|

市場調查報告書

商品編碼

1982358

廚房水槽市場機會、成長要素、產業趨勢分析及2026-2035年預測。Kitchen Sink Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

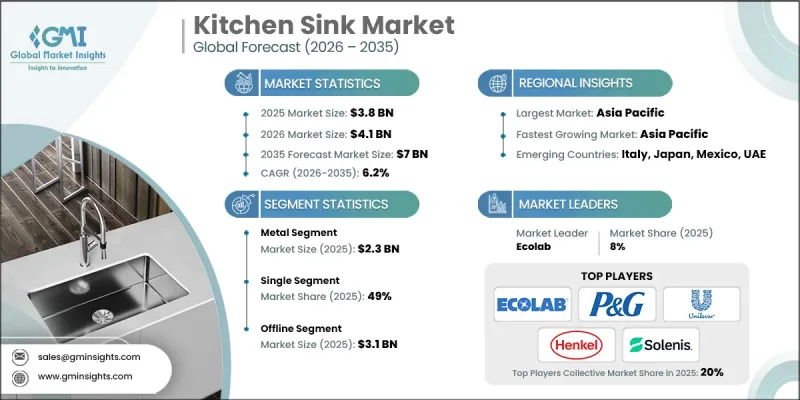

全球廚房水槽市場預計到 2025 年價值 38 億美元,預計年複合成長率為 6.2%,到 2035 年達到 70 億美元。

城市發展進步、飲食習慣改變以及對便利餐飲解決方案的強勁需求推動了這一成長。餐飲服務業的穩定擴張持續帶動商用廚房水槽的穩定需求,因為所有商用廚房都需要可靠的清潔設備來滿足衛生標準。經營者越來越重視符合監管要求、經久耐用且易於維護的水槽。不銹鋼因其強度高、衛生且使用壽命長,仍是首選材料。同時,餐飲連鎖店和獨立餐廳基礎設施的標準化也影響採購決策。緊湊型廚房佈局和最佳化設計也影響產品設計,促使製造商推出節省空間的型號。在住宅應用方面,翻新趨勢和美觀提升進一步推動了銷售。總而言之,耐用性、功能性和合規性仍然是關鍵的採購考量因素,為廚房水槽產業的長期持續成長奠定了基礎。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 38億美元 |

| 預計金額 | 70億美元 |

| 複合年成長率 | 6.2% |

連鎖餐廳網路的持續擴張推動了標準化廚房佈局的普及,而這又需要高品質的水槽安裝。餐飲服務商必須遵守嚴格的衛生法規,這也促使市場對先進的多腔式非接觸式水槽系統的需求不斷成長。此外,以配送為中心的廚房和緊湊型餐廳空間的興起,也加速了對小型水槽配置的需求,這些小型水槽能夠在不影響性能的前提下最大限度地提高效率。

預計2025年,金屬製品市場規模將達23億美元。金屬廚房水槽因其耐用性、成本效益和衛生優勢,正推動全球市場的需求。其耐腐蝕性、耐溫差性以及能夠承受日常高強度使用,使其成為商業和住宅環境的首選。不銹鋼水槽尤其受到都市區住宅和專業廚房的青睞,因為可靠性和耐用性是這些場所的關鍵購買因素。

到2025年,單槽水槽將佔據49%的市場。其受歡迎的原因在於其簡潔的設計,這種設計增強了工作空間的柔軟性,並最佳化了櫥櫃的使用率。一個完整的單槽水槽可以容納大型廚具,並簡化清潔工作,因此適用於各種廚房佈局。在緊湊型廚房中,這種配置最大限度地利用了有限的櫥櫃面積;而在較大的空間中,它可以與各種配件無縫銜接,打造出一個實用且美觀的工作空間。

預計到2025年,美國廚房水槽市佔率將達到87.8%,市場規模將達到7.171億美元。這主要得益於活躍的住宅翻新和強勁的住宅建設。消費者對高品質、美觀耐用的廚房設備的需求日益成長,推動了此類產品需求的持續成長。客製化廚房安裝服務越來越受歡迎,同時,人們對永續和環保材料的興趣也日益濃厚。競爭激烈的零售市場,以及許多知名品牌的湧現,也是美國保持在主導地位的關鍵因素。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 在全球範圍內,快餐店和餐廳的數量正在增加。

- 住宅建設和翻新活動增加

- 消費者偏好永續耐用材料

- 產業潛在風險與挑戰

- 安裝和維護成本高昂

- 市場飽和

- 機會

- 智慧和物聯網廚房設備的擴展

- 對模組化和節省空間的廚房設計的需求日益成長

- 促進因素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 材料

- 監理情勢

- 標準和合規要求

- 區域法規結構

- 認證標準

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依材料分類,2022-2035年

- 金屬

- 不銹鋼

- 銅

- 鑄鐵

- 青銅

- 鋁

- 非金屬

- 花崗岩

- 石英複合材料

- 耐火粘土

- 陶瓷製品

- 丙烯酸纖維

- 其他材料(大理石、皂石等)

