|

市場調查報告書

商品編碼

1844454

南美乳酸:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)South America Lactic Acid - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

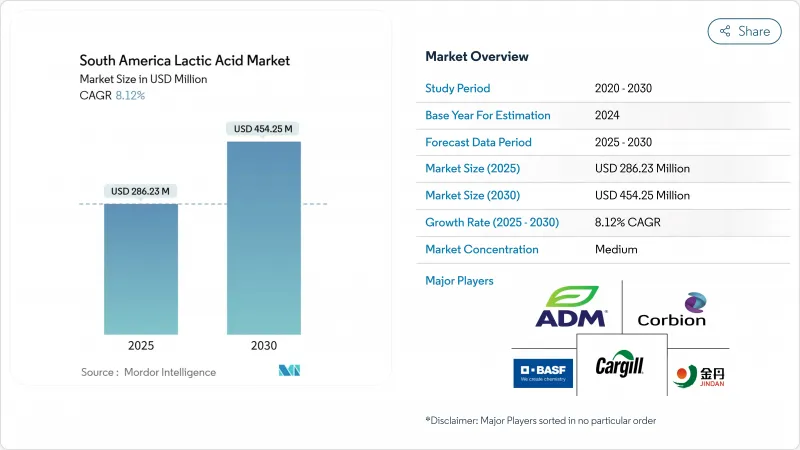

南美乳酸市場預計將從 2025 年的 2.8623 億美元成長到 2030 年的 4.5425 億美元,複合年成長率為 8.12%。

這種快速成長主要得益於對生物基化學品日益成長的需求,而該地區豐富的甘蔗和玉米原料蘊藏量則為其提供了支持。此外,巴西的支持性能源和產業政策發揮關鍵作用。食品加工行業傾向於潔淨標示配方,而製藥和個人護理行業正在擴大其應用,進一步推動了市場成長。地理差異顯著影響市場動態。巴西的綜合甘蔗綜合體是該地區的供應支柱,確保了原料的穩定供應。受各行各業需求成長的推動,哥倫比亞已成為成長最快的消費市場。相較之下,阿根廷和智利已經磨練出專注於特定應用的高價利基市場。適度的競爭為區域和全球參與者提供了機會。企業正專注於高價值等級和應用,以鞏固其在這個快速成長的市場中的地位。

南美洲乳酸市場趨勢與見解

巴西植物性食品加工的成長將推動對天然酸味劑的需求

巴西植物性食品產業正在經歷重大的監管變革,預計將推動天然酸味劑在生產過程中的應用。巴西國家食品安全監督局(ANVISA)和巴西農業食品管理局(MAPA)等監管機構正積極完善其植物來源產品架構。這些更新旨在消除消費者的困惑,同時建立明確的最低標識和品質標準。這種監管轉變正在推動對天然防腐劑的標準化需求,而乳酸正成為關鍵的解決方案。提案的法規要求清晰的標籤以區分植物來源產品和動物性產品,鼓勵製造商根據潔淨標示和永續性發展的策略採用天然酸味劑。加工廠擴大將乳酸納入其生產流程,利用其在各種應用中(包括植物性肉類替代品、乳製品替代品和發酵產品)控制pH值和延長保存期限的優勢。該行業對創新的重視,尤其是對植物來源和潔淨標示產品的開發,進一步推動了對天然酸味劑的需求。這些成分不僅滿足不斷變化的監管要求,也滿足了消費者對永續和透明產品配方日益成長的期望。這種與監管和市場趨勢的雙重結合使得天然酸味劑成為巴西植物來源食品產業持續成長的重要組成部分。

