|

市場調查報告書

商品編碼

1959593

2026 年至 2035 年二手相機和鏡頭的市場機會、成長要素、產業趨勢和預測。Secondhand Camera and Lens Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

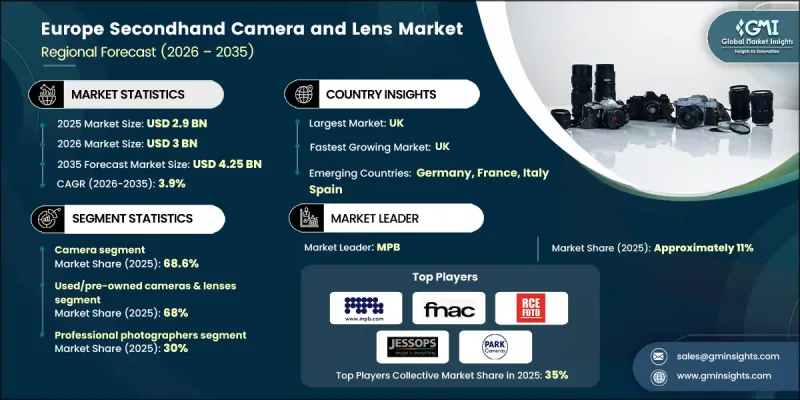

2025年全球二手相機和鏡頭市場價值為29億美元,預計2035年將達到42.5億美元,年複合成長率為3.9%。

二手相機和鏡頭是指已經使用過的影像設備,它們以實惠的價格出售,同時仍能保持足夠的使用壽命。該市場涵蓋數位相機和鏡頭、二手底片設備以及二手專業設備,所有這些產品都能保持其功能性和可靠性,可供長期使用。隨著消費者尋求性價比更高的新產品替代品,以及獲得更先進的設備,二手相機和鏡頭的需求持續成長。在歐洲,二手相機和鏡頭市場正發展成為一個充滿活力且快速成長的細分市場,其驅動力包括價格優勢、永續性意識的增強以及消費者偏好的轉變。隨著新影像設備價格的上漲,基於價值的購買決策正成為買家越來越重要的促進因素。該地區對循環經濟原則的堅定承諾進一步加速了照相機的再利用和轉售,這不僅有助於加強永續性目標,也有利於市場擴張。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 29億美元 |

| 預測金額 | 42.5億美元 |

| 複合年成長率 | 3.9% |

預計到2025年,相機產業將佔據68.6%的市場佔有率,並創造29.2億美元的收入。隨著攝影師向新的系統格式過渡,歐洲二手數位單眼相機市場正經歷顯著擴張,從而形成了高品質的二手數位單眼相機穩定供應。知名全球品牌的二手需求依然強勁,高階機型在二手市場中維持較高的價值。同時,受消費者偏好變化和對舊款數位設備日益成長的興趣的推動,對輕便型相機的需求也呈現出新的成長勢頭。

預計到2025年,二手相機和鏡頭市場將佔據68%的市場佔有率,這表明高價值影像資產的保存和轉售是該行業的基石。二手設備市場構成了歐洲二手攝影器材市場的基礎,其成長動力來自經濟因素、日益增強的永續性意識以及數位轉售平台的擴張。線上市場透過引入標準化的評級系統、認證通訊協定和買家保護措施,提高了透明度和消費者信心,從而改變了買賣流程。

預計到2025年,歐洲二手相機和鏡頭市場將佔據68.6%的市場。促進設備再利用的環保措施持續推動全部區域市場的成長。英國是歐洲最成熟、最成熟的市場之一,這得益於其完善的分銷網路、消費者理性的購買行為以及成熟的攝影社區。長期以來,英國民眾對攝影的文化認同感,加上相關機構和充滿活力的行業網路的支持,使得不同消費群體對高品質二手相機和鏡頭的需求保持穩定。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 向無反光鏡相機過渡及升級週期

- 提高永續性和循環性

- 線上轉售基礎設施的興起

- 產業潛在風險與挑戰

- 對品質差異和保固問題的擔憂

- 假冒風險和有限的認證

- 機會

- 經認證的二手產品和延長保修

- 人工智慧驅動的定價和診斷

- 促進因素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 國家

- 按類型

- 監管環境

- 標準和合規要求

- 區域法規結構

- 認證標準

- 波特的分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 國家

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 其他歐洲地區

- 國家

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章 市場估計與預測:依類型分類,2022-2035年

- 相機

- 鏡片

第6章 市場估價與預測:依產品狀況分類,2022-2035年

- 二手相機和鏡頭

- 翻新相機和鏡頭

第7章 市場估計與預測:依價格區間分類,2022-2035年

- 入門級

- 中檔

- 專業的

- 優質的

第8章 市場估算與預測:依最終使用者分類,2022-2035年

- 專業攝影師

- 半專業

- 以攝影為業餘愛好的人

- 對於教育機構

第9章 市場估計與預測:依地區分類,2022-2035年

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

第10章:公司簡介

- Calumet Photographic

- Canon Inc.

