|

市場調查報告書

商品編碼

1936514

工業焚化市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)Industrial Burner on Incineration Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

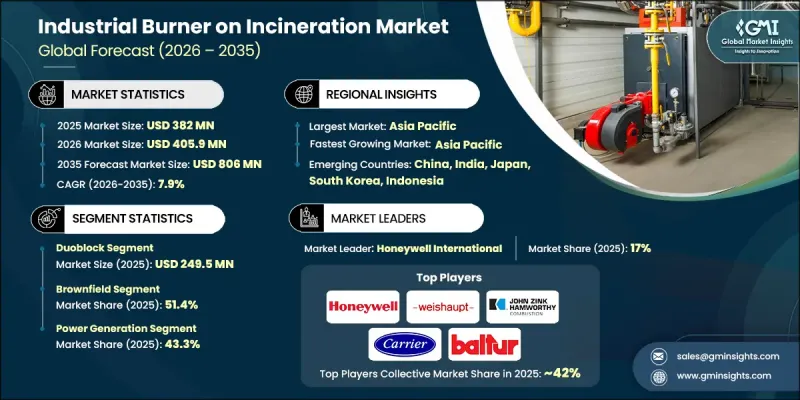

全球工業焚化市場預計到 2025 年將達到 3.82 億美元,到 2035 年將達到 8.06 億美元,年複合成長率為 7.9%。

市場成長的驅動力廢棄物化學、醫療和製造業等行業產生的危險廢棄物和工業廢棄物的增加,這些廢棄物需要可靠且合規的處置方法。焚燒系統中的工業燃燒器對於符合法規和環境保護至關重要,因為它們能夠確保有毒化合物的完全運作並最大限度地減少有害排放。由於廢棄物產生量的增加,廢棄物的運作時間也隨之延長,因此對能夠精確維持最佳溫度的耐用高效能燃燒器系統的需求日益成長。現代燃燒器能夠更好地控制燃燒過程,從而提高安全性、運作可靠性和排放效率。廢棄物管理設施營運商正加大對先進燃燒器解決方案的投資,以實現經濟高效且可靠的性能,同時滿足監管標準。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始金額 | 3.82億美元 |

| 預測金額 | 8.06億美元 |

| 複合年成長率 | 7.9% |

雙塊燃燒器市場預計到2025年將達到2.495億美元,並在2035年之前以7.4%的複合年成長率成長。雙塊燃燒器將燃燒器和風扇整合於一體,確保了精確的空燃混合、穩定的火焰控制和高效的燃燒。其緊湊的結構簡化了安裝和維護,使其成為工業焚燒爐、危險廢棄物處理設施和垃圾焚化發電發電廠的理想選擇。工業廢棄物的不斷成長以及對符合環保法規的節能解決方案日益成長的需求,正在推動雙塊燃燒器在各個地區的普及應用。

2025年,發電領域佔了43.3%的市場佔有率,預計2026年至2035年將以7.9%的複合年成長率成長。燃燒器在火力發電廠和垃圾焚化發電發電廠中至關重要,它能確保穩定的火焰性能、高效的熱能產生和最小化的排放氣體。不斷成長的電力需求、可再生和替代能源計劃的擴展以及嚴格的環境法規正在推動高性能燃燒器的應用。在高熱負載下持續可靠運作的需求使得工業燃燒器成為能源生產的關鍵,進一步鞏固了發電領域的領先地位。

中國工業焚化爐市場預計到2025年將達到5,090萬美元,2026年至2035年複合年成長率將達8.3%。快速的工業化進程、不斷成長的城市垃圾和危險廢棄物,以及廢棄物焚化發電廠和化工廠的擴張,正在推動對大容量焚燒爐的需求。政府推行的排放控制和高效廢棄物管理政策也進一步促進了市場滲透。工業領域需要可靠、高性能且能夠在連續運作條件下處理多種燃料的焚化爐。都市化和不斷完善的城市廢棄物基礎設施也為中國市場的持續成長做出了貢獻。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段的附加價值

- 影響價值鏈的因素

- 產業影響因素

- 促進要素

- 廢棄物安全處置的危險廢棄物和工業廢棄物日益增多。

- 擴大從工業廢棄物和市政垃圾中回收能源的設施

- 加強有關廢棄物處置和排放的環境法規

- 挑戰與困難

- 先進低排放燃燒器系統的高昂資本成本

- 公眾對焚燒設施的反對和監管審查

- 機會

- 開發超低氮氧化物和高效能燃燒器技術

- 對老舊焚燒爐維修以符合更新法規的需求日益成長

- 促進要素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 監管環境

- 標準和合規要求

- 區域法規結構

- 認證標準

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章 2022年至2035年按燃燒器設計分類的市場估算與預測

