|

市場調查報告書

商品編碼

1959576

威脅偵測設備市場機會、成長要素、產業趨勢分析及2026年至2035年預測。Threat Detection Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

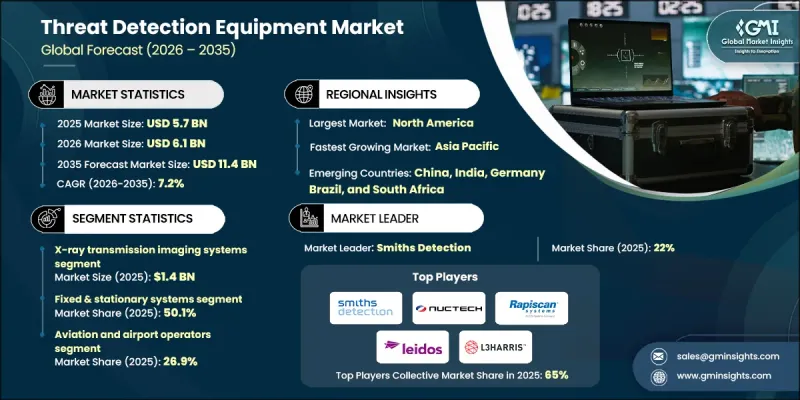

2025 年全球威脅偵測設備市場價值為 57 億美元,預計到 2035 年將達到 114 億美元,年複合成長率為 7.2%。

市場擴張的關鍵促進因素包括更嚴格的航空安全法規、不斷擴大的城市監控基礎設施以及國防和國防安全保障支出的持續成長。此外,貿易量的成長也推動了對能夠應對高風險等級的先進貨物檢查和港口保護技術的需求增加。人工智慧 (AI) 與檢測平台的整合顯著提高了威脅識別的準確性,減少了誤報,並提升了篩檢效率。世界各地的安全機構正在加強旅客、行李和貨物檢查的標準,並加速篩檢基礎設施的現代化。將影像檢查、痕跡偵測、生物識別和輻射監測等技術整合到多層偵測系統中,正在改變產業格局。這一轉變在 2010 年代初開始加速,預計將持續到 2030 年,因為營運商優先考慮擴充性和集中式指揮控制整合。此外,隨著各組織尋求加強其監控能力、最佳化人員配置和加快威脅解決速度,遠端和集中式篩檢模式的採用也正在加速。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 57億美元 |

| 預測金額 | 114億美元 |

| 複合年成長率 | 7.2% |

預計到2025年,X光透射成像系統市場規模將達14億美元。憑藉其久經考驗的可靠性和監管部門的核准,這些系統在交通樞紐、邊境檢查站、貨運設施和人流密集的公共區域中持續保持著較高的應用率。它們能夠以極高的處理速度對行李、小包裹和貨物進行安檢,確保在嚴苛的安全環境下持續穩定運作。完善的訓練體系和熟練的操作技能進一步鞏固了這些系統在高通量安檢環境中的主導地位。

預計到2025年,固定系統市佔率將達到50.1%。這些系統廣泛應用於交通樞紐和關鍵基礎設施,滿足不間斷、高容量的篩檢。穩定的性能、合規性以及與集中式管理平台的兼容性,支撐了市場的長期需求。與廣泛的安全網路整合,實現了協同監控和高效的響應通訊協定,進一步鞏固了公司在威脅偵測設備行業的市場主導地位。

預計到2025年,北美威脅偵測設備市佔率將達到31%。該地區的成長主要得益於嚴格的監管要求、持續的國防安全保障資金投入以及交通和基礎設施資產檢測技術的不斷升級。為了符合不斷變化的聯邦標準和風險管理框架,政府機構和私人企業正在擴大先進成像技術、電腦斷層掃描(CT)、輻射監測和生物識別系統的部署。對人工智慧驅動的分析、自動化檢測通道以及整合指揮控制解決方案的投資正在提高全部區域的檢測精度和營運效率。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 加強全球航空安全措施

- 都市化正在推動智慧城市監控系統的應用。

- 增加國防和國防安全保障預算

- 透過人工智慧分析提高檢測精度

- 跨境貿易與港口成長

- 產業潛在風險與挑戰

- 誤報導致業務中斷

- 舊有系統互通性面臨的挑戰

- 市場機遇

- 對現有檢測系統進行人工智慧維修

- 公私合營安全現代化計劃

- 成長潛力分析

- 監理情勢

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 定價策略

- 新興經營模式

- 合規要求

- 專利和智慧財產權分析

- 地緣政治和貿易趨勢

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 市場集中度分析

- 主要企業的競爭標竿分析

- 財務績效比較

- 收入

- 利潤率

- 研究與開發

- 產品系列比較

- 產品線的廣度

- 科技

- 創新

- 地理位置比較

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導企業

- 受讓人

- 追蹤者

- 小眾玩家

- 戰略展望矩陣

- 財務績效比較

- 主要進展

- 併購

- 夥伴關係與合作

- 技術進步

- 擴張和投資策略

- 數位轉型計劃

- 新興/Start-Ups競爭對手的發展趨勢

第5章 市場估計與預測:依檢測技術分類,2022-2035年

- X光透射成像系統

- 痕跡檢測系統

- 光譜檢測系統

- 輻射探測系統

- 金屬探測系統

- 毫米波成像系統

第6章 市場估計與預測:依已偵測到的威脅類別分類,2022-2035年

- 爆炸物和簡易爆炸裝置(IED)

