|

市場調查報告書

商品編碼

1959606

聯苯市場機會、成長要素、產業趨勢分析及2026年至2035年預測Biphenyl Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

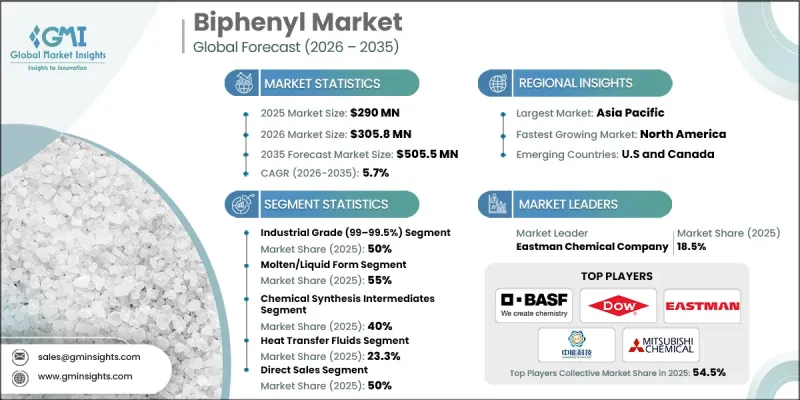

2025 年全球聯苯市場價值為 2.9 億美元,預計到 2035 年將以 5.7% 的複合年成長率成長至 5.055 億美元。

聯苯市場成長主要受特種化學品生產中對聯苯需求不斷成長的驅動。在製藥和農業化學品領域,對高純度中間體的依賴性日益增強,使得聯苯成為複雜分子配方中的關鍵組成部分。由於聯苯化合物具有穩定性好、性能可預測等優點,日益嚴格的化學品純度和性能監管要求推動了其應用。另一個關鍵促進因素是聯苯作為導熱流體和工業溶劑的用途不斷擴大。其優異的熱穩定性和溶解性使其成為高性能工業應用的理想選擇,尤其是在石油化學和汽車行業。環境和監管方面的考慮也促進了聯苯的應用;其明確的安全性和可預測的性能使其適用於塗料、黏合劑、塑膠和其他受監管的應用領域。總而言之,工業復甦、能源效率舉措以及對可靠且受監管的化學解決方案的需求共同推動了市場的發展。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 2.9億美元 |

| 預測金額 | 5.055億美元 |

| 複合年成長率 | 5.7% |

預計到2035年,技術級聯苯市場將以4.1%的複合年成長率成長,這主要得益於在更先進、更高性能的應用中,低純度產品擴大被高純度聯苯所替代。對品質標準和化學性能有嚴格要求的行業更傾向於選擇超高純度聯苯,因為它們具有更優異的穩定性、均一性和反應活性。這種轉變限制了對工業級聯苯的需求,因為工業級聯苯主要用於對絕對純度要求不高的相對簡單的應用領域。

預計到2025年,固體聯苯市佔率將達到45%,這主要得益於其在製藥、農業化學品和特種化學品生產的廣泛應用。其穩定的出貨量成長(年複合成長率5.4%)也印證了這一點。固體聯苯具有許多操作優勢,例如易於操作、可精確計量以及儲存穩定性好,使其成為需要可控且穩定的化學性能的應用的理想選擇。

預計2026年至2035年,北美聯苯市場將以6.7%的複合年成長率成長。該地區是一個成熟且監管嚴格的市場,需求主要集中在製藥、特種化學品製造和導熱油等成熟應用領域。區域成長相對穩定,主要受監管合規、技術逐步升級以及對持續高品質產品的需求所驅動。北美市場的競爭差異化日益受到以下因素的影響:應用開發方面的創新(可提升產品性能和可靠性)、永續的生產方法以及先進的提純製程。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 藥物原料藥產量的增加推動了對超高純度聯苯中間體的需求。

- 擴大聯苯基傳熱流體在工業溫度控管系統的應用。

- 高性能聚合物在航太、電子和先進工程塑膠領域的應用不斷擴展。

- 產業潛在風險與挑戰

- 嚴格的環境法規和對多氯聯苯污染的擔憂限制了生產的柔軟性和核准。

- 苯原料價格波動對生產經濟效益及長期價格穩定性的影響

- 來自其他傳熱流體和替代化學合成路線的競爭日益加劇。

- 市場機遇

- 利用生物基和綠色化學實現聯苯生產技術的商業化

- 隨著電子製造業的快速擴張,OLED 和半導體應用對超高純度聯苯的需求日益成長。

- 新興亞太地區和拉丁美洲工業化經濟體尚未開發的需求

- 促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 按純度等級

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利狀態

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續努力

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 公司矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依純度等級分類,2022-2035年

- 醫藥級(99.5%或更高)

- 工業級(99-99.5%)

- 工業級(95-99%)

第6章 市場估算與預測:依產品類型分類,2022-2035年

- 固體形式

- 薄片

- 粉末

- 水晶

- 熔融/液態

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 化學合成中間體

- 熱傳導劑

- 特殊用途

第8章 市場估算與預測:依最終用途產業分類,2022-2035年

- 製藥業

- 農業化學工業

- 聚合物和塑膠產業

- 電子電氣產業

- 傳熱流體產業

- 其他行業

第9章 市場估價與預測:依通路分類,2022-2035年

- 直銷(從製造商到最終用戶)

- 化學品批發商和批發公司

- 特種化學品供應商

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第11章:公司簡介

- BASF SE

- Dow Inc.

- Eastman Chemical Company

- Huntsman Corporation

- Jiangsu Zhongneng Chemical Technology Co., Ltd.

