|

市場調查報告書

商品編碼

1982354

汽車行人保護系統市場:市場機會、成長要素、產業趨勢分析及2026-2035年預測Automotive Pedestrian Protection System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

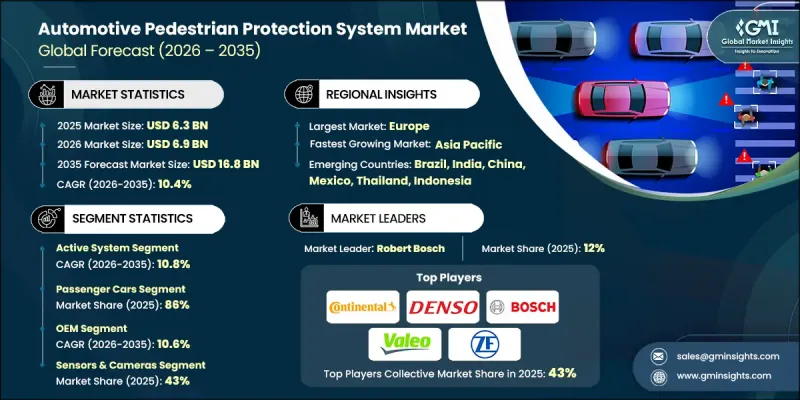

全球汽車行人保護系統市場預計到 2025 年將價值 63 億美元,預計到 2035 年將以 10.4% 的複合年成長率成長至 168 億美元。

隨著汽車製造商優先採用旨在減少行人傷亡的車輛安全技術,尤其是在擁擠的都市區,市場呈現強勁的成長動能。行人保護系統 (PPS) 結合了先進的緊急煞車和行人偵測技術、可部署的安全組件、基於感測器的監控以及智慧碰撞緩解技術,旨在預防碰撞或減輕傷亡程度。該市場涵蓋整合安全軟體、感測器硬體、致動器系統、結構能量吸收設計以及為原始設備製造商 (OEM) 和一級供應商提供的工程支援服務。隨著時間的推移,行人保護解決方案已從被動結構設計發展到能夠即時識別物體和預測碰撞避免的人工智慧智慧系統。由於全球嚴格的安全法規和車輛評估計劃,以及監管機構強制要求新車配備具備行人和騎乘者偵測功能的高級煞車系統,提前部署正在加速進行。對基於雲端的模擬工具和數位檢驗平台的日益依賴,進一步提高了系統精度,並加速了整個汽車行人保護系統市場的創新。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 63億美元 |

| 預測金額 | 168億美元 |

| 複合年成長率 | 10.4% |

預計到2025年,主動式行人保護系統市佔率將達到59%,並在2026年至2035年間以10.8%的複合年成長率成長。主動式行人保護技術整合了前置攝影機、雷達感測器以及日益普及的LiDAR系統,並搭配先進的處理軟體。這些系統透過偵測行人移動、評估軌跡風險、計算碰撞機率,並在達到預設安全閾值時自動啟動煞車功能,顯著提升了即時反應能力。

預計到2025年,乘用車市佔率將達到86%,複合年成長率(CAGR)為10.2%。此細分市場的需求主要受歐洲新車安全評估協會(Euro NCAP)和美國國家公路交通安全管理局(NHTSA)等機構制定的嚴格行人安全評估標準的驅動,這些標準尤其重視主動行人安全性能。所有車型類別的監管壓力正促使製造商採用先進的模擬和檢驗平台,以確保合規性並最佳化系統效率。

德國汽車行人保護系統市場預計將在2026年至2035年間以10.9%的複合年成長率成長。 BMW、賓士、奧迪和保時捷等主要汽車製造商對安全技術創新的大力投資,鞏固了德國在該領域的主導地位。日益複雜的都市區交通環境和混合交通格局,推動了可靠行人保護系統的應用,這些系統旨在有效應對動態的實際交通狀況。

目錄

第1章:調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率分析

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 全球有關行人安全的嚴格法規和義務

- 都市區行人死亡率上升

- 消費者對先進安全功能的需求日益成長

- ADAS和自動駕駛技術的廣泛應用。

- 保險業會推廣安全評級的車輛

- 產業潛在風險與挑戰

- 高昂的實施和整合成本

- 惡劣天氣條件下系統效率下降

- 由於技術複雜,售後市場接受度有限。

- 被動式系統(外部安全氣囊)的一次性特性

- 市場機遇

- 現有商用車輛車隊的改裝解決方案

- 與V2X和智慧城市基礎設施的整合

- 正在建立安全標準的新興市場

- 人工智慧驅動的夜間偵測系統

- 用於被動防護系統的輕質材料

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 美國聯邦安全法規與ADAS實施指南

- 加拿大 - 連網和自動駕駛汽車安全框架 (CASF)