第6章 市場估價與預測:按碗賽分類,2022-2035年

- 單身的

- 雙倍的

- 多種的

第7章 市場估計與預測:依設備類型分類,2022-2035年

- 嵌入式或頂裝式

- 下裝式

- 農舍式或圍裙式

- 其他(例如,工作站同步)

第8章 市場估計與預測:依價格分類,2022-2035年

- 低價位(低於 299 美元)

- 中價位(300-699美元)

- 高價位(超過700美元)

第9章 市場估價與預測:依最終用戶分類,2022-2035年

- 住宅

- 商業的

第10章 市場估價與預測:依通路分類,2022-2035年

- 線上

- 離線

第11章 市場估價與預測:按地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第12章:公司簡介

- American Standard Brands

- Blanco GmbH+Co KG

- Bonke

- Carysil Global

- Elkay Manufacturing Company

- Foster

- Franke Kitchen Systems

- Houzer

- Kohler

- Moen Incorporated

- Nirali

- Roca

- Ruvati USA

- Schock

- Teka

The Global Kitchen Sink Market was valued at USD 3.8 billion in 2025 and is estimated to grow at a CAGR of 6.2% to reach USD 7 billion by 2035.

Growth is fueled by rising urban development, evolving food consumption patterns, and strong demand for convenient dining solutions. The steady expansion of foodservice operations continues to generate consistent demand for commercial kitchen sinks, as every professional kitchen requires reliable washing infrastructure to meet sanitation standards. Operators increasingly prioritize durable, easy-to-maintain sinks that comply with regulatory requirements. Stainless steel remains the preferred material due to its strength, hygienic properties, and long service life. At the same time, infrastructure standardization across foodservice chains and independent establishments is shaping purchasing decisions. Compact kitchen formats and optimized layouts are also influencing product design, encouraging manufacturers to introduce space-efficient models. Across residential applications, remodeling trends and aesthetic upgrades further support sales. Overall, durability, functionality, and compliance remain central purchasing considerations, positioning the kitchen sink industry for sustained long-term growth.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.8 Billion |

| Forecast Value | $7 Billion |

| CAGR | 6.2% |

The continued rise of franchise-based restaurant networks has encouraged standardized kitchen layouts that require premium-quality sink installations. Foodservice operators must comply with strict sanitation regulations, which drives demand for advanced, multi-compartment, and touchless sink systems. Additionally, the development of delivery-focused kitchens and compact restaurant spaces has accelerated demand for smaller sink configurations that maximize efficiency without compromising performance.

The metal-based products segment generated USD 2.3 billion in 2025. Metal kitchen sinks lead global demand because they offer durability, cost efficiency, and hygiene advantages. Their resistance to corrosion, tolerance to temperature variations, and ability to withstand heavy daily usage make them a preferred option in both commercial and residential environments. Stainless steel models are particularly popular in urban households and professional food preparation spaces, where reliability and longevity are essential purchasing factors.

The single bowl segment accounted for 49% share in 2025. Its popularity stems from a streamlined design that enhances workspace flexibility and optimizes cabinet utilization. A single, uninterrupted basin accommodates large cookware and simplifies cleaning tasks, making it suitable for diverse kitchen layouts. In compact kitchens, this configuration maximizes usable sink area within limited cabinetry, while in larger settings it integrates seamlessly with accessories to create a practical and visually appealing workstation.

U.S. Kitchen Sink Market captured 87.8% share in 2025, generating USD 717.1 million, supported by robust home renovation activity and steady residential construction. Consumers increasingly seek premium-quality, visually appealing, and long-lasting kitchen fixtures, contributing to higher product demand. Custom kitchen installations are gaining traction, alongside growing interest in sustainable and environmentally responsible materials. A competitive retail landscape with well-established brands continues to reinforce the country's leadership within the regional market.

