|

市場調查報告書

商品編碼

1936588

血栓症藥物市場機會、成長要素、產業趨勢分析及2026年至2035年預測Thrombosis Drugs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

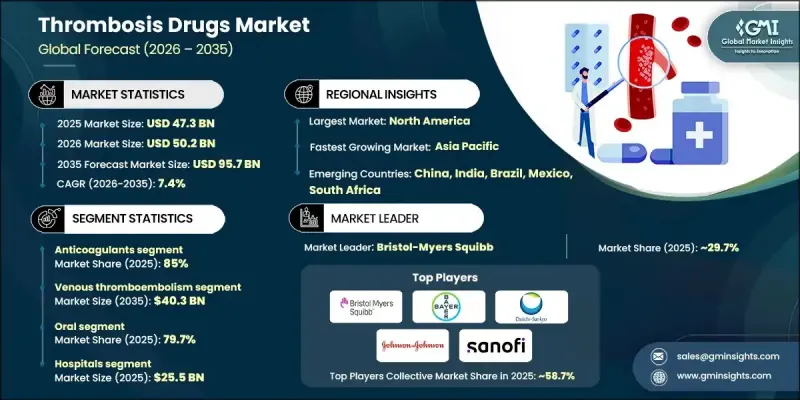

全球血栓症藥物市場預計到 2025 年將達到 473 億美元,到 2035 年將達到 957 億美元,年複合成長率為 7.4%。

心血管疾病(如心肌梗塞、肺動脈栓塞和缺血性中風)發病率的上升推動了這一成長。在這些疾病中,迅速恢復血流至關重要,因此血栓症治療在急救中至關重要。血栓症藥物旨在預防和治療血管內血栓形成,包括抑制凝血因子的抗凝血劑、抑制血小板凝集的抗血小板藥物以及溶解現有血栓的溶栓劑。直介面服抗凝血劑(DOAC)的日益普及,因其使用方便且安全性更高,進一步推動了市場成長。外科手術量的增加、癌症相關血栓症發生率的上升、抗凝血治療的延長以及臨床上對血栓併發症日益成長的關注,都在推動市場需求。新型口服抗凝血劑(NOAC)因其在預防缺血性中風(尤其是在非瓣膜性心房顫動患者中)方面的確切療效,已成為首選治療方法。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 473億美元 |

| 預測金額 | 957億美元 |

| 複合年成長率 | 7.4% |

抗凝血劑市佔率佔85%,預計到2025年將創造402億美元的收入。此細分市場包括直介面服抗凝血劑、肝素、維生素K拮抗劑和注射直接凝血酶抑制劑。其主導地位歸功於其在預防和治療領域的廣泛應用,包括心房顫動、中風預防、靜脈血栓栓塞症的治療以及術後血栓預防。直介面服抗凝血劑因其完善的臨床指南、醫生熟悉度高、療效可預測、給藥方便且監測需求低而備受青睞,其日益成長的使用進一步鞏固了其在該細分市場的領先地位。

預計到2035年,靜脈血栓栓塞症症市場規模將達403億美元。此領域(包括深層靜脈栓塞症和肺動脈栓塞)的成長主要受人口老化、肥胖和癌症發生率上升、住院時間延長以及外科手術數量增加等因素所驅動。醫院和門診機構對血栓預防指引的認知不斷提高,並推動了全球診斷率和治療率的提升。

預計到2025年,北美血栓症藥物市佔率將達到59.5%。該地區受益於完善的醫療基礎設施,包括先進的醫院、專業的心臟中心以及口服和注射抗凝血劑的便捷獲取途徑。心血管疾病、心房顫動和靜脈血栓栓塞症的高發生率,尤其是在老年人,推動了血栓症藥物的強勁需求。新型口服抗凝血劑(NOAC)的早期應用、完善的醫保報銷體係以及醫護人員對抗血栓通訊協定的廣泛了解,進一步鞏固了該地區的主導地位。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 產業影響因素

