|

市場調查報告書

商品編碼

1936645

抗痘化妝品市場機會、成長要素、產業趨勢分析及2026年至2035年預測Anti-acne Cosmetics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

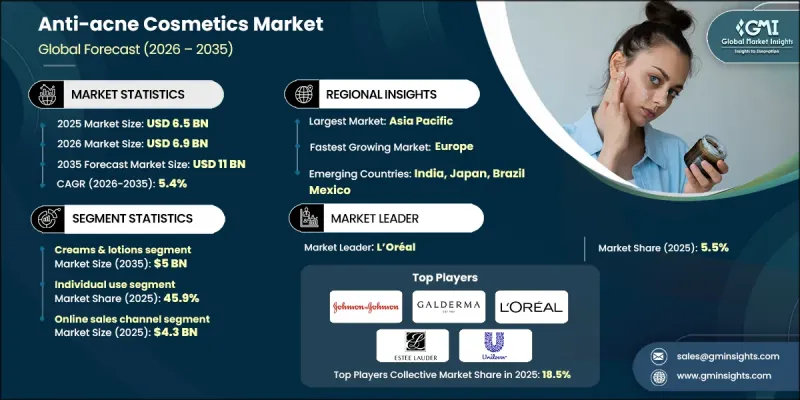

全球抗痘化妝品市場預計到 2025 年將達到 65 億美元,到 2035 年將達到 110 億美元,年複合成長率為 5.4%。

市場成長主要受清潔美容運動的興起以及消費者對天然有機成分護膚品日益成長的偏好驅動。消費者對合成化合物潛在副作用的擔憂日益加劇,促使他們優先選擇成分較溫和、無毒且天然的保養品。這種消費行為的轉變正在重塑整個產業的研發策略,製造商紛紛調整產品配方以符合潔淨標示的要求。消費者對皮膚健康的日益關注,以及個人護理支出的成長,持續支撐著市場需求。此外,人們對永續美容實踐的日益重視,以及有利於環保產品的法規結構,也推動了市場的長期擴張。隨著護膚程序越來越注重成分和健康,抗痘化妝品正被不同年齡和膚質的消費者廣泛接受,這預示著市場將在2025年以後保持穩步成長。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 起始值 | 65億美元 |

| 預測金額 | 110億美元 |

| 複合年成長率 | 5.4% |

預計到2025年,乳霜和乳液類產品市場收入將達29億美元,到2035年將達到50億美元。由於其多功能性和易用性,該品類持續保持主流地位。消費者更傾向於選擇外用產品,這些產品不僅有助於控制痤瘡,還能提供保濕、調理和長期護膚等額外功效。消費者對多功能護膚方案的需求不斷成長,進一步推動了抗痤瘡乳霜和乳液類產品的需求。

預計到2025年,個人使用細分市場將佔45.9%的市場佔有率。此細分市場的成長主要得益於消費者對價格實惠、方便在家使用的祛痘解決方案的需求日益成長。這種轉向自我護理的趨勢減少了對頻繁專業治療的依賴,從而節省了時間和成本。這一趨勢反映了消費者對個人化護膚和自主選擇產品的更廣泛需求,也印證了個人消費者在推動整體市場成長的重要性。

預計到2025年,美國抗痘化妝品市場佔有率將達到74.5% 。主導地位得益於消費者的高度認知、非處方護膚品的高滲透率以及先進皮膚科解決方案的廣泛應用。此外,知名高階品牌的存在、數位行銷的影響以及對經臨床檢驗的化妝品日益成長的需求,共同推動了市場滲透率的持續成長。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段的附加價值

- 影響價值鏈的因素

- 產業影響因素

- 促進要素

- 青少年和成年人痤瘡盛行率不斷上升

- 意識提高和皮膚科諮詢量增加

- 配方和遞送系統的創新

- 產業潛在風險與挑戰

- 消費者偏好和趨勢的變化

- 仿冒品品

- 機會

- 智慧護膚與個人化結合

- 永續性和清潔美容趨勢

- 促進要素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 依產品類型

- 按地區

- 監管環境

- 標準和合規要求

- 區域法規結構

- 認證標準

- 貿易統計

- 主要進口國

- 主要出口國

- 差距分析

- 風險評估與緩解

- 波特五力分析

- PESTEL 分析

- 消費行為分析

- 購買模式

- 偏好分析

- 消費行為的區域差異

- 電子商務對購買決策的影響

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章 依產品類型分類的市場估算與預測,2022-2035年

