|

市場調查報告書

商品編碼

1959557

電子安防市場機會、成長要素、產業趨勢分析及2026年至2035年預測Electronic Security Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

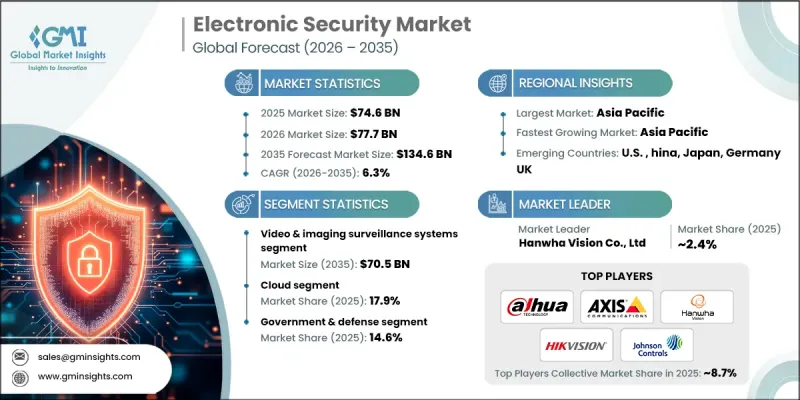

2025 年全球電子安防市場價值為 746 億美元,預計到 2035 年將達到 1,346 億美元,年複合成長率為 6.3%。

全球安全情勢日益嚴峻、技術持續創新以及跨行業監管要求日益嚴格,共同推動了市場擴張。智慧城市計畫的不斷普及,以及人們對家庭和企業遠端監控功能的日益關注,進一步刺激了市場需求。硬體成本的降低和雲端平台的興起,使得企業能夠開發擴充性的整合式安防系統,以滿足不斷變化的需求。電子安防涵蓋了旨在保護人員、財產和資產的解決方案,這些方案利用視訊監控、門禁控制、入侵檢測系統、生物識別和高級監控軟體等設備。人工智慧和機器學習的融合是關鍵趨勢,使系統能夠偵測異常情況、預測威脅並自動回應。這些進步正促使企業、政府和住宅用戶擴大利用智慧互聯的安防解決方案,以提高安全性和營運效率。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 746億美元 |

| 預測金額 | 1346億美元 |

| 複合年成長率 | 6.3% |

預計到2025年,門禁系統市場規模將達到188億美元,並在2035年之前維持7.1%的複合年成長率。該行業正朝著生物識別和非接觸式解決方案轉型,例如指紋識別、臉部認證辨識和虹膜辨識,從而提升安全性並增強用戶便利性。行動認證日益普及,用戶可以透過智慧型手機進行遠端存取。同時,物聯網和雲端整合為商業設施、醫療機構和關鍵基礎設施提供了集中管理、即時監控和警報功能。

預計到2025年,雲端安全解決方案的市佔率將達到17.9%,顯示基於雲端的安全平台正被迅速採用。這些系統具有擴充性、遠端系統管理,並降低了硬體需求,使企業能夠安全地儲存視訊資料、利用人工智慧分析,並透過單一介面監控多個位置。與行動和物聯網技術的進一步整合增強了柔軟性,使雲端平台成為企業、智慧城市和住宅用戶的理想選擇。

預計到2025年,北美電子安防市佔率將達到26.9%。該地區的成長主要得益於住宅、商業和公共部門的廣泛應用,尤其是與雲端平台、人工智慧分析和先進存取管理技術的整合。公共舉措充分利用監控和自動化監控,而個人用戶也擴大採用具備遠端存取和即時警報功能的連網安防系統。政府計畫也持續加強基礎設施建設,作為更廣泛的安全和犯罪預防策略的一部分。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率分析

