戶和地區分類的全球分析 2026年全球汽車電池溫度控管系統市場報告電池溫度控管系統市場:全球市場預測(按應用、冷卻技術、電池化學成分和系統類型分類),2026年至2032年新能源汽車電子水閥市場按推進類型、車輛類型、應用、材料和銷售管道,全球預測(2026-2032年)

2026年全球汽車電池溫度控管系統市場報告電池溫度控管系統市場:全球市場預測(按應用、冷卻技術、電池化學成分和系統類型分類),2026年至2032年新能源汽車電子水閥市場按推進類型、車輛類型、應用、材料和銷售管道,全球預測(2026-2032年) 全球電動車電池溫度控管系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球電動車電池溫度控管系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 汽車電池溫度控管系統市場 - 全球產業規模、佔有率、趨勢、機會及預測(按車輛類型、技術、電池類型、電池容量、動力系統、地區和競爭格局分類),2021-2031年新能源汽車空調壓縮機市場:按壓縮機類型、車輛類型、冷凍方式、銷售管道和應用分類-2026-2032年全球預測

汽車電池溫度控管系統市場 - 全球產業規模、佔有率、趨勢、機會及預測(按車輛類型、技術、電池類型、電池容量、動力系統、地區和競爭格局分類),2021-2031年新能源汽車空調壓縮機市場:按壓縮機類型、車輛類型、冷凍方式、銷售管道和應用分類-2026-2032年全球預測