- 面具

- 乳霜和乳液

- 洗面乳和化妝水

- 其他

第6章 2022-2035年按價格分類的市場估計與預測

- 低價位

- 中號

- 高價位範圍

7. 依最終用途分類的市場估計與預測,2022-2035 年

- 個人使用

- 水療中心及美容院

- 皮膚科診所

- 其他

第8章 按分銷管道分類的市場估算與預測,2022-2035年

- 線上

- 電子商務

- 我們的網站

- 離線

- 超級市場/大賣場

- 專賣店

- 其他(個體店、百貨公司等)

第9章 2022-2035年各地區市場估算與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- AbbVie

- Bayer

- Beiersdorf

- Estee Lauder

- Galderma

- Honasa Consumer

- Johnson &Johnson

- L'Oreal

- Mario Badescu

- Natura &Co

- Pierre Fabre

- Shiseido

- Sunday Riley

- Teva

- Unilever

The Global Anti-acne Cosmetics Market was valued at USD 6.5 billion in 2025 and is estimated to grow at a CAGR of 5.4% to reach USD 11 billion by 2035.

Market growth is strongly influenced by the expanding clean beauty movement and the rising preference for natural and organic skincare formulations. Consumers are increasingly prioritizing products made with gentle, non-toxic, and naturally derived ingredients, driven by growing concerns about the potential side effects of synthetic compounds. This shift in consumer behavior is reshaping product development strategies across the industry, with manufacturers responding by reformulating offerings to align with clean-label expectations. Rising awareness of skin health, combined with increased spending on personal care, continues to support sustained demand. Additionally, growing interest in sustainable beauty practices and supportive regulatory frameworks promoting environmentally responsible products are reinforcing long-term market expansion. As skincare routines become more ingredient-conscious and wellness-oriented, anti-acne cosmetics are gaining wider acceptance across diverse age groups and skin types, supporting consistent growth beyond 2025.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.5 Billion |

| Forecast Value | $11 Billion |

| CAGR | 5.4% |

The creams and lotions segment generated USD 2.9 billion in 2025 and is expected to reach USD 5 billion by 2035. This segment remains dominant due to its versatility and ease of application. Consumers favor topical formats that not only help manage acne but also deliver complementary benefits such as moisturization, skin tone enhancement, and long-term skin maintenance. Changing consumer expectations toward multifunctional skincare solutions continue to strengthen demand for creams and lotions within the anti-acne category.

The individual-use segment accounted for 45.9% share in 2025. Growth in this segment is driven by increasing consumer preference for accessible, affordable, and convenient acne care solutions used at home. The shift toward self-care routines has reduced reliance on frequent professional treatments, offering time and cost efficiency. This trend reflects a broader movement toward personalized skincare and independent product selection, reinforcing the importance of individual consumers in driving overall market growth.

United States Anti-acne Cosmetics Market held 74.5% share in 2025. Market leadership is supported by strong consumer awareness, high adoption of over-the-counter skincare products, and widespread availability of advanced dermatological solutions. The presence of established premium brands, combined with digital marketing influence and growing demand for clinically validated cosmetic products, continues to accelerate market penetration.

Key companies operating in the Global Anti-acne Cosmetics Market include L'Oreal, Johnson & Johnson, Unilever, Estee Lauder, Beiersdorf, Galderma, Shiseido, Bayer, AbbVie, Natura & Co, Pierre Fabre, Sunday Riley, Mario Badescu, Honasa Consumer, and Teva. Companies in the Anti-acne Cosmetics Market are strengthening their market position through product innovation, clean-label reformulations, and sustainability-focused strategies. Leading players are investing in research to develop gentle yet effective formulations that align with natural and dermatologically tested standards. Expansion across digital and direct-to-consumer channels is improving brand reach and customer engagement. Firms are also leveraging influencer marketing, personalization tools, and targeted product portfolios to capture specific consumer segments.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Price

- 2.2.4 End Use

- 2.2.5 Distribution Channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of acne among adolescents and adults.

- 3.2.1.2 Growing awareness and dermatological consultations.

- 3.2.1.3 Innovation in formulations and delivery systems.

