|

市場調查報告書

商品編碼

1959555

農業機械租賃市場機會、成長要素、產業趨勢分析及2026年至2035年預測。Farm Equipment Rental Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

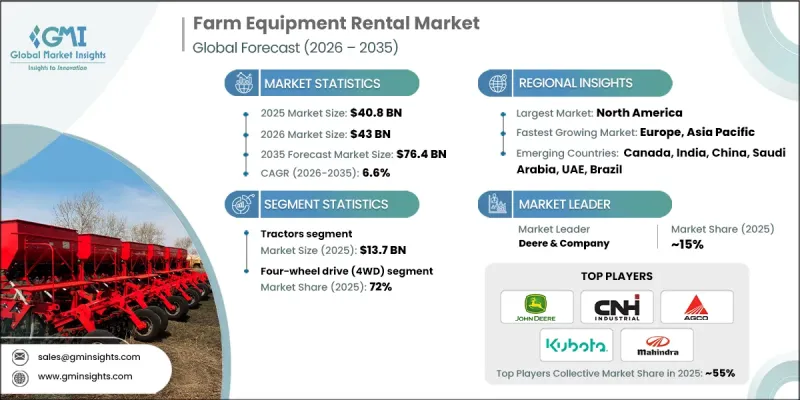

2025年全球農業機械租賃市場價值408億美元,預計2035年將達764億美元,年複合成長率為6.6%。

該市場的成長源自於購買現代農業機械的高成本。現代曳引機、收割機、噴霧器和其他設備融合了精密農業技術、自動化功能和高功率,導致擁有成本不斷攀升。租賃公司順應此趨勢,提供種類繁多的機械,以滿足不同作物類型、田間條件和耕作需求。農民現在可以租用從基本曳引機到專業收割機和精準噴霧器等先進設備,而無需承擔購買的經濟負擔。鑑於天氣不確定性、農產品價格波動、投入成本上漲和勞動力短缺等因素導致農民收入不穩定,對財務柔軟性的需求成為推動市場發展的主要動力。機械租賃使農民能夠將資源集中用於關鍵投入,這在融資管道有限的地區尤其具有吸引力。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 408億美元 |

| 預測金額 | 764億美元 |

| 複合年成長率 | 6.6% |

預計到2025年,曳引機市場規模將達到137億美元,並在2026年至2035年間以6.4%的複合年成長率成長。曳引機用途廣泛,能夠勝任犁地、翻土、運輸、播種和土地準備等多種作業,因此租賃需求強勁,尤其是在那些可能難以負擔購置曳引機的中小農戶群體中。曳引機租賃服務使用戶能夠使用現代化、節能且技術先進的機型,而無需承擔維護、儲存和折舊免稅額的負擔。季節性農業週期會造成需求高峰期,因此臨時租賃曳引機對於及時進行農務至關重要,並進一步推動了市場成長。

預計到2025年,四輪驅動(4WD)曳引機市佔率將達到72%,並在2035年之前以6.7%的複合年成長率成長。四輪驅動設備因其卓越的牽引力、增強的穩定性和整體牽引力而日益受到青睞,使其成為深耕、大規模犁地以及操作複雜附件等重型農業作業的理想選擇。隨著農場規模的擴大和機械化技術的進步,對能夠在複雜地形上高效運作的堅固耐用的四輪驅動機械的需求持續成長,使得租賃成為比傳統兩輪驅動設備更實用的解決方案。

美國農業機械租賃市場預計到2025年將達到132億美元,並在2026年至2035年間以6.3%的複合年成長率成長。全美各地的農民擴大使用租賃服務來降低購買高科技、高性能機械的前期成本。投入價格上漲、大宗商品市場波動以及氣候變遷帶來的不確定性,正促使中小農戶轉向更靈活、更經濟的租賃解決方案。精密農業、自動化和智慧機械的快速發展進一步提升了租賃服務的吸引力,使農民能夠在無需承擔長期購置機械的財務負擔的情況下,緊跟技術發展步伐,因為購買的設備很快就會過時。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 新農業機械高成本

- 租賃公司提供各種設備。

- 全球範圍內,減輕農民經濟負擔的需求日益成長。

- 對生產力和營運效率的需求日益成長

- 產業潛在風險與挑戰

- 政府主導的措施和擴大購買新型農業機械的補貼

- 發展中國家缺乏安全法規所帶來的問題

- 促進因素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 透過裝置

- 監理情勢

- 標準和合規要求

- 區域法規結構

- 認證標準

- 貿易統計

- 主要進口國

- 主要出口國

- 波特的分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 公司矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章 市場估算與預測:依設備類型分類,2022-2035年

- 聯結機

- 收割機

- 噴霧器

- 打包機

- 其他

第6章 市場估計與預測:依驅動系統分類,2022-2035年

- 兩輪驅動(2WD)

