|

市場調查報告書

商品編碼

1936605

遊戲引擎市場機會、成長要素、產業趨勢分析及2026年至2035年預測Game Engine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

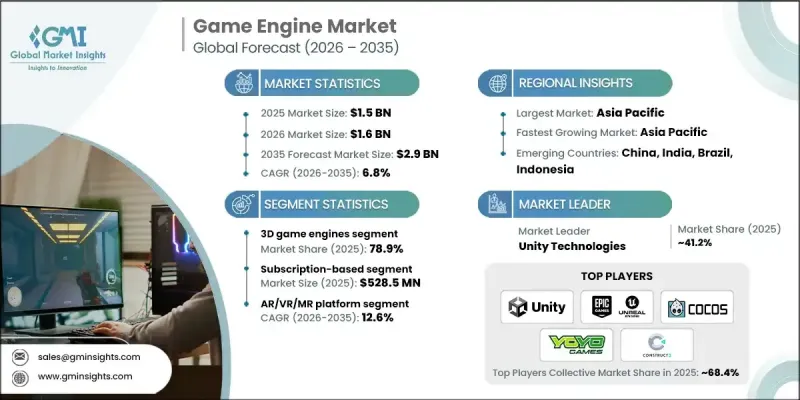

全球遊戲引擎市場預計到 2025 年將達到 15 億美元,到 2035 年將達到 29 億美元,年複合成長率為 6.8%。

行動遊戲和跨平台遊戲的日益普及推動了這一成長,開發者致力於在多種裝置上提供無縫體驗。此外,在電影、建築、汽車和工業模擬等非遊戲垂直領域,身臨其境型視覺化數位雙胞胎應用也日益普及。雲端遊戲引擎因其支援即時開發、協作工作流程以及可擴展的分散式團隊資產管理而備受青睞。隨著遠距辦公的興起和「線上即服務」(LaaS)遊戲模式的擴展,這一轉變正在加速。更短的開發週期、更低的基礎設施需求以及基於訂閱的持續收入模式正在推動市場進一步擴張。開發者正擴大利用這些引擎,在娛樂、汽車、航空航太和國防等領域提供高品質的圖形、即時渲染和模擬應用。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 15億美元 |

| 預測金額 | 29億美元 |

| 複合年成長率 | 6.8% |

預計到2025年,3D遊戲引擎市佔率將達到78.9%。這一細分市場受益於PC、主機、行動裝置和擴增實境平台對照片級真實感畫面、即時實體效果和身臨其境型遊戲體驗日益成長的需求。除了遊戲領域,3D引擎也廣泛應用於AAA級遊戲、虛擬製作、汽車視覺化數位雙胞胎計劃。其擴充性、跨行業適用性和提供逼真體驗的能力正在推動其收入的顯著成長。

預計到2025年,訂閱制遊戲市場規模將達到5.285億美元。 SaaS模式提供可預測的經常性收入、整合開發工具、雲端服務和持續更新。這些優勢降低了開發者的前期成本,同時支援協作式、跨平台和可擴展的遊戲開發工作流程。

預計到2025年,北美遊戲引擎市場將佔據31.5%的市場。該地區的成長主要得益於大型引擎開發人員、實力雄厚的AAA級遊戲工作室以及雲端和身臨其境型技術的早期採用者。汽車、航太和電影製作等領域的應用不斷擴展,也推動了對高品質3D引擎的需求,從而創造了多元化的商機。電子競技、基於模擬的訓練和虛擬製作的興起進一步拓展了遊戲引擎的應用範圍,而人工智慧工具則提高了效率和創造性。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段的附加價值