- 單體塊

- 雙區塊

第6章 按設備類型分類的市場估算與預測,2022-2035年

- 現有設施

- 新開發項目

第7章 依功率範圍分類的市場估計與預測,2022-2035年

- 小於300千瓦

- 300 kW~1 MW

- 1~5 MW

- 5~20MW

- 20~50MW

- 50兆瓦或以上

第8章 依最終用途產業分類的市場估算與預測,2022-2035年

- 發電

- 化工/石油化工

- 金屬加工

- 食品加工

- 紡織業

- 紙漿和造紙

- 其他

第9章 2022-2035年各地區市場估算與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

第10章:公司簡介

- Alfa Laval

- Babcock Wanson

- Baltur

- Bloom Engineering Company

- Carrier

- Fives Group

- Forbes Marshall Pvt. Ltd.

- Honeywell International

- John Zink Hamworthy Combustion

- Limpsfield Combustion Engineering

- Max Weishaupt

- Miura America Co.

- Oilon Group Oy

- QED Combustion

- Selas Heat Technology Company

The Global Industrial Burner on Incineration Market was valued at USD 382 million in 2025 and is estimated to grow at a CAGR of 7.9% to reach USD 806 million by 2035.

The market growth is driven by rising volumes of hazardous and industrial waste across chemical, healthcare, and manufacturing sectors, which require reliable and compliant disposal methods. Industrial burners in incineration systems ensure complete combustion of toxic compounds and minimize harmful emissions, making them critical for regulatory compliance and environmental protection. As waste generation intensifies, operational hours for incinerators increase, creating demand for durable and efficient burner systems capable of maintaining optimal temperature with precision. Modern burners offer superior control over combustion processes, improving safety, operational reliability, and emission efficiency. Waste management facility operators are increasingly investing in advanced burner solutions to meet regulatory standards while achieving cost-effective and dependable performance.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $382 Million |

| Forecast Value | $806 Million |

| CAGR | 7.9% |

The duoblock burner segment accounted for USD 249.5 million in 2025 and is expected to grow at a CAGR of 7.4% through 2035. Duoblock designs integrate the burner and fan into a single unit, ensuring precise air-fuel mixing, stable flame control, and highly efficient combustion. Their compact construction simplifies installation and maintenance, making them ideal for industrial incinerators, hazardous waste treatment facilities, and waste-to-energy plants. Rising industrial waste volumes and the push for energy-efficient, environmentally compliant solutions are driving the adoption of duoblock burners across regions.

The power generation segment held a 43.3% share in 2025 and is projected to grow at a CAGR of 7.9% from 2026 to 2035. Burners are essential in thermal power plants and waste-to-energy facilities to ensure stable flame performance, efficient heat generation, and minimized emissions. Increasing electricity demand, growth in renewable and alternative energy initiatives, and stringent environmental regulations are fueling the adoption of high-performance burners. The requirement for continuous, reliable operation under high thermal loads makes industrial burners indispensable for energy production, reinforcing the dominance of the power generation segment.

China Industrial Burner on Incineration Market reached USD 50.9 million in 2025 and is expected to grow at a CAGR of 8.3% between 2026 and 2035. Rapid industrialization, increasing municipal and hazardous waste, and expansion of waste-to-energy and chemical plants are driving demand for high-capacity burners. Government policies promoting emission control and efficient waste management further support market adoption. Industrial sectors require burners that are reliable, high-performing, and capable of handling multiple fuel types under continuous operations. Urbanization and growing municipal waste treatment infrastructure also contribute to sustained market growth in China.

Key players in the Global Industrial Burner on Incineration Market include Babcock Wanson, Alfa Laval, Bloom Engineering Company, Selas Heat Technology Company, Carrier, Miura America Co., Fives Group, John Zink Hamworthy Combustion, Limpsfield Combustion Engineering, Honeywell International, Baltur, Forbes Marshall Pvt. Ltd., Max Weishaupt, Oilon Group Oy, and QED Combustion. Companies in the industrial burner on incineration market focus on strategies such as expanding regional distribution networks and increasing manufacturing capacities to meet growing demand. R&D investments enable the development of energy-efficient, low-emission burner systems with enhanced precision and durability. Strategic partnerships and collaborations with waste management operators and energy facilities strengthen market reach. Firms are integrating advanced combustion technologies and automated controls to optimize performance, reduce operational downtime, and comply with regulatory standards.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Burner design

