|

市場調查報告書

商品編碼

1936661

汽車安全氣囊充氣機市場機會、成長要素、產業趨勢分析及2026年至2035年預測Automotive Airbag Inflator Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

全球汽車安全氣囊充氣機市場預計到 2025 年將達到 56 億美元,到 2035 年將達到 87 億美元,年複合成長率為 4.8%。

全球汽車產量的成長是推動這一成長的關鍵因素。隨著製造商擴大生產規模以滿足激增的需求,每輛新車需要多個安全氣囊充氣裝置,這促使安裝率上升,並加強了長期供應協議。產量的增加提高了規模經濟效益,並加速了先進充氣裝置技術在各個車型領域的應用。隨著消費者在購車時越來越重視被動安全系統和碰撞保護功能,汽車製造商甚至在中階車型中也整合了高性能多氣囊系統。智慧聯網汽車系統(包括預測感測器和智慧碰撞響應機制)的整合,需要能夠快速高效展開的充氣裝置。乘員保護和高級駕駛輔助系統 (ADAS) 的整合正在推動對下一代充氣裝置的需求,為市場上的供應商創造了巨大的機會。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 56億美元 |

| 預測金額 | 87億美元 |

| 複合年成長率 | 4.8% |

預計到2025年,乘用車市佔率將達到67%,2026年至2035年複合年成長率(CAGR)為4.7%。強制所有乘用車(包括入門級車型)安裝安全氣囊的法規是推動成長的主要因素。強制安裝多種安全氣囊系統(例如前排、側面和簾式氣囊)的法規直接增加了每輛車的安全氣囊充氣裝置數量。隨著各地法規實施期限的臨近,製造商正在加快安全氣囊系統的安裝,為供應商帶來由法規主導的穩定成長。

2025年,原始設備製造商 (OEM) 市佔率佔比高達71%,預計2026年至2035年將以4.5%的複合年成長率成長。 OEM嚴格遵守不斷變化的安全法規,有助於避免召回、罰款和聲譽損失。高品質、創新的充氣裝置使OEM能夠在多個汽車平臺上保持一致的碰撞保護標準。這種對合規性和安全性的重視促使OEM與充氣裝置供應商簽訂長期契約,從而帶來穩定的需求和持續的創新。

預計到2025年,中國汽車安全氣囊充氣機市場規模將達8.453億美元,佔全球市場佔有率的40%。作為全球最大的汽車製造地,中國每年生產數百萬輛乘用車,對各細分市場的安全氣囊充氣機需求強勁。本土及合資汽車製造商不斷擴大產能,支撐了充氣機的強勁消費,並促進了供應商的持續成長。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率分析

- 成本結構

- 每個階段的附加價值

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 促進要素

- 全球汽車產量增加

- 嚴格的安全規章

- 多氣囊結構的發展

- 充氣機技術的進步

- 產業潛在風險與挑戰

- 召回和責任風險

- 原料成本波動

- 市場機遇

- 電動車和自動駕駛汽車的成長

- 新興市場安全措施的實施

- 售後市場及召回更換

- 永續充氣材料

- 促進要素

- 成長潛力分析

- 監管環境

- 北美洲

- 美國國家公路交通安全管理局(NHTSA)法規

- 美國環保署(EPA)排放標準

- 加州空氣資源委員會 (CARB) 標準

- 歐洲

- 歐盟一般安全法規(EU GSR)

- 歐盟報廢車輛指令(ELV)

- 歐盟委員會乘用車安全標準

- 歐盟型式核准流程

- 亞太地區

- 中國國家汽車安全標準

- 印度標準局(BIS)安全氣囊法規

- 國土交通省(MLIT)規章

- 東協道路安全標準

- 拉丁美洲

- 巴西國家交通運輸局 (DENATRAN) 標準

- 阿根廷國家道路安全局 (ANSV) 法規

- 墨西哥運輸部(SCT) 條例

- 南方共同市場車輛安全標準協調

- 中東和非洲

- 阿拉伯聯合大公國聯邦機動車安全法

- 沙烏地阿拉伯標準組織(SASO)車輛安全法規

- 南非標準局(SABS)機動車輛法規

- 北美洲

- 關鍵市場趨勢與顛覆性因素

- 未來市場趨勢

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 生產統計

- 生產基地

- 消費基礎

- 進出口

- 成本細分分析

- 安全氣囊充氣機零件成本

- 研發和創新費用

- 製造和組裝成本

- 物流和配送成本

- 專利分析

- 永續性和環境方面

- 永續努力

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 企業擴張計畫和資金籌措

第5章 依車輛類型分類的市場估計與預測,2022-2035年

- 搭乘用車

- 掀背車

- 轎車

- SUV

- 其他

- 商用車輛

- 輕型商用車(LCV)