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 犯罪率上升,公共安全問題令人擔憂

- 行動應用與DIY智慧家庭安防的融合。

- 對遠端監控和雲端安全的需求

- 商業和工業設施的擴建

- 無線和行動技術的不斷進步

- 產業潛在風險與挑戰

- 較高的初始實施和整合成本

- 對資料隱私和監控法規的擔憂

- 市場機遇

- 老舊公共基礎設施的安全現代化

- 醫療機構電子安防的擴展

- 促進因素

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 新興經營模式

- 合規要求

- 專利和智慧財產權分析

- 地緣政治和貿易趨勢

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 主要企業的競爭標竿分析

- 財務績效比較

- 收入

- 利潤率

- 研究與開發

- 產品系列比較

- 產品線的廣度

- 科技

- 創新

- 區域擴張比較

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導企業

- 受讓人

- 追蹤者

- 小眾玩家

- 戰略展望矩陣

- 財務績效比較

- 2021-2024 年重大發展

- 併購

- 合作夥伴關係和合資企業

- 技術進步

- 擴張和投資策略

- 數位轉型計劃

- 新興/Start-Ups競爭對手的發展趨勢

第5章 市場估計與預測:依系統類型分類,2022-2035年

- 影像監控系統

- 門禁系統

- 入侵偵測和周界安全系統

- 整合生命安全系統

- 其他

第6章 市場估算與預測:依部署模式分類,2022-2035年

- 現場

- 基於雲端的

- 混合

第7章 市場估計與預測:依最終用戶產業分類,2022-2035年

- 政府/國防

- 適用於商業和企業用途

- 零售與消費空間

- 飯店和娛樂

- 工業和製造業

- 住宅住宅相關

- 衛生保健

- 教育

- 其他

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- Hikvision Digital Technology Co., Ltd.

- Dahua Technology Co., Ltd.

- Axis Communications AB

- Hanwha Vision Co., Ltd.

- Bosch Security Systems

- Honeywell International Inc.

- Johnson Controls International

- Motorola Solutions, Inc.

- ASSA ABLOY

- Allegion plc

- Dormakaba Holding AG

- Siemens

- HID Global

- Avigilon

- FLIR Systems

- Genetec Inc.

- Panasonic

- Hanwha

The Global Electronic Security Market was valued at USD 74.6 billion in 2025 and is estimated to grow at a CAGR of 6.3% to reach USD 134.6 billion by 2035.

The market expansion is driven by increasing global security concerns, continuous technological innovation, and stricter regulatory requirements across industries. Growing adoption of smart city initiatives, coupled with rising awareness of remote monitoring capabilities for homes and businesses, is further fueling demand. The declining cost of hardware, alongside the emergence of cloud-based platforms, enables companies to develop scalable, integrated security systems to meet evolving needs. Electronic security encompasses solutions designed to protect people, property, and assets using devices such as video surveillance, access control, intrusion detection systems, biometrics, and advanced monitoring software. Integration of AI and machine learning is a key trend, allowing systems to detect anomalies, predict threats, and respond automatically. With these advancements, businesses, governments, and residential users are increasingly leveraging intelligent and connected security solutions to enhance safety and operational efficiency.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $74.6 Billion |

| Forecast Value | $134.6 Billion |

| CAGR | 6.3% |

The access control systems segment reached USD 18.8 billion in 2025 and is expected to grow at a CAGR of 7.1% through 2035. The segment is shifting toward biometric and contactless solutions, including fingerprint, facial, and iris recognition, improving security and user convenience. Mobile credentialing is gaining traction, allowing remote access through smartphones, while IoT and cloud integration provide centralized control, real-time monitoring, and alerts across commercial, healthcare, and critical infrastructure facilities.

The cloud segment accounted for 17.9% share in 2025, reflecting strong adoption of cloud-based security platforms. These systems offer scalability, remote management, and reduced hardware requirements, enabling organizations to securely store video data, utilize AI analytics, and monitor multiple locations from a single interface. Mobile and IoT integration further enhances flexibility, making cloud platforms attractive for businesses, smart cities, and residential users.

North America Electronic Security Market captured 26.9% share in 2025. Growth in the region is fueled by widespread deployment across residential, commercial, and public sectors, including integration with cloud platforms, AI analytics, and advanced access management technologies. Public safety initiatives leverage surveillance and automated monitoring, while private users increasingly adopt connected security systems with remote access and real-time alerts. Government programs continue to strengthen infrastructure as part of broader safety and crime prevention strategies.

Leading players in the Global Electronic Security Market include Axis Communications, Allegion, Dahua Technology, Honeywell Security, Johnson Controls Security, Milestone Systems, ASSA ABLOY, Bosch Security Product Biz, Hikvision Digital Technology Co., Ltd., Resideo Security, Siemens SI Security, Secom, Hanwha Vision, TKH Group, and Motorola Solutions Video & Access. Companies in the electronic security market are strengthening their position through investment in AI-driven analytics, IoT integration, and cloud-based monitoring platforms. Many are expanding product portfolios to include biometric and mobile access solutions to meet rising demand for secure, contactless access. Strategic partnerships with smart city initiatives, government agencies, and commercial enterprises enable early adoption and long-term contracts. Emphasis on cybersecurity, product reliability, and real-time monitoring capabilities enhances customer trust.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 System type trends