烘焙業消費者對潔淨標示防腐劑的偏好日益成長

潔淨標示運動正在推動南美烘焙配方的重大變革,因為消費者越來越追求透明度和天然成分而不是合成替代品。有機酸,尤其是乳酸,由於其雙重功能而成為關鍵成分。乳酸透過兩種機制有效對抗大腸桿菌和沙門氏菌等食源性病原體:降低 pH 值和直接抗菌作用,同時維持烘焙點心的感官品質。此功能使配方師能夠在不影響食品安全標準的情況下取代合成防腐劑。在這種日益成長的需求的推動下,巴西的烘焙店正在採用基於乳酸的解決方案,不僅可以延長保存期限,而且符合清潔標籤的聲明。乳酸衍生物,例如 PURACAL® PP,不僅用於延長保存期限,還可以減少烘焙過程中形成的有害化合物丙烯醯胺的形成。這些新功能凸顯了乳酸的多功能性,使其成為烘焙店的戰略成分。透過滿足消費者對天然成分的偏好並遵守嚴格的食品安全法規,乳酸在重塑南美洲烘焙市場方面發揮關鍵作用。

原料(玉米、甘蔗)價格波動影響生產利潤

受天氣和政策因素影響,農業市場波動加劇,導致原料價格不穩定,南美乳酸生產商的利潤率面臨巨大壓力。在巴西,惡劣天候條件影響了甘蔗產量。儘管種植面積穩定,但預計2025/26年度甘蔗產量將比上一季減少2%。主要產區乾旱導致產量下降2.3%,導致依賴甘蔗衍生基質的製造商的原料成本上升。同時,玉米乙醇產量的快速擴張加劇了玉米原料的競爭。預計2024/25年度巴西玉米消費量將達到34.64億蒲式耳,屆時將有25家運作中的乙醇工廠與傳統的飼料和食品用途競爭。甘蔗供應減少和玉米需求上升的雙重挑戰已將國內原料價格推至2022年以來的最高水準。為了應對這些壓力,乳酸製造商正在最佳化其原料籌資策略,並積極探索替代基材選擇——這些措施對於在日益受到供應鏈中斷和投入成本上升影響的市場中保持競爭力至關重要。

細分分析

到2024年,天然乳酸將佔據92.04%的市場佔有率,並以8.52%的強勁複合年成長率持續成長,直至2030年。這項成長主要得益於巴西豐富的農業原料和消費者對生物基原料日益成長的需求。巴西先進的甘蔗加工基礎設施易於適應生化生產,與合成替代品相比具有顯著的成本優勢。此外,巴西農業部對天然飼料原料製定了嚴格的安全性和有效性標準,這推動了天然乳酸在動物營養中的應用。最近頒布的第15,070/2024號法律進一步加強了天然產品產業的發展,為農業和畜牧業中的微生物和生物技術產品製定了嚴格的品質標準,確保了產品的一致性和市場拓展。

此外,受政府扶持生物基化學品生產的舉措以及天然乳酸在潔淨標示食品中的使用激增的推動,市場正在經歷顯著成長。巴西能源研究機構預測,2023年,在甘蔗和玉米乙醇生產的推動下,甘蔗加工量將達到創紀錄的7.13億噸。這一成長動能為天然乳酸製造商提供了可靠的原料供應。此外,拉丁美洲開發銀行對永續發展和改善環境品質的承諾,進一步支持了在各種工業應用中優先選擇天然化學品而非合成化學品。

到2024年,液體乳酸將佔據60.11%的市場佔有率,這得益於其在大規模食品加工中的高效運作以及與飲料配方的無縫整合。液體乳酸易於操作且易於精確計量,是乳製品酸化、肉類保鮮和飲料pH值控制等應用的關鍵。這些特性使其成為南美洲龐大食品加工產業不可或缺的原料。此外,阿根廷嚴格的食品標準對乳製品和食品添加劑製定了具體的標準,從而促進了對液體酸化劑的標準化需求。這些酸味劑能夠與現有的加工系統無縫整合,進一步鞏固其市場主導地位。

粉劑和顆粒劑市場正在快速成長,預計到2030年複合年成長率將達到9.34%。這一成長得益於乾混應用和出口市場對耐儲存配方的日益青睞。該市場也受益於工業應用,尤其是水處理。世界銀行強調需要對拉丁美洲的污水基礎設施進行大規模投資,預計2010年至2030年間,該地區將在污水處理方面投資800億美元,在污水處理方面投資330億美元。這些投資為粉劑在工業水處理製程的應用創造了機會。此外,粉劑在動物飼料行業越來越受歡迎,其乾混能力和較長的保存期限帶來了營運優勢。這些特性對於服務該地區日益成長的畜牧業的飼料製造商尤其有價值,將進一步推動該市場的擴張。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況

