|

市場調查報告書

商品編碼

1959288

V2X 資料品質保證市場機會、成長要素、產業趨勢分析及 2026 年至 2035 年預測V2X Data Quality Assurance Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

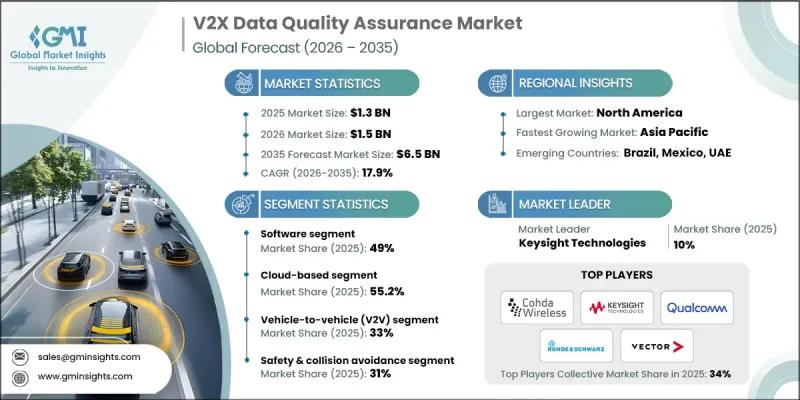

2025 年全球 V2X 數據品質保證市場價值為 13 億美元,預計到 2035 年將達到 65 億美元,年複合成長率為 17.9%。

這一成長反映了汽車生態系統和交通基礎設施在互聯出行、自動駕駛技術進步以及數位化道路基礎設施整合的推動下,正加速轉型。產業相關人員正積極應對由不斷演進的通訊標準、網路安全要求、監管協調、智慧基礎設施投資以及進階檢驗要求等因素所帶來的結構性變化。隨著車聯網(V2X)成為智慧型運輸系統(ITS)的基礎,對穩健的測試、檢驗和監控框架的需求持續成長。向下一代無線技術的過渡以及車輛、路側和雲端互操作系統的日益複雜化進一步推動了市場擴張。持續檢驗訊息的準確性、延遲、認證和可靠性對於維護運行完整性至關重要。隨著全球部署的擴展,相關人員正優先考慮容錯架構和標準化合規框架,以確保在2035年建立一個安全、可靠且高效能的車聯網生態系統。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 13億美元 |

| 預測金額 | 65億美元 |

| 複合年成長率 | 17.9% |

V2X 資料品質保證產業的關鍵組成部分之一是安全憑證管理系統 (SCMS),這是一個由美國運輸部定義的公開金鑰基礎建設,所有 V2X 部署都必須採用。該架構支援基於憑證的身份驗證,從而實現加密通訊,旨在保護匿名性的同時,確保資料的完整性和真實性。該框架還支援識別和移除受損及不合規的設備,從而在互聯行動網路中強化持續的、反饋驅動的品質保證循環。

軟體領域預計在2025年將佔據49%的市場佔有率,並在2026年至2035年間以19%的複合年成長率成長。這一主導地位凸顯了軟體驅動的檢驗工具在管理V2X生態系統的技術複雜性方面發揮的關鍵作用。核心產品包括通訊協定分析解決方案、網路模擬環境、自動化測試框架、一致性檢驗平台和即時監控系統。聯邦機構採用的開放原始碼智慧型運輸系統軟體計畫進一步加強了這個生態系統。品質保證平台必須檢驗SAE J2735標準中規定的各種訊息格式,以確保安全、交通管理、旅客資訊和路側通訊交換的可靠性。

預計到2025年,基於雲端的部署模式將佔據55.2%的市場佔有率,且成長速度最快,到2035年複合年成長率將達到18.8% 。雲端對應平臺因其初始投資要求低、擴充性、部署速度快以及軟體更新高效等優勢,正受到汽車零件供應商、出行Start-Ups和區域運輸機構的青睞。透過將檢驗環境遷移到雲端基礎設施,企業無需建造資本密集型設施即可使用先進的測試工具。遠端和分散式檢驗功能使運作不同地理區域的車輛和基礎設施系統能夠無縫連接到集中式品質保證環境。

預計到2025年,北美V2X數據品質保證市場規模將達到3.535億美元,並在2026年至2035年間以17.5%的複合年成長率成長。美國擁有許多優勢,包括高聯網汽車普及率、先進的數位道路基礎設施以及成熟的汽車和技術生態系統,這些都為互通性測試和訊息檢驗工具提供了支援。跨多個州的大規模聯網汽車部署需要持續的效能監控和系統的品質檢驗,以確保運作安全和通訊可靠性。

