|

市場調查報告書

商品編碼

1959331

自修復聚合物市場機會、成長要素、產業趨勢分析及2026年至2035年預測。Self-Healing Polymers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

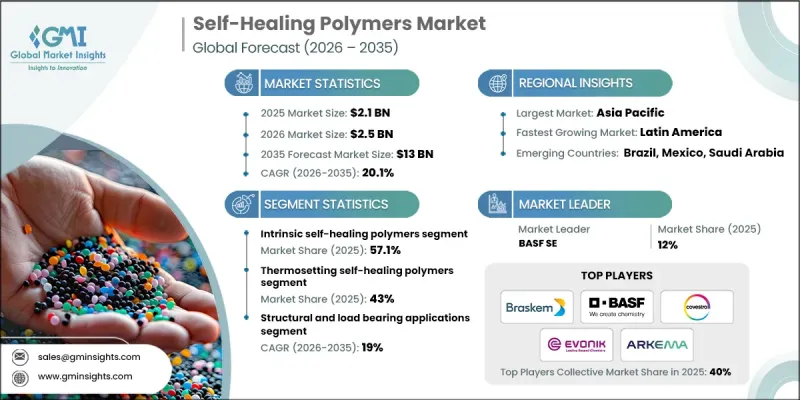

2025 年全球自修復聚合物市場價值為 21 億美元,預計到 2035 年將達到 130 億美元,複合年成長率為 20.1%。

自修復聚合物已從早期的實驗室概念發展成為具有商業性可行性的材料,尤其是在2022年至2025年間,隨著工業領域對耐久性、延長使用壽命和最佳化性能的日益重視,這一發展趨勢尤為顯著。學術和技術文獻中關於自修復聚合物的顯著成長表明,動態分子網路和響應性化學體系的創新正在不斷拓展,這些創新能夠實現材料的自主修復。研究活動的激增與製造商對能夠在損傷後恢復功能的尖端材料日益成長的需求密切相關。市場需求的驅動力在於對能夠減少維護需求、最大限度減少停機時間並提高長期可靠性的材料的需求不斷成長。隨著研發工作不斷從理論探索轉向大規模生產,在製造技術的進步以及人們對其經濟和性能優勢日益認可的推動下,自修復聚合物正被整合到更廣泛的高附加價值應用中。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 21億美元 |

| 預測金額 | 130億美元 |

| 複合年成長率 | 20.1% |

在工業製造領域,自修復聚合物正被日益廣泛地應用於解決材料反覆劣化的難題。這些材料能夠將修復機制直接融入塗層和複合材料系統中,從而延長零件的使用壽命,尤其是在高性能應用領域。市場需求也正轉向在單一聚合物體系中整合多種功能特性的材料。如今,自修復解決方案旨在將機械修復能力與其他性能特性相結合,從而實現在尖端材料平台上的廣泛應用。這種多功能方法有助於簡化材料的複雜性,同時提高系統的整體效率和可靠性,從而促進其更廣泛的應用。

預計到2025年,熱固性自修復聚合物市場佔有率將達到43%,並在2026年至2035年間以19.6%的複合年成長率成長。市場趨勢表明,對通用材料平台的依賴正在減少,聚合物系統的選擇與最終用途的需求之間的匹配度將更高。熱固性體系在需要結構完整性和表面保護的應用領域中仍然佔據主導地位。同時,熱塑性和彈性體系統則適用於需要柔軟性的應用場景。透過平衡剛性、韌性、加工性和可重複的自修復能力,共混和互穿網路技術能夠實現可自訂的效能,從而進一步提升其商業性吸引力。

到2025年,結構和承重應用將佔市場佔有率的29.2%,預計到2035年將以19%的複合年成長率成長。隨著越來越多的企業尋求降低整體擁有成本並最大限度地減少運作,結構、防護、電子、生物醫學、消費品和能源相關領域的應用持續成長。在承重環境中,自修復能力有助於抑製材料疲勞和裂縫形成;而在防護應用中,表面修復和抵抗環境應力至關重要。這些性能優勢持續推動此技術在嚴苛運作條件下的整合應用。

預計到2025年,北美自修復聚合物市場規模將達到6.525億美元,2035年將達到19億美元,年複合成長率(CAGR)為19.3%。全部區域的成長主要得益於塗料、先進複合材料和電子材料領域的高應用率,以及成熟的創新生態系統。美國仍然是商業化活動的中心,這得益於材料製造商、研究機構和製造終端用戶之間的密切合作。這些夥伴關係正在加速認證流程,並推動自修復聚合物在多個高效能應用領域的早期部署。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 市場機遇

