|

市場調查報告書

商品編碼

1982305

食品中膳食纖維的市場機會、成長要素、產業趨勢及 2026-2035 年預測。Food Fibers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

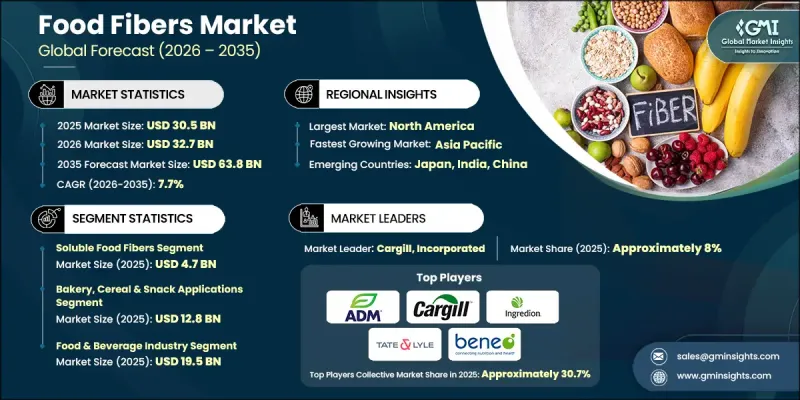

預計到 2025 年,全球食品中膳食纖維市場價值將達到 305 億美元,並預計以 7.7% 的複合年成長率成長,到 2035 年達到 638 億美元。

隨著消費者越來越重視健康、保健和預防性營養,膳食纖維產業正經歷強勁成長。人們對消化系統健康和整體健康的日益關注,促使他們將富含膳食纖維的產品納入日常飲食中。因此,全球市場對強化膳食纖維食品和飲料的需求持續上升。對生活方式相關健康問題(例如代謝性疾病和心血管疾病)的日益關注,進一步影響消費者的購買行為。消費者積極尋求有助於體重管理、血糖值穩定和長期健康維護的膳食解決方案。這種向預防性營養的轉變,促使食品製造商開發創新富含膳食纖維的功能性產品。功能性食品和飲料領域正在成為整個營養產業的主要成長引擎,進一步提升了膳食纖維成分的策略重要性。持續的產品開發和零售通路的改善,正進一步鞏固全球膳食纖維市場的成長動能。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 305億美元 |

| 預測金額 | 638億美元 |

| 複合年成長率 | 7.7% |

預計到2025年,可溶性膳食纖維市場規模將達到47億美元,並在2026年至2035年間以8.2%的複合年成長率成長。這一成長歸功於人們日益認知到可溶性膳食纖維在維持消化平衡、控制膽固醇和血糖值的益處。為了滿足注重健康的消費者的需求,生產商正將可溶性膳食纖維添加到機能性食品、飲料和膳食補充劑中。同時,不溶性膳食纖維也因其在促進腸道功能和維持腸道健康環境方面的作用而備受關注。

預計到2025年,烘焙食品、穀物和零食市場規模將達到128億美元,並在2035年之前以7.3%的複合年成長率成長。該細分市場持續保持領先地位,因為製造商在日常食品中添加膳食纖維,以改善其質地、穩定性和營養價值。膳食纖維還能賦予乳製品替代品和植物來源產品理想的黏度和結構特性,進而促進其創新。在膳食補充劑領域,膳食纖維因其對消化器官系統健康的益處而被廣泛應用,並用於開發針對特定健康益處、滿足消費者偏好的混合配方。

預計到2025年,北美食品中膳食纖維的市場規模將達到107億美元,並在整個預測期內保持穩定成長。該地區市場的擴張主要得益於消費者對消化健康、體重管理和預防性飲食習慣的日益重視。此外,完善的零售分銷網路以及人們對膳食纖維長期健康益處的認知不斷普及,也進一步推動了消費者對富含膳食纖維的機能性食品、飲料和膳食補充劑的強勁需求。

目錄

第1章:調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 市場機遇

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 依纖維類型

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利趨勢

- 貿易統計(註:僅提供主要國家的貿易統計)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 環保意識的舉措

