|

市場調查報告書

商品編碼

1936622

休閒船舶洗滌器系統市場:機會、成長要素、產業趨勢分析及預測(2026-2035年)Recreational Marine Scrubber Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

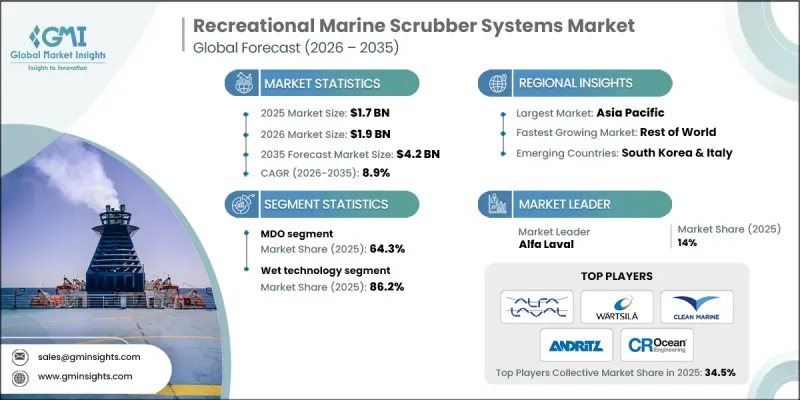

全球休閒船舶洗滌器系統市場預計到 2025 年將達到 17 億美元,到 2035 年將達到 42 億美元,年複合成長率為 8.9%。

全球對環境永續性的日益關注和更嚴格的船舶排放標準的訂定,推動了市場成長。為了在繼續使用高硫燃料的同時遵守排放法規,休閒船舶船東正在採用脫硫系統,從而在燃料管理方面實現柔軟性和成本效益。這些系統在燃料品質要求各異的地區尤其重要,為營運商提供了經濟高效且營運便利的解決方案。船隊改造和維修以及綠色航海實踐的投資增加,進一步推動了市場需求。休閒遊艇產業的成長也影響著脫硫系統的普及。船東優先考慮兼顧環境責任、性能和維護效率的綠色技術。隨著各國努力清理沿海水域,拉丁美洲、非洲和大洋洲等地區的脫硫系統應用正迅速普及。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始金額 | 17億美元 |

| 預測金額 | 42億美元 |

| 複合年成長率 | 8.9% |

預計到2025年,船用柴油(MDO)市佔率將達到64.3%,並在2035年之前以9.2%的複合年成長率成長。 MDO因其燃燒更清潔、燃油效率更高以及能夠與脫硫系統無縫整合,幫助船舶滿足嚴格的環保法規要求,同時保持運營成本效益,因而越來越受歡迎。其多功能性使船東能夠在不影響性能的情況下切換高硫和低硫燃料,使其成為休閒海上作業的實用靈活之選。

預計到2025年,濕式洗滌器技術領域的市佔率將達到86.2%,並在2026年至2035年間以9.2%的複合年成長率成長。濕式洗滌器因其卓越的硫氧化物、氮氧化物和顆粒物去除能力而備受青睞,確保符合國際排放標準。其對不同尺寸船舶和運作條件的適應性使其適用於新造船和改造計劃。對能夠提高燃料柔軟性並滿足嚴格環保法規的多污染物控制系統的需求不斷成長,正在推動濕式洗滌器的應用。

預計2025年,美國休閒船舶洗滌器系統市場將佔全球市場的71.1%,2035年將成長至7.35億美元。來自美國環保署(EPA)等監管機構的壓力,以及大規模的休閒船艇群體和人們對永續航行方式日益成長的興趣,都在推動洗滌器的應用。更嚴格的監管合規要求和消費者對環保船舶的偏好也進一步促進了洗滌器的安裝。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 產業生態系統

- 原物料供應及採購分析

- 製造能力評估

- 供應鏈韌性與風險因素

- 配電網路分析

- 監管環境

- 產業影響因素

- 促進要素

- 產業潛在風險與挑戰

- 成長潛力分析

- 成本結構分析

- 波特五力分析

- PESTEL 分析

- 新的機會與趨勢

- 數位化和物聯網整合

- 拓展新興市場

- 投資分析及未來展望

第4章 競爭情勢

- 介紹

- 按地區分類的公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 其他地區

- 戰略儀錶板

- 策略舉措

- 企業標竿管理

- 創新與科技趨勢

第5章 依燃料類型分類的市場規模及預測(2022-2035年)

- MDO

- MGO

- 混合

- 其他

第6章 依應用領域分類的市場規模及預測(2022-2035年)

- 濕法技術

- 乾式科技

第7章 2022-2035年各地區市場規模及預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 希臘

- 亞太地區

- 中國

- 日本

- 韓國

- 馬來西亞

- 印尼

- 其他地區

第8章:公司簡介

- ANDRITZ

- Aarco Engineering Projects Pvt. Ltd.

