|

市場調查報告書

商品編碼

1936623

乳酸市場機會、成長要素、產業趨勢分析及2026年至2035年預測Lactic Acid Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

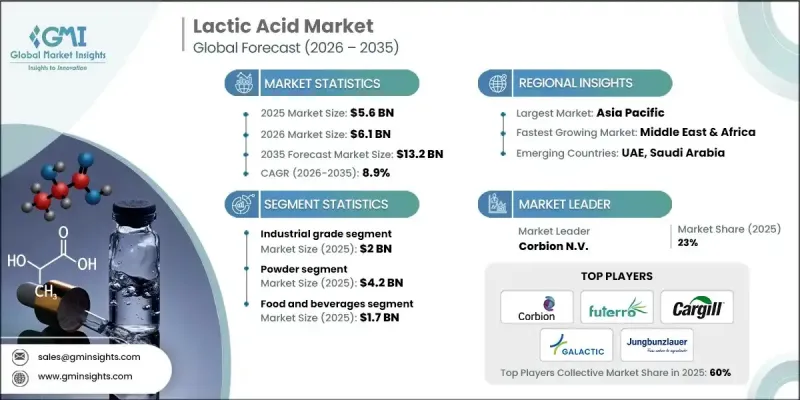

全球乳酸市場預計到 2025 年將達到 56 億美元,到 2035 年將達到 132 億美元,年複合成長率為 8.9%。

乳酸作為生物基聚合物(尤其是聚乳酸 (PLA))的關鍵原料,其重要性日益凸顯,推動了市場擴張。日益嚴格的環境法規和企業永續性措施正在加速包裝、消費品和工業應用領域從傳統塑膠向可生物分解替代品的轉型。除了傳統的食品應用外,乳酸在大規模工業應用中的採用率也越來越高,從而支撐了市場的穩定成長。汽車和航太等行業的需求也刺激了市場需求,因為製造商正在尋求輕質、永續的材料以提高燃油效率並減少排放。乳酸衍生物在內飾零件、複合材料和非結構材料中的應用越來越廣泛,在這些領域,輕量化和環境友善至關重要。乳酸在高階應用領域的逐步普及增強了其在各行業的長期發展前景。發酵和聚合物加工技術的進步,以及全球對生物基材料的關注,進一步提升了其市場潛力。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 56億美元 |

| 預測金額 | 132億美元 |

| 複合年成長率 | 8.9% |

預計到2025年,工業乳酸市場規模將達20億美元。其市場主導地位歸功於其在生質塑膠、化學中間體、溶劑和工業流程中的廣泛應用,以及其高產量和成本效益。工業乳酸非常適合大規模發酵和聚合物生產,因此成為全球包裝、特殊化學品和生物聚合物生產商的首選原料。

以物理形態分類,粉狀乳酸市場預計到2025年將達到42億美元。粉狀乳酸因其穩定性高、保存期限長、易於儲存和運輸而備受青睞。它廣泛應用於食品加工、製藥和工業組合藥物,在這些領域中,精確計量、低操作風險和與乾混料的相容性至關重要。粉狀乳酸易於批量管理,且擁有廣泛的分銷網路,這進一步鞏固了其在全球供應鏈中的主導地位。

預計到2025年,北美乳酸市場規模將達到14億美元。美國約佔全球乳酸市場的25%,這主要得益於其先進的發酵基礎設施以及對生質塑膠、食品飲料、醫藥和個人保健產品等領域的高需求。豐富的原料來源、先進的生物加工技術以及成熟的工業消費模式,共同支撐了該地區的市場領先地位。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段的附加價值

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 促進要素

- 對天然、潔淨標示的食品防腐劑的需求日益成長

- 消費者正逐漸拋棄合成添加劑

- 3.生質塑膠市場和循環經濟計劃的不斷成長

- 產業潛在風險與挑戰

- 室溫下緩慢分解

- 缺乏工業堆肥基礎設施

- 市場機遇

- 木質纖維素和非食品原料的開發

- 將溫室氣體轉化為乳酸的技術

- 促進要素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 產品類型

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利狀態

- 貿易統計(HS編碼)(註:僅提供主要國家的貿易統計)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續努力