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 促進要素

- 對身臨其境型遊戲體驗和AAA級遊戲開發的需求日益成長

- 擴展擴增實境(AR)/虛擬實境 (VR)/混合實境 (MR) 和元宇宙應用

- 雲端遊戲引擎的日益普及

- 在非遊戲產業中不斷擴大應用

- 行動遊戲與跨平台遊戲的發展

- 產業潛在風險與挑戰

- 免費增值/開放原始碼引擎的激烈競爭和價格壓力

- 引擎複雜度高,學習曲線陡峭

- 市場機遇

- 採用人工智慧引擎功能和程式化內容生成

- 與雲端遊戲、SaaS 和協作開發平台整合

- 促進要素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 新興經營模式

- 合規要求

- 專利和智慧財產權分析

- 地緣政治和貿易趨勢

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 市場集中度分析

- 按地區

- 主要企業的競爭標竿分析

- 財務績效比較

- 收入

- 利潤率

- 研究與開發

- 產品系列比較

- 產品線的廣度

- 科技

- 創新

- 地理分佈比較

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導企業

- 受讓人

- 追蹤者

- 小眾玩家

- 戰略展望矩陣

- 財務績效比較

- 重大進展

- 併購

- 夥伴關係與合作

- 技術進步

- 擴張與投資策略

- 數位轉型計劃

- 新興/Start-Ups競賽的趨勢

第5章 依引擎類型分類的市場估算與預測,2022-2035年

- 2D遊戲引擎

- 3D遊戲引擎

- 混合

第6章 按車型分類的市場估計與預測,2022-2035年

- 本地部署

- 基於雲端的

- 混合

7. 按授權模式分類的市場估算與預測,2022-2035 年

- 免費增值

- 訂閱類型

- 永久許可

- 收益分成/版稅制

第8章 2022-2035年各平台市場估算與預測

- PC

- 主機

- 移動的

- Web

- AR/VR/MR

第9章 按應用領域分類的市場估算與預測,2022-2035年

- 遊戲

- 主機

- PC

- 移動的

- 線上

- 電影與動畫/虛擬製作

- 建築、工程和施工 (AEC)

- 汽車/運輸設備

- 航太/國防

- 其他

第10章 2022-2035年各地區市場估計與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章 公司簡介

- 主要企業

- Unity Technologies

- Epic Games, Inc.(Unreal Engine)

- YoYo Games Ltd.

- 按地區分類的主要企業

- 北美洲

- MonoGame

- Open 3D Engine

- GDevelop

- 亞太地區

- Cocos

- RPG Maker(ASCII Corporation)

- Solar2D LLC

- 歐洲

- YoYo Games Ltd.

- Construct(Scirra Ltd.)

- Crytek GmbH

- Godot Foundation

- Stencyl LLC

- 北美洲

- 小眾玩家/顛覆者

- Ren'Py

- Torque3 D(GarageGames)

The Global Game Engine Market was valued at USD 1.5 billion in 2025 and is estimated to grow at a CAGR of 6.8% to reach USD 2.9 billion by 2035.

Growth is driven by the rising popularity of mobile and cross-platform gaming, as developers focus on delivering seamless experiences across multiple devices. Adoption is also expanding in non-gaming sectors, including film, architecture, automotive, and industrial simulations, where immersive visualization and digital twin applications are becoming essential. Cloud-based game engines are gaining traction as they support real-time development, collaborative workflows, and scalable asset management for distributed teams. This shift has accelerated since the remote work trend and live service gaming model became widespread. Faster development cycles, reduced infrastructure requirements, and recurring subscription-based revenue are further propelling market expansion. Developers increasingly use engines for high-quality graphics, real-time rendering, and simulation applications across entertainment, automotive, aerospace, and defense sectors.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.5 Billion |

| Forecast Value | $2.9 Billion |

| CAGR | 6.8% |

The 3D game engines segment held 78.9% share in 2025. This segment benefits from growing demand for photorealistic graphics, real-time physics, and immersive gameplay on PC, console, mobile, and extended reality platforms. Beyond gaming, 3D engines are widely used for AAA titles, virtual production, automotive visualization, and digital twin projects. Their scalability, cross-industry applications, and ability to deliver lifelike experiences have significantly boosted revenue.

The subscription-based segment reached USD 528.5 million in 2025. SaaS-based delivery models offer predictable recurring revenue, integrated development tools, cloud services, and continuous updates. These benefits reduce upfront costs for developers while supporting collaborative, cross-platform, and scalable game development workflows.

North America Game Engine Market held a 31.5% share in 2025. The region's growth is supported by major engine developers, strong AAA gaming studios, and early adoption of cloud-based and immersive technologies. Expanding applications in automotive, aerospace, and film production are also driving demand for high-quality 3D engines, creating diverse revenue opportunities. The rise of esports, simulation-based training, and virtual production is further broadening the scope of game engine use, while AI-powered tools enhance efficiency and creative capabilities.

Key players in the Global Game Engine Market include Cocos, Construct (Scirra Ltd.), Crytek GmbH, Epic Games, Inc. (Unreal Engine), GDevelop, Godot Foundation, Marmalade SDK, MonoGame, Open 3D Engine, RPG Maker (ASCII Corporation), Solar2D LLC, Stencyl LLC, The Game Creators Ltd., Torque3D (GarageGames), Unity Technologies, Ren'Py, and YoYo Games Ltd. Companies in the game engine market are adopting several strategies to strengthen their market position. They are investing heavily in R&D to improve rendering quality, cross-platform capabilities, and support for immersive technologies. Strategic partnerships with cloud providers, software vendors, and enterprise clients enable wider adoption and integration. Mergers and acquisitions are used to expand technology portfolios and gain access to new markets. Firms are also emphasizing subscription-based models for predictable revenue streams and global reach. Additionally, companies are developing AI-powered tools, real-time collaboration features, and scalable cloud-based solutions to enhance usability, attract developers, and maintain a competitive advantage.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Engine type trends