- Fnac

- Foto Erhardt

- Fujifilm Holdings

- Grays of Westminster

- Jessops

- Kamerastore

- Leica Camera AG

- London Camera Exchange(LCE)

- MediaMarkt

- Miss Numerique

- MPB

- Nikon Corporation

- Park Cameras

- RCE Foto

- Saturn

- Sigma Corporation

- Sony Corporation

- Zeiss

The Global Secondhand Camera and Lens Market was valued at USD 2.9 billion in 2025 and is estimated to grow at a CAGR of 3.9% to reach USD 4.25 billion by 2035.

Pre-owned cameras and lenses refer to imaging equipment that has been previously used and resold at more accessible price points while still offering substantial functional lifespan. This market encompasses digital cameras and lenses, pre-owned film equipment, and secondhand professional-grade gear, all of which remain operational and reliable for extended use. Demand continues to rise as consumers seek cost-effective alternatives to new products while gaining access to higher-tier equipment. Across Europe, the secondhand camera and lens market has evolved into a dynamic and fast-growing segment driven by affordability, sustainability awareness, and shifting purchasing preferences. Buyers are increasingly motivated by value-based purchasing decisions as new imaging equipment becomes more expensive. The region's strong commitment to circular economy principles has further accelerated the reuse and resale of photography equipment, reinforcing sustainability goals while supporting market expansion.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.9 Billion |

| Forecast Value | $4.25 Billion |

| CAGR | 3.9% |

In 2025, the camera segment accounted for 68.6% share, generating USD 2.92 billion. The European secondhand DSLR category has experienced notable expansion as photographers transition toward newer system formats, creating a steady supply of high-quality pre-owned DSLR models. Established global brands continue to maintain strong resale demand, with premium models retaining significant value in the resale ecosystem. At the same time, compact camera demand has shown renewed momentum, supported by evolving consumer preferences and renewed interest in earlier-generation digital devices.

The used and pre-owned cameras and lenses segment held 68% share in 2025, underscoring the industry's reliance on preserving and redistributing high-value imaging assets. The pre-owned equipment segment forms the foundation of Europe's secondhand photography market, benefiting from economic considerations, growing sustainability awareness, and the expansion of digital resale platforms. Online marketplaces have transformed the buying and selling process by introducing standardized grading systems, authentication protocols, and buyer protection measures that enhance transparency and consumer confidence.

Europe Secondhand Camera and Lens Market accounted for 68.6% share in 2025. Growth across the region continues to be influenced by environmental initiatives encouraging equipment reuse. The United Kingdom represents one of the most established and mature markets within Europe, supported by advanced distribution networks, informed purchasing behavior, and a well-developed photography community. A long-standing cultural appreciation for photography, supported by institutions and active industry networks, sustains consistent demand for quality secondhand cameras and lenses across diverse consumer groups.

Major companies operating in the Global Secondhand Camera and Lens Market include Calumet Photographic, Canon Inc., Fnac, Foto Erhardt, Fujifilm Holdings, Grays of Westminster, Jessops, Kamerastore, Leica Camera AG, London Camera Exchange (LCE), MediaMarkt, Miss Numerique, MPB, Nikon Corporation, Park Cameras, RCE Foto, Saturn, Sigma Corporation, Sony Corporation, and Zeiss. Companies competing in the secondhand camera and lens market are enhancing their market foothold through digital platform expansion, inventory certification programs, and customer trust initiatives. Many players are investing in advanced grading systems and transparent product authentication to build credibility and reduce purchase risk. Strategic partnerships with logistics providers and refurbishment specialists are improving supply chain efficiency and product quality assurance. Firms are also leveraging omnichannel retail strategies, combining physical stores with online marketplaces to broaden reach. Subscription models, trade-in programs, and warranty-backed resale offerings are strengthening customer loyalty.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Europe

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Country

- 2.2.2 Type

- 2.2.3 Product Condition

- 2.2.4 Price Range

- 2.2.5 End User

- 2.2.6 Distribution Channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Mirrorless shift & upgrade cycles

- 3.2.1.2 Increasing sustainability & circularity

- 3.2.1.3 Rise of online resale infrastructure

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Quality variance and warranty concerns