- 武器和金屬威脅

- 整合威脅偵測系統

- 毒品和走私貨

- 生物製劑

- 化學品和危險工業化學品(TICS)

- 輻射和核材料

第7章 市場估算與預測:依產品類型分類,2022-2035年

- 固定/靜止系統

- 攜帶式/可攜式系統

- 手持裝置

- 車載和移動系統

- 穿戴式檢測系統

第8章 市場估算與預測:依部署類型分類,2022-2035年

- 查核點和門禁篩檢

- 邊界和遠端檢測

- 區域和環境監測

- 移動/巡邏偵測

- 貨物及貨物檢驗

第9章 市場估價與預測:依最終用戶分類,2022-2035年

- 航空公司和機場營運商

- 政府安全和監管機構

- 國防/軍事組織

- 懲教和司法系統的運作者

- 關鍵基礎設施營運商

- 運輸/物流企業經營者

- 私部門

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- 主要企業

- Smith's Detection

- Raytheon Technologies

- Lockheed Martin

- L3Harris Technologies

- Thales

- 按地區分類的主要企業

- 北美洲

- Rapiscan Systems

- Leidos Holdings, Inc.

- FLIR Systems(Teledyne FLIR)

- Analogic Corporation

- 亞太地區

- Nuctech Company Limited

- 歐洲

- Safran Electronics & Defense

- CEIA SpA

- Chemring Group

- 北美洲

- 特殊玩家/干擾者

- Astrophysics Inc.

- Garrett Metal Detectors

- Honeywell International

The Global Threat Detection Equipment Market was valued at USD 5.7 billion in 2025 and is estimated to grow at a CAGR of 7.2% to reach USD 11.4 billion by 2035.

Market expansion is driven by tightening aviation security regulations, expanding urban surveillance infrastructure, and sustained growth in defense and homeland security spending. Increasing global trade flows are also strengthening demand for advanced cargo inspection and port protection technologies capable of managing elevated risk levels. The integration of artificial intelligence into detection platforms is significantly enhancing threat identification accuracy, reducing false positives, and improving screening efficiency. Security authorities worldwide are reinforcing standards for passenger, baggage, and cargo inspection, accelerating the modernization of screening infrastructure. A transition toward multi-layered detection systems that combine imaging, trace detection, biometric verification, and radiation monitoring into unified platforms is reshaping the industry landscape. This shift, which gained traction earlier in the decade, is expected to continue through 2030 as operators prioritize scalability and centralized command integration. Additionally, remote and centralized screening models are gaining momentum as organizations seek improved oversight, workforce optimization, and faster threat resolution.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.7 Billion |

| Forecast Value | $11.4 Billion |

| CAGR | 7.2% |

The X-ray transmission imaging systems segment reached USD 1.4 billion in 2025. These systems maintain strong adoption across transportation hubs, border control points, cargo facilities, and high-traffic public locations due to their proven reliability and regulatory acceptance. Their capability to screen baggage, parcels, and freight at high throughput rates supports continuous operations in demanding security environments. Established training frameworks and operational familiarity further reinforce their leadership position in high-volume inspection settings.

The fixed and stationary systems segment accounted for 50.1% share in 2025. These installations are widely deployed at transportation gateways and critical infrastructure facilities where uninterrupted, high-capacity screening is required. Their consistent performance, regulatory compliance, and compatibility with centralized command platforms sustain long-term demand. Integration with broader security networks enables coordinated monitoring and streamlined response protocols, strengthening their dominant share within the threat detection equipment industry.

North America Threat Detection Equipment Market held 31% share in 2025. Regional growth is supported by stringent regulatory requirements, sustained homeland security funding, and continuous upgrades of inspection technologies across transportation and infrastructure assets. Authorities and private operators are increasingly implementing advanced imaging, computed tomography, radiation monitoring, and biometric systems to align with evolving federal standards and risk management frameworks. Investment in AI-driven analytics, automated inspection lanes, and integrated command-and-control solutions is enhancing detection precision and operational efficiency throughout the region.