- Albion Marine Solutions

- Alfa Laval

- Brenntag Asia Pacific Pte Ltd

- Clean Marine

- CR Ocean Engineering

- DuPont Clean Technologies

- Ecospray Technologies

- Fuji Electric

- Langh Tech

- ME Production

- Nicro

- SAACKE

- Solvay

- VDL AEC Maritime

- Yara Marine Technologies

The Global Recreational Marine Scrubber Systems Market was valued at USD 1.7 billion in 2025 and is estimated to grow at a CAGR of 8.9% to reach USD 4.2 billion by 2035.

Market growth is driven by increasing global emphasis on environmental sustainability and stricter maritime emission standards. Recreational vessel owners are adopting scrubber systems to continue using high-sulfur fuels while remaining compliant with emission regulations, offering flexibility in fuel management and cost efficiency. These systems are especially valuable in regions with varying fuel quality requirements, providing operators with a cost-effective and operationally efficient solution. Rising investment in fleet retrofitting, refurbishment, and green maritime practices is further fueling demand. Scrubber adoption is also influenced by the growing recreational boating sector, where vessel owners prioritize eco-friendly technologies that balance environmental responsibility with performance and maintenance efficiency. Regions including Latin America, Africa, and Oceania are witnessing rapid uptake as nations push for cleaner coastal waters.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.7 Billion |

| Forecast Value | $4.2 Billion |

| CAGR | 8.9% |

The marine diesel oil (MDO) segment held a 64.3% share in 2025 and is projected to grow at a CAGR of 9.2% through 2035. MDO is increasingly favored due to its ability to deliver cleaner combustion, improved fuel efficiency, and seamless integration with scrubber systems, helping operators meet strict environmental regulations while maintaining operational cost-effectiveness. Its versatility allows vessel owners to switch between high- and low-sulfur fuels without compromising performance, making it a practical and flexible choice for recreational maritime operations.

The wet scrubber technology segment accounted for an 86.2% share in 2025 and is expected to grow at a CAGR of 9.2% from 2026 to 2035. Wet scrubbers are preferred for their superior ability to remove sulfur oxides, nitrogen oxides, and particulate matter, ensuring compliance with international emission standards. Their adaptability to various vessel sizes and operational conditions makes them suitable for both new builds and retrofitting projects. Increasing demand for multi-pollutant control systems, capable of meeting stringent environmental regulations while enhancing fuel flexibility, is boosting the uptake of wet scrubbers.

U.S. Recreational Marine Scrubber Systems Market held a 71.1% share in 2025 and is expected to generate USD 735 million by 2035. Regulatory pressure from agencies like the EPA, along with a large recreational boating community and growing interest in sustainable boating, is driving scrubber adoption. Increasing compliance requirements and consumer preference for eco-friendly vessels are further boosting installations.

Key players in the Global Recreational Marine Scrubber Systems Market include: Andritz, Alfa Laval, CR Ocean Engineering, Clean Marine AS, Damen Shipyards Group, EnviroCare, Ecospray Technologies S.r.l., Fuji Electric, Hitachi Energy, KwangSung, Keppel, LiqTech, ME Production, Mitsubishi Heavy Industries, Nicro, SAACKE, Valmet, VDL AEC Maritime, Wartsila, Yara. Companies in the recreational marine scrubber systems market are employing strategies to strengthen their market foothold by investing in R&D for more compact, efficient, and multi-pollutant scrubbing solutions. Manufacturers are expanding global service networks, forming partnerships with shipyards, and targeting regions with emerging environmental regulations. Additionally, companies focus on retrofitting existing fleets, providing customized solutions for different vessel types, and promoting cost-effective, fuel-flexible technologies to enhance customer adoption. Strategic marketing campaigns emphasizing environmental compliance and operational efficiency also reinforce brand positioning and long-term growth.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Market estimates & forecast parameters

- 1.3 Forecast

- 1.3.1 Key trends for market estimates

- 1.3.1.1 Quantified market impact analysis

- 1.3.2 Mathematical impact of growth parameters on forecast

- 1.3.3 Scenario analysis framework

- 1.3.1 Key trends for market estimates

- 1.4 Primary research and validation

- 1.4.1 Some of the primary sources (but not limited to)