- 促進要素

- 心血管和腦血管疾病發生率增加

- 擴大新型口服抗凝血劑(NOACs)的引入

- 手術數量增加

- 溶栓藥物製劑的進展

- 產業潛在風險與挑戰

- 副作用和不良反應的風險

- 嚴格的監管核准

- 市場機遇

- 擴大預防性心血管護理的覆蓋範圍

- 下一代上游凝血抑制劑的研發

- 促進要素

- 成長潛力分析

- 監管環境

- 科技趨勢

- 當前技術趨勢

- 新興技術

- 救贖方案

- 管道分析

- 定價分析

- 未來市場趨勢

- 差距分析

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 世界

- 北美洲

- 歐洲

- 亞太地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

5. 按藥物類別分類的市場估計和預測,2022-2035 年

- 抗凝血劑

- 直介面服抗凝血劑

- 肝素

- 維生素K拮抗劑

- 注射用直接凝血酶原抑制劑(DTIs)

- 抗血小板藥物

- P2Y12受體抑制劑

- 阿斯匹靈

- GlicoIIb/IIIa抑制劑

- 溶栓藥物

第6章 依疾病類型分類的市場估計與預測,2022-2035年

- 靜脈血栓栓塞症

- 深層靜脈栓塞症

- 肺動脈栓塞

- 動脈血栓症

- 心房顫動

- 腦血管疾病

- 其他疾病類型

7. 依行政途徑分類的市場估計與預測,2022-2035 年

- 口服

- 注射

- 外用

第8章 依最終用途分類的市場估算與預測,2022-2035年

- 醫院

- 門診手術中心

- 其他用途

第9章 2022-2035年各地區市場估算與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- Aspen Pharmacare

- AstraZeneca

- Bayer

- Boehringer Ingelheim

- Bristol-Myers Squibb

- Chiesi Farmaceutici

- Daiichi Sankyo

- Dr. Reddy's Laboratories

- Johnson &Johnson

- Karma Pharmatech

- Lupin

- Microbix Biosystems

- Novartis

- Pfizer

- Sanofi

- Teva Pharmaceuticals

The Global Thrombosis Drugs Market was valued at USD 47.3 billion in 2025 and is estimated to grow at a CAGR of 7.4% to reach USD 95.7 billion by 2035.

The growth is driven by the rising prevalence of cardiovascular disorders, including myocardial infarction, pulmonary embolism, and ischemic stroke, which necessitate rapid restoration of blood flow, making thrombosis treatment critical in emergency care. Thrombosis drugs are designed to prevent and treat clot formation in blood vessels, including anticoagulants that inhibit clotting factors, antiplatelet agents that block platelet aggregation, and thrombolytics that dissolve existing clots. The growing adoption of direct oral anticoagulants, which offer convenience and improved safety profiles, has further accelerated market expansion. Increased surgical procedures, rising incidences of cancer-associated thrombosis, and prolonged anticoagulation therapy, alongside growing clinical focus on thrombotic complications, collectively fuel demand. Novel oral anticoagulants (NOACs) emerge as a preferred therapy, particularly for non-valvular atrial fibrillation, due to their proven efficacy in preventing ischemic stroke.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $47.3 Billion |

| Forecast Value | $95.7 Billion |

| CAGR | 7.4% |

The anticoagulants segment held an 85% share, generating USD 40.2 billion in 2025. This segment includes direct oral anticoagulants, heparin, vitamin K antagonists, and injectable direct thrombin inhibitors. Its dominance is attributed to widespread use in both prophylactic and therapeutic settings, including atrial fibrillation, stroke prevention, venous thromboembolism management, and post-surgical thromboprophylaxis. Strong clinical guidelines, physician familiarity, and growing use of direct oral anticoagulants valued for predictable efficacy, convenient dosing, and minimal monitoring have further solidified this segment's leadership.

