|

市場調查報告書

商品編碼

1936652

露營裝備市場機會、成長要素、產業趨勢分析及2026年至2035年預測Camping Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

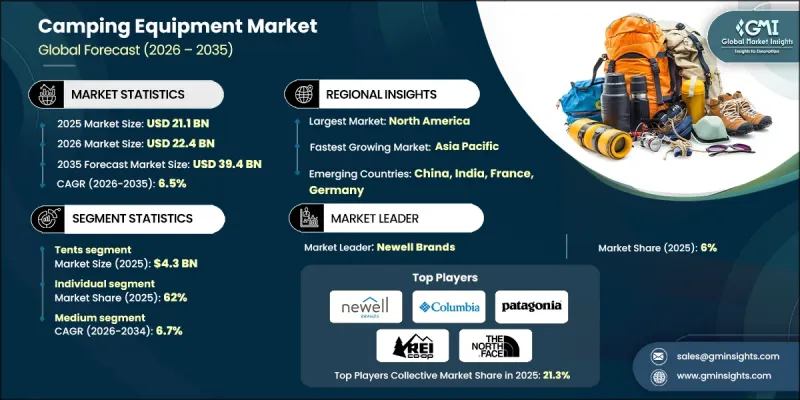

全球露營裝備市場預計到 2025 年將達到 211 億美元,到 2035 年將達到 394 億美元,年複合成長率為 6.5%。

戶外休閒的日益普及以及人們對露營有益身心健康的認知不斷提高,是推動市場擴張的主要因素。消費者越來越追求能夠緩解壓力、促進健康生活方式的自然體驗,從而刺激了對露營相關產品的需求。此外,以探險為導向和注重環保的旅行方式的興起也推動了市場成長。公共和私營機構持續進行教育活動,鼓勵人們更親近自然,從而推廣戶外活動。同時,產品設計和材料的創新正在重塑消費者的期望,更加重視產品的便利性、便攜性和舒適性。這些發展與不斷變化的生活方式偏好密切相關,尤其是在年輕消費者群體中。可支配收入的增加,尤其是在開發中國家,也使得人們更容易獲得高品質的露營裝備。生活方式的改變、創新、收入的成長以及有效的推廣活動,共同為全球露營裝備市場的持續成長創造了有利條件。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 211億美元 |

| 預測金額 | 394億美元 |

| 複合年成長率 | 6.5% |

預計到2025年,個人用戶市場將佔據62%的市場佔有率,並在2026年至2035年間以6.8%的複合年成長率成長。人們對戶外休閒活動的興趣日益濃厚、購買力不斷提升以及環保旅遊意識的增強,持續推動個人消費者的需求成長。因此,注重易用性和便攜性的設備尤其受到該細分市場的青睞。

預計到2035年,中價位市場將以6.7%的複合年成長率成長。該價位段的消費者注重性價比,希望獲得性能可靠且價格合理的產品。製造商正透過改進產品功能並保持成本競爭力來滿足這一需求。

2025年,美國露營裝備市場價值54億美元,佔全球市場佔有率的80%。露營活動的高參與度、對經濟實惠的旅行方式日益成長的興趣以及材料的不斷創新,都在支撐著該國露營裝備市場的整體成長。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段的附加價值

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 促進要素

- 產業潛在風險與挑戰

- 機會

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品類型

- 法律規範

- 標準與認證

- 環境法規

- 進出口限制

- 波特五力分析

- PESTEL 分析

- 消費行為分析

- 購買模式

- 偏好分析

- 消費行為的區域差異

- 電子商務如何影響購買決策

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章 依產品類型分類的市場估算與預測,2022-2035年

- 帳篷

- 家具

- 背包

- 睡袋

- 烹飪系統

- 爐灶和燃燒器

- 炊具

- 其他(空調等)

- 其他(裝備、求生工具包等)

第6章 2022-2035年按價格分類的市場估計與預測

- 低價位

- 中號

- 高價位範圍

7. 按最終用戶分類的市場估計和預測,2022-2035 年

- 個人

- 面向專業人士

第8章 按分銷管道分類的市場估算與預測,2022-2035年

- 線上

- 電子商務

- 公司網站

- 離線

- 超級市場/大賣場

- 專賣店

- 其他(例如,獨立零售商)

第9章 2022-2035年各地區市場估算與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- Big Agnes

- Clarus

- Columbia

- Garmin

- Johnson Outdoors

- Marmot

- MSR

- Nemo

- Newell(Coleman)

- Patagonia

- REI Co-op

- RSP

- Sea to Summit

- The North Face

- YETI Holdings

The Global Camping Equipment Market was valued at USD 21.1 billion in 2025 and is estimated to grow at a CAGR of 6.5% to reach USD 39.4 billion by 2035.

Market expansion is driven by the rising participation in outdoor recreation and the growing perception of camping as a positive activity for physical and mental wellness. Consumers are increasingly seeking nature-based experiences that support stress reduction and healthy lifestyles, which is accelerating demand for camping-related products. The growth of adventure-oriented and environmentally focused travel is further reinforcing market momentum. Public institutions and private organizations continue to promote outdoor engagement through awareness initiatives that encourage people to spend more time in natural environments. At the same time, innovation in product design and materials is reshaping consumer expectations, with a strong focus on convenience, portability, and comfort. These developments align closely with evolving lifestyle preferences, particularly among younger consumer groups. Rising disposable income levels, especially across developing economies, are also enabling broader access to higher-quality camping equipment. Together, lifestyle shifts, innovation, income growth, and supportive promotional efforts are creating favorable conditions for sustained growth in the global camping equipment market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $21.1 Billion |

| Forecast Value | $39.4 Billion |

| CAGR | 6.5% |

The individual user segment accounted for 62% share in 2025 and is expected to grow at a CAGR of 6.8% from 2026 to 2035. Increasing personal interest in outdoor leisure activities, combined with higher spending power and greater awareness of eco-focused travel, continues to support demand from individual consumers. Equipment designed for ease of use and transport is particularly appealing to this segment.