- 3.2.2.2 Counterfeit risk & limited certification

- 3.2.3 Opportunities

- 3.2.3.1 Certified pre owned & extended warranties

- 3.2.3.2 AI assisted pricing and diagnostics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By Country

- 3.6.2 By Type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Country

- 4.2.1.1 UK

- 4.2.1.2 Germany

- 4.2.1.3 France

- 4.2.1.4 Italy

- 4.2.1.5 Spain

- 4.2.1.6 Netherlands

- 4.2.1.7 Rest of Europe

- 4.2.1 By Country

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 Camera

- 5.3 Lens

Chapter 6 Market Estimates and Forecast, By Product Condition, 2022 - 2035 (USD Million) (Thousand Units)

- 6.1 Key trends

- 6.2 Used/pre-owned cameras & lenses

- 6.3 Refurbished cameras & lenses

Chapter 7 Market Estimates and Forecast, By Price Range, 2022 - 2035 (USD Million) (Thousand Units)

- 7.1 Key trends

- 7.2 Entry-level

- 7.3 Mid-range

- 7.4 Professional

- 7.5 Premium

Chapter 8 Market Estimates and Forecast, By End User, 2022 - 2035 (USD Million) (Thousand Units)

- 8.1 Key trends

- 8.2 Professional Photographers

- 8.3 Semi-Professional

- 8.4 Amateur/Hobbyist

- 8.5 Institutional/Educational

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million) (Thousand Units)

- 9.1 Key trends

- 9.2 Europe

- 9.2.1 Germany

- 9.2.2 UK

- 9.2.3 France

- 9.2.4 Italy

- 9.2.5 Spain

- 9.2.6 Netherlands

Chapter 10 Company Profiles

- 10.1 Calumet Photographic

- 10.2 Canon Inc.

- 10.3 Fnac

- 10.4 Foto Erhardt

- 10.5 Fujifilm Holdings

- 10.6 Grays of Westminster

- 10.7 Jessops

- 10.8 Kamerastore

- 10.9 Leica Camera AG

- 10.10 London Camera Exchange (LCE)

- 10.11 MediaMarkt

- 10.12 Miss Numerique

- 10.13 MPB

- 10.14 Nikon Corporation

- 10.15 Park Cameras

- 10.16 RCE Foto

- 10.17 Saturn

- 10.18 Sigma Corporation

- 10.19 Sony Corporation

- 10.20 Zeiss

餅乾鏡頭市場:2026-2032年全球市場預測(按焦距、光學設計、應用、銷售管道和最終用戶分類)廣角定焦鏡頭市場:以對焦方式、感光元件格式、應用、最終用戶和通路分類-2026-2032年全球預測緊湊型鏡頭產生器市場:按類型、技術、分銷管道、應用、最終用戶分類,全球預測(2026-2032)光學透鏡產生器市場:按類型、技術、材料和應用分類,全球預測(2026-2032年)

餅乾鏡頭市場:2026-2032年全球市場預測(按焦距、光學設計、應用、銷售管道和最終用戶分類)廣角定焦鏡頭市場:以對焦方式、感光元件格式、應用、最終用戶和通路分類-2026-2032年全球預測緊湊型鏡頭產生器市場:按類型、技術、分銷管道、應用、最終用戶分類,全球預測(2026-2032)光學透鏡產生器市場:按類型、技術、材料和應用分類,全球預測(2026-2032年) 可更換鏡頭市場分析及預測(至2035年):依類型、產品類型、技術、組件、應用、材質、設備、最終用戶、功能及安裝類型分類按產品類型、分銷管道、應用和最終用戶分類的定焦鏡頭相機市場-2026-2032年全球預測非球面透鏡市場:2026-2032年全球預測(按產品類型、材料、應用、通路和最終用戶分類)

可更換鏡頭市場分析及預測(至2035年):依類型、產品類型、技術、組件、應用、材質、設備、最終用戶、功能及安裝類型分類按產品類型、分銷管道、應用和最終用戶分類的定焦鏡頭相機市場-2026-2032年全球預測非球面透鏡市場:2026-2032年全球預測(按產品類型、材料、應用、通路和最終用戶分類) 相機鏡頭市場機會、成長要素、產業趨勢分析及2026年至2035年預測

相機鏡頭市場機會、成長要素、產業趨勢分析及2026年至2035年預測 可更換鏡頭市場規模、佔有率和成長分析(按鏡頭類型、相機類型、焦距和地區分類)-2026-2033年產業預測

可更換鏡頭市場規模、佔有率和成長分析(按鏡頭類型、相機類型、焦距和地區分類)-2026-2033年產業預測 全球手機鏡頭市場

全球手機鏡頭市場