目錄

第1章:調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率分析

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 聯網汽車和自動駕駛汽車的廣泛應用。

- 政府關於V2X安全標準的強制規定

- 在安全性至關重要的應用中,對即時資料檢驗的需求日益成長。

- 智慧交通基礎設施的發展

- V2X通訊中網路安全的需求

- 產業潛在風險與挑戰

- 高昂的實施成本和基礎設施成本

- 多重標準 V2X 環境(DSRC 與 C-V2X)的複雜性

- 缺乏統一的全球標準

- OEM廠商間互通性挑戰

- 市場機遇

- 新興技術:5G-V2X 和 6G-V2X 技術

- 智慧城市和智慧交通系統基礎設施擴建

- 售後服務需求不斷成長

- 人工智慧驅動的預測數據品質解決方案

- V2X相容於電動車充電(V2G)品質保證

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 美國聯邦V2X法規和頻段分配

- 加拿大 - 連網和自動駕駛汽車安全框架 (CASF)

- 歐洲

- 德國、歐盟智慧交通系統和國家舉措

- 英國-脫歐後的V2X柔軟性

- 法國——國家車聯網試驗與智慧交通系統戰略

- 義大利——智慧交通系統試點計畫和智慧基礎設施

- 亞太地區

- 中國工信部C-V2X強制性法規與標準

- 印度—新興的V2X和汽車互聯法規

- 日本——智慧交通系統連結性與頻率政策

- 澳洲—技術中立的智慧交通系統政策

- LATAM

- 墨西哥 - NOM車輛安全標準

- 阿根廷 - 國家交通法 24.449

- 中東和非洲

- 南非共和國 - 道路交通法(1996 年)

- 沙烏地阿拉伯—交通運輸法律與2030願景交通運輸政策

- 北美洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 基於有效性的檢測機制

- 機器學習方法(多層感知器、支援向量機、深度學習)

- 人工智慧和機器學習在數據品質方面的應用

- 用於V2X資料完整性的區塊鏈

- 新興技術

- 用於即時檢驗的邊緣運算

- 量子抗性密碼技術的發展

- 數位雙胞胎與模擬技術

- 5G網路切片提升V2X質量

- 當前技術趨勢

- 專利分析

- 價格分析

- 軟體授權定價模式

- 硬體價格趨勢

- 專業服務收費系統

- 使用案例和成功案例

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 碳足跡考量

- 最佳實踐和實施指南

- 設計品質保證框架

- 實施最佳實踐

- 數據品管最佳實踐

- 安全最佳實踐

- 效能最佳化最佳實踐

- 監理合規最佳實踐

- 引言場景和模型

- 都市區實施方案

- 主要道路發展方案

- 農村和偏遠地區的部署場景

- 混合技術引入方案

- 特殊環境場景

- 產品和服務基準測試

- 軟體功能比較矩陣

- 硬體技術規格基準測試

- 服務組合和服務等級協定比較

- 定價和總擁有成本分析

- 未來前景與機遇

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃及資金籌措

第5章 市場估計與預測:依組件分類,2022-2035年

- 軟體

- 資料檢驗和清洗

- 分析與異常檢測

- 即時監測與分析

- 模擬和測試平台

- 合規和報告軟體

- 硬體

- 感應器

- 通訊模組

- 邊緣/處理單元

- 汽車單元(OBU)

- 路側單元(RSU)

- 服務

- 諮詢

- 系統整合

- 引言和部署

- 維護和支援

- 培訓和文檔

第6章 市場估算與預測:依部署類型分類,2022-2035年

- 現場

- 基於雲端的

第7章 市場估計與預測:依性別分類的互聯互通情況,2022-2035年

- 車對車(V2V)通訊

- 車路通訊(V2I)

- 車行通訊(V2P)

- 車聯網(V2N)

- 其他

第8章 市場估計與預測:依應用領域分類,2022-2035年

- 安全/防碰撞

- 交通管理與最佳化

- 自動駕駛和進階駕駛輔助系統

- 車隊管理

- 其他

第9章 市場估計與預測:依應用領域分類,2022-2035年

- 汽車製造商

- 政府機構

- 車隊營運商

- 其他

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 荷蘭

- 瑞典

- 丹麥

- 波蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 新加坡

- 泰國

- 印尼

- 越南

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥倫比亞

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 以色列

第11章:公司簡介

- 世界玩家

- Anritsu

- Cohda Wireless

- IPG Automotive

- Keysight Technologies

- NI(National Instruments)