- 市場促進因素

- 巴西植物來源食品加工的成長將推動對天然酸味劑的需求

- 烘焙業消費者對潔淨標示防腐劑的偏好日益成長

- 巴西政府對甘蔗生物基化學品生產的獎勵措施

- 增加乳酸在牲畜飼料酸化劑中的使用,以應對抗生素禁令

- 製藥公司在外用皮膚病製劑採用乳酸

- 南美洲都市區對發酵乳製品替代品的需求不斷成長

- 市場限制

- 原料(玉米、甘蔗)價格波動影響生產利潤

- 巴西境外食品級發酵基礎設施有限

- 更嚴格的廢水處理標準增加了安地斯國家的營運成本

- 來自亞洲的廉價進口酸味劑(如檸檬酸)的競爭

- 供應鏈分析

- 監理展望

- 五力分析

- 新進入者的威脅

- 購買者和消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭強度

第5章市場規模及成長預測

- 按來源

- 自然的

- 合成

- 按形式

- 液體

- 固體(粉末/顆粒)

- 按年級

- 食品級

- 工業級

- 醫藥級

- 化妝品級

- 按用途

- 飲食

- 麵包店

- 糖果甜點

- 乳製品

- 肉類、家禽和魚貝類

- 飲料

- 其他食品和飲料應用

- 個人護理和化妝品

- 製藥

- 動物飼料

- 工業和化學加工

- 飲食

- 按地區

- 巴西

- 阿根廷

- 哥倫比亞

- 智利

- 秘魯

- 南美洲其他地區

第6章 競爭態勢

- 市場集中度

- 策略舉措

- 市場排名分析

- 公司簡介

- Corbion NV

- Cargill, Incorporated

- BASF SE

- Archer-Daniels-Midland Company

- Galactic Holdings, Inc

- Henan Jindan Lactic Acid Co., Ltd.

- Jungbunzlauer Suisse AG, Basel

- Arshine Food Additives Co., Ltd.

- Cellulac plc,

- Brenntag AG

- Dsm-Firmenich AG

- Futerro SA

- Univar Solutions LLC.

- Shenzhen Esun Industrial Co., Ltd.

- BBCA Group Corporation

- International Flavors & Fragrances(Danisco)

- Natureworks LLC

- Musashino Chemical Laboratory, Ltd.

- DuPont de Nemours, Inc.

- Tokyo Chemical Industry Co., Ltd.

第7章 市場機會與未來展望

Projected to grow from a valuation of USD 286.23 million in 2025 to USD 454.25 million by 2030, the South America lactic acid market size is set to expand at a CAGR of 8.12%.

This surge is largely driven by a rising demand for bio-based chemicals, bolstered by the region's rich reserves of sugarcane and corn feedstocks. Additionally, Brazil's supportive energy and industrial policies play a pivotal role. The food processing sector is gravitating towards clean-label formulations, while the pharmaceutical and personal care industries are broadening their application spectrum, fueling the market's growth. Geographical nuances significantly influence the market dynamics. Brazil's integrated sugarcane complex stands as the backbone of the regional supply, guaranteeing a consistent feedstock. Colombia is rapidly emerging as the quickest-growing consumer market, spurred by heightened demand across diverse sectors. In contrast, Argentina and Chile are honing in on premium-priced niches, catering to specific applications. The competitive arena is moderately intense, presenting avenues for both regional entities and global corporations to stake their claim. Companies are zeroing in on high-value grades and applications, aiming to solidify their presence in this burgeoning market.