Key companies operating in the Global Threat Detection Equipment Market include Smiths Detection, Rapiscan Systems, L3Harris Technologies, Thales, Lockheed Martin, Raytheon Technologies, Safran Electronics & Defense, Nuctech Company Limited, Leidos Holdings, Inc., Honeywell International, Analogic Corporation, Astrophysics Inc., Garrett Metal Detectors, Chemring Group, FLIR Systems (Teledyne FLIR), and CEIA S.p.A. Companies in the Threat Detection Equipment Market are reinforcing their competitive advantage through technology innovation, system integration, and long-term government partnerships. Leading vendors are investing in AI-powered analytics, automation capabilities, and multi-sensor fusion platforms to enhance detection accuracy and reduce inspection time. Strategic collaborations with aviation authorities, defense agencies, and border security organizations support multi-year procurement contracts and recurring service revenue. Firms are also expanding global service networks to provide maintenance, upgrades, and training solutions.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Detection technology trends

- 2.2.2 Threat category detected trends

- 2.2.3 Product form factor trends

- 2.2.4 Deployment mode trends

- 2.2.5 End-User trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Stricter aviation security mandates worldwide

- 3.2.3 Urbanization driving smart city surveillance deployments

- 3.2.4 Increased defense and homeland security budgets

- 3.2.5 AI-powered analytics improving detection accuracy

- 3.2.6 Growth in cross-border trade and ports

- 3.2.7 Industry pitfalls and challenges

- 3.2.8 False alarms causing operational disruptions

- 3.2.9 Interoperability issues across legacy systems

- 3.2.10 Market opportunities

- 3.2.11 AI retrofits for installed detection systems

- 3.2.12 Public-private security modernization programs

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

- 3.13 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Detection Technology, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 X-ray transmission imaging systems

- 5.3 Trace detection systems

- 5.4 Spectroscopy-based detection systems

- 5.5 Radiation detection systems

- 5.6 Metal detection systems

- 5.7 Millimeter-wave imaging systems

Chapter 6 Market Estimates and Forecast, By Threat Category Detected, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Explosives & improvised explosive devices (IEDS)

- 6.3 Weapons & metallic threats

- 6.4 Multi-threat detection systems

- 6.5 Narcotics & contraband

- 6.6 Biological agents

- 6.7 Chemical agents & toxic industrial chemicals (TICS)

- 6.8 Radiological & nuclear materials

Chapter 7 Market Estimates and Forecast, By Product Form Factor, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Fixed & stationary systems

- 7.3 Portable & transportable systems

- 7.4 Handheld devices

- 7.5 Vehicle-mounted & mobile systems

- 7.6 Wearable detection systems

Chapter 8 Market Estimates and Forecast, By Deployment Mode, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Checkpoint & access control screening

- 8.3 Perimeter & standoff detection

- 8.4 Area & ambient monitoring

- 8.5 Mobile & patrol-based detection

- 8.6 Cargo & freight inspection

Chapter 9 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Aviation & airport operators

- 9.3 Government security & regulatory agencies

- 9.4 Defense & military organizations

- 9.5 Corrections & justice system operators

- 9.6 Critical infrastructure operators

- 9.7 Transportation & logistics operators

- 9.8 Commercial & private sector

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 Smith's Detection

- 11.1.2 Raytheon Technologies

- 11.1.3 Lockheed Martin

- 11.1.4 L3Harris Technologies

- 11.1.5 Thales

- 11.2 Regional key players

- 11.2.1 North America

- 11.2.1.1 Rapiscan Systems

- 11.2.1.2 Leidos Holdings, Inc.

- 11.2.1.3 FLIR Systems (Teledyne FLIR)

- 11.2.1.4 Analogic Corporation

- 11.2.2 Asia Pacific

- 11.2.2.1 Nuctech Company Limited

- 11.2.3 Europe

- 11.2.3.1 Safran Electronics & Defense

- 11.2.3.2 CEIA S.p.A.

- 11.2.3.3 Chemring Group

- 11.2.1 North America

- 11.3 Niche Players/Disruptors

- 11.3.1 Astrophysics Inc.

- 11.3.2 Garrett Metal Detectors

- 11.3.3 Honeywell International

電子安防系統市場:依系統類型、技術、服務類型及最終用戶分類-2026-2032年全球市場預測

電子安防系統市場:依系統類型、技術、服務類型及最終用戶分類-2026-2032年全球市場預測 2026年東西方威脅偵測設備全球市場報告

2026年東西方威脅偵測設備全球市場報告 威脅偵測設備市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終使用者、功能及安裝類型分類監獄郵件偵測與安全系統市場分析及預測(至2035年):依類型、產品、服務、技術、組件、應用、最終使用者、功能及安裝類型分類

威脅偵測設備市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終使用者、功能及安裝類型分類監獄郵件偵測與安全系統市場分析及預測(至2035年):依類型、產品、服務、技術、組件、應用、最終使用者、功能及安裝類型分類 電子安防市場機會、成長要素、產業趨勢分析及2026年至2035年預測2026年全球攜帶式工作站市場報告2026年全球安防機器人指揮顯示市場報告2026年全球電子安防市場報告

電子安防市場機會、成長要素、產業趨勢分析及2026年至2035年預測2026年全球攜帶式工作站市場報告2026年全球安防機器人指揮顯示市場報告2026年全球電子安防市場報告 電子安防市場-全球產業規模、佔有率、趨勢、機會及預測(依產品類型、終端用戶產業、地區及競爭格局分類,2020-2030 年預測)

電子安防市場-全球產業規模、佔有率、趨勢、機會及預測(依產品類型、終端用戶產業、地區及競爭格局分類,2020-2030 年預測) 電子安全系統市場:2025-2030 年預測

電子安全系統市場:2025-2030 年預測