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Changing consumer preferences and trends

- 3.2.2.2 Counterfeit and imitation products

- 3.2.3 Opportunities

- 3.2.3.1 Integration of smart skincare and personalization.

- 3.2.3.2 Sustainability and clean beauty trends.

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By product type

- 3.6.2 By region

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Gap analysis

- 3.10 Risk assessment and mitigation

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

- 3.13 Consumer behaviour analysis

- 3.13.1 Purchasing patterns

- 3.13.2 Preference analysis

- 3.13.3 Regional variations in consumer behaviour

- 3.13.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022-2035 (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Masks

- 5.3 Creams & lotions

- 5.4 Cleansers & toners

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Price, 2022-2035 (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Low

- 6.3 Medium

- 6.4 High

Chapter 7 Market Estimates & Forecast, By End Use, 2022-2035 (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Individual use

- 7.3 Spas and parlors

- 7.4 Dermatological clinics

- 7.5 Others

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Online

- 8.2.1 E-Commerce

- 8.2.2 Company website

- 8.3 Offline

- 8.3.1 Supermarkets/Hypermarkets

- 8.3.2 Specialty Stores

- 8.3.3 Others (Individual stores, Departmental stores, etc.)

Chapter 9 Market Estimates & Forecast, By Region, 2022-2035 (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 France

- 9.3.3 UK

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AbbVie

- 10.2 Bayer

- 10.3 Beiersdorf

- 10.4 Estee Lauder

- 10.5 Galderma

- 10.6 Honasa Consumer

- 10.7 Johnson & Johnson

- 10.8 L'Oreal

- 10.9 Mario Badescu

- 10.10 Natura & Co

- 10.11 Pierre Fabre

- 10.12 Shiseido

- 10.13 Sunday Riley

- 10.14 Teva

- 10.15 Unilever

痤瘡治療化妝品市場-2026-2032年全球市場預測痤瘡治療面膜市場:2026-2032年全球市場預測(按產品類型、成分、原料、分銷管道和最終用戶分類)痤瘡治療市場:2026-2032年全球市場預測(按藥物類型、治療類別、痤瘡類型、分銷管道、患者群體和最終用戶分類)

痤瘡治療化妝品市場-2026-2032年全球市場預測痤瘡治療面膜市場:2026-2032年全球市場預測(按產品類型、成分、原料、分銷管道和最終用戶分類)痤瘡治療市場:2026-2032年全球市場預測(按藥物類型、治療類別、痤瘡類型、分銷管道、患者群體和最終用戶分類) 痤瘡治療市場:按藥物類別、類型、適應症、劑型、分銷管道和地區分類

痤瘡治療市場:按藥物類別、類型、適應症、劑型、分銷管道和地區分類 痤瘡治療市場規模、佔有率、趨勢和預測:按痤瘡類型、藥物類別、劑型、給藥途徑和地區分類,2026-2034 年痤瘡護理化妝品市場:按產品類型、性別、價格範圍、配方、銷售管道和地區分類

痤瘡治療市場規模、佔有率、趨勢和預測:按痤瘡類型、藥物類別、劑型、給藥途徑和地區分類,2026-2034 年痤瘡護理化妝品市場:按產品類型、性別、價格範圍、配方、銷售管道和地區分類 抗痘化妝品市場分析及預測(至2035年):依類型、產品、技術、成分、應用、劑型、部署方式、最終用戶及功能分類痤瘡治療藥物市場分析及預測(至2035年):依類型、產品、技術、應用、劑型、最終用戶、給藥途徑、治療階段及溶液分類

抗痘化妝品市場分析及預測(至2035年):依類型、產品、技術、成分、應用、劑型、部署方式、最終用戶及功能分類痤瘡治療藥物市場分析及預測(至2035年):依類型、產品、技術、應用、劑型、最終用戶、給藥途徑、治療階段及溶液分類 全球抗痘化妝品市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球抗痘化妝品市場規模、佔有率、趨勢和成長分析報告(2026-2034) 抗痘化妝品市場-全球產業規模、佔有率、趨勢、機會和預測:按類型、最終用戶、配方、分銷管道、地區和競爭格局分類,2021-2031年

抗痘化妝品市場-全球產業規模、佔有率、趨勢、機會和預測:按類型、最終用戶、配方、分銷管道、地區和競爭格局分類,2021-2031年