- Qualcomm Technologies

- Robert Bosch

- Rohde & Schwarz

- Vector Informatik

- VIAVI Solutions

- 本地球員

- Autotalks

- Commsignia

- Continental

- DEKRA

- Denso

- NOFFZ Technologies

- NXP Semiconductors

- Savari

- SEA Datentechnik

- Valeo Telematik

- 新興科技創新者

- ADAS iiT

- Allion Labs

- msg

- Neusoft

- u-blox

The Global V2X Data Quality Assurance Market was valued at USD 1.3 billion in 2025 and is estimated to grow at a CAGR of 17.9% to reach USD 6.5 billion by 2035.

The growth reflects accelerating transformation across automotive ecosystems and transportation infrastructure, fueled by connected mobility, autonomous driving advancements, and digital roadway integration. Industry participants are navigating structural shifts driven by evolving communication standards, cybersecurity mandates, regulatory alignment, smart infrastructure investments, and advanced validation requirements. As vehicle-to-everything communication becomes foundational to intelligent transportation systems, demand for robust testing, verification, and monitoring frameworks continues to expand. Market expansion is further supported by the transition to next-generation wireless technologies and the increasing complexity of interoperable vehicle, roadside, and cloud-based systems. Continuous validation of message accuracy, latency, authentication, and reliability is essential to maintain operational integrity. As deployment scales globally, stakeholders are prioritizing resilient architectures and standardized compliance frameworks to ensure safe, secure, and high-performance V2X ecosystems through 2035.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.3 Billion |

| Forecast Value | $6.5 Billion |

| CAGR | 17.9% |

A critical component of the V2X data quality assurance industry is the Security Credential Management System, a public key infrastructure framework defined by the US Department of Transportation and required across V2X implementations. This architecture enables encrypted communication supported by certificate-based authentication, designed to protect anonymity while safeguarding data integrity and authenticity. The framework also supports the identification and removal of compromised or non-compliant devices, reinforcing a continuous feedback-driven quality assurance loop within connected mobility networks.

The software segment accounted for 49% share in 2025 and is forecast to grow at a CAGR of 19% from 2026 to 2035. This dominance underscores the essential role of software-driven validation tools in managing the technical complexity of V2X ecosystems. Core offerings include protocol analysis solutions, network simulation environments, automated test frameworks, compliance validation platforms, and real-time monitoring systems. Open-source intelligent transportation software initiatives introduced by federal agencies have further strengthened the ecosystem. Quality assurance platforms must verify diverse message formats standardized under SAE J2735, ensuring reliability across safety, traffic management, traveler information, and roadside communication exchanges.

The cloud-based deployment models segment held 55.2% share in 2025 and is expanding at the fastest CAGR of 18.8% through 2035. Cloud-enabled platforms are gaining adoption among automotive suppliers, mobility startups, and regional transportation agencies due to lower upfront investment requirements, scalability, rapid deployment, and streamlined software updates. By shifting validation environments to cloud infrastructure, organizations can access sophisticated testing tools without building capital-intensive facilities. Remote and distributed validation capabilities allow vehicles and infrastructure systems operating in different geographic regions to connect seamlessly to centralized quality assurance environments.

North America V2X Data Quality Assurance Market generated USD 353.5 million in 2025 and is projected to grow at a CAGR of 17.5% from 2026 to 2035. The US benefits from strong connected vehicle adoption rates, advanced digital roadway infrastructure, and a mature automotive and technology ecosystem supporting interoperability testing and message validation tools. Large-scale connected vehicle deployments across multiple states require continuous performance monitoring and structured quality validation to maintain operational safety and communication reliability.

