|

市場調查報告書

商品編碼

1936649

金屬射出成型零件市場機會、成長要素、產業趨勢分析及預測(2026-2035年)Metal Injection Molding (MIM) Parts Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

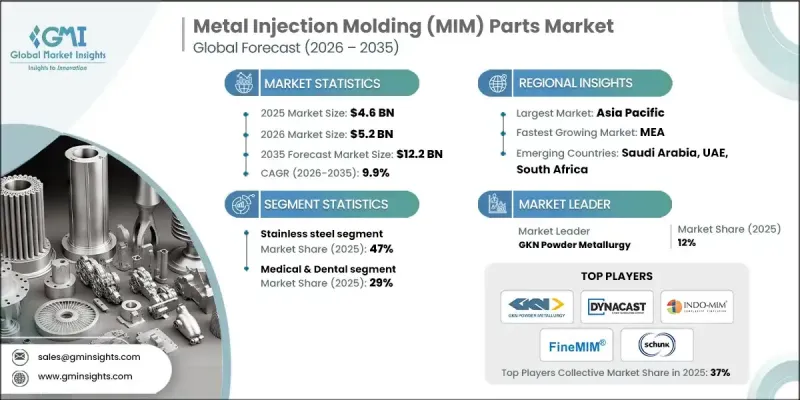

全球金屬射出成型(MIM) 零件市場預計到 2025 年將達到 46 億美元,到 2035 年將達到 122 億美元,年複合成長率為 9.9%。

隨著設計師們日益尋求將複雜的微型金屬部件融入現代產品,金屬注射成型(MIM)市場正蓬勃發展。越來越多的原始設備製造商(OEM)選擇MIM來製造小型、複雜且精密的零件,這些零件難以透過傳統的機械加工或鑄造流程實現。 MIM尤其適用於對微型化和精度要求極高的應用領域,例如醫療、牙科、航太和消費性電子產業。不銹鋼、鈦和特殊磁性合金正被擴大用於生產輕量化、高功能性和生物相容性零件。先進的CAD建模、拓撲最佳化和數位製程模擬技術正被用於改進零件設計、收縮控制、密度分佈和流動特性,從而確保一次性生產成功,尤其對於安全至關重要的汽車和航太零件而言。 MIM兼具高精度、高重複性和設計柔軟性,正推動其在全球多個高成長產業中廣泛應用。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始金額 | 46億美元 |

| 預測金額 | 122億美元 |

| 複合年成長率 | 9.9% |

不銹鋼市佔率佔47%,預計到2035年將以7.1%的複合年成長率成長。不銹鋼和低合金鋼因其在汽車、工業和五金領域的廣泛應用而佔據市場主導地位。鈦和生物相容性不銹鋼在醫療和牙科應用領域日益受到青睞,而銅和磁性合金則擴大用於感測器、致動器和電氣連接。這些材料趨勢反映了各行各業對耐用、輕量和高性能組件日益成長的需求,凸顯了金屬注射成型(MIM)作為製造技術的通用性。

預計到2025年,醫療和牙科領域將佔據29%的市場佔有率,並在2026年至2035年間以9.8%的複合年成長率成長。推動這些領域採用MIM技術的關鍵因素是對微型、高精度和幾何形狀複雜的零件的需求。在醫療和牙科應用中,不銹鋼和鈦合金MIM零件被廣泛用於植入、手術器械和生物相容性組件。消費性電子產業對堅固耐用且美觀的微型MIM零件的需求也不斷成長。在精度和性能至關重要的領域,MIM技術能夠製造輕量化、功能齊全且可重複的複雜設計,這是推動其應用日益廣泛的主要因素。

預計到2025年,北美金屬射出成型(MIM)零件市場規模將達12億美元。成長的主要驅動力來自醫療、槍械和汽車等高價值應用領域。該地區受益於先進的設計能力、嚴格的品質標準以及受監管行業對MIM技術的早期應用。美國是北美的核心市場,其需求來自醫療設備、航太與國防、消費性電子和高性能汽車等多個產業。先進的契約製造的存在以及對高精度、大批量生產的重視,正在推動材料、模具和MIM製程的持續創新。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段的附加價值

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 促進要素

- 醫療設備和電子設備的微型化

- 汽車輕量化和效率要求

- 設計自由度與材料利用優勢

- 產業潛在風險與挑戰

- 高昂的模具和初始開發成本

- 認證流程的複雜性與所需時間

- 市場機遇

- 植入、外科和牙科器械的成長

- 穿戴式裝置和智慧硬體的普及率不斷提高

- 促進要素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 依材料類型

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利狀態

- 貿易統計(HS編碼)(註:僅提供主要國家的貿易統計)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續努力

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 考慮到碳足跡

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 按材質的市場估算與預測,2022-2035年

- 不銹鋼

- 低合金鋼

- 鉬合金

- 鈦

- 磁性材料

- 銅及銅合金

- 其他(鎢、鈷合金)

