|

市場調查報告書

商品編碼

1936667

燃氣表市場機會、成長要素、產業趨勢分析及預測(2026年至2035年)Gas Meters Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

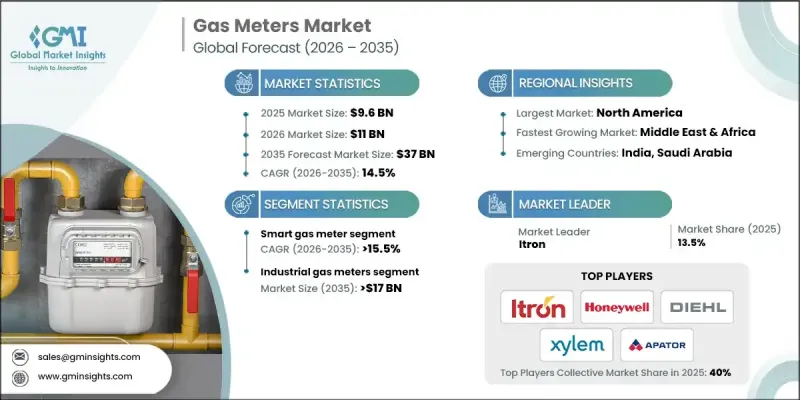

全球燃氣表市場預計到 2025 年價值 96 億美元,到 2035 年達到 370 億美元,年複合成長率為 14.5%。

對能源安全的投資不斷增加,推動了市場需求,而公共產業需要更精確、更精細的數據來應對日益緊張的全球天然氣供應。多公用事業數位平台的整合正在重塑市場格局,實現跨服務視覺性、流程自動化和增強客戶參與。在監管執法和雄心勃勃的部署目標的支持下,數位計量基礎設施的採用正在不斷擴展,以提供詳細的用量數據並提高營運效率。第二代高級計量基礎設施 (AMI) 引入了網路安全、細分時間間隔資料和遠端監控等增強功能,同時也促進了設備互通性並塑造了行業標準。對精確、連網資料的日益重視正促使公共產業對現有系統進行現代化改造,並投資於智慧計量解決方案,以深入了解營運效率和能源管理。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 96億美元 |

| 預測金額 | 370億美元 |

| 複合年成長率 | 14.5% |

預計到2035年,智慧燃氣表市場將以15.5%的複合年成長率成長。這些設備整合了微控制器、精密感測器和通訊模組,可實現燃氣表與公共產業系統之間的自動雙向資料傳輸。智慧燃氣表支援多種數據採集方式,包括固定網路、蜂窩網路連接和路邊抄表,從而減少人工干預,並為公共產業和終端用戶提供近乎即時的用氣量資訊。智慧瓦斯表的部署可提高營運效率,促進節能舉措,同時確保符合不斷變化的監管要求。

預計到2025年,工業燃氣表表市佔率將達到46.7%,到2035年市場規模將達到170億美元。這些計量表專為高流量工業應用而設計,例如製造業、化學生產、煉油業、發電業和食品加工業。渦輪計量表等先進技術可在寬廣的流量範圍內(通常從每小時500立方米到超過10,000立方米)提供精確測量,從而確保在關鍵工業環境中的可靠性和性能。

預計到2025年,美國燃氣表市場規模將達24億美元,其成長主要得益於公共產業的持續現代化、更新換代以及數位化。日益嚴格的監管壓力,例如加強排放監測和網路安全,以及政府主導的環境準則,正在推動先進計量解決方案的普及。對精準洩漏檢測和符合法規要求的計量設備的需求,也持續推動美國瓦斯表市場的擴張。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 原物料供應及採購分析

- 製造能力評估

- 供應鏈韌性與風險因素

- 配電網路分析

- 監管環境

- 產業影響因素

- 促進要素

- 產業潛在風險與挑戰

- 成長潛力分析

- 波特五力分析

- PESTEL 分析

- 燃氣表成本結構分析

- 新的機會與趨勢

- 投資分析及未來展望

第4章 競爭情勢

- 介紹

- 按地區分類的公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 戰略儀錶板

- 策略舉措

- 重要夥伴關係與合作

- 重大併購活動

- 產品創新與新產品發布

- 市場擴大策略

- 競爭標竿分析

- 創新與永續性格局

第5章 依技術分類的市場規模及預測(2022-2035年)

