|

市場調查報告書

商品編碼

1959284

無線條形音箱市場機會、成長要素、產業趨勢分析及2026年至2035年預測Wireless Soundbar Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

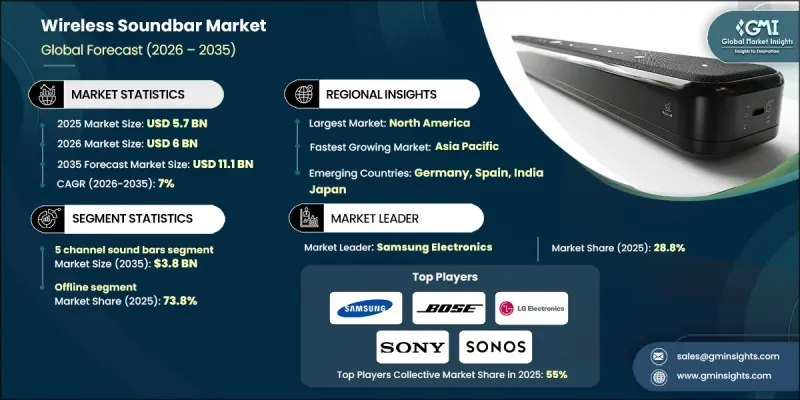

2025 年全球無線條形音箱市場價值 57 億美元,預計到 2035 年將達到 111 億美元,年複合成長率為 7%。

無線連接和音訊處理技術的不斷進步顯著提升了音質,同時免去了繁瑣的佈線。消費者正享受著許多好處,例如靈活的安裝方式、整潔的生活空間以及與多種音源設備的無縫連接。政府主導的數位基礎設施投資和智慧家庭環境推廣計畫也進一步推動了無線產品的普及。製造商積極響應這些趨勢,推出了可無縫整合到智慧連網家庭環境中的多功能條形音箱。數位串流媒體平台的日益普及提升了人們對身臨其境型家庭音訊體驗的期待,並持續推動高階無線條形音箱的需求。技術創新、配套基礎設施的完善以及消費者偏好的不斷變化,共同促進了這個市場的持續成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 57億美元 |

| 預測金額 | 111億美元 |

| 複合年成長率 | 7% |

預計2025年,5聲道長條音箱市場規模將達19億美元,2035年將達38億美元。這個細分市場之所以備受關注,是因為它能提供更具沉浸感的聆聽體驗,而無需像傳統多揚聲器系統那樣複雜。均衡的聲道輸出和增強的環繞聲功能滿足了消費者在家中聆聽環境中追求卓越音質的需求。家庭娛樂消費的持續成長也推動了對這類產品的需求。

預計到2025年,線下通路將佔據73.8%的市佔率。實體零售仍然至關重要,因為消費者更傾向於在購買前親身體驗音質。商店示範可以讓買家即時評估效能、清晰度和音量。個人化支援和即時供貨進一步提升了線下銷售的吸引力,尤其對於高階音訊設備而言。

預計到2025年,美國無線條形音箱市場佔有率將達到88.4%。主要促進因素包括先進音訊技術的早期應用、智慧家居設備的普及以及消費者在家庭娛樂方面的強勁支出。較高的可支配收入和對身臨其境型音訊環境日益成長的需求將繼續支撐強勁的銷售。與連網家庭系統的日益融合也進一步加速了無線條形音箱在家庭中的普及。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 家庭娛樂系統需求不斷成長

- 技術進步和智慧功能的整合

- 平面電視的普及

- 產業潛在風險與挑戰

- 高價條形音箱高成本

- 與舊設備的兼容性問題

- 機會

- 遊戲和身臨其境型娛樂領域的成長潛力

- 智慧型功能型無線條形音箱的普及

- 促進因素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 依產品類型

- 按地區

- 監理情勢

- 標準和合規要求

- 區域法規結構

- 認證標準

- 貿易統計(HS編碼 - 8518)

- 主要進口國

- 主要出口國

- 差距分析

- 風險評估和緩解措施

- 波特的分析

- PESTEL 分析

- 消費行為分析

- 購買模式

- 偏好分析

- 消費者行為的區域差異

- 電子商務對購買決策的影響

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 公司矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 雙聲道長條音箱

- 三聲道長條音箱

- 5聲道長條音箱

- 7聲道長條音箱

第6章 市場估計與預測:依性別分類的互聯互通情況,2022-2035年

- Bluetooth

- Wi-Fi

第7章 市場估計與預測:依安裝類型分類,2022-2035年

- 壁掛式

- 桌面型

- 獨立式

第8章 市場估計與預測:依價格分類,2022-2035年

- 低價位

- 中號

- 高價位範圍

第9章 市場估算與預測:按瓦特計,2022-2035年

- 99瓦或以下

- 100-199瓦

- 200-499瓦

- 500-799瓦

- 800瓦或以上

第10章 市場規模估計與預測(2022-2035年)