- 歐洲

- 德國 - 歐洲新車安全評估協會 (Euro NCAP) 行人安全評估

- 英國:脫歐後ADAS的柔軟性

- 法國-國內ADAS測試與智慧交通系統戰略

- 義大利——智慧交通系統示範計畫與智慧基礎設施

- 亞太地區

- 中國——工業和資訊化部強制實施和規範C-V2X

- 印度:新興ADAS和汽車互聯技術的監管

- 日本——智慧交通系統連結性與頻率政策

- 澳洲—技術中立的智慧交通系統政策

- 拉丁美洲

- 墨西哥 - NOM 汽車安全標準

- 阿根廷 - 交通法第 24.449 號

- 中東和非洲

- 南非 - 道路交通法(1996 年)

- 沙烏地阿拉伯—交通運輸法律與「2030願景」交通運輸舉措

- 北美洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 感測器技術的發展(攝影機、LiDAR、雷達、超音波)

- 整合感測器融合

- 人工智慧和機器學習在行人偵測的應用

- 新興技術

- V2X 通訊可提高偵測能力

- 適用於夜間和低光源環境的偵測技術

- 當前技術趨勢

- 專利分析

- 主要專利趨勢

- 技術創新熱點

- 主要企業提交的專利申請

- 新興智慧財產權策略

- 價格分析

- 對過去價格趨勢的分析

- 按業務類型分類的定價策略(溢價/價值/成本加成)

- 總擁有成本 (TCO) 分析

- 使用案例和成功案例

- 案例研究

- OEM整合PPS技術

- 商用車輛車隊簡介

- 行人保護計畫改裝

- 智慧城市都市區示範計劃

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 關於碳足跡的考量

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 針對特定領域的生成式人工智慧應用案例和實施藍圖

- 風險、限制和監管考量

- 未來趨勢和市場展望

- 下一代感測器技術

- 與自動駕駛生態系統的整合

- 人工智慧驅動的行人安全預測系統

- 新興市場的擴張

- 市場風險及風險緩解策略

- 監理合規風險

- 技術採用的障礙

- 供應鏈中斷

- 網路安全和資料隱私問題

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲(MEA)

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃及資金籌措

第5章 市場估計與預測:依組件分類,2022-2035年

- 感應器和攝影機

- 控制單元

- 致動器

- 其他

第6章 市場估算與預測:依產品分類,2022-2035年

- 主動系統

- 被動系統

第7章 市場估價與預測:依車輛類型分類,2022-2035年

- 搭乘用車

- 掀背車

- 轎車

- SUV

- 商用車輛

- 輕型商用車(LCV)

- 中型商用車(MCV)

- 重型商用車(HCV)

第8章 市場估算與預測:依通路分類,2022-2035年

- OEM

- 售後市場

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 荷蘭

- 瑞典

- 丹麥

- 波蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 新加坡

- 泰國

- 印尼

- 越南

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥倫比亞

- 中東和非洲(MEA)

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 以色列

第10章:公司簡介

- 世界公司

- Autoliv

- Continental

- Denso

- Ford Motor

- Magna International

- Mobileye

- Nissan Motor

- Robert Bosch

- Toyota Motor

- ZF Friedrichshafen

- 本地球員

- Aptiv

- HELLA

- Hitachi Astemo

- Hyundai Mobis

- Knorr-Bremse

- Magneti Marelli

- Subaru

- Valeo

- 新興企業和技術基礎設施公司

- Gentex

- Luminar Technologies

The Global Automotive Pedestrian Protection System Market was valued at USD 6.3 billion in 2025 and is estimated to grow at a CAGR of 10.4% to reach USD 16.8 billion by 2035.

The market is gaining strong momentum as automakers prioritize vehicle safety technologies designed to reduce pedestrian injuries and fatalities, particularly in high-traffic urban environments. Pedestrian protection systems (PPS) combine advanced emergency braking with pedestrian detection, deployable safety components, sensor-based monitoring, and intelligent impact mitigation technologies to either prevent collisions or reduce injury severity. The market encompasses integrated safety software, sensor hardware, actuator systems, structural energy-absorbing designs, and engineering support services supplied to OEMs and Tier 1 manufacturers. Over time, pedestrian protection solutions have evolved from passive structural designs to intelligent, AI-enabled systems capable of real-time object recognition and predictive collision avoidance. Strict safety mandates and vehicle rating programs worldwide are accelerating adoption, as regulators require advanced braking systems with pedestrian and cyclist detection capabilities in new vehicles. Growing reliance on cloud-based simulation tools and digital validation platforms is further enhancing system accuracy and accelerating innovation across the automotive pedestrian protection system market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.3 Billion |

| Forecast Value | $16.8 Billion |

| CAGR | 10.4% |

The active system segment accounted for 59% share in 2025 and is anticipated to grow at a CAGR of 10.8% from 2026 to 2035. Active pedestrian protection technologies integrate forward-facing cameras, radar sensors, and increasingly LiDAR systems with advanced processing software. These systems detect pedestrian movement, assess trajectory risks, calculate collision probability, and automatically activate braking functions when predefined safety thresholds are reached, significantly improving real-time response capabilities.