- 2.2.2 Deployment model trends

- 2.2.3 Licensing model trends

- 2.2.4 Platform trends

- 2.2.5 Application trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for immersive gaming experiences and AAA game development

- 3.2.1.2 Expansion of AR/VR/MR and metaverse applications

- 3.2.1.3 Increasing adoption of cloud-based game engines

- 3.2.1.4 Rising use in non-gaming industries

- 3.2.1.5 Growth of mobile and cross-platform gaming

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Intense competition and price pressure from freemium/open-source engines

- 3.2.2.2 Complexity and high learning curve of advanced engines

- 3.2.3 Market opportunities

- 3.2.3.1 Adoption of AI-powered engine features and procedural content generation

- 3.2.3.2 Integration with cloud gaming, SaaS, and collaborative development platforms

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging Business Models

- 3.9 Compliance Requirements

- 3.10 Patent and IP analysis

- 3.11 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Engine Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 2D game engines

- 5.3 3D game engines

- 5.4 Hybrid

Chapter 6 Market Estimates and Forecast, By Deployment Model, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 On-premise

- 6.3 Cloud-based

- 6.4 Hybrid

Chapter 7 Market Estimates and Forecast, By Licensing Model, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Freemium

- 7.3 Subscription-based

- 7.4 Perpetual license

- 7.5 Revenue-sharing / royalty-based

Chapter 8 Market Estimates and Forecast, By Platform, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 PC

- 8.3 Console

- 8.4 Mobile

- 8.5 Web

- 8.6 AR/VR/MR

Chapter 9 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Gaming

- 9.2.1 Console

- 9.2.2 PC

- 9.2.3 Mobile

- 9.2.4 Online

- 9.3 Film & animation / virtual production

- 9.4 Architecture, engineering & construction (AEC)

- 9.5 Automotive & transportation

- 9.6 Aerospace & defense

- 9.7 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 Unity Technologies

- 11.1.2 Epic Games, Inc. (Unreal Engine)

- 11.1.3 YoYo Games Ltd.

- 11.2 Regional key players

- 11.2.1 North America

- 11.2.1.1 MonoGame

- 11.2.1.2 Open 3D Engine

- 11.2.1.3 GDevelop

- 11.2.2 Asia Pacific

- 11.2.2.1 Cocos

- 11.2.2.2 RPG Maker (ASCII Corporation)

- 11.2.2.3 Solar2D LLC

- 11.2.3 Europe

- 11.2.3.1 YoYo Games Ltd.

- 11.2.3.2 Construct (Scirra Ltd.)

- 11.2.3.3 Crytek GmbH

- 11.2.3.4 Godot Foundation

- 11.2.3.5 Stencyl LLC

- 11.2.1 North America

- 11.3 Niche Players/Disruptors

- 11.3.1 Ren’Py

- 11.3.2. Torque3 D (GarageGames)

遊戲引擎市場:按平台、技術類型、授權模式、部署類型和應用程式分類-2026-2032年全球預測行動遊戲引擎市場:2026-2032年全球預測(按平台、授權模式、遊戲類型、組織規模、開發人員類型、獲利模式和部署類型分類)

遊戲引擎市場:按平台、技術類型、授權模式、部署類型和應用程式分類-2026-2032年全球預測行動遊戲引擎市場:2026-2032年全球預測(按平台、授權模式、遊戲類型、組織規模、開發人員類型、獲利模式和部署類型分類) 遊戲引擎市場-全球產業規模、佔有率、趨勢、機會及預測(按組件、類型、平台、類型、地區和競爭格局分類,2021-2031年預測)

遊戲引擎市場-全球產業規模、佔有率、趨勢、機會及預測(按組件、類型、平台、類型、地區和競爭格局分類,2021-2031年預測) 遊戲引擎市場規模、佔有率及成長分析(按組件、類型、平台、類型及地區分類)-2026-2033年產業預測

遊戲引擎市場規模、佔有率及成長分析(按組件、類型、平台、類型及地區分類)-2026-2033年產業預測 遊戲引擎市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測(2024-2032)

遊戲引擎市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測(2024-2032) 遊戲引擎和開發軟體-全球市場佔有率和排名、總收入和需求預測(2025-2031年)

遊戲引擎和開發軟體-全球市場佔有率和排名、總收入和需求預測(2025-2031年) 全球遊戲引擎市場

全球遊戲引擎市場 2024-2028年全球遊戲引擎市場

2024-2028年全球遊戲引擎市場