- 中型商用車(MCV)

- 重型商用車(HCV)

第6章 依通膨因素分類的市場估計與預測,2022-2035年

- 煙火充氣裝置

- 儲氣式充氣機

- 混合充氣機

7. 2022-2035年按安全氣囊類型分類的市場估算與預測

- 前座安全氣囊

- 側邊氣囊

- 側簾式氣囊

- 膝蓋

- 行人

第8章 2022-2035年按推進方式分類的市場估算與預測

- 汽油

- 柴油引擎

- 電池式電動車(BEV)

- PHEV

- HEV

- 燃料電池汽車(FCEV)

- CNG/LPG

第9章 依銷售管道分類的市場估計與預測,2022-2035年

- OEM

- 售後市場

第10章 依實施類型分類的市場估計與預測,2022-2035年

- 單級

- 多階段

第11章 2022-2035年各地區市場估計與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ANZ

- 東南亞

- 拉丁美洲

- 巴西

- 阿根廷

- 墨西哥

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

第12章:公司簡介

- 世界公司

- Autoliv

- Bosch

- Continental

- Daicel

- Delphi

- Denso

- Hyundai Mobis

- Joyson Safety Systems

- ZF

- 本地製造商

- ARC Automotive

- Ashimori Industry

- ITW Automotive

- Kolon Industries

- Nippon Kayaku

- Seiren

- Toyoda Gosei

- 新興企業

- Jinheng Automotive Safety Technology

- Nihon Plast

- Swicofil

- Tenaris

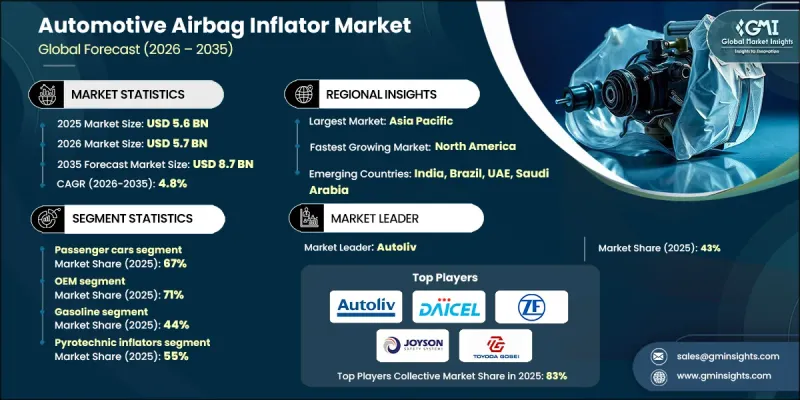

The Global Automotive Airbag Inflator Market was valued at USD 5.6 billion in 2025 and is estimated to grow at a CAGR of 4.8% to reach USD 8.7 billion by 2035.

The rising production of motor vehicles worldwide is a significant driver of this growth. As manufacturers ramp up output to meet surging demand, each new vehicle requires multiple airbag inflators, which elevates installation rates and strengthens long-term supply agreements. This higher production volume also improves economies of scale and accelerates the adoption of advanced inflator technologies across different vehicle segments. Consumers are increasingly prioritizing passive safety systems and crash protection when purchasing vehicles, leading automakers to integrate high-performance multi-airbag systems even in mid-tier models. The integration of smart, connected vehicle systems, including predictive sensors and intelligent crash-response mechanisms, requires inflators that deploy quickly and efficiently. By aligning occupant protection with advanced driver-assistance systems (ADAS), next-generation inflators are seeing higher demand, creating substantial opportunities for suppliers in the market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.6 Billion |

| Forecast Value | $8.7 Billion |

| CAGR | 4.8% |

The passenger vehicles segment accounted for 67% share in 2025 and is expected to grow at a CAGR of 4.7% between 2026 and 2035. Regulatory mandates requiring airbags in all passenger vehicles, including entry-level models, are a key factor driving growth. Laws enforcing multiple airbag systems, frontal, side, and curtain, directly increase the number of inflators per vehicle. As compliance deadlines approach across various regions, manufacturers are accelerating the installation of airbag systems, ensuring steady, regulation-driven growth for suppliers.

The original equipment manufacturers (OEMs) segment held a 71% share in 2025 and is projected to grow at a CAGR of 4.5% from 2026 to 2035. OEMs' strict adherence to evolving safety regulations helps them avoid recalls, penalties, and reputational damage. High-quality, innovative inflators allow OEMs to maintain consistency in crash protection standards across multiple vehicle platforms. This focus on compliance and safety drives long-term contracts with inflator suppliers, providing stable demand and continuous technological advancements.