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 透過癒合機制

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利狀態

- 貿易統計(HS編碼)

(註:貿易統計數據僅涵蓋主要國家。)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 公司矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依治療機制分類,2022-2035年

- 固有自修復聚合物

- 可逆共用價鍵體系

- 基於超分子(非共用)相互作用的系統

- 動態交聯網路

- 熱可逆網路

- 外源性自修復聚合物

- 基於微膠囊的系統

- 血管或微通道系統

- 顆粒狀或相分離的自癒合劑

- 植入式形狀記憶或刺激反應系統

第6章 市場估算與預測:依聚合物基質類型分類,2022-2035年

- 熱固性自修復聚合物

- 熱塑性自修復聚合物

- 基於彈性體的自修復聚合物

- 聚合物共混物與互穿網路

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 結構/荷載支撐應用

- 防護塗層和油漆

- 電子設備和軟設備

- 生物醫學和醫療保健應用

- 消費品和紡織品

- 能源和環境應用

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第9章:公司簡介

- BASF SE

- Covestro AG

- Evonik Industries AG

- Arkema SA

- Huntsman Corporation

- The Dow Chemical Company

- 3M Company

- AkzoNobel NV

- Henkel AG &Co. KGaA

- DSM-Firmenich(formerly Royal DSM)

- LG Chem Ltd.

- SABIC

- Mitsubishi Chemical Group

- Toray Industries, Inc.

- Sumitomo Chemical Co., Ltd.

- Nippon Paint Holdings Co., Ltd.

The Global Self-Healing Polymers Market was valued at USD 2.1 billion in 2025 and is estimated to grow at a CAGR of 20.1% to reach USD 13 billion by 2035.

Self-healing polymers have evolved from early-stage laboratory concepts into commercially viable materials, particularly between 2022 and 2025, as industries increasingly focus on durability, lifecycle extension, and performance optimization. A noticeable rise in academic and technical publications referencing self-healing polymers indicates growing innovation around dynamic molecular networks and responsive chemical systems that enable autonomous material repair. This surge in research activity aligns with expanding industrial interest, as manufacturers seek advanced materials capable of restoring functionality after damage. The market benefits from rising demand for materials that reduce maintenance needs, minimize downtime, and improve long-term reliability. As development efforts continue to shift from theoretical exploration to scalable production, self-healing polymers are being integrated into a wider range of high-value applications, supported by improved manufacturing techniques and increasing awareness of their economic and performance advantages.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.1 Billion |

| Forecast Value | $13 Billion |

| CAGR | 20.1% |

Within industrial manufacturing, self-healing polymers are increasingly adopted to address recurring material degradation challenges. These materials enable original equipment manufacturers to enhance component longevity by embedding repair mechanisms directly into coatings and composite systems, particularly in high-performance sectors. Market demand is also shifting toward materials that combine multiple functional properties within a single polymer system. Self-healing solutions are now designed to integrate mechanical recovery with additional performance attributes, enabling broader applicability across advanced material platforms. This multifunctional approach supports wider adoption by enabling manufacturers to simplify material complexity while enhancing overall system efficiency and reliability.

The thermosetting self-healing polymers segment accounted for held 43% share in 2025 and is projected to grow at a CAGR of 19.6% from 2026 to 2035. The market landscape shows increasing alignment between polymer system selection and end-use requirements rather than reliance on generalized material platforms. Thermosetting systems remain dominant in applications requiring structural integrity and surface protection, while thermoplastic and elastomeric systems support flexibility-driven use cases. Blend and interpenetrating network technologies enable tailored performance by balancing rigidity, toughness, ease of processing, and repeatable healing capability, further strengthening their commercial appeal.

The structural and load-bearing applications held 29.2% share in 2025 and are expected to grow at a CAGR of 19% through 2035. Adoption across structural, protective, electronic, biomedical, consumer, and energy-related segments continues to expand as organizations aim to lower total ownership costs and reduce operational interruptions. In load-bearing environments, self-healing functionality helps slow material fatigue and crack development, while protective applications emphasize surface restoration and resistance to environmental stressors. These performance benefits continue to drive integration across demanding operating conditions.

North America Self-Healing Polymers Market reached USD 652.5 million in 2025 to USD 1.9 billion by 2035 at a CAGR of 19.3%. Growth across the region is supported by strong adoption across coatings, advanced composites, and electronic materials, along with a well-established innovation ecosystem. The United States remains the central hub for commercialization activity, supported by close collaboration among material producers, research institutions, and manufacturing end users. These partnerships accelerate qualification processes and early-stage deployment across multiple high-performance applications.