- 四輪驅動(4WD)

第7章 市場估計與預測:依產量分類,2022-2035年

- 30馬力

- 31-70馬力

- 71-130馬力

- 131-250馬力

- 250馬力以上

第8章 市場估計與預測:依技術分類,2022-2035年

- 短期

- 中期

- 長期

第9章 市場估計與預測:依電源類型分類,2022-2035年

- 柴油引擎

- 電

- 油壓

- 氣動型

第10章 市場估價與預測:依應用領域分類,2022-2035年

- 犁地和土壤準備

- 播種和種植

- 植物保護/施肥

- 收割和脫粒

- 後處理

- 畜牧業相關用途

- 森林農場活動

第11章 市場估價與預測:依最終用戶分類,2022-2035年

- 私人農場主

- 農業合作社

- 商業農場

- 政府機構

- 研究機構

第12章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 印尼

- 馬來西亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

第13章:公司簡介

- AGCO Corporation

- Bobcat Company

- Case IH

- Caterpillar(CAT)

- Claas

- CNH Industrial

- Deere &Company

- Fendt

- JCB

- Kubota Corporation

- Mahindra &Mahindra

- Massey Ferguson

- New Holland Agriculture

- SDF Group(Same Deutz-Fahr)

- Yanmar

The Global Farm Equipment Rental Market was valued at USD 40.8 billion in 2025 and is estimated to grow at a CAGR of 6.6% to reach USD 76.4 billion by 2035.

The market is propelled by the high costs of acquiring modern agricultural machinery. Today's tractors, harvesters, sprayers, and other equipment come equipped with precision farming technologies, automation features, and high-horsepower capabilities, making ownership increasingly expensive. Rental companies are responding by providing an expansive range of machinery suited to diverse crop types, field conditions, and farming operations. Farmers can now access advanced equipment, from basic tractors to specialized harvesters and precision sprayers, without the financial burden of full ownership. The need for financial flexibility is a major factor driving the market, as farmers face volatile incomes due to unpredictable weather, fluctuating commodity prices, rising input costs, and labor shortages. Renting machinery allows farmers to allocate resources to critical inputs, making rentals particularly appealing in regions where access to credit is limited.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $40.8 Billion |

| Forecast Value | $76.4 Billion |

| CAGR | 6.6% |

The tractors segment generated USD 13.7 billion in 2025 and is expected to grow at a CAGR of 6.4% from 2026 to 2035. Their versatility in performing tasks such as plowing, tilling, hauling, planting, and land preparation ensures strong rental demand, especially among small and mid-sized farmers who cannot afford ownership. Renting tractors provides access to modern, fuel-efficient, and technologically advanced models without the burden of maintenance, storage, or depreciation. Seasonal farming cycles create peak demand periods, making temporary tractor rentals essential for timely field operations, further fueling market growth.

The four-wheel drive (4WD) tractors segment held 72% share in 2025 and is anticipated to grow at a CAGR of 6.7% through 2035. 4WD equipment is increasingly preferred for its higher traction, enhanced stability, and superior pulling power, making it ideal for heavy-duty farming activities such as deep tillage, large-scale plowing, and handling complex attachments. As farm sizes expand and mechanization becomes more prevalent, the demand for robust 4WD machinery that can operate efficiently on challenging terrains continues to rise, positioning rentals as a practical solution compared to traditional two-wheel drive machines.

U.S. Farm Equipment Rental Market reached USD 13.2 billion in 2025 and is projected to grow at a CAGR of 6.3% from 2026 to 2035. Farmers across the country are increasingly adopting rental services to reduce upfront costs associated with purchasing high-tech, high-performance machinery. Rising input prices, unpredictable commodity markets, and climate-related uncertainties are driving small and medium-sized operators toward more flexible and cost-efficient rental solutions. Rapid advancements in precision agriculture, automation, and smart machinery mean that equipment can quickly become outdated if purchased outright, further boosting the attractiveness of rental services for staying technologically current without long-term financial commitment.

Key players in the Global Farm Equipment Rental Market include Fendt, Kubota Corporation, Mahindra & Mahindra, Case IH, CNH Industrial, Claas, JCB, Massey Ferguson, New Holland Agriculture, AGCO Corporation, Bobcat Company, Deere & Company, Caterpillar (CAT), SDF Group (Same Deutz-Fahr), and Yanmar. Companies in the farm equipment rental market are adopting multiple strategies to strengthen their market foothold. They are expanding rental fleets to offer a wider variety of machinery, including specialized and high-tech models. Strategic partnerships with financial institutions and government programs help increase accessibility for small and mid-sized farmers. Firms are also investing in maintenance and logistics solutions to ensure equipment availability, reliability, and quick deployment during peak seasons. Technological integration, such as GPS-enabled tracking, IoT-based monitoring, and digital rental platforms, enhances operational efficiency and user experience.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Equipment type