- 2.2.3 Installation

- 2.2.4 Power Range

- 2.2.5 End Use Industry

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising volumes of hazardous and industrial waste requiring safe disposal

- 3.2.1.2 Expansion of industrial and municipal waste-to-energy facilities

- 3.2.1.3 Stricter environmental regulations on waste treatment and emission control

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 High capital cost of advanced low-emission burner systems

- 3.2.2.2 Public opposition and regulatory scrutiny toward incineration facilities

- 3.2.3 Opportunities

- 3.2.3.1 Development of ultra-low NOx and high-efficiency burner technologies

- 3.2.3.2 Retrofit demand for aging incinerators to meet updated regulations

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Burner Design, 2022 - 2035, (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 Monoblock

- 5.3 Duoblock

Chapter 6 Market Estimates & Forecast, By Installation, 2022 - 2035, (USD Million) (Thousand Units)

- 6.1 Key trends

- 6.2 Brownfield

- 6.3 Greenfield

Chapter 7 Market Estimates & Forecast, By Power Range, 2022 - 2035, (USD Million) (Thousand Units)

- 7.1 Key trends

- 7.2 < 300 kW

- 7.3 300 kW - 1 MW

- 7.4 1 - 5 MW

- 7.5 5 - 20MW

- 7.6 20 - 50 MW

- 7.7 > 50 MW

Chapter 8 Market Estimates & Forecast, By End Use Industry, 2022 - 2035, (USD Million) (Thousand Units)

- 8.1 Key trends

- 8.2 Power generation

- 8.3 Chemical and petrochemical

- 8.4 Metalworking

- 8.5 Food processing

- 8.6 Textile

- 8.7 Pulp and paper

- 8.8 Others

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Million) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 Saudi Arabia

- 9.6.2 UAE

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Alfa Laval

- 10.2 Babcock Wanson

- 10.3 Baltur

- 10.4 Bloom Engineering Company

- 10.5 Carrier

- 10.6 Fives Group

- 10.7 Forbes Marshall Pvt. Ltd.

- 10.8 Honeywell International

- 10.9 John Zink Hamworthy Combustion

- 10.10 Limpsfield Combustion Engineering

- 10.11 Max Weishaupt

- 10.12 Miura America Co.

- 10.13 Oilon Group Oy

- 10.14 QED Combustion

- 10.15 Selas Heat Technology Company

工業燃燒器市場:按燃燒器類型、燃料類型、燃燒器技術、熱容量和最終用途產業分類-2026-2032年全球市場預測

工業燃燒器市場:按燃燒器類型、燃料類型、燃燒器技術、熱容量和最終用途產業分類-2026-2032年全球市場預測 工業燃燒器市場機會、成長要素、產業趨勢分析及2026-2035年預測。

工業燃燒器市場機會、成長要素、產業趨勢分析及2026-2035年預測。 2026年全球工業燃燒器市場報告工業槍式燃燒器市場:依燃料類型、技術、安裝方式、容量、應用、最終用戶和通路分類,全球預測,2026-2032年預混合料燃燒器市場:依燃料類型、應用、終端用戶產業及通路分類,全球預測,2026-2032年

2026年全球工業燃燒器市場報告工業槍式燃燒器市場:依燃料類型、技術、安裝方式、容量、應用、最終用戶和通路分類,全球預測,2026-2032年預混合料燃燒器市場:依燃料類型、應用、終端用戶產業及通路分類,全球預測,2026-2032年 工業燃燒器市場報告:按燃燒器類型、燃料類型、自動化程度、動作溫度、應用、終端用戶產業和地區分類(2026-2034 年)點火燃燒器市場:依產品類型、燃料類型、最終用戶和分銷管道分類,全球預測,2026-2032年低氮真空熱水器市場按應用、燃料類型、終端用戶產業、容量、分銷管道和安裝量分類,全球預測(2026-2032年)

工業燃燒器市場報告:按燃燒器類型、燃料類型、自動化程度、動作溫度、應用、終端用戶產業和地區分類(2026-2034 年)點火燃燒器市場:依產品類型、燃料類型、最終用戶和分銷管道分類,全球預測,2026-2032年低氮真空熱水器市場按應用、燃料類型、終端用戶產業、容量、分銷管道和安裝量分類,全球預測(2026-2032年) 全球工業燃燒器市場規模、佔有率、趨勢和成長分析報告:2026-2034年

全球工業燃燒器市場規模、佔有率、趨勢和成長分析報告:2026-2034年 全球工業燃燒器市場,2026-2030年

全球工業燃燒器市場,2026-2030年