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估價與預測:依光纖類型分類,2022-2035年

- 水溶性膳食纖維

- 果膠和樹膠

- BETA-葡聚醣和特殊纖維

- 其他水溶性膳食纖維

- 不溶性膳食纖維

- 纖維素和改性纖維素

- 小麥麩皮和穀物纖維

- 膳食纖維來自水果和蔬菜

- 益生元纖維

- 菊糖

- 抗解澱粉

- FOS

- GOS

- 其他益生元纖維

- 功能性纖維/機械加工纖維

- 聚葡萄糖

- 抗麥芽糊精

- 新型工程纖維

第6章 市場估計與預測:依應用領域分類,2022-2035年

- 在烘焙、穀物和零食領域的應用

- 麵包和烘焙產品

- 早餐用麥片穀類和零食

- 糖果甜點和甜點

- 其他

- 乳製品和植物來源產品的用途

- 乳製品

- 優格和發酵乳製品

- 乳酪及加工乳製品

- 其他乳製品

- 植物來源乳製品替代品

- 植物來源奶

- 植物來源優格

- 植物來源乳酪和其他乳製品替代品

- 乳製品

- 飲料

- 機能飲料和運動飲料

- 果汁和機能水

- 其他添加膳食纖維的飲料

- 營養補充品

- 粉末/膠囊

- 益生元/腸道健康補充劑

- 體重管理和代謝健康補充劑

第7章 市場估計與預測:依最終用途分類,2022-2035年

- 食品飲料業

- 營養保健品(膳食補充品)

- 醫學和臨床營養

- 運動營養

- 動物和寵物的營養

- 其他

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第9章:公司簡介

- Archer Daniels Midland Company(ADM)

- Cargill, Incorporated

- Ingredion Incorporated

- Tate &Lyle PLC

- BENEO GmbH

- Roquette Freres

- Kerry Group

- International Flavors and Aromas Other

- J Rettenmaier &Sohne GmbH+Co KG

- Nexira Inc.

The Global Food Fibers Market was valued at USD 30.5 billion in 2025 and is estimated to grow at a CAGR of 7.7% to reach USD 63.8 billion by 2035.

The food fibers industry is witnessing strong expansion as consumers place greater emphasis on health, wellness, and preventive nutrition. Increasing awareness about digestive health and overall well-being is encouraging individuals to incorporate fiber-rich products into their daily diets. As a result, demand for fiber-fortified foods and beverages continues to rise across global markets. Growing concerns related to lifestyle-associated health conditions, including metabolic and cardiovascular disorders, are further influencing purchasing behavior. Consumers are actively seeking dietary solutions that support weight management, balanced blood sugar levels, and long-term health outcomes. This shift toward proactive nutrition is motivating food manufacturers to develop innovative functional products enriched with dietary fibers. The functional food and beverage segment has emerged as a key growth engine within the broader nutrition industry, reinforcing the strategic importance of fiber-based ingredients. Continuous product development and increasing retail availability are further strengthening the growth trajectory of the global food fibers market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $30.5 Billion |

| Forecast Value | $63.8 Billion |

| CAGR | 7.7% |

The soluble food fibers segment generated USD 4.7 billion in 2025 and is expected to grow at a CAGR of 8.2% between 2026 and 2035. Growth in this segment is driven by rising recognition of soluble fibers for supporting digestive balance, cholesterol management, and glycemic control. Manufacturers are incorporating soluble fibers into functional foods, beverages, and dietary supplements to meet consumer demand for health-oriented solutions. At the same time, indigestible food fibers are gaining attention for their role in promoting regular bowel function and maintaining overall gut wellness.

The bakery, cereal, and snack applications segment accounted for USD 12.8 billion in 2025 and is projected to grow at a CAGR of 7.3% through 2035. This segment maintains market leadership as producers integrate dietary fibers to enhance texture, improve stability, and increase nutritional value in everyday food products. Food fibers also support innovation in dairy alternatives and plant-based formulations by contributing to desirable consistency and structural properties. In the dietary supplements category, fibers are utilized to deliver digestive health benefits and to formulate targeted wellness blends aligned with consumer preferences.