- 2.2.3 Drive type

- 2.2.4 Power output

- 2.2.5 Rental duration

- 2.2.6 Power source

- 2.2.7 Application

- 2.2.8 End user

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 High cost of new farm equipment

- 3.2.1.2 Diverse equipment offerings by rental companies

- 3.2.1.3 Increasing need to reduce the financial burden on farmers across the globe

- 3.2.1.4 Growing demand for productivity and operational efficiency

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Growing government initiatives and subsidies for purchasing new farm equipment

- 3.2.2.2 Problems related to lack of safety-related regulation in developing countries

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By equipment type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Equipment Type, 2022 - 2035, (USD Billion)

- 5.1 Key trends

- 5.2 Tractors

- 5.3 Harvesters

- 5.4 Sprayers

- 5.5 Balers

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Drive Type, 2022 - 2035, (USD Billion)

- 6.1 Key trends

- 6.2 Two-wheel drive (2WD)

- 6.3 Four-wheel drive (4WD)

Chapter 7 Market Estimates & Forecast, By Power Output, 2022 - 2035, (USD Billion)

- 7.1 Key trends

- 7.2 30 HP

- 7.3 31-70 HP

- 7.4 71-130 HP

- 7.5 131-250 HP

- 7.6 >250HP

Chapter 8 Market Estimates & Forecast, By Technology, 2022 - 2035, (USD Billion)

- 8.1 Key trends

- 8.2 Short-term

- 8.3 Medium-term

- 8.4 Long-term

Chapter 9 Market Estimates & Forecast, By Power Source, 2022 - 2035, (USD Billion)

- 9.1 Key trends

- 9.2 Diesel

- 9.3 Electric

- 9.4 Hydraulic

- 9.5 Pneumatic

Chapter 10 Market Estimates & Forecast, By Application, 2022 - 2035, (USD Billion)

- 10.1 Key trends

- 10.2 Plowing & soil preparation

- 10.3 Sowing & planting

- 10.4 Plant protection & fertilization

- 10.5 Harvesting & threshing

- 10.6 Post-harvest operations

- 10.7 Livestock-related applications

- 10.8 Forest farm activities

Chapter 11 Market Estimates & Forecast, By End User, 2022 - 2035, (USD Billion)

- 11.1 Key trends

- 11.2 Individual farmers

- 11.3 Agricultural cooperatives

- 11.4 Commercial farms

- 11.5 Government agencies

- 11.6 Research institutions

Chapter 12 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Million Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 South Korea

- 12.4.5 Australia

- 12.4.6 Indonesia

- 12.4.7 Malaysia

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.6 MEA

- 12.6.1 Saudi Arabia

- 12.6.2 UAE

- 12.6.3 South Africa

Chapter 13 Company Profiles

- 13.1 AGCO Corporation

- 13.2 Bobcat Company

- 13.3 Case IH

- 13.4 Caterpillar (CAT)

- 13.5 Claas

- 13.6 CNH Industrial

- 13.7 Deere & Company

- 13.8 Fendt

- 13.9 JCB

- 13.10 Kubota Corporation

- 13.11 Mahindra & Mahindra

- 13.12 Massey Ferguson

- 13.13 New Holland Agriculture

- 13.14 SDF Group (Same Deutz-Fahr)

- 13.15 Yanmar

農業機械租賃市場-2026-2032年全球市場預測

農業機械租賃市場-2026-2032年全球市場預測 農業機械租賃市場:市場規模、佔有率和趨勢分析(按機器類型、驅動系統、租賃方式和應用分類),細分市場預測(2026-2033 年)

農業機械租賃市場:市場規模、佔有率和趨勢分析(按機器類型、驅動系統、租賃方式和應用分類),細分市場預測(2026-2033 年) 農業機械租賃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

農業機械租賃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 全球農業機械租賃市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球農業機械租賃市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026-2034年農業機械租賃市場規模、佔有率、趨勢及預測(依設備類型、傳動系統、功率輸出及地區分類)

2026-2034年農業機械租賃市場規模、佔有率、趨勢及預測(依設備類型、傳動系統、功率輸出及地區分類) 農業設備租賃市場規模、佔有率和成長分析(按設備類型、產量和地區分類)—產業預測(2026-2033 年)

農業設備租賃市場規模、佔有率和成長分析(按設備類型、產量和地區分類)—產業預測(2026-2033 年) 2030 年農業設備租賃市場預測:按機器類型、驅動類型、功率、租賃類型、所有權類型、應用和地區進行的全球分析

2030 年農業設備租賃市場預測:按機器類型、驅動類型、功率、租賃類型、所有權類型、應用和地區進行的全球分析