The passenger cars segment held 86% share in 2025 and is projected to grow at a CAGR of 10.2%. Demand within this segment is supported by stringent pedestrian safety assessment standards established by organizations such as the European New Car Assessment Programme and the National Highway Traffic Safety Administration, which place significant emphasis on active pedestrian safety performance. Regulatory pressure across vehicle categories is encouraging manufacturers to adopt advanced simulation and validation platforms to ensure compliance and optimize system efficiency.

Germany Automotive Pedestrian Protection System Market is forecast to grow at a CAGR of 10.9% between 2026 and 2035. The country's leadership is supported by strong investments in safety innovation from major automotive manufacturers such as BMW, Mercedes-Benz, Audi, and Porsche. Increasing urban mobility complexity and mixed-traffic environments are driving the integration of highly reliable pedestrian protection systems designed to operate effectively in dynamic real-world conditions.

Key companies operating in the Global Automotive Pedestrian Protection System Market include ZF Friedrichshafen, Aptiv, Denso, Valeo, Robert Bosch, Autoliv, Continental, Marelli, Hitachi Astemo, and Hella. Companies in the Automotive Pedestrian Protection System Market strengthen their competitive position through continuous investment in research and development focused on AI-driven sensing, advanced braking algorithms, and sensor fusion technologies. Strategic collaborations with OEMs and Tier 1 suppliers enable co-development of integrated safety platforms tailored to specific vehicle architectures. Firms are expanding simulation capabilities using cloud-based validation tools to accelerate product certification and regulatory compliance. Geographic expansion, portfolio diversification, and modular system designs allow suppliers to serve both premium and mass-market vehicle segments. In addition, companies emphasize cost optimization, scalable production, and software updates to enhance long-term system performance, ensuring sustainable growth and stronger market penetration in the evolving global automotive safety landscape.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 Research trail and confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Best estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Components

- 2.2.3 Product

- 2.2.4 Vehicles

- 2.2.5 Distribution Channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Stringent global pedestrian safety regulations & mandates

- 3.2.1.2 Rising pedestrian fatality rates in urban areas

- 3.2.1.3 Increasing consumer demand for advanced safety features

- 3.2.1.4 Growing adoption of ADAS & autonomous driving technologies

- 3.2.1.5 Insurance industry push for safety-rated vehicles

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High installation & integration costs

- 3.2.2.2 Low system efficiency in adverse weather conditions

- 3.2.2.3 Limited aftermarket adoption due to technical complexity

- 3.2.2.4 One-time use nature of passive systems (external airbags)

- 3.2.3 Market opportunities

- 3.2.3.1 Retrofit solutions for existing commercial vehicle fleets

- 3.2.3.2 Integration with V2X & smart city infrastructure

- 3.2.3.3 Emerging markets with developing safety standards

- 3.2.3.4 AI-enhanced nighttime detection systems

- 3.2.3.5 Lightweight materials for passive protection systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 US- Federal safety rules & ADAS deployment guidance

- 3.4.1.2 Canada - Safety framework for connected & automated vehicles (CASF)

- 3.4.2 Europe

- 3.4.2.1 Germany- Euro NCAP pedestrian safety ratings

- 3.4.2.2 UK- Post-Brexit ADAS flexibility

- 3.4.2.3 France- National ADAS testing & ITS strategy

- 3.4.2.4 Italy- ITS pilots & smart infrastructure

- 3.4.3 Asia Pacific

- 3.4.3.1 China- MIIT C-V2X mandates & standards

- 3.4.3.2 India- Emerging ADAS & automotive connectivity regulations

- 3.4.3.3 Japan- ITS connect & spectrum policy

- 3.4.3.4 Australia- Technology neutral ITS policies

- 3.4.4 LATAM

- 3.4.4.1 Mexico- NOM vehicle safety standards

- 3.4.4.2 Argentina- National traffic law 24.449

- 3.4.5 MEA

- 3.4.5.1 South Africa- National road traffic act (1996)

- 3.4.5.2 Saudi Arabia- Traffic law & vision 2030 transport initiatives

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.1.1 Sensor technology evolution (camera, LiDAR, RADAR, ultrasonic)