- 2.2.2 Deployment model trends

- 2.2.3 End-user industry trends

- 2.2.4 Regional trends

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising crime and public safety concerns

- 3.2.1.2 Convergence of mobile applications and DIY smart home security

- 3.2.1.3 Demand for remote monitoring and cloud security

- 3.2.1.4 Expansion of commercial and industrial facilities

- 3.2.1.5 Growing advancement in wireless and mobile technologies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial installation and integration costs

- 3.2.2.2 Data privacy and surveillance regulation concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Security modernization in aging public infrastructure

- 3.2.3.2 Expansion of electronic security in healthcare facilities

- 3.2.1 Growth drivers

- 3.3 Regulatory landscape

- 3.3.1 North America

- 3.3.2 Europe

- 3.3.3 Asia Pacific

- 3.3.4 Latin America

- 3.3.5 Middle East & Africa

- 3.4 Porter’s analysis

- 3.5 PESTEL analysis

- 3.6 Technology and innovation landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Emerging business models

- 3.8 Compliance requirements

- 3.9 Patent and IP analysis

- 3.10 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By System Type, 2022 - 2035 (USD Mn)

- 5.1 Key trends

- 5.2 Video & Imaging Surveillance Systems

- 5.3 Access Control Systems

- 5.4 Intrusion & Perimeter Detection Systems

- 5.5 Life-Safety Integration Systems

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Deployment Model, 2022 - 2035 (USD Mn)

- 6.1 Key trends

- 6.2 On-Premises

- 6.3 Cloud-Based

- 6.4 Hybrid

Chapter 7 Market Estimates and Forecast, By End-User Industry, 2022 - 2035 (USD Mn)

- 7.1 Key trends

- 7.2 Government & Defense

- 7.3 Commercial & Corporate

- 7.4 Retail & Consumer Spaces

- 7.5 Hospitality & Entertainment

- 7.6 Industrial & Manufacturing

- 7.7 Residential & Housing

- 7.8 Healthcare

- 7.9 Education

- 7.10 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Hikvision Digital Technology Co., Ltd.

- 9.2 Dahua Technology Co., Ltd.

- 9.3 Axis Communications AB

- 9.4 Hanwha Vision Co., Ltd.

- 9.5 Bosch Security Systems

- 9.6 Honeywell International Inc.

- 9.7 Johnson Controls International

- 9.8 Motorola Solutions, Inc.

- 9.9 ASSA ABLOY

- 9.10 Allegion plc

- 9.11 Dormakaba Holding AG

- 9.12 Siemens

- 9.13 HID Global

- 9.14 Avigilon

- 9.15 FLIR Systems

- 9.16 Genetec Inc.

- 9.17 Panasonic

- 9.18 Hanwha

電子安防系統市場:依系統類型、技術、服務類型及最終用戶分類-2026-2032年全球市場預測

電子安防系統市場:依系統類型、技術、服務類型及最終用戶分類-2026-2032年全球市場預測 2026年東西方威脅偵測設備全球市場報告

2026年東西方威脅偵測設備全球市場報告 威脅偵測設備市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終使用者、功能及安裝類型分類

威脅偵測設備市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終使用者、功能及安裝類型分類 威脅偵測設備市場機會、成長要素、產業趨勢分析及2026年至2035年預測。監獄郵件偵測與安全系統市場分析及預測(至2035年):依類型、產品、服務、技術、組件、應用、最終使用者、功能及安裝類型分類2026年全球攜帶式工作站市場報告2026年全球安防機器人指揮顯示市場報告2026年全球電子安防市場報告

威脅偵測設備市場機會、成長要素、產業趨勢分析及2026年至2035年預測。監獄郵件偵測與安全系統市場分析及預測(至2035年):依類型、產品、服務、技術、組件、應用、最終使用者、功能及安裝類型分類2026年全球攜帶式工作站市場報告2026年全球安防機器人指揮顯示市場報告2026年全球電子安防市場報告 電子安防市場-全球產業規模、佔有率、趨勢、機會及預測(依產品類型、終端用戶產業、地區及競爭格局分類,2020-2030 年預測)

電子安防市場-全球產業規模、佔有率、趨勢、機會及預測(依產品類型、終端用戶產業、地區及競爭格局分類,2020-2030 年預測) 電子安全系統市場:2025-2030 年預測

電子安全系統市場:2025-2030 年預測