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章 各等級市場估算與預測,2022-2035年

- 食品級

- 工業級

- 醫藥級

- 技術級

- 化妝品級

- 其他

6. 依實物形式分類的市場估算與預測,2022-2035 年

- 粉末

- 液體

第7章 按應用領域分類的市場估算與預測,2022-2035年

- 聚醯胺和尼龍

- 塑化劑

- 潤滑油和潤滑脂

- 合成潤滑油

- 複合油脂

- 金屬加工油

- 化妝品和個人護理

- 黏合劑和密封劑

- 油漆和塗料

- 其他

第8章 2022-2035年各地區市場估算與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第9章:公司簡介

- Corbion NV

- Arkema

- BASF SE

- DSM-Firmenich

- Evonik Industries

- JIAAN BIOTECH

- Galactic

- Jungbunzlauer Suisse AG, Basel

- Cargill Incorporated

- TEIJIN LIMITED

- Musashino Chemical(China)Co., Ltd.

- Futerro

- DOW

- NatureWorks LLC

The Global Lactic Acid Market was valued at USD 5.6 billion in 2025 and is estimated to grow at a CAGR of 8.9% to reach USD 13.2 billion by 2035.

Market expansion is driven by the growing importance of lactic acid as a core raw material for bio-based polymers, particularly polylactic acid (PLA). Increasing environmental regulations and corporate sustainability commitments are accelerating the shift from conventional plastics to biodegradable alternatives across packaging, consumer goods, and industrial applications. Beyond traditional food use, lactic acid is increasingly incorporated into high-volume industrial applications, maintaining steady market growth. Additionally, sectors like automotive and aerospace are stimulating demand, as manufacturers seek lightweight and sustainable materials to improve fuel efficiency and reduce emissions. Lactic acid derivatives are finding wider adoption in interior components, composite blends, and non-structural materials, where weight reduction and ecological compliance are crucial. This gradual incorporation into high-end applications strengthens the long-term outlook for lactic acid across industries. Technological advancements in fermentation and polymer processing, along with global emphasis on bio-based materials, continue to reinforce its market potential.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.6 Billion |

| Forecast Value | $13.2 Billion |

| CAGR | 8.9% |

The industrial-grade lactic acid segment accounted for USD 2 billion in 2025. Its dominance stems from broad applications in bioplastics, chemical intermediates, solvents, and industrial processing, coupled with high production volumes and cost-effectiveness. Industrial-grade lactic acid is ideal for large-scale fermentation and polymer manufacturing, making it the preferred choice for packaging, specialty chemicals, and biopolymer producers worldwide.

By physical form, the powder segment reached USD 4.2 billion in 2025. Powdered lactic acid is favored for its high stability, long shelf life, easy storage, and convenient transportation. It is widely used in food processing, pharmaceuticals, and industrial formulations where precise dosing, low handling risk, and compatibility with dry blends are critical. Its suitability for bulk management and broad distribution networks further reinforces its position as the dominant form in global supply chains.

North America Lactic Acid Market captured USD 1.4 billion in 2025. The U.S. accounted for roughly 25% of the global lactic acid market, driven by its advanced fermentation infrastructure and high demand for bioplastics, food and beverage applications, pharmaceuticals, and personal care products. The availability of abundant feedstock, sophisticated bioprocessing capabilities, and established industrial consumption patterns support the region's market leadership.