- 3.7.1.2 Sensor fusion & integration

- 3.7.1.3 AI & machine learning in pedestrian detection

- 3.7.2 Emerging technologies

- 3.7.2.1 V2X communication for enhanced detection

- 3.7.2.2 Nighttime & low-light detection technologies

- 3.7.1 Current technological trends

- 3.8 Patent analysis

- 3.8.1 Key patent trends

- 3.8.2 Technology innovation hotspots

- 3.8.3 Patent filing by key players

- 3.8.4 Emerging IP strategies

- 3.9 Pricing analysis

- 3.9.1 Historical price trend analysis

- 3.9.2 Pricing strategy by player type (premium / value / cost-plus)

- 3.9.3 Total cost of ownership (TCO) analysis

- 3.10 Use cases & success stories

- 3.11 Case studies

- 3.11.1 OEM integration of PPS technologies

- 3.11.2 Commercial vehicle fleet deployments

- 3.11.3 Retrofit pedestrian protection programs

- 3.11.4 Urban pilot projects in smart cities

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Impact of AI & generative AI on the market

- 3.13.1 AI-driven disruption of existing business models

- 3.13.2 GenAI use cases & adoption roadmap by segment

- 3.13.3 Risks, limitations & regulatory considerations

- 3.14 Future trends and market outlook

- 3.14.1 Next-generation sensor technologies

- 3.14.2 Integration with autonomous driving ecosystems

- 3.14.3 AI-driven predictive pedestrian safety systems

- 3.14.4 Expansion in emerging markets

- 3.15 Market risks and mitigation strategies

- 3.15.1 Regulatory compliance risks

- 3.15.2 Technology adoption barriers

- 3.15.3 Supply chain disruptions

- 3.15.4 Cybersecurity and data privacy concerns

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Sensors & cameras

- 5.3 Control unit

- 5.4 Actuators

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Product, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Active system

- 6.3 Passive system

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicles

- 7.3.1 Light commercial vehicles (LCVs)

- 7.3.2 Medium commercial vehicles (MCVs)

- 7.3.3 Heavy commercial vehicles (HCVs)

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Netherlands

- 9.3.8 Sweden

- 9.3.9 Denmark

- 9.3.10 Poland

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Singapore

- 9.4.7 Thailand

- 9.4.8 Indonesia

- 9.4.9 Vietnam

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Colombia

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

- 9.6.4 Israel

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Autoliv

- 10.1.2 Continental

- 10.1.3 Denso

- 10.1.4 Ford Motor

- 10.1.5 Magna International

- 10.1.6 Mobileye

- 10.1.7 Nissan Motor

- 10.1.8 Robert Bosch

- 10.1.9 Toyota Motor

- 10.1.10 ZF Friedrichshafen

- 10.2 Regional Players

- 10.2.1 Aptiv

- 10.2.2 HELLA

- 10.2.3 Hitachi Astemo

- 10.2.4 Hyundai Mobis

- 10.2.5 Knorr-Bremse

- 10.2.6 Magneti Marelli

- 10.2.7 Subaru

- 10.2.8 Valeo

- 10.3 Emerging Players & Technology Enablers

- 10.3.1 Gentex

- 10.3.2 Luminar Technologies

車行通訊市場-2026-2032年全球市場預測

車行通訊市場-2026-2032年全球市場預測 全球汽車行人保護系統市場

全球汽車行人保護系統市場 汽車行人保護系統(PPS)市場:按技術、車輛類型和地區分類

汽車行人保護系統(PPS)市場:按技術、車輛類型和地區分類 2026-2034年全球汽車行人保護系統市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球汽車行人保護系統市場規模、佔有率、趨勢和成長分析報告 2026年全球行人保護氣囊市場報告2026年全球行人偵測系統市場報告全球行人偵測系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

2026年全球行人保護氣囊市場報告2026年全球行人偵測系統市場報告全球行人偵測系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 行人偵測系統市場:商業機會、成長要素、產業趨勢分析及 2026-2035 年預測。汽車行人保護系統市場:依行人偵測技術、系統類型、ADAS等級、車輛類型和通路分類-2026-2032年全球預測

行人偵測系統市場:商業機會、成長要素、產業趨勢分析及 2026-2035 年預測。汽車行人保護系統市場:依行人偵測技術、系統類型、ADAS等級、車輛類型和通路分類-2026-2032年全球預測 汽車行人保護系統市場規模、佔有率及成長分析(依技術、組件類型、類型及地區分類)-2026-2033年產業預測

汽車行人保護系統市場規模、佔有率及成長分析(依技術、組件類型、類型及地區分類)-2026-2033年產業預測