- LANXESS AG

- Merck KGaA

- Mitsubishi Chemical Corporation

- Solvay SA

- Tokyo Chemical Industry Co., Ltd

The Global Biphenyl Market was valued at USD 290 million in 2025 and is estimated to grow at a CAGR of 5.7% to reach USD 505.5 million by 2035.

Market growth is driven by the rising demand for biphenyl in the production of specialty chemicals. The pharmaceutical and agrochemical sectors increasingly rely on high-purity intermediates, making biphenyl a critical component in complex molecular formulations. Stricter regulatory requirements on chemical purity and performance are encouraging manufacturers to adopt biphenyl-based compounds for their stability and predictable results. Another significant driver is the expanding use of biphenyl as a heat transfer fluid and industrial solvent. Its excellent thermal stability and solubility make it ideal for high-performance industrial applications, particularly in the petrochemical and automotive sectors. Environmental and regulatory considerations also support biphenyl adoption, as its well-characterized safety profile and predictable behavior make it suitable for coatings, adhesives, plastics, and other regulated applications. Overall, the market is benefiting from a combination of industrial recovery, energy efficiency initiatives, and the need for reliable, compliant chemical solutions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $290 Million |

| Forecast Value | $505.5 Million |

| CAGR | 5.7% |

The technical-grade biphenyl segment will grow at a CAGR of 4.1% through 2035 due to the increasing replacement of lower-purity products with higher-purity biphenyl in more advanced and high-performance applications. Industries requiring stringent quality standards and enhanced chemical performance are favoring ultra-pure grades, which offer superior stability, consistency, and reactivity. This shift is limiting the demand for technical-grade biphenyl, which is primarily used in less complex applications where absolute purity is not a critical requirement.

The solid biphenyl segment is projected to capture 45% share in 2025, driven by its widespread use in pharmaceuticals, agrochemicals, and the production of specialty chemicals. Its popularity is supported by steady shipment growth at a CAGR of 5.4%. Solid biphenyl offers several operational advantages, including ease of handling, precise dosing capabilities, and stable storage properties, making it an ideal choice for applications requiring controlled and consistent chemical performance.

North America Biphenyl Market is expected to grow at a CAGR of 6.7% during 2026-2035. The region represents a mature and highly regulated market, where demand is primarily concentrated in pharmaceutical production, specialty chemical manufacturing, and established uses such as heat transfer fluids. Growth in the region is relatively stable, largely driven by regulatory compliance, incremental technological upgrades, and the need for consistent, high-quality products. Competitive differentiation in North America is increasingly shaped by factors such as innovation in application development, sustainable manufacturing practices, and advanced purification processes that enhance product performance and reliability.

Key companies active in the Global Biphenyl Market include Kishida Chemical Co., Ltd., Thermo Fisher Scientific, Eastman Chemical Company, Otto Chemie Pvt. Ltd., Ennore India Chemicals, and others. Market participants are strengthening their position by expanding high-purity biphenyl production capabilities, developing cleaner and more efficient synthesis processes, and diversifying feedstock sources to natural gas-based routes. Companies are also investing in R&D to enhance biphenyl applications in specialty chemicals, heat transfer media, and industrial solvents. Strategic partnerships with downstream chemical manufacturers and regional expansion initiatives help firms secure long-term contracts and global market share.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Purity

- 2.2.3 Physical Form

- 2.2.4 Application

- 2.2.5 End Use Industry

- 2.2.6 Distribution Channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising pharmaceutical API production driving demand for ultra-high-purity biphenyl intermediates

- 3.2.1.2 Growing adoption of biphenyl-based heat transfer fluids across industrial thermal management systems

- 3.2.1.3 Expanding high-performance polymer usage in aerospace, electronics, and advanced engineering plastics

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent environmental regulations and PCB contamination concerns limiting production flexibility and approvals

- 3.2.2.2 Volatile benzene feedstock pricing impacting production economics and long-term pricing stability

- 3.2.2.3 Increasing competition from alternative heat transfer fluids and substitute chemical synthesis pathways

- 3.2.3 Market opportunities

- 3.2.3.1 Commercialization of bio-based and green-chemistry biphenyl production technologies

- 3.2.3.2 Rapid expansion of electronics manufacturing requiring ultra-pure biphenyl for OLED and semiconductor applications

- 3.2.3.3 Untapped demand in emerging Asia Pacific and Latin American industrializing economies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By purity grade

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Purity Grade, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Pharmaceutical Grade (≥99.5%)

- 5.3 Industrial Grade (99-99.5%)

- 5.4 Technical Grade (95-99%)

Chapter 6 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Solid Form

- 6.2.1 Flakes

- 6.2.2 Powder

- 6.2.3 Crystals

- 6.3 Molten/Liquid Form

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Chemical Synthesis Intermediate

- 7.3 Heat Transfer Agent

- 7.4 Specialty Applications

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Pharmaceutical Industry

- 8.3 Agrochemical Industry

- 8.4 Polymer & Plastics Industry

- 8.5 Electronics & Electrical Industry

- 8.6 Heat Transfer Fluid Industry

- 8.7 Other Industries

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 Direct Sales (Manufacturer to End-User)

- 9.3 Chemical Distributors & Wholesalers

- 9.4 Specialty Chemical Suppliers

Chapter 10 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 BASF SE

- 11.2 Dow Inc.

- 11.3 Eastman Chemical Company

- 11.4 Huntsman Corporation

- 11.5 Jiangsu Zhongneng Chemical Technology Co., Ltd.

- 11.6 LANXESS AG

- 11.7 Merck KGaA

- 11.8 Mitsubishi Chemical Corporation

- 11.9 Solvay S.A.

- 11.10 Tokyo Chemical Industry Co., Ltd