|

市場調查報告書

商品編碼

1959622

維生素K市場機會、成長要素、產業趨勢分析及2026年至2035年預測Vitamin K Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

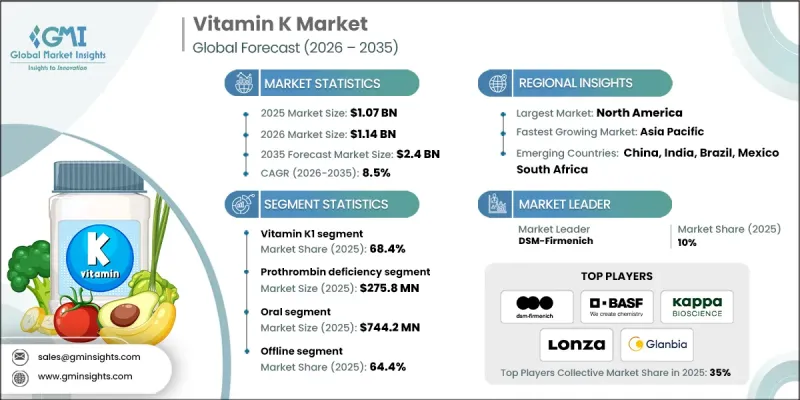

2025 年全球維生素 K 市場價值為 10.7 億美元,預計到 2035 年將達到 24 億美元,年複合成長率為 8.5%。

市場成長的促進因素包括人們對維生素K在血液凝固、骨骼強度和心血管健康方面生理重要性的認知不斷提高,以及老年人中心血管疾病和營養缺乏症發病率的上升。預防醫學的發展趨勢和對微量營養素補充劑日益成長的關注進一步強化了市場需求。維生素K因其在調節鈣代謝和維持血管健康方面的作用,在臨床營養和健康促進領域備受關注。隨著消費者越來越重視長期健康益處,膳食補充劑的作用也從糾正營養缺乏轉向積極主動的疾病風險管理。膳食補充劑應用範圍的擴大、配方穩定性的提高以及補充劑和藥品生物利用度的整體提升,也對市場產生了積極影響。生產方法和原料採購的持續創新使製造商能夠在滿足不斷成長的全球需求的同時,確保產品品質的穩定性。這些因素共同作用,在臨床應用和主導健康意識的雙重推動下,創造了一個穩定擴張的市場模式。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 10.7億美元 |

| 預測金額 | 24億美元 |

| 複合年成長率 | 8.5% |

維生素K是一種脂溶性營養素,對血液凝固、骨骼礦化以及激活維持心血管平衡的蛋白質至關重要。該市場包括主要用於治療和營養補充劑的維生素K1,以及擴大用於維護骨骼和心臟健康的補充劑中的維生素K2。這兩種形式的維生素K在調節鈣轉運和防止礦物質沉積異常方面發揮核心作用,並在從預防醫學到治療醫學的廣泛領域中都具有重要意義。

預計到2025年,維生素K1市佔率將達到68.4%,並在2026年至2035年間以8.3%的複合年成長率成長。該細分市場持續保持主導地位,這主要得益於其在凝血相關疾病治療和維生素K1缺乏症糾正方面的臨床重要性。來自藥品製劑和醫用營養產品的強勁需求推動了其持續應用,而不斷的產品最佳化也進一步提升了其在醫療保健領域的重要性。

預計到2025年,凝血酶原缺乏症市場規模將達2.758億美元。這個市場之所以保持主導地位,是因為維生素K在合成和活化維持正常血液功能所需的凝血因子方面發揮著至關重要的作用。臨床上對維生素K在凝血障礙治療中的依賴性持續推動著市場需求的穩定成長,尤其是在醫院治療和急診通訊協定。

預計到2025年,北美維生素K市佔率將達到41.1%。先進的醫療保健體系、較高的預防保健意識以及營養補充劑的廣泛應用,鞏固了主導地位。持續增加研發投入、產品開發和高品質配方技術,推動了市場成長;同時,消費者對實證營養解決方案的偏好,也進一步增強了區域市場需求。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 影響產業的因素