China Automotive Airbag Inflator Market held 40% share, generating USD 845.3 million in 2025. Being the world's largest automotive manufacturing hub, China produces millions of passenger vehicles annually, resulting in high demand for inflators across all vehicle segments. Ongoing capacity expansions by local and joint-venture OEMs support strong inflator consumption and encourage sustained growth for suppliers.

Key players operating in the Global Automotive Airbag Inflator Market include ARC Automotive, Autoliv, Joyson Safety Systems, Toyoda Gosei, Daicel, Ashimori Industry, Hyundai Mobis, ITW Automotive, Nippon Kayaku, and ZF. Companies in the automotive airbag inflator market are focusing on several strategies to strengthen their market presence and competitive position. They are investing heavily in research and development to create next-generation, high-performance inflators that meet evolving safety standards. Long-term supply agreements with OEMs are being secured to ensure stable demand and foster collaboration for technological innovation. Strategic mergers, acquisitions, and partnerships are also employed to expand global footprints and leverage complementary capabilities. Additionally, manufacturers are diversifying their product portfolios to cater to passenger vehicles, commercial vehicles, and connected vehicle platforms.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Inflator

- 2.2.4 Airbag

- 2.2.5 Propulsion

- 2.2.6 Sales channel

- 2.2.7 Deployment mode

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global vehicle production

- 3.2.1.2 Stringent safety regulations

- 3.2.1.3 Growth of multi-airbag architectures

- 3.2.1.4 Inflator technology advancements

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Recall and liability risks

- 3.2.2.2 Raw material cost volatility

- 3.2.3 Market opportunities

- 3.2.3.1 EV & autonomous vehicle growth

- 3.2.3.2 Emerging market safety adoption

- 3.2.3.3 Aftermarket & recall replacements

- 3.2.3.4 Sustainable inflator materials

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 US National Highway Traffic Safety Administration (NHTSA) Regulations

- 3.4.1.2 Environmental Protection Agency (EPA) Emission Standards

- 3.4.1.3 California Air Resources Board (CARB) Standards

- 3.4.2 Europe

- 3.4.2.1 European Union General Safety Regulation (EU GSR)

- 3.4.2.2 EU Directive on End-of-Life Vehicles (ELV)

- 3.4.2.3 European Commission Safety Standards for Passenger Vehicles

- 3.4.2.4 European Union Type Approval Process

- 3.4.3 Asia Pacific

- 3.4.3.1 China National Standards for Vehicle Safety

- 3.4.3.2 India Bureau of Indian Standards (BIS) Airbag Regulations

- 3.4.3.3 Japan Ministry of Land, Infrastructure, Transport and Tourism (MLIT) Regulations

- 3.4.3.4 ASEAN Road Safety Standards

- 3.4.4 Latin America

- 3.4.4.1 Brazil National Traffic Department (DENATRAN) Standards

- 3.4.4.2 Argentina National Road Safety Agency (ANSV) Regulations

- 3.4.4.3 Mexico Secretariat of Communications and Transport (SCT) Regulations

- 3.4.4.4 MERCOSUR Harmonization of Vehicle Safety Standards

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE Federal Vehicle Safety Law

- 3.4.5.2 Saudi Arabian Standards Organization (SASO) Vehicle Safety Regulations

- 3.4.5.3 South African Bureau of Standards (SABS) Automotive Regulations

- 3.4.1 North America

- 3.5 Major market trends and disruptions

- 3.6 Future market trends

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Price trends

- 3.10.1 By region

- 3.10.2 By product

- 3.11 Production statistics

- 3.11.1 Production hubs

- 3.11.2 Consumption hubs

- 3.11.3 Export and import

- 3.12 Cost breakdown analysis

- 3.12.1 Airbag Inflator Component Costs

- 3.12.2 R&D and Innovation Costs

- 3.12.3 Manufacturing and Assembly Costs

- 3.12.4 Logistics and Distribution Costs

- 3.13 Patent analysis

- 3.14 Sustainability and environmental aspects

- 3.14.1 Sustainable practices

- 3.14.2 Waste reduction strategies

- 3.14.3 Energy efficiency in production

- 3.14.4 Eco-friendly Initiatives

- 3.14.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 Passenger cars

- 5.2.1 Hatchback

- 5.2.2 Sedan

- 5.2.3 SUV

- 5.2.4 Others

- 5.3 Commercial vehicle

- 5.3.1 Light commercial vehicle (LCV)

- 5.3.2 Medium commercial vehicle (MCV)

- 5.3.3 Heavy commercial vehicle (HCV)