- 小於30英寸

- 30-60英寸

- 60吋或更大

第11章 市場估計與預測:依應用領域分類,2022-2035年

- 住宅

- 商業的

第12章 市場估計與預測:依通路分類,2022-2035年

- 線上

- 電子商務

- 我們的網站

- 離線

- 超級市場/大賣場

- 專賣店

- 其他(個體店、百貨公司等)

第13章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第14章:公司簡介

- Bose

- Bowers &Wilkins

- Klipsch

- LG Electronics

- Panasonic

- Philips

- Pioneer

- Polk Audio(Sound United)

- Samsung Electronics

- Sennheiser

- Sonos

- Sony

- TCL Technology Group

- VIZIO

- Yamaha

The Global Wireless Soundbar Market was valued at USD 5.7 billion in 2025 and is estimated to grow at a CAGR of 7% to reach USD 11.1 billion by 2035.

Continuous advancements in wireless connectivity and audio processing technologies have significantly improved sound quality while eliminating the need for complex wiring. Consumers benefit from flexible installation, cleaner living spaces, and seamless connectivity with multiple source devices. Government-led investments in digital infrastructure and initiatives that promote smart living environments are further supporting adoption. Manufacturers are actively responding to these trends by introducing feature-rich soundbars that integrate smoothly with connected home ecosystems. Growing use of digital streaming platforms has heightened expectations for immersive audio experiences at home, which continues to push demand for premium wireless soundbars. Together, technological innovation, supportive infrastructure development, and evolving consumer preferences are reinforcing sustained growth in this market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.7 Billion |

| Forecast Value | $11.1 Billion |

| CAGR | 7% |

The 5-channel soundbar segment generated USD 1.9 billion in 2025 and is forecast to reach USD 3.8 billion by 2035. This segment is gaining traction as it delivers a more immersive listening experience without the complexity of traditional multi-speaker systems. Balanced channel output and enhanced surround sound capabilities appeal to consumers seeking improved audio performance for in-home viewing. The ongoing shift toward home-based entertainment consumption continues to support demand for these configurations.

The offline distribution channels segment accounted for 73.8% share in 2025. Physical retail continues to play a critical role as consumers prefer to experience audio quality firsthand before purchasing. In-store demonstrations allow buyers to assess performance, clarity, and volume in real time. Personalized assistance and immediate product availability further strengthen the appeal of offline sales, particularly for higher-value audio equipment.

U.S. Wireless Soundbar Market held 88.4% share in 2025. Market leadership is driven by early adoption of advanced audio technologies, widespread use of smart home devices, and strong consumer spending on home entertainment. High disposable incomes and growing demand for immersive audio setups continue to support robust sales. Expanding integration with connected home systems further accelerates household adoption.

Key companies operating in the Global Wireless Soundbar Market include Samsung Electronics, Sony, LG Electronics, Bose, Sonos, Yamaha, Sennheiser, Panasonic, Philips, TCL Technology Group, VIZIO, Polk Audio, Klipsch, Pioneer, and Bowers & Wilkins. Companies in the wireless soundbar market focus on innovation, ecosystem integration, and brand differentiation to strengthen their market position. Manufacturers invest heavily in audio engineering, wireless connectivity, and immersive sound technologies to enhance user experience. Compatibility with smart home platforms and voice-enabled systems is a key priority. Strategic pricing across entry-level and premium segments helps capture diverse consumer groups. Expanding retail partnerships and direct-to-consumer channels improve visibility and accessibility. Design aesthetics, compact form factors, and ease of installation further influence purchasing decisions and support long-term brand loyalty.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Connectivity

- 2.2.4 Installation Type

- 2.2.5 Price

- 2.2.6 Speaker Wattage

- 2.2.7 Size

- 2.2.8 Application

- 2.2.9 Distribution Channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for home entertainment systems

- 3.2.1.2 Technological advancements and integration of smart features

- 3.2.1.3 Growing adoption of flat panel TVs

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High cost of premium soundbars

- 3.2.2.2 Compatibility issues with older devices

- 3.2.3 Opportunities

- 3.2.3.1 Growth potential in gaming & immersive entertainment

- 3.2.3.2 Expansion of smart and functional wireless soundbar

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By product type

- 3.6.2 By region

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics (HS Code- 8518)

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Gap analysis

- 3.10 Risk assessment and mitigation

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

- 3.13 Consumer behaviour analysis

- 3.13.1 Purchasing patterns

- 3.13.2 Preference analysis

- 3.13.3 Regional variations in consumer behaviour

- 3.13.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022-2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 2 channel sound bars