North America Food Fibers Market reached USD 10.7 billion in 2025 and is anticipated to experience steady growth over the forecast period. Regional expansion is supported by heightened consumer awareness regarding digestive health, weight management, and preventive dietary practices. Strong demand for fiber-enriched functional foods, beverages, and supplements is reinforced by well-established retail distribution networks and growing education about the long-term health benefits of dietary fiber consumption.

Major companies operating in the Global Food Fibers Market include Cargill, Incorporated; Archer Daniels Midland Company (ADM); Ingredion Incorporated; Tate & Lyle PLC; Roquette Freres; Kerry Group; BENEO GmbH; J Rettenmaier & Sohne GmbH + Co KG; Nexira Inc.; and International Flavors and Aromas. Companies in the Food Fibers Market are strengthening their competitive position through product innovation, strategic partnerships, and expansion into high-growth regions. Leading players are investing in research and development to create customized fiber solutions tailored to specific functional and nutritional needs. Collaboration with food and beverage manufacturers is accelerating the integration of advanced fiber ingredients into new product launches. Firms are also focusing on clean-label formulations and sustainable sourcing practices to align with evolving consumer expectations.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Fiber Type

- 2.2.3 Application

- 2.2.4 End use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By fiber type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Fiber Type, 2022- 2035 (USD Billion, Kilo Tons)

- 5.1 Key trends

- 5.2 Soluble fibers

- 5.2.1 Pectins and gums

- 5.2.2 Beta-glucan and specialized fibers

- 5.2.3 Other soluble fibers

- 5.3 Insoluble fibers

- 5.3.1 Cellulose and modified cellulose

- 5.3.2 Wheat bran and cereal fibers

- 5.3.3 Fruit and vegetable fibers

- 5.4 Prebiotic fibers

- 5.4.1 Inulin

- 5.4.2 Resistant starch

- 5.4.3 FOS

- 5.4.4 GOS

- 5.4.5 Other prebiotic fibers

- 5.5 Functional fibers/engineered fibers

- 5.5.1 Polydextrose

- 5.5.2 Resistant maltodextrin

- 5.5.3 Novel engineered fibers

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion, Kilo Tons)

- 6.1 Key trends

- 6.2 Bakery, Cereal & Snack Applications

- 6.2.1 Bread and Bakery Products

- 6.2.2 Breakfast Cereals and Snacks

- 6.2.3 Confectionary and Sweet Products

- 6.2.4 Others

- 6.3 Dairy & Plant-Based Applications

- 6.3.1 Dairy Products

- 6.3.1.1 Yogurt & Fermented Dairy

- 6.3.1.2 Cheese & Processed Dairy Products

- 6.3.1.3 Other Dairy Products

- 6.3.2 Plant-Based Dairy Alternatives

- 6.3.2.1 Plant-Based Milks

- 6.3.2.2 Plant-Based Yogurts

- 6.3.2.3 Plant-Based Cheese & Other Dairy Replacements

- 6.3.1 Dairy Products

- 6.4 Beverages

- 6.4.1 Functional & Sports Drinks

- 6.4.2 Juices & Enhanced Waters

- 6.4.3 Other Fiber-Fortified Beverages

- 6.5 Dietary Supplements

- 6.5.1 Powders & Capsules

- 6.5.2 Prebiotic / Gut and Health Supplements

- 6.5.3 Weight Management & Metabolic Health Supplements

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 (USD Billion, Kilo Tons)

- 7.1 Key trends

- 7.2 Food & Beverage Industry

- 7.3 Dietary Supplements & Nutraceuticals

- 7.4 Medical & Clinical Nutrition

- 7.5 Sports & Performance Nutrition

- 7.6 Animal & Pet Nutrition

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion, Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East & Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East & Africa

Chapter 9 Company Profiles

- 9.1 Archer Daniels Midland Company (ADM)

- 9.2 Cargill, Incorporated

- 9.3 Ingredion Incorporated

- 9.4 Tate & Lyle PLC

- 9.5 BENEO GmbH

- 9.6 Roquette Freres

- 9.7 Kerry Group

- 9.8 International Flavors and Aromas Other

- 9.9 J Rettenmaier & Sohne GmbH + Co KG

- 9.10 Nexira Inc.