- 促進因素

- 人們對骨骼和心血管健康的認知不斷提高

- 營養補充品和維生素的廣泛應用

- 製劑技術和生物利用度的進步

- 在製藥領域不斷拓展的應用

- 產業潛在風險與挑戰

- 監管複雜性和合規要求

- 過量服用和副作用的風險

- 市場機遇

- 新興市場健康意識日益增強

- 個人化營養與數位健康的融合

- 促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 未來市場趨勢

- 波特的分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 公司矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章 市場估計與預測:依類型分類,2022-2035年

- 維生素K1

- 維生素K2

第6章 市場估計與預測:依應用領域分類,2022-2035年

- 骨質疏鬆症

- 維生素K依賴性凝血因子缺乏症(VKCFD)

- 凝血酶原缺乏症

- 維生素K缺乏性出血(VKDB)

- 皮膚塗抹

- 其他用途

第7章 市場估計與預測:依給藥途徑分類,2022-2035年

- 口服

- 藥片

- 粉末

- 液體

- 腸外

- 外用

第8章 市場估算與預測:依通路分類,2022-2035年

- 離線

- 大賣場/超級市場

- 專賣店

- 藥局

- 線上

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- Amphastar Pharmaceuticals

- BASF SE

- Country Life(Kikkoman)

- DSM-Firmenich

- Glanbia

- Gnosis by Lesaffre

- Kappa Bioscience

- Livealth Biopharma

- Lonza

- Nature's Bounty(Nestle Health Science)

- Nature Made(Pharmavite)

- NOW Foods

- Pfizer

- Solgar

The Global Vitamin K Market was valued at USD 1.07 billion in 2025 and is estimated to grow at a CAGR of 8.5% to reach USD 2.4 billion by 2035.

Market growth is supported by rising awareness of the physiological importance of vitamin K in blood coagulation, bone strength, and cardiovascular wellness, alongside a growing incidence of cardiovascular conditions and nutrient deficiencies among older populations. Preventive healthcare trends and increased focus on micronutrient supplementation are further strengthening demand. Vitamin K has gained significant attention in clinical nutrition and wellness applications due to its role in regulating calcium metabolism and maintaining vascular integrity. As consumers increasingly prioritize long-term health outcomes, supplementation has moved beyond deficiency correction to proactive disease risk management. The market is also benefiting from expanding nutraceutical usage, improved formulation stability, and enhanced bioavailability across supplement and pharmaceutical products. Continuous innovation in production methods and ingredient sourcing is allowing manufacturers to deliver consistent quality while addressing rising global demand. Together, these factors are shaping a steadily expanding market landscape supported by both clinical utilization and consumer-driven wellness adoption.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.07 Billion |

| Forecast Value | $2.4 Billion |

| CAGR | 8.5% |

Vitamin K represents a class of fat-soluble nutrients that are essential for activating proteins responsible for coagulation, bone mineralization, and cardiovascular balance. The market includes vitamin K1, primarily used in therapeutic and dietary formulations, and vitamin K2, which is increasingly incorporated into supplements designed to support skeletal and heart health. Both forms play a central role in regulating calcium transport and preventing improper mineral deposition, making them critical across preventive and therapeutic healthcare applications.

The vitamin K1 segment accounted for 68.4% share in 2025 and is expected to grow at a CAGR of 8.3% during 2026-2035. This segment continues to lead due to its established clinical importance in managing coagulation-related conditions and correcting deficiency states. Strong demand from pharmaceutical formulations and medical nutrition products supports its sustained adoption, while ongoing product optimization is reinforcing its relevance across healthcare settings.

The prothrombin deficiency segment generated USD 275.8 million in 2025. This segment maintained a leading position as vitamin K remains essential for the synthesis and activation of clotting factors required for normal blood function. Clinical reliance on vitamin K for managing coagulation disorders continues to drive consistent demand, particularly within hospital-based and acute care treatment protocols.

North America Vitamin K Market held 41.1% share in 2025. Regional leadership is supported by advanced healthcare systems, strong preventive health awareness, and widespread adoption of dietary supplementation. Continued investment in research, product development, and high-quality formulation technologies is reinforcing market growth, while consumer preference for scientifically backed nutritional solutions further strengthens regional demand.