Key companies operating in the Global V2X Data Quality Assurance Market include Anritsu, Rohde & Schwarz, Vector Informatik, Keysight Technologies, NI (National Instruments), VIAVI Solutions, IPG Automotive, Cohda Wireless, Qualcomm Technologies, and Robert Bosch. Companies in the V2X Data Quality Assurance Market are strengthening their market position through strategic technology partnerships, advanced R&D investments, and expansion of cloud-native testing platforms. Leading players are focusing on interoperability validation solutions aligned with evolving 5G NR-V2X and future 6G standards. Many firms are integrating AI-driven analytics into quality monitoring platforms to enhance anomaly detection and predictive diagnostics. Strategic collaborations with automotive OEMs, infrastructure providers, and telecom operators are accelerating ecosystem integration.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 Research trail and confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Best estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Deployment Mode

- 2.2.4 Connectivity

- 2.2.5 Application

- 2.2.6 End Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing adoption of connected and autonomous vehicles

- 3.2.1.2 Government mandates for V2X safety standards

- 3.2.1.3 Rising need for real-time data validation in safety-critical applications

- 3.2.1.4 Growth of smart transportation infrastructure

- 3.2.1.5 Demand for cybersecurity in V2X communications

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High implementation and infrastructure costs

- 3.2.2.2 Complexity of multi-standard V2X environments (DSRC vs C-V2X)

- 3.2.2.3 Lack of unified global standards

- 3.2.2.4 Interoperability challenges across OEMs

- 3.2.3 Market opportunities

- 3.2.3.1 Emerging 5G-V2X and 6G-V2X technologies

- 3.2.3.2 Smart city and ITS infrastructure expansion

- 3.2.3.3 Growing aftermarket services demand

- 3.2.3.4 AI-driven predictive data quality solutions

- 3.2.3.5 V2X-enabled electric vehicle charging (V2G) quality assurance

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 US- Federal V2X rules & spectrum allocation

- 3.4.1.2 Canada - safety framework for connected & automated vehicles (CASF)

- 3.4.2 Europe

- 3.4.2.1 Germany- EU ITS & national initiatives

- 3.4.2.2 UK- Post Brexit V2X flexibility

- 3.4.2.3 France- National V2X testing & ITS strategy

- 3.4.2.4 Italy- ITS pilots & smart infrastructure

- 3.4.3 Asia Pacific

- 3.4.3.1 China- MIIT C-V2X mandates & standards

- 3.4.3.2 India- Emerging V2X & automotive connectivity regulations

- 3.4.3.3 Japan- ITS connect & spectrum policy

- 3.4.3.4 Australia- Technology neutral ITS policies

- 3.4.4 LATAM

- 3.4.4.1 Mexico- NOM vehicle safety standards

- 3.4.4.2 Argentina- National traffic law 24.449

- 3.4.5 MEA

- 3.4.5.1 South Africa- National road traffic act (1996)

- 3.4.5.2 Saudi Arabia- Traffic law & vision 2030 transport initiatives

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.1.1 Plausibility-based detection mechanisms

- 3.7.1.2 Machine learning approaches (MLP, SVM, deep learning)

- 3.7.1.3 AI and machine learning for data quality

- 3.7.1.4 Blockchain for V2X data integrity

- 3.7.2 Emerging technologies

- 3.7.2.1 Edge computing for real-time validation

- 3.7.2.2 Quantum-safe cryptography development

- 3.7.2.3 Digital twin and simulation technologies

- 3.7.2.4 5G network slicing for V2X quality

- 3.7.1 Current technological trends

- 3.8 Patent analysis

- 3.9 Pricing analysis

- 3.9.1 Software licensing pricing models

- 3.9.2 Hardware equipment pricing trends

- 3.9.3 Professional services pricing structure

- 3.10 Use cases & success stories

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly Initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Best practices and implementation guidelines

- 3.12.1 Quality assurance framework design

- 3.12.2 Deployment best practices

- 3.12.3 Data quality management best practices

- 3.12.4 Security best practices

- 3.12.5 Performance optimization best practices

- 3.12.6 Regulatory compliance best practices

- 3.13 Deployment scenarios and models

- 3.13.1 Urban deployment scenarios

- 3.13.2 Highway deployment scenarios

- 3.13.3 Rural and remote deployment scenarios

- 3.13.4 Mixed technology deployment scenarios

- 3.13.5 Special environment scenarios

- 3.14 Product and service benchmarking

- 3.14.1 Software feature comparison matrix

- 3.14.2 Hardware technical specifications benchmarking

- 3.14.3 Service portfolio and SLA comparison

- 3.14.4 Pricing and total cost of ownership analysis

- 3.15 Future outlook and opportunities

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Bn)

- 5.1 Key trends

- 5.2 Software

- 5.2.1 Data validation & cleansing

- 5.2.2 Analytics & anomaly detection

- 5.2.3 Real-time monitoring & analytics

- 5.2.4 Simulation & testing platforms

- 5.2.5 Compliance & reporting software

- 5.3 Hardware

- 5.3.1 Sensors

- 5.3.2 Communication modules

- 5.3.3 Edge/processing units

- 5.3.4 On-board units (OBUs)