Chapter 6 Market Estimates & Forecast, By Inflator, 2022 - 2035 ($Mn, Units)

- 6.1 Key trends

- 6.2 Pyrotechnic inflators

- 6.3 Stored gas inflators

- 6.4 Hybrid inflators

Chapter 7 Market Estimates & Forecast, By Airbag, 2022 - 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 Frontal

- 7.3 Side

- 7.4 Curtain

- 7.5 Knee

- 7.6 Pedestrian

Chapter 8 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 Gasoline

- 8.3 Diesel

- 8.4 BEV

- 8.5 PHEV

- 8.6 HEV

- 8.7 FCEV

- 8.8 CNG/LPG

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Mn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Deployment Mode, 2022 - 2035 ($Mn, Units)

- 10.1 Key trends

- 10.2 Single-stage

- 10.3 Multi-stage

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 ANZ

- 11.4.6 Southeast Asia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Argentina

- 11.5.3 Mexico

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 Saudi Arabia

- 11.6.3 South Africa

Chapter 12 Company Profiles

- 12.1 Global Players

- 12.1.1 Autoliv

- 12.1.2 Bosch

- 12.1.3 Continental

- 12.1.4 Daicel

- 12.1.5 Delphi

- 12.1.6 Denso

- 12.1.7 Hyundai Mobis

- 12.1.8 Joyson Safety Systems

- 12.1.9 ZF

- 12.2 Regional Players

- 12.2.1 ARC Automotive

- 12.2.2 Ashimori Industry

- 12.2.3 ITW Automotive

- 12.2.4 Kolon Industries

- 12.2.5 Nippon Kayaku

- 12.2.6 Seiren

- 12.2.7 Toyoda Gosei

- 12.3 Emerging Players

- 12.3.1 Jinheng Automotive Safety Technology

- 12.3.2 Nihon Plast

- 12.3.3 Swicofil

- 12.3.4 Tenaris

汽車安全氣囊充氣機市場報告:按類型、操作方式、車輛類型和地區分類,2026-2034 年

汽車安全氣囊充氣機市場報告:按類型、操作方式、車輛類型和地區分類,2026-2034 年 汽車安全氣囊充氣機市場:按車輛類型、技術、銷售管道和安裝類型分類 - 2026-2032年全球預測

汽車安全氣囊充氣機市場:按車輛類型、技術、銷售管道和安裝類型分類 - 2026-2032年全球預測 汽車安全氣囊充氣機市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並提供2026-2034年的洞察和預測氣體採樣器市場:依產品類型、應用、終端用戶產業及通路分類,全球預測,2026-2032年以推進劑類型、驅動機構、應用、終端用戶產業和分銷管道分類的煙火充氣器市場-2026-2032年全球預測安全氣囊管材市場按產品類型、安全氣囊類型、車輛類型、原料、分銷管道和應用分類-2026-2032年全球預測汽車安全氣囊氣體發生器市場按產品類型、展開機制、車輛類型、應用和最終用途分類-2026-2032年全球預測混合式安全氣囊充氣機市場按推進劑類型、部署位置、銷售管道和車輛類型分類 - 全球預測 2026-2032

汽車安全氣囊充氣機市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並提供2026-2034年的洞察和預測氣體採樣器市場:依產品類型、應用、終端用戶產業及通路分類,全球預測,2026-2032年以推進劑類型、驅動機構、應用、終端用戶產業和分銷管道分類的煙火充氣器市場-2026-2032年全球預測安全氣囊管材市場按產品類型、安全氣囊類型、車輛類型、原料、分銷管道和應用分類-2026-2032年全球預測汽車安全氣囊氣體發生器市場按產品類型、展開機制、車輛類型、應用和最終用途分類-2026-2032年全球預測混合式安全氣囊充氣機市場按推進劑類型、部署位置、銷售管道和車輛類型分類 - 全球預測 2026-2032 汽車安全氣囊充氣機市場規模、佔有率和成長分析(按車輛類型、充氣機、安全氣囊、驅動方式、銷售管道和地區分類)-2026-2033年產業預測

汽車安全氣囊充氣機市場規模、佔有率和成長分析(按車輛類型、充氣機、安全氣囊、驅動方式、銷售管道和地區分類)-2026-2033年產業預測 汽車安全氣囊充氣機市場 - 全球產業規模、佔有率、趨勢、機會和預測,按安全氣囊類型、充氣機類型、車輛類型、地區和競爭格局分類,2020-2030 年預測

汽車安全氣囊充氣機市場 - 全球產業規模、佔有率、趨勢、機會和預測,按安全氣囊類型、充氣機類型、車輛類型、地區和競爭格局分類,2020-2030 年預測