South America Lactic Acid Market Trends and Insights

Growth of plant-based food processing in brazil boosting demand for natural acidulants

Brazil's plant-based food sector is witnessing significant regulatory advancements, which are expected to drive the adoption of natural acidulants in manufacturing processes. Regulatory bodies such as ANVISA and MAPA are actively refining their frameworks for plant-based products. These updates aim to eliminate consumer confusion while establishing clear minimum identity and quality standards. This regulatory shift is fostering a standardized demand for natural preservatives, with lactic acid emerging as a key solution. The proposed regulations mandate clear labeling to distinguish plant-based products from animal-based ones, encouraging manufacturers to adopt natural acidulants that align with clean-label and sustainability-focused strategies. Processing facilities are increasingly integrating lactic acid into their operations, leveraging its benefits for pH control and shelf-life extension across various applications, including plant-based meat alternatives, dairy substitutes, and fermented products. The sector's emphasis on innovation, particularly in developing plant-based and clean-label offerings, is further fueling the demand for natural acidulants. These ingredients not only comply with evolving regulatory requirements but also meet growing consumer expectations for sustainable and transparent product formulations. This dual alignment with regulatory and market trends positions natural acidulants as essential components in the continued growth of Brazil's plant-based food sector.

Rising consumer preference for clean-label preservatives in bakery segment

The clean-label movement is driving significant changes in South American bakery formulations as consumers increasingly demand transparency and natural ingredients over synthetic alternatives. Organic acids, particularly lactic acid, are emerging as key components due to their dual functionality. Lactic acid effectively combats foodborne pathogens such as E. coli and Salmonella through its dual mechanism of pH reduction and direct antimicrobial action, all while maintaining the sensory quality of baked goods. This capability enables formulators to replace synthetic preservatives without compromising food safety standards. In response to this growing demand, Brazilian bakery manufacturers are adopting lactic acid-based solutions that not only extend shelf life but also align with clean-label claims. Beyond preservation, lactic acid derivatives, such as PURACAL(R) PP, are being utilized to reduce acrylamide formation-a harmful compound generated during baking processes. This additional functionality highlights the versatility of lactic acid, making it a strategic ingredient for bakery manufacturers. By addressing consumer preferences for natural ingredients and adhering to stringent food safety regulations, lactic acid is playing a pivotal role in reshaping the bakery market in South America.

Volatility in feedstock (corn, sugarcane) prices impacting production margins

South American lactic acid producers are facing significant margin pressures due to feedstock price instability, driven by heightened volatility in agricultural commodity markets influenced by climate and policy factors. In Brazil, sugarcane production remains under strain from adverse weather conditions. The 2025/26 harvest is projected to decline by 2% compared to the previous season, despite a stable cultivation area. This decline is attributed to a 2.3% drop in productivity caused by drought conditions in key producing regions, which is driving up feedstock costs for manufacturers reliant on sugarcane-derived substrates. Simultaneously, the rapid expansion of corn ethanol production is intensifying competition for corn feedstocks. Brazil's corn consumption is expected to reach 3,464 million bushels in 2024/25, as 25 operational ethanol plants compete with traditional feed and food applications. This dual challenge of reduced sugarcane availability and heightened corn demand has pushed domestic feedstock prices to their highest levels since 2022. To navigate these pressures, lactic acid producers are optimizing their feedstock sourcing strategies and actively exploring alternative substrate options. These measures are critical for maintaining competitive positioning in a market increasingly shaped by supply chain disruptions and rising input costs.

Other drivers and restraints analyzed in the detailed report include:

- Government incentives for sugarcane bio-based chemicals production in brazil

- Increasing utilization of lactic acid in livestock feed acidifiers to combat antibiotic ban

- Limited availability of food-grade fermentation infrastructure outside brazil

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2024, natural lactic acid commands a dominant 92.04% market share and is set to expand at a robust CAGR of 8.52% through 2030. This growth is largely driven by Brazil's rich agricultural feedstock and a rising consumer appetite for bio-based ingredients. Brazil's sophisticated sugarcane processing infrastructure, easily adaptable for biochemical production, provides a notable cost edge over synthetic counterparts. Furthermore, the Brazilian Ministry of Agriculture's stringent safety and efficacy standards for natural feed ingredients bolster the adoption of naturally derived lactic acid in animal nutrition. The recent enactment of Law #15,070/2024 further fortifies the natural segment, instituting rigorous quality benchmarks for microbial and biotechnological products in agriculture and livestock, thereby ensuring product consistency and market expansion.