- 聰明的

- 傳統的

第6章 2022-2035年依產品分類的市場規模及預測

- 隔膜流量計

- 旋轉式流量計

- 渦輪流量計

- 超音波流量計

- 科氏流量計

7. 依最終用途分類的市場規模及預測(2022-2035年)

- 住宅

- 商業的

- 工業的

第8章 2022-2035年各地區市場規模及預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

第9章:公司簡介

- ABB

- Aclara

- AKG Acoustics

- Apator SA

- Badger Meter

- Diehl Stiftung

- Edmi Limited

- Elster Group

- Emerson Electrics

- Honeywell International

- Itron

- Pietro Fiorentini

- Schneider Electric

- Siemens

- Suntront

- Raychem RPG

- RMG

- Romet

- Xylem

- ZENNER

The Global Gas Meters Market was valued at USD 9.6 billion in 2025 and is estimated to grow at a CAGR of 14.5% to reach USD 37 billion by 2035.

Rising investments focused on energy security are driving demand as utilities increasingly require precise, granular data to manage a tighter global gas supply. The integration of multi-utility digital platforms is reshaping the market, enabling cross-service visibility, process automation, and enhanced customer engagement. Digital metering infrastructure is increasingly adopted to provide detailed usage data and streamline operations, supported by regulatory enforcement and ambitious rollout targets. Second-generation advanced metering infrastructures are introducing enhanced functions, including cybersecurity, granular interval data, and remote monitoring, while promoting device interoperability and shaping industry standards. The growing focus on accurate, networked data is encouraging utilities to modernize existing systems and invest in smart metering solutions that deliver operational efficiency and energy management insights.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $9.6 Billion |

| Forecast Value | $37 Billion |

| CAGR | 14.5% |

The smart gas meters segment is expected to grow at 15.5% CAGR through 2035. These devices integrate microcontrollers, precision sensors, and communication modules, enabling automated, two-way data transfer between meters and utility systems. Smart meters support multiple data collection methods, including fixed networks, cellular connectivity, and drive-by readings, reducing manual interventions and providing near real-time consumption visibility for both utilities and end-users. Their deployment strengthens operational efficiency and facilitates energy conservation initiatives while ensuring compliance with evolving regulatory requirements.

The industrial gas meters segment accounted for 46.7% share in 2025 and is projected to reach USD 17 billion by 2035. These meters are designed to accommodate high-volume industrial applications, including manufacturing, chemical production, refining, power generation, and food processing. Advanced technologies such as turbine meters provide precise measurement across a wide range of flow rates, often handling 500 to over 10,000 cubic meters per hour, ensuring reliability and performance in critical industrial environments.

U.S. Gas Meters Market was valued at USD 2.4 billion in 2025, fueled by ongoing modernization, replacement cycles, and widespread utility digitalization. Increasing regulatory pressure to monitor emissions and enhance network safety, coupled with government-led environmental guidelines, is driving the adoption of advanced metering solutions. The demand for accurate leak detection and compliance-focused measurement devices continues to accelerate market expansion across the country.

Key players active in the Global Gas Meters Market include Itron, Emerson Electrics, ABB, Xylem, Badger Meter, Pietro Fiorentini, Schneider Electric, Diehl Stiftung, Suntront, Elster Group, Romet, AKG Acoustics, Edmi Limited, RMG, Siemens, Raychem RPG, ZENNER, Apator SA, Honeywell International, and Aclara. Companies in the gas meters market are strengthening their position through continuous technological innovation, product diversification, and strategic partnerships. Manufacturers are investing in smart meter development with advanced communication capabilities, cybersecurity features, and real-time analytics. Expanding service networks and providing comprehensive maintenance solutions improve customer retention. Companies are also focusing on integrating meters with broader energy management platforms and multi-utility digital ecosystems to enhance operational intelligence. Geographic expansion into emerging markets, coupled with flexible deployment options for industrial and residential applications, supports a long-term market foothold.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Market estimates & forecast parameters