The medium-priced segment is forecast to grow at a CAGR of 6.7% through 2035. Consumers in this category prioritize value, seeking reliable performance without premium pricing. Manufacturers are responding by advancing product features while maintaining competitive cost structures.

United States Camping Equipment Market held 80% share generating USD 5.4 billion in 2025. Strong participation in camping activities, increasing interest in cost-effective travel options, and ongoing material innovation are supporting market growth across the country.

Key companies active in the Global Camping Equipment Market include Decathlon, The North Face, YETI Holdings, Patagonia, REI Co-op, Columbia, Big Agnes, Marmot, Nemo, MSR, Sea to Summit, Garmin, Johnson Outdoors, Newell (Coleman), and Clarus. Companies in the camping equipment market are strengthening their market position through product innovation, brand building, and expanded distribution strategies. Many players are investing in advanced materials and design improvements to enhance durability, comfort, and portability. Expanding direct-to-consumer and omnichannel sales models helps brands reach a wider audience while improving customer engagement. Sustainability-focused product development and responsible sourcing are increasingly used to align with consumer values. Strategic partnerships, targeted marketing campaigns, and strong brand storytelling are helping companies connect with younger and experience-driven consumers.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Price

- 2.2.4 End Users

- 2.2.5 Distribution Channel

- 2.3 CXO perspectives: strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product type

- 3.7 Regulatory framework

- 3.7.1 Standards and certifications

- 3.7.2 Environmental regulations

- 3.7.3 Import export regulations

- 3.8 Porter's five forces analysis

- 3.9 PESTEL analysis

- 3.10 Consumer behavior analysis

- 3.10.1 Purchasing patterns

- 3.10.2 Preference analysis

- 3.10.3 Regional variations in consumer behavior

- 3.10.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035 ($Billion, Thousand Units)

- 5.1 Key trends

- 5.2 Tents

- 5.3 Furniture

- 5.4 Backpack

- 5.5 Sleeping bags

- 5.6 Cooking systems

- 5.6.1 Stoves and burners

- 5.6.2 Utensils

- 5.6.3 Others (coolers, etc.)

- 5.7 Others (gears, survival kit, etc.)

Chapter 6 Market Estimates & Forecast, By Price, 2022 - 2035 ($Billion, Thousand Units)

- 6.1 Key trends

- 6.2 Low

- 6.3 Medium

- 6.4 High

Chapter 7 Market Estimates & Forecast, By End User, 2022 - 2035 ($Billion, Thousand Units)

- 7.1 Key trends

- 7.2 Individual

- 7.3 Professional

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 ($Billion, Thousand Units)

- 8.1 Key trends

- 8.2 Online

- 8.2.1 E-commerce

- 8.2.2 Company websites

- 8.3 Offline

- 8.3.1 Supermarkets/hypermarket

- 8.3.2 Specialty retail stores

- 8.3.3 Others (independent retailer etc.)

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Billion, Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Big Agnes

- 10.2 Clarus

- 10.3 Columbia

- 10.4 Garmin

- 10.5 Johnson Outdoors

- 10.6 Marmot

- 10.7 MSR

- 10.8 Nemo

- 10.9 Newell (Coleman)

- 10.10 Patagonia

- 10.11 REI Co-op

- 10.12 RSP

- 10.13 Sea to Summit

- 10.14 The North Face

- 10.15 YETI Holdings

房車市場:2026-2032年全球市場預測(按房車類型、銷售管道和應用分類)露營廚房市場:2026-2032年全球市場預測(按產品類型、燃料類型、價格範圍、活動類型、材料類型、分銷管道和最終用戶分類)露營椅市場:2026-2032年全球市場預測(依產品類型、材料、價格範圍、承重能力、銷售管道及最終用戶分類)露營冷藏箱市場:全球市場按產品類型、容量、材料、應用和銷售管道分類的預測 - 2026-2032 年露營和房車市場:2026-2032年全球市場預測(按露營方式、產品類型、活動、最終用戶和分銷管道分類)

房車市場:2026-2032年全球市場預測(按房車類型、銷售管道和應用分類)露營廚房市場:2026-2032年全球市場預測(按產品類型、燃料類型、價格範圍、活動類型、材料類型、分銷管道和最終用戶分類)露營椅市場:2026-2032年全球市場預測(依產品類型、材料、價格範圍、承重能力、銷售管道及最終用戶分類)露營冷藏箱市場:全球市場按產品類型、容量、材料、應用和銷售管道分類的預測 - 2026-2032 年露營和房車市場:2026-2032年全球市場預測(按露營方式、產品類型、活動、最終用戶和分銷管道分類) 露營裝備市場規模、佔有率、趨勢和預測:按產品類型、分銷管道和地區分類,2026-2034年

露營裝備市場規模、佔有率、趨勢和預測:按產品類型、分銷管道和地區分類,2026-2034年 露營家具市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年

露營家具市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年 露營家具市場機會、成長要素、產業趨勢分析及2026年至2035年預測露營裝備市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年

露營家具市場機會、成長要素、產業趨勢分析及2026年至2035年預測露營裝備市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年 露營冷藏箱市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、材料、產能、應用、地區和競爭格局分類,2021-2031年

露營冷藏箱市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、材料、產能、應用、地區和競爭格局分類,2021-2031年