Moreover, bolstered by government initiatives championing bio-based chemical production and the surging use of natural lactic acid in clean-label food products, the market is witnessing significant growth. In 2023, Brazil's Energy Research Office highlighted a record sugarcane processing volume of 713 million tons, buoyed by both sugarcane and corn-based ethanol production. This achievement guarantees a reliable feedstock supply for natural lactic acid producers. Additionally, the Development Bank of Latin America's commitment to sustainable development and enhancing environmental quality further propels the preference for natural chemicals over synthetic ones across diverse industrial applications.

In 2024, liquid lactic acid secures a significant 60.11% share of the market, driven by its operational efficiency in large-scale food processing and its seamless incorporation into beverage formulations. The liquid form offers ease of handling and precise dosing, which are critical for applications such as dairy acidification, meat preservation, and beverage pH control. These attributes make it indispensable in South America's expansive food processing industry. Additionally, Argentina's stringent food code, which outlines specific standards for dairy products and food additives, has fostered a standardized demand for liquid acidulants. These acidulants integrate effortlessly into existing processing systems, further solidifying their market dominance.

The powder and granules segment is poised for rapid growth, with a projected CAGR of 9.34% through 2030. This growth is fueled by the increasing preference for shelf-stable formulations in dry mix applications and export markets, where concentrated forms reduce transportation costs. The segment also benefits from industrial applications, particularly in water treatment. The World Bank has highlighted the need for significant investments in Latin America's wastewater infrastructure, estimating USD 80 billion for sewerage and USD 33 billion for wastewater treatment between 2010 and 2030. These investments create opportunities for powder forms in industrial water treatment processes. Moreover, the powder segment is gaining traction in the animal feed industry, where its dry mixing capabilities and extended shelf life provide operational advantages. These features are particularly valuable for feed manufacturers catering to the region's growing livestock sector, further driving the segment's expansion.

The South America Lactic Acid Market Report Segments the Industry by Source (Natural and Synthetic); Form (Liquid and Solid); Grade (Food Grade, Industrial Grade, Pharmaceutical Grade, and Cosmetic Grade); and Application (Food and Beverages, Personal Care and Cosmetics, Pharmaceutical, Animal Feed, and Industrial and Chemical Processing), and Geography (Brazil and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Corbion NV

- Cargill, Incorporated

- BASF SE

- Archer-Daniels-Midland Company

- Galactic Holdings, Inc

- Henan Jindan Lactic Acid Co., Ltd.

- Jungbunzlauer Suisse AG, Basel

- Arshine Food Additives Co., Ltd.

- Cellulac plc,

- Brenntag AG

- Dsm-Firmenich AG

- Futerro SA

- Univar Solutions LLC.

- Shenzhen Esun Industrial Co., Ltd.

- BBCA Group Corporation

- International Flavors & Fragrances (Danisco)

- Natureworks LLC

- Musashino Chemical Laboratory, Ltd.

- DuPont de Nemours, Inc.

- Tokyo Chemical Industry Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth of plant-based food processing in brazil boosting demand for natural acidulants

- 4.2.2 Rising consumer preference for clean-label preservatives in bakery segment

- 4.2.3 Government incentives for sugarcane bio-based chemicals production in brazil

- 4.2.4 Increasing utilization of lactic acid in livestock feed acidifiers to combat antibiotic ban

- 4.2.5 Pharmaceutical companies adopting lactic acid for topical drug formulations in dermatology

- 4.2.6 Rising demand for fermented dairy alternatives in urban south american markets

- 4.3 Market Restraints

- 4.3.1 Volatility in feedstock (corn, sugarcane) prices impacting production margins

- 4.3.2 Limited availability of food-grade fermentation infrastructure outside brazil

- 4.3.3 Stringent effluent disposal norms increasing operating costs in andean countries

- 4.3.4 Competition from cheaper imported acidulants such as citric acid from asia

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Source

- 5.1.1 Natural

- 5.1.2 Synthetic

- 5.2 By Form

- 5.2.1 Liquid

- 5.2.2 Solid (Powder/Granules)