- 5.3.5 Roadside units (RSUs)

- 5.4 Services

- 5.4.1 Consulting

- 5.4.2 System integration

- 5.4.3 Implementation & deployment

- 5.4.4 Maintenance & support

- 5.4.5 Training & documentation

Chapter 6 Market Estimates & Forecast, By Deployment Mode, 2022 - 2035 ($Bn)

- 6.1 Key trends

- 6.2 On premises

- 6.3 Cloud-based

Chapter 7 Market Estimates & Forecast, By Connectivity, 2022 - 2035 ($Bn)

- 7.1 Key trends

- 7.2 Vehicle-to-vehicle (V2V)

- 7.3 Vehicle-to-infrastructure (V2I)

- 7.4 Vehicle-to-pedestrian (V2P)

- 7.5 Vehicle-to-network (V2N)

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn)

- 8.1 Key trends

- 8.2 Safety & collision avoidance

- 8.3 Traffic management & optimization

- 8.4 Autonomous driving & ADAS

- 8.5 Fleet management

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Bn)

- 9.1 Key trends

- 9.2 Automotive OEMs

- 9.3 Government Agencies

- 9.4 Fleet Operators

- 9.5 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Netherlands

- 10.3.8 Sweden

- 10.3.9 Denmark

- 10.3.10 Poland

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Singapore

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Colombia

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Israel

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Anritsu

- 11.1.2 Cohda Wireless

- 11.1.3 IPG Automotive

- 11.1.4 Keysight Technologies

- 11.1.5 NI (National Instruments)

- 11.1.6 Qualcomm Technologies

- 11.1.7 Robert Bosch

- 11.1.8 Rohde & Schwarz

- 11.1.9 Vector Informatik

- 11.1.10 VIAVI Solutions

- 11.2 Regional Players

- 11.2.1 Autotalks

- 11.2.2 Commsignia

- 11.2.3 Continental

- 11.2.4 DEKRA

- 11.2.5 Denso

- 11.2.6 NOFFZ Technologies

- 11.2.7 NXP Semiconductors

- 11.2.8 Savari

- 11.2.9 SEA Datentechnik

- 11.2.10 Valeo Telematik

- 11.3 Emerging Technology Innovators

- 11.3.1 ADAS iiT

- 11.3.2 Allion Labs

- 11.3.3 msg

- 11.3.4 Neusoft

- 11.3.5 u-blox

車對車通訊市場:2026-2032年全球市場預測(按通訊方式、組件、車輛類型、應用和最終用戶分類)汽車V2X市場:依通訊技術、組件類型、應用、車輛類型及最終用戶分類-2026-2032年全球市場預測汽車V2X市場:按服務類型、通訊方式、應用和車輛類型分類-2026-2032年全球市場預測

車對車通訊市場:2026-2032年全球市場預測(按通訊方式、組件、車輛類型、應用和最終用戶分類)汽車V2X市場:依通訊技術、組件類型、應用、車輛類型及最終用戶分類-2026-2032年全球市場預測汽車V2X市場:按服務類型、通訊方式、應用和車輛類型分類-2026-2032年全球市場預測 2026年全球車對車(V2X)訊息顯示面板市場報告2026年全球車對車通訊市場報告2026年全球汽車V2X市場報告

2026年全球車對車(V2X)訊息顯示面板市場報告2026年全球車對車通訊市場報告2026年全球汽車V2X市場報告 車聯網(V2X)市場機會、成長要素、產業趨勢分析及2026年至2035年預測。

車聯網(V2X)市場機會、成長要素、產業趨勢分析及2026年至2035年預測。 全球汽車V2X技術市場規模、佔有率、趨勢和成長分析報告:2026-2034年

全球汽車V2X技術市場規模、佔有率、趨勢和成長分析報告:2026-2034年 全球汽車AR/VR使用者體驗市場預測(至2034年),按車輛類型、技術、分銷管道、應用、最終用戶和地區分類汽車廣角擴散器市場按產品類型、原料、推進方式、車輛類型、應用和最終用途分類-2026-2032年全球預測

全球汽車AR/VR使用者體驗市場預測(至2034年),按車輛類型、技術、分銷管道、應用、最終用戶和地區分類汽車廣角擴散器市場按產品類型、原料、推進方式、車輛類型、應用和最終用途分類-2026-2032年全球預測