Key companies operating in the Global Lactic Acid Market include Arkema, Corbion N.V., BASF SE, DSM-Firmenich, Evonik Industries, Cargill Incorporated, Galactic, JIAAN BIOTECH, Jungbunzlauer Suisse AG, TEIJIN LIMITED, Musashino Chemical (China) Co., Ltd., Futerro, DOW, and NatureWorks LLC. Leading players in the lactic acid market are strengthening their positions through strategies such as expanding production capacity, improving fermentation technologies, and diversifying into high-value biopolymer derivatives. Companies are investing in research and development to enhance purity, yield, and bio-based product integration. Strategic partnerships and acquisitions allow firms to extend regional footprints and secure raw material supply chains. Focus on sustainable and cost-effective production processes, as well as product innovation for industrial, pharmaceutical, and food-grade applications, enables these companies to maintain competitiveness.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Grade

- 2.2.3 Physical Form

- 2.2.4 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for natural & clean-label food preservatives

- 3.2.1.2 Consumer shift away from synthetic additives

- 3.2.1. 3 Growing bioplastics market & circular economy initiatives

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Slow degradation in ambient conditions

- 3.2.2.2 Limited industrial composting infrastructure

- 3.2.3 Market opportunities

- 3.2.3.1 Lignocellulosic & non-food feedstock development

- 3.2.3.2 Greenhouse gas-to-lactic acid technology

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 Product type

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Grade, 2022 - 2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Food grade

- 5.3 Industrial grade

- 5.4 Pharmaceutical grade

- 5.5 Technical grade

- 5.6 Cosmetic grade

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Physical Form, 2022 - 2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Powder

- 6.3 Liquid

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Polyamides & nylons

- 7.3 Plasticizers

- 7.4 Lubricants & greases

- 7.4.1 Synthetic lubricants

- 7.4.2 Complex greases

- 7.4.3 Metalworking fluids

- 7.5 Cosmetics & personal care

- 7.6 Adhesives & sealants

- 7.7 Coatings & paints

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Corbion N.V.

- 9.2 Arkema

- 9.3 BASF SE

- 9.4 DSM-Firmenich

- 9.5 Evonik Industries

- 9.6 JIAAN BIOTECH

- 9.7 Galactic

- 9.8 Jungbunzlauer Suisse AG, Basel

- 9.9 Cargill Incorporated

- 9.10 TEIJIN LIMITED

- 9.11 Musashino Chemical (China) Co., Ltd.

- 9.12 Futerro

- 9.13 DOW

- 9.14 NatureWorks LLC

乳酸市場-2026-2032年全球市場預測

乳酸市場-2026-2032年全球市場預測 乳酸市場規模、佔有率和趨勢分析報告:按原料、應用、地區和細分市場預測(2026-2033 年)

乳酸市場規模、佔有率和趨勢分析報告:按原料、應用、地區和細分市場預測(2026-2033 年) 乳酸和聚乳酸市場規模、佔有率和成長分析:按產品類型、原料、應用、最終用途產業、形態、製造技術和地區分類-2026-2033年產業預測

乳酸和聚乳酸市場規模、佔有率和成長分析:按產品類型、原料、應用、最終用途產業、形態、製造技術和地區分類-2026-2033年產業預測 乳酸市場:依原料、應用和地區分類

乳酸市場:依原料、應用和地區分類 全球聚乳酸市場規模、佔有率、趨勢和成長分析報告(2026-2034年)乳酸市場規模、佔有率、成長及全球產業分析:按類型、應用和地區的洞察,2026-2034年的預測乳酸全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)耐熱乳酸市場:按類型、等級、形態、應用和分銷管道分類,全球預測(2026-2032年)

全球聚乳酸市場規模、佔有率、趨勢和成長分析報告(2026-2034年)乳酸市場規模、佔有率、成長及全球產業分析:按類型、應用和地區的洞察,2026-2034年的預測乳酸全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)耐熱乳酸市場:按類型、等級、形態、應用和分銷管道分類,全球預測(2026-2032年) 日本乳酸市場報告:按原料、形態、應用和地區分類(2026-2034年)

日本乳酸市場報告:按原料、形態、應用和地區分類(2026-2034年) 乳酸市場規模、佔有率及成長分析(按來源、形態、應用和地區分類)-2026-2033年產業預測

乳酸市場規模、佔有率及成長分析(按來源、形態、應用和地區分類)-2026-2033年產業預測