- 5.3 By Grade

- 5.3.1 Food Grade

- 5.3.2 Industrial Grade

- 5.3.3 Pharmaceutical Grade

- 5.3.4 Cosmetic Grade

- 5.4 By Application

- 5.4.1 Food and Beverages

- 5.4.1.1 Bakery

- 5.4.1.2 Confectionery

- 5.4.1.3 Dairy Products

- 5.4.1.4 Meat, Poultry and, Seafood

- 5.4.1.5 Beverages

- 5.4.1.6 Other Food and Beverage Applications

- 5.4.2 Personal Care and Cosmetics

- 5.4.3 Pharmaceutical

- 5.4.4 Animal Feed

- 5.4.5 Industrial and Chemical Processing

- 5.4.1 Food and Beverages

- 5.5 By Geography

- 5.5.1 Brazil

- 5.5.2 Argentina

- 5.5.3 Colombia

- 5.5.4 Chile

- 5.5.5 Peru

- 5.5.6 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Corbion NV

- 6.4.2 Cargill, Incorporated

- 6.4.3 BASF SE

- 6.4.4 Archer-Daniels-Midland Company

- 6.4.5 Galactic Holdings, Inc

- 6.4.6 Henan Jindan Lactic Acid Co., Ltd.

- 6.4.7 Jungbunzlauer Suisse AG, Basel

- 6.4.8 Arshine Food Additives Co., Ltd.

- 6.4.9 Cellulac plc,

- 6.4.10 Brenntag AG

- 6.4.11 Dsm-Firmenich AG

- 6.4.12 Futerro SA

- 6.4.13 Univar Solutions LLC.

- 6.4.14 Shenzhen Esun Industrial Co., Ltd.

- 6.4.15 BBCA Group Corporation

- 6.4.16 International Flavors & Fragrances (Danisco)

- 6.4.17 Natureworks LLC

- 6.4.18 Musashino Chemical Laboratory, Ltd.

- 6.4.19 DuPont de Nemours, Inc.

- 6.4.20 Tokyo Chemical Industry Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

乳酸市場:2026-2032年全球市場預測(依原料、狀態、等級、形態和應用分類)

乳酸市場:2026-2032年全球市場預測(依原料、狀態、等級、形態和應用分類) 乳酸全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)

乳酸全球市場規模、佔有率、趨勢和成長分析報告(2026-2034) 乳酸市場機會、成長要素、產業趨勢分析及2026年至2035年預測耐熱乳酸市場:按類型、等級、形態、應用和分銷管道分類,全球預測(2026-2032年)

乳酸市場機會、成長要素、產業趨勢分析及2026年至2035年預測耐熱乳酸市場:按類型、等級、形態、應用和分銷管道分類,全球預測(2026-2032年) 日本乳酸市場報告:按原料、形態、應用和地區分類(2026-2034年)

日本乳酸市場報告:按原料、形態、應用和地區分類(2026-2034年) 乳酸市場規模、佔有率及成長分析(按來源、形態、應用和地區分類)-2026-2033年產業預測

乳酸市場規模、佔有率及成長分析(按來源、形態、應用和地區分類)-2026-2033年產業預測 乳酸市場規模、佔有率和趨勢分析報告:按原料、應用、地區和細分市場預測(2026-2033 年)

乳酸市場規模、佔有率和趨勢分析報告:按原料、應用、地區和細分市場預測(2026-2033 年) 乳酸市場-全球產業規模、佔有率、趨勢、機會與預測,按應用、原料、地區和競爭細分,2020-2030 年

乳酸市場-全球產業規模、佔有率、趨勢、機會與預測,按應用、原料、地區和競爭細分,2020-2030 年 乳酸:市場佔有率分析、產業趨勢、統計數據、成長預測(2025-2030)

乳酸:市場佔有率分析、產業趨勢、統計數據、成長預測(2025-2030) 乳酸的全球市場:來歷,各等級,各用途,各終端用戶產業,各地區,機會,預測,2018年~2032年

乳酸的全球市場:來歷,各等級,各用途,各終端用戶產業,各地區,機會,預測,2018年~2032年