第6章 依最終用戶分類的市場估算與預測,2022-2035年

- 醫療和牙科

- 手術器械

- 正畸托槽

- 植入

- 其他

- 車

- 渦輪增壓器零件

- 燃油系統組件

- 傳動部件

- 其他

- 消費性電子產品

- 智慧型手機鉸鏈

- 穿戴式裝置零件

- 其他

- 航太/國防

- 引擎部件

- 飛彈導引部件

- 工業的

- 閥門部件

- 油壓元件

- 其他

- 槍枝

- 扳機

- 視線

- 其他(休閒、IT 等)

第7章 2022-2035年各地區市場估算與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第8章 公司簡介

- Smith Metal Products

- Advanced Materials Technologies Pte. Ltd

- CMG Technologies

- Form Technologies Company(Dynacast)

- ARC Group Worldwide, Inc.

- Akron Porcelain &Plastics Co.

- Dynacast

- Nippon Piston Ring Co. Ltd.

- INDO-MIM

- ASH Industries

- Hamamatsu Metal Works Co., Ltd.

- Parmaco Metal Injection Molding

- GKN Powder Metallurgy

- MPP(Metal Powder Products)

- Zcmim(Zhejiang Yibo Technology)

- Epson Atmix Corporation

- Schunk Group

- FineMIM

- OptiMIM

- Advanced Power Products

- Rockleigh Industries

- Injectamax International, LLC

The Global Metal Injection Molding (MIM) Parts Market was valued at USD 4.6 billion in 2025 and is estimated to grow at a CAGR of 9.9% to reach USD 12.2 billion by 2035.

The market is gaining momentum as designers increasingly seek to integrate complex, miniaturized metal components into modern products. More original equipment manufacturers (OEMs) are choosing MIM to produce parts that are too small, intricate, or delicate for conventional machining or casting processes. MIM is particularly suited to sectors requiring high levels of miniaturization and precision, including medical, dental, aerospace, and consumer electronics. Stainless steel, titanium, and specialty magnetic alloys are increasingly used to manufacture lightweight, functional, and biocompatible components. Advanced CAD modeling, topology optimization, and digital process simulation are being leveraged to improve part design, shrinkage control, density distribution, and flow characteristics, enabling first-time-right production, especially for safety-critical automotive and aerospace components. The combination of precision, repeatability, and design flexibility is solidifying MIM's adoption across multiple high-growth industries worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.6 Billion |

| Forecast Value | $12.2 Billion |

| CAGR | 9.9% |

The stainless steel segment held 47% share and is expected to grow at a CAGR of 7.1% through 2035. Stainless steel and low-alloy steel dominate the market due to extensive applications in automotive, industrial, and hardware segments. Titanium and biocompatible stainless steel are gaining traction in medical and dental applications, while copper and magnetic alloys are increasingly used in sensors, actuators, and electrical connectivity applications. These material trends reflect the growing demand for durable, lightweight, and high-performance components across a wide range of industries, highlighting the versatility of MIM as a production technology.

The medical and dental sector accounted for 29% share in 2025 and is projected to grow at a CAGR of 9.8% during 2026-2035. The primary driver for MIM adoption in these segments is the demand for small, precise, and geometrically complex components. In medical and dental applications, stainless steel and titanium MIM parts are extensively used for implants, surgical instruments, and biocompatible components. Consumer electronics also drive demand for miniature MIM components that require both robustness and aesthetic finishes. The ability of MIM to produce intricate designs that are lightweight, functional, and repeatable is a key reason for its rising adoption in sectors where precision and performance are critical.

North America Metal Injection Molding (MIM) Parts Market reached USD 1.2 billion in 2025. Growth is primarily driven by high-value applications in medical, firearms, and automotive sectors. The region benefits from advanced design capabilities, rigorous quality standards, and early adoption of MIM technology in regulated industries. The United States remains the core market in North America, supported by diverse demand from medical devices, aerospace, defense, consumer electronics, and performance automotive sectors. The presence of advanced contract manufacturers and the focus on high-precision, high-volume production foster ongoing innovation in materials, tooling, and MIM processes.

Major players operating in the Global Metal Injection Molding (MIM) Parts Market include Dynacast, Akron Porcelain & Plastics Co., Rockleigh Industries, Smith Metal Products, Advanced Materials Technologies Pte. Ltd., MPP (Metal Powder Products), FineMIM, CMG Technologies, GKN Powder Metallurgy, Hamamatsu Metal Works Co., Ltd., Zcmim (Zhejiang Yibo Technology), Epson Atmix Corporation, OptiMIM, Parmaco Metal Injection Molding, Injectamax International LLC, ARC Group Worldwide, Inc., ASH Industries, Form Technologies Company (Dynacast), INDO-MIM, and Schunk Group. Companies in the metal injection molding parts market are pursuing several strategies to strengthen their market presence and expand global reach. They are investing heavily in research and development to optimize MIM processes, improve material performance, and develop innovative lightweight and biocompatible components. Strategic partnerships with OEMs, aerospace firms, medical device manufacturers, and electronics companies are being formed to secure long-term contracts and access to emerging high-value markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material type