- 1.5 Data mining sources

- 1.5.1 Paid Sources

- 1.5.2 Sources, by region

- 1.6 Research trail & scoring components

- 1.6.1 Research trail components

- 1.6.2 Scoring components

- 1.7 Research transparency addendum

- 1.7.1 Source attribution framework

- 1.7.2 Quality assurance metrics

- 1.7.3 Our commitment to trust

- 1.8 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Fuel trends

- 2.4 Technology trends

- 2.5 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Cost structure analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

- 3.7.1 Political factors

- 3.7.2 Economic factors

- 3.7.3 Social factors

- 3.7.4 Technological factors

- 3.7.5 Legal factors

- 3.7.6 Environmental factors

- 3.8 Emerging opportunities & trends

- 3.8.1 Digitalization & IoT integration

- 3.8.2 Emerging market penetration

- 3.9 Investment analysis and future outlook

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Rest of World

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.5 Company benchmarking

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Fuel, 2022 - 2035 (USD Million & Units)

- 5.1 Key trends

- 5.2 MDO

- 5.3 MGO

- 5.4 Hybrid

- 5.5 Others

Chapter 6 Market Size and Forecast, By Application, 2022 - 2035 (USD Million & Units)

- 6.1 Key trends

- 6.2 Wet technology

- 6.3 Dry technology

Chapter 7 Market Size and Forecast, By Region, 2022 - 2035 (USD Million & Units)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 France

- 7.3.3 UK

- 7.3.4 Italy

- 7.3.5 Greece

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 South Korea

- 7.4.4 Malaysia

- 7.4.5 Indonesia

- 7.5 Rest of World

Chapter 8 Company Profiles

- 8.1 ANDRITZ

- 8.2 Aarco Engineering Projects Pvt. Ltd.

- 8.3 Albion Marine Solutions

- 8.4 Alfa Laval

- 8.5 Brenntag Asia Pacific Pte Ltd

- 8.6 Clean Marine

- 8.7 CR Ocean Engineering

- 8.8 DuPont Clean Technologies

- 8.9 Ecospray Technologies

- 8.10 Fuji Electric

- 8.11 Langh Tech

- 8.12 ME Production

- 8.13 Nicro

- 8.14 SAACKE

- 8.15 Solvay

- 8.16 VDL AEC Maritime

- 8.17 Yara Marine Technologies

全球船舶濕式洗滌器系統市場(按洗滌器系統類型、船舶類型、安裝類型、流動機制和分配管道分類)預測(2026-2032年)

全球船舶濕式洗滌器系統市場(按洗滌器系統類型、船舶類型、安裝類型、流動機制和分配管道分類)預測(2026-2032年) 2026年全球船舶洗滌器系統市場報告

2026年全球船舶洗滌器系統市場報告 乾式船舶洗滌器系統市場機會、成長要素、產業趨勢分析及2026年至2035年預測

乾式船舶洗滌器系統市場機會、成長要素、產業趨勢分析及2026年至2035年預測 船舶洗滌器市場規模、佔有率及成長分析(按技術、應用、安裝方式、最終用戶和地區分類)-2026-2033年產業預測

船舶洗滌器市場規模、佔有率及成長分析(按技術、應用、安裝方式、最終用戶和地區分類)-2026-2033年產業預測 船舶洗滌器系統市場規模、佔有率及成長分析(按技術、燃料、應用和地區分類)-產業預測(2026-2033 年)按系統配置、船舶類型、安裝類型和洗滌器技術分類的船舶洗滌器系統市場-全球預測,2025年至2032年船舶洗滌器系統市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

船舶洗滌器系統市場規模、佔有率及成長分析(按技術、燃料、應用和地區分類)-產業預測(2026-2033 年)按系統配置、船舶類型、安裝類型和洗滌器技術分類的船舶洗滌器系統市場-全球預測,2025年至2032年船舶洗滌器系統市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 船用洗滌器市場規模、佔有率、趨勢分析報告:按類型、安裝類型、應用、地區、細分市場預測,2025-2030 年濕式船舶洗滌器系統市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測商用乾式船用洗滌器系統市場機會、成長促進因素、產業趨勢分析與預測 2024 - 2032 年

船用洗滌器市場規模、佔有率、趨勢分析報告:按類型、安裝類型、應用、地區、細分市場預測,2025-2030 年濕式船舶洗滌器系統市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測商用乾式船用洗滌器系統市場機會、成長促進因素、產業趨勢分析與預測 2024 - 2032 年