Key companies operating in the Global Vitamin K Market include Pfizer, BASF SE, DSM-Firmenich, Lonza, Glanbia, Amphastar Pharmaceuticals, Gnosis by Lesaffre, Kappa Bioscience, Country Life (Kikkoman), Nature Made (Pharmavite), Nature's Bounty (Nestle Health Science), NOW Foods, Solgar, and Livealth Biopharma, with competitive positioning driven by diversified portfolios and global distribution capabilities. Companies active in the vitamin K market are strengthening their market position through continuous investment in formulation innovation, bioavailability enhancement, and product differentiation. Manufacturers are focusing on developing high-purity and stable vitamin K ingredients that meet pharmaceutical and nutraceutical quality standards. Strategic partnerships with healthcare providers and nutrition brands are expanding market reach, while geographic expansion into emerging regions is supporting long-term growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Type trends

- 2.2.3 Application trends

- 2.2.4 Route of administration trends

- 2.2.5 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing awareness of bone and cardiovascular health

- 3.2.1.2 Growing adoption of nutraceuticals and dietary supplements

- 3.2.1.3 Advancements in formulation and bioavailability

- 3.2.1.4 Expanding pharmaceutical applications

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Regulatory complexity and compliance requirements

- 3.2.2.2 Risk of overdosing and side effects

- 3.2.3 Market opportunities

- 3.2.3.1 Emerging markets with rising health awareness

- 3.2.3.2 Integration with personalized nutrition and digital health

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Future market trends

- 3.6 Porter’s analysis

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Vitamin K1

- 5.3 Vitamin K2

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Osteoporosis

- 6.3 Vitamin K-dependent clotting factors deficiency (VKCFD)

- 6.4 Prothrombin deficiency

- 6.5 Vitamin K deficiency bleeding (VKDB)

- 6.6 Dermal applications

- 6.7 Other applications

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Oral

- 7.2.1 Pills

- 7.2.2 Powders

- 7.2.3 Liquids

- 7.3 Parenteral

- 7.4 Topical

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Offline

- 8.2.1 Hypermarkets/ supermarkets

- 8.2.2 Specialty stores

- 8.2.3 Pharmacy stores

- 8.3 Online

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Amphastar Pharmaceuticals

- 10.2 BASF SE

- 10.3 Country Life (Kikkoman)

- 10.4 DSM-Firmenich

- 10.5 Glanbia

- 10.6 Gnosis by Lesaffre

- 10.7 Kappa Bioscience

- 10.8 Livealth Biopharma

- 10.9 Lonza

- 10.10 Nature's Bounty (Nestle Health Science)

- 10.11 Nature Made (Pharmavite)

- 10.12 NOW Foods

- 10.13 Pfizer

- 10.14 Solgar

維生素K2市場:依產品類型、原料、應用、通路和地區分類

維生素K2市場:依產品類型、原料、應用、通路和地區分類 維生素K2全球市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

維生素K2全球市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 維生素K2市場規模、佔有率和成長分析(按功能、產品類型、形態、來源、應用和地區分類)-2026-2033年產業預測

維生素K2市場規模、佔有率和成長分析(按功能、產品類型、形態、來源、應用和地區分類)-2026-2033年產業預測 維生素K3 - 全球市場佔有率和排名、總收入和需求預測(2025-2031年)

維生素K3 - 全球市場佔有率和排名、總收入和需求預測(2025-2031年) 全球維生素 K2 補充劑市場

全球維生素 K2 補充劑市場 維生素 K2 市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

維生素 K2 市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 全球維生素 K2 市場按功能、產品類型、應用形式、產地、用途和地區分類 - 預測至 2029 年

全球維生素 K2 市場按功能、產品類型、應用形式、產地、用途和地區分類 - 預測至 2029 年 維生素 K2 市場、規模、佔有率、趨勢、行業分析報告(按產品類型、來源、形式和地區)- 市場預測,2025-2034 年

維生素 K2 市場、規模、佔有率、趨勢、行業分析報告(按產品類型、來源、形式和地區)- 市場預測,2025-2034 年 2030 年維生素 K2 市場預測:按產品類型、成分、形式、分銷管道、應用和地區進行的全球分析

2030 年維生素 K2 市場預測:按產品類型、成分、形式、分銷管道、應用和地區進行的全球分析 全球維生素 K2 市場規模、佔有率和趨勢分析:按產品類型、形式、應用、地區、前景和預測,2024-2031 年

全球維生素 K2 市場規模、佔有率和趨勢分析:按產品類型、形式、應用、地區、前景和預測,2024-2031 年