Leading companies operating in the Global Kitchen Sink Market include Franke Kitchen Systems, Elkay Manufacturing Company, Kohler, Blanco, Moen Incorporated, Roca, American Standard Brands, Teka, Carysil Global, Schock, Foster, Houzer, Ruvati USA, Nirali, and Bonke. Companies in the Global Kitchen Sink Market are strengthening their competitive position through product innovation, material advancement, and portfolio diversification. Manufacturers are investing in research and development to introduce scratch-resistant finishes, noise-reduction technology, and integrated workstation features that enhance functionality. Strategic collaborations with distributors and home improvement retailers are expanding market reach, while digital marketing initiatives are improving brand visibility. Many players are focusing on sustainable manufacturing practices and eco-friendly materials to align with shifting consumer preferences. Customization options and modular sink solutions are also being introduced to meet evolving residential and commercial kitchen design trends.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material

- 2.2.3 Bowl

- 2.2.4 Installation

- 2.2.5 Price

- 2.2.6 End use

- 2.2.7 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing numbers of quick service restaurants & food joints across the globe

- 3.2.1.2 Rising residential construction and renovation activities

- 3.2.1.3 Consumer preference for sustainable and durable materials

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High installation and maintenance costs

- 3.2.2.2 Market saturation

- 3.2.3 Opportunities

- 3.2.3.1 Expansion in smart and IoT-enabled kitchen fixtures

- 3.2.3.2 Growing demand for modular and space-saving kitchen designs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By material

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Material, 2022 - 2035 (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Metal

- 5.2.1 Stainless steel

- 5.2.2 Copper

- 5.2.3 Cast Iron

- 5.2.4 Bronze

- 5.2.5 Aluminium

- 5.3 Non-metal

- 5.3.1 Granite

- 5.3.2 Quartz composite

- 5.3.3 Fireclay

- 5.3.4 Ceramic

- 5.3.5 Acrylic

- 5.3.6 Others (marble, soapstone etc.)

Chapter 6 Market Estimates and Forecast, By Bowl, 2022 - 2035 (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Single

- 6.3 Double

- 6.4 Multiple

Chapter 7 Market Estimates and Forecast, By Installation, 2022 - 2035 (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Drop-in or top mount

- 7.3 Undermount

- 7.4 Farmhouse or apron-front

- 7.5 Others (workstation sinks etc.)

Chapter 8 Market Estimates and Forecast, By Price, 2022 - 2035 (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Low (up to $299)

- 8.3 Medium ($300-$699)

- 8.4 High ($700 and above)

Chapter 9 Market Estimates and Forecast, By End User, 2022 - 2035 (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 Residential

- 9.3 Commercial

Chapter 10 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Million Units)

- 10.1 Key trends

- 10.2 Online

- 10.3 Offline

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Million Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 American Standard Brands

- 12.2 Blanco GmbH + Co KG

- 12.3 Bonke

- 12.4 Carysil Global

- 12.5 Elkay Manufacturing Company

- 12.6 Foster

- 12.7 Franke Kitchen Systems

- 12.8 Houzer

- 12.9 Kohler

- 12.10 Moen Incorporated

- 12.11 Nirali

- 12.12 Roca

- 12.13 Ruvati USA

- 12.14 Schock

- 12.15 Teka

浴室洗手盆市場:2026-2032年全球市場預測(依材料、安裝方式、類型、形狀、最終用戶和銷售管道)按槽數、安裝方式、材質、分銷管道和應用分類的全球分槽式水槽市場預測(2026-2032年)

浴室洗手盆市場:2026-2032年全球市場預測(依材料、安裝方式、類型、形狀、最終用戶和銷售管道)按槽數、安裝方式、材質、分銷管道和應用分類的全球分槽式水槽市場預測(2026-2032年) 全球石英水槽市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球石英水槽市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 水處理設備市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、應用、分銷管道、地區和競爭格局分類,2021-2031年)石英水槽市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、應用、分銷管道、地區和競爭格局分類,2021-2031年)

水處理設備市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、應用、分銷管道、地區和競爭格局分類,2021-2031年)石英水槽市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、應用、分銷管道、地區和競爭格局分類,2021-2031年) 水洗水槽市場機會、成長要素、產業趨勢分析及2026年至2035年預測廚房水槽市場 - 全球產業規模、佔有率、趨勢、機會和預測,按材質(金屬、花崗岩、其他)、水槽數量(單槽、多槽)、最終用戶(住宅、商業)、地區和競爭格局分類,2021-2031年預測

水洗水槽市場機會、成長要素、產業趨勢分析及2026年至2035年預測廚房水槽市場 - 全球產業規模、佔有率、趨勢、機會和預測,按材質(金屬、花崗岩、其他)、水槽數量(單槽、多槽)、最終用戶(住宅、商業)、地區和競爭格局分類,2021-2031年預測 石英水槽市場規模、佔有率及成長分析(按類型、應用、通路和地區分類)-2026-2033年產業預測家用廚房水槽市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)

石英水槽市場規模、佔有率及成長分析(按類型、應用、通路和地區分類)-2026-2033年產業預測家用廚房水槽市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年) 全球多功能廚房水槽市場

全球多功能廚房水槽市場