- 2.2.3 End-Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Miniaturization of medical and electronic devices

- 3.2.1.2 Automotive light-weighting and efficiency requirements

- 3.2.1.3 Design freedom and material utilization benefits

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High tooling and upfront development costs

- 3.2.2.2 Process complexity and qualification timelines

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in implants, surgical and dental devices

- 3.2.3.2 Rising adoption in wearables and smart hardware

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By material type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Material Type, 2022-2035 (USD Billion) (Mn Units)

- 5.1 Key trends

- 5.2 Stainless steel

- 5.3 Low alloy steel

- 5.4 Molybdenum alloys

- 5.5 Titanium

- 5.6 Magnetic materials

- 5.7 Copper & copper alloys

- 5.8 Others (tungsten, cobalt alloys)

Chapter 6 Market Estimates and Forecast, By End-User, 2022-2035 (USD Billion) (Mn Units)

- 6.1 Key trends

- 6.2 Medical & dental

- 6.2.1 Surgical instruments

- 6.2.2 Orthodontic brackets

- 6.2.3 Dental implants

- 6.2.4 Others

- 6.3 Automotive

- 6.3.1 Turbocharger components

- 6.3.2 Fuel system parts

- 6.3.3 Transmission parts

- 6.3.4 Others

- 6.4 Consumer electronics

- 6.4.1 Smartphone hinges

- 6.4.2 Wearable device components

- 6.4.3 Others

- 6.5 Aerospace & defense

- 6.5.1 Engine components

- 6.5.2 Missile guidance parts

- 6.6 Industrial

- 6.6.1 Valve parts

- 6.6.2 Hydraulic component

- 6.6.3 Others

- 6.7 Firearms

- 6.7.1 Triggers

- 6.7.2 Sights

- 6.8 Others (recreation, IT etc.)

Chapter 7 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Mn Units)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Rest of Europe

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.4.6 Rest of Asia Pacific

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.5.4 Rest of Latin America

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

- 7.6.4 Rest of Middle East and Africa

Chapter 8 Company Profiles

- 8.1 Smith Metal Products

- 8.2 Advanced Materials Technologies Pte. Ltd

- 8.3 CMG Technologies

- 8.4 Form Technologies Company (Dynacast)

- 8.5 ARC Group Worldwide, Inc.

- 8.6 Akron Porcelain & Plastics Co.

- 8.7 Dynacast

- 8.8 Nippon Piston Ring Co. Ltd.

- 8.9 INDO-MIM

- 8.10 ASH Industries

- 8.11 Hamamatsu Metal Works Co., Ltd.

- 8.12 Parmaco Metal Injection Molding

- 8.13 GKN Powder Metallurgy

- 8.14 MPP (Metal Powder Products)

- 8.15 Zcmim (Zhejiang Yibo Technology)

- 8.16 Epson Atmix Corporation

- 8.17 Schunk Group

- 8.18 FineMIM

- 8.19 OptiMIM

- 8.20 Advanced Power Products

- 8.21 Rockleigh Industries

- 8.22 Injectamax International, LLC

金屬射出成型市場:依材料、產品類型、製程及應用分類-2026-2032年全球市場預測

金屬射出成型市場:依材料、產品類型、製程及應用分類-2026-2032年全球市場預測 2026年全球金屬射出成型市場報告

2026年全球金屬射出成型市場報告 金屬射出成型市場-全球產業規模、佔有率、趨勢、機會及預測(依材料類型、最終用途產業、地區及競爭格局分類,2021-2031年)家用電子電器用MIM組件市場按產品、材質、應用和最終用戶分類 - 全球預測(2026-2032年)

金屬射出成型市場-全球產業規模、佔有率、趨勢、機會及預測(依材料類型、最終用途產業、地區及競爭格局分類,2021-2031年)家用電子電器用MIM組件市場按產品、材質、應用和最終用戶分類 - 全球預測(2026-2032年) 金屬射出成型市場規模、佔有率和成長分析(按材料類型、最終用途產業和地區分類)-2026-2033年產業預測

金屬射出成型市場規模、佔有率和成長分析(按材料類型、最終用途產業和地區分類)-2026-2033年產業預測 金屬射出成型市場:全球產業分析、市場規模、佔有率、成長、趨勢與未來預測,2025-2032

金屬射出成型市場:全球產業分析、市場規模、佔有率、成長、趨勢與未來預測,2025-2032 2030 年金屬射出成型市場預測:按材料、最終用戶和地區分類的全球分析全球金屬射出成型市場:2033 年的機會與策略

2030 年金屬射出成型市場預測:按材料、最終用戶和地區分類的全球分析全球金屬射出成型市場:2033 年的機會與策略 金屬射出成型市場,依材料類型、最終用戶、國家和地區分類 - 2024-2032 年行業分析、市場規模、市場佔有率和預測

金屬射出成型市場,依材料類型、最終用戶、國家和地區分類 - 2024-2032 年行業分析、市場規模、市場佔有率和預測