- 1.3 Forecast

- 1.3.1 Key trends for market estimates

- 1.3.2 Quantified market impact analysis

- 1.3.2.1 Mathematical impact of growth parameters on forecast

- 1.3.3 Scenario analysis framework

- 1.4 Primary research and validation

- 1.4.1 Some of the primary sources (but not limited to)

- 1.5 Data mining sources

- 1.5.1 Paid Sources

- 1.5.2 Sources, by region

- 1.6 Research trail & scoring components

- 1.6.1 Research trail components

- 1.6.2 Scoring components

- 1.7 Research transparency addendum

- 1.7.1 Source attribution framework

- 1.7.2 Quality assurance metrics

- 1.7.3 Our commitment to trust

- 1.8 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Technology trends

- 2.1.3 Product trends

- 2.1.4 End use trends

- 2.1.5 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of gas meters

- 3.8 Emerging opportunities & trends

- 3.9 Investment analysis & future prospects

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.4.1 Key partnerships & collaborations

- 4.4.2 Major M&A activities

- 4.4.3 Product innovations & launches

- 4.4.4 Market expansion strategies

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Technology, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Smart

- 5.3 Conventional

Chapter 6 Market Size and Forecast, By Product, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Diaphragm meters

- 6.3 Rotary meters

- 6.4 Turbine meters

- 6.5 Ultrasonic meters

- 6.6 Coriolis meters

Chapter 7 Market Size and Forecast, By End Use, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Residential

- 7.3 Commercial

- 7.4 Industrial

Chapter 8 Market Size and Forecast, By Region, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Mexico

- 8.6.3 Argentina

Chapter 9 Company Profiles

- 9.1 ABB

- 9.2 Aclara

- 9.3 AKG Acoustics

- 9.4 Apator SA

- 9.5 Badger Meter

- 9.6 Diehl Stiftung

- 9.7 Edmi Limited

- 9.8 Elster Group

- 9.9 Emerson Electrics

- 9.10 Honeywell International

- 9.11 Itron

- 9.12 Pietro Fiorentini

- 9.13 Schneider Electric

- 9.14 Siemens

- 9.15 Suntront

- 9.16 Raychem RPG

- 9.17 RMG

- 9.18 Romet

- 9.19 Xylem

- 9.20 ZENNER

燃氣表市場-2026-2032年全球市場預測

燃氣表市場-2026-2032年全球市場預測 2026-2030年全球濕式燃氣表市場

2026-2030年全球濕式燃氣表市場 燃氣表市場規模、佔有率、趨勢和預測:按類型、應用和地區分類,2026-2034年旋轉式燃氣表市場:2026-2032年全球市場預測(按應用、最終用戶、功能、儀表類型、壓力等級、流量、安裝方式和精度等級分類)渦輪燃氣表市場:2026-2032年全球市場預測(按應用、最終用途、技術類型、安裝方式和通路分類)

燃氣表市場規模、佔有率、趨勢和預測:按類型、應用和地區分類,2026-2034年旋轉式燃氣表市場:2026-2032年全球市場預測(按應用、最終用戶、功能、儀表類型、壓力等級、流量、安裝方式和精度等級分類)渦輪燃氣表市場:2026-2032年全球市場預測(按應用、最終用途、技術類型、安裝方式和通路分類) 2026年全球旋轉式燃氣表市場報告2026年全球燃氣表市場報告

2026年全球旋轉式燃氣表市場報告2026年全球燃氣表市場報告 全球濕式氣體流量計市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的考量、未來預測(2026-2034)

全球濕式氣體流量計市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的考量、未來預測(2026-2034) 瓦斯表市場 - 全球產業規模、佔有率、趨勢、機會和預測(按技術、應用、類型、地區和競爭格局分類,2021-2031 年預測)

瓦斯表市場 - 全球產業規模、佔有率、趨勢、機會和預測(按技術、應用、類型、地區和競爭格局分類,2021-2031 年預測) 燃氣表市場規模、佔有率及成長分析(按類型、應用和地區分類)-2026-2033年產業預測

燃氣表市場規模、佔有率及成長分析(按類型、應用和地區分類)-2026-2033年產業預測