- 5.3 3 channel sound bars

- 5.4 5 channel sound bars

- 5.5 7 channel sound bars

Chapter 6 Market Estimates & Forecast, By Connectivity, 2022-2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Bluetooth

- 6.3 Wi-fi

Chapter 7 Market Estimates & Forecast, By Installation Type, 2022-2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Wall mounted

- 7.3 Tabletop

- 7.4 Free standing

Chapter 8 Market Estimates & Forecast, By Price, 2022-2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Low

- 8.3 Medium

- 8.4 High

Chapter 9 Market Estimates & Forecast, By Wattage, 2022-2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Up to 99 watts

- 9.3 100-199 watts

- 9.4 200-499 watts

- 9.5 500-799 watts

- 9.6 Above 800 watts

Chapter 10 Market Estimates & Forecast, By Size, 2022-2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Under 30 inches

- 10.3 30-60 inches

- 10.4 Above 60 inches

Chapter 11 Market Estimates & Forecast, By Application, 2022-2035 (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 Residential

- 11.3 Commercial

Chapter 12 Market Estimates & Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Thousand Units)

- 12.1 Key trends

- 12.2 Online

- 12.2.1 E-Commerce

- 12.2.2 Company website

- 12.3 Offline

- 12.3.1 Supermarkets/Hypermarkets

- 12.3.2 Specialty Stores

- 12.3.3 Others (Individual stores, Departmental stores, etc.)

Chapter 13 Market Estimates & Forecast, By Region, 2022-2035 (USD Billion) (Thousand Units)

- 13.1 Key trends

- 13.2 North America

- 13.2.1 U.S.

- 13.2.2 Canada

- 13.3 Europe

- 13.3.1 Germany

- 13.3.2 France

- 13.3.3 UK

- 13.3.4 Italy

- 13.3.5 Spain

- 13.4 Asia Pacific

- 13.4.1 China

- 13.4.2 India

- 13.4.3 Japan

- 13.4.4 South Korea

- 13.4.5 Australia

- 13.5 Latin America

- 13.5.1 Brazil

- 13.5.2 Mexico

- 13.5.3 Argentina

- 13.6 MEA

- 13.6.1 South Africa

- 13.6.2 Saudi Arabia

- 13.6.3 UAE

Chapter 14 Company Profiles

- 14.1 Bose

- 14.2 Bowers & Wilkins

- 14.3 Klipsch

- 14.4 LG Electronics

- 14.5 Panasonic

- 14.6 Philips

- 14.7 Pioneer

- 14.8 Polk Audio (Sound United)

- 14.9 Samsung Electronics

- 14.10 Sennheiser

- 14.11 Sonos

- 14.12 Sony

- 14.13 TCL Technology Group

- 14.14 VIZIO

- 14.15 Yamaha

條形音箱市場:2026-2032年全球市場預測(按技術、連接方式、安裝方法、安裝類型、輸出功率、應用、最終用戶和銷售管道)

條形音箱市場:2026-2032年全球市場預測(按技術、連接方式、安裝方法、安裝類型、輸出功率、應用、最終用戶和銷售管道) 條形音箱市場報告:按類型、安裝方式、連接方式、應用和地區分類(2026-2034 年)

條形音箱市場報告:按類型、安裝方式、連接方式、應用和地區分類(2026-2034 年) 全球條形音箱市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球條形音箱市場規模、佔有率、趨勢和成長分析報告(2026-2034) 條形音箱市場-全球產業規模、佔有率、趨勢、機會和預測:按安裝類型、連接方式、銷售管道、地區和競爭格局分類,2021-2031年藍牙長條音箱市場按通道配置、技術、應用和分銷管道分類,全球預測(2026-2032年)

條形音箱市場-全球產業規模、佔有率、趨勢、機會和預測:按安裝類型、連接方式、銷售管道、地區和競爭格局分類,2021-2031年藍牙長條音箱市場按通道配置、技術、應用和分銷管道分類,全球預測(2026-2032年) 條形音箱市場規模、佔有率和成長分析(按類型、連接方式、安裝方式、分銷管道、應用和地區分類)-2026-2033年產業預測

條形音箱市場規模、佔有率和成長分析(按類型、連接方式、安裝方式、分銷管道、應用和地區分類)-2026-2033年產業預測 長條音箱市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)

長條音箱市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年) 全球條形音箱市場

全球條形音箱市場 條形音箱:季度市場追蹤

條形音箱:季度市場追蹤 條形音箱的全球市場:安裝類別,連接性別,各用途,各種價格,各流通管道,各地區,機會,預測,2018年~2032年

條形音箱的全球市場:安裝類別,連接性別,各用途,各種價格,各流通管道,各地區,機會,預測,2018年~2032年