Prominent participants in the Global Self-Healing Polymers Market include BASF SE, Arkema S.A., Covestro AG, The Dow Chemical Company, Evonik Industries AG, Huntsman Corporation, DSM-Firmenich (formerly Royal DSM), 3M Company, Henkel AG & Co. KGaA, AkzoNobel N.V., SABIC, LG Chem Ltd., Mitsubishi Chemical Group, Toray Industries, Inc., Sumitomo Chemical Co., Ltd., and Nippon Paint Holdings Co., Ltd. Companies active in the self-healing polymers market employ a combination of strategic initiatives to strengthen their competitive positioning. Investment in research and development remains a primary focus, enabling firms to improve healing efficiency, durability, and compatibility with existing manufacturing processes. Strategic partnerships with industrial end users support faster commercialization and application-specific customization. Many companies expand production capabilities to support scaling and cost optimization. Portfolio diversification across coatings, composites, and advanced materials allows suppliers to address multiple industries. Sustainability-focused innovation, including extended material lifespans and reduced maintenance requirements, further enhances market acceptance.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Healing mechanism

- 2.2.3 Polymer matrix type

- 2.2.4 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By Healing mechanism

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Healing mechanism, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Intrinsic self-healing polymers

- 5.2.1 Reversible covalent bond-based systems

- 5.2.2 Supramolecular (non-covalent) interaction-based systems

- 5.2.3 Dynamic crosslinked networks

- 5.2.4 Thermally reversible networks

- 5.3 Extrinsic self-healing polymers

- 5.3.1 Microcapsule-based systems

- 5.3.2 Vascular or microchannel-based systems

- 5.3.3 Particulate or phase-separated healing agents

- 5.3.4 Embedded shape-memory or stimulus-triggered systems

Chapter 6 Market Estimates and Forecast, By Polymer matrix type, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Thermosetting self-healing polymers

- 6.3 Thermoplastic self-healing polymers

- 6.4 Elastomeric self-healing polymers

- 6.5 Polymer blends and interpenetrating networks

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Structural and load-bearing applications

- 7.3 Protective coatings and paints

- 7.4 Electronics and soft devices

- 7.5 Biomedical and healthcare applications

- 7.6 Consumer goods and textiles

- 7.7 Energy and environmental applications

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 BASF SE

- 9.2 Covestro AG

- 9.3 Evonik Industries AG

- 9.4 Arkema S.A.

- 9.5 Huntsman Corporation

- 9.6 The Dow Chemical Company

- 9.7 3M Company

- 9.8 AkzoNobel N.V.

- 9.9 Henkel AG & Co. KGaA

- 9.10 DSM-Firmenich (formerly Royal DSM)

- 9.11 LG Chem Ltd.

- 9.12 SABIC

- 9.13 Mitsubishi Chemical Group

- 9.14 Toray Industries, Inc.

- 9.15 Sumitomo Chemical Co., Ltd.

- 9.16 Nippon Paint Holdings Co., Ltd.

全球自修復材料市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球自修復材料市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 自癒式IT基礎設施市場預測至2034年-按組件、部署模式、組織規模、技術、應用、最終用戶和地區分類的全球分析自修復材料市場預測至2034年-按材料類型、形態、應用和地區分類的全球分析

自癒式IT基礎設施市場預測至2034年-按組件、部署模式、組織規模、技術、應用、最終用戶和地區分類的全球分析自修復材料市場預測至2034年-按材料類型、形態、應用和地區分類的全球分析 自修復材料市場報告:按類型、形態、技術、終端應用產業和地區分類(2026-2034 年)

自修復材料市場報告:按類型、形態、技術、終端應用產業和地區分類(2026-2034 年) 2026年全球自修復材料市場報告自修復材料市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測

2026年全球自修復材料市場報告自修復材料市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測 生物分解自組裝材料市場分析及預測(至2035年):類型、產品、應用、技術、材料類型、最終用戶、功能、安裝類型自癒式電子電路市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、材料類型、裝置、功能及最終用戶分類自組裝奈米電路市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、材料類型、製程、最終用戶、功能分類

生物分解自組裝材料市場分析及預測(至2035年):類型、產品、應用、技術、材料類型、最終用戶、功能、安裝類型自癒式電子電路市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、材料類型、裝置、功能及最終用戶分類自組裝奈米電路市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、材料類型、製程、最終用戶、功能分類 自修復材料市場規模、佔有率和成長分析(按類型、產品、技術、應用和地區分類)-2026-2033年產業預測

自修復材料市場規模、佔有率和成長分析(按類型、產品、技術、應用和地區分類)-2026-2033年產業預測