The venous thromboembolism segment is expected to reach USD 40.3 billion by 2035. It encompasses deep vein thrombosis and pulmonary embolism, with growth driven by aging populations, increasing rates of obesity and cancer, longer hospital stays, and higher volumes of surgical procedures. Greater awareness and implementation of thromboprophylaxis guidelines in both hospital and outpatient settings are contributing to rising diagnosis and treatment rates globally.

North America Thrombosis Drugs Market held a 59.5% share in 2025. The region benefits from a well-established healthcare infrastructure, including advanced hospitals, specialized cardiac centers, and access to both oral and parenteral anticoagulants. High prevalence of cardiovascular diseases, atrial fibrillation, and venous thromboembolism, especially in older populations, drives strong demand for thrombosis therapies. Early adoption of NOACs, supportive reimbursement frameworks, and widespread knowledge of thromboprophylaxis protocols among healthcare professionals further reinforce the region's leadership.

Leading players in the Global Thrombosis Drugs Market include AstraZeneca, Sanofi, Dr. Reddy's Laboratories, Johnson & Johnson, Pfizer, Novartis, Bayer, Boehringer Ingelheim, Microbix Biosystems, Karma Pharmatech, Daiichi Sankyo, Bristol-Myers Squibb, Aspen Pharmacare, Chiesi Farmaceutici, Teva Pharmaceuticals, and Lupin. Key strategies adopted by companies in the Thrombosis Drugs Market to strengthen their market position include heavy investments in research and development to enhance drug efficacy, safety, and patient adherence. Firms are entering strategic collaborations and licensing agreements with hospitals, research institutions, and biotech companies to expand their product portfolios and clinical reach. Expanding into emerging markets and improving supply chain distribution networks ensures wider therapy accessibility.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.2 Source consistency protocol

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.2 Sources, by region

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Drug class trends

- 2.2.3 Disease type trends

- 2.2.4 Route of administration trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising incidence of cardiovascular and cerebrovascular events

- 3.2.1.2 Growing adoption of novel oral anticoagulants (NOACs)

- 3.2.1.3 Rising number of surgical procedures

- 3.2.1.4 Advancements in thrombolytic drug formulations

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Risk of adverse reactions and side effects

- 3.2.2.2 Stringent regulatory approval

- 3.2.3 Market opportunities

- 3.2.3.1 Growing shift towards preventive cardiovascular care

- 3.2.3.2 Developing next-generation upstream coagulation inhibitors

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Reimbursement scenario

- 3.7 Pipeline analysis

- 3.8 Pricing analysis

- 3.9 Future market trends

- 3.10 Gap analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Drug Class, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Anticoagulants

- 5.2.1 Direct oral anticoagulants

- 5.2.2 Heparin

- 5.2.3 Vitamin K antagonists

- 5.2.4 Injectable DTIs

- 5.3 Antiplatelet drugs

- 5.3.1 P2Y12 platelet inhibitor

- 5.3.2 Aspirin

- 5.3.3 Glycoprotein IIb/IIIa inhibitors

- 5.4 Thrombolytic drugs

Chapter 6 Market Estimates and Forecast, By Disease Type, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Venous thromboembolism

- 6.2.1 Deep vein thrombosis

- 6.2.2 Pulmonary embolism

- 6.3 Arterial thrombosis

- 6.4 Atrial fibrillation

- 6.5 Cerebrovascular disorders

- 6.6 Other disease types

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Oral

- 7.3 Parenteral

- 7.4 Topical

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Ambulatory surgical centers

- 8.4 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Aspen Pharmacare

- 10.2 AstraZeneca

- 10.3 Bayer

- 10.4 Boehringer Ingelheim

- 10.5 Bristol-Myers Squibb

- 10.6 Chiesi Farmaceutici

- 10.7 Daiichi Sankyo

- 10.8 Dr. Reddy’s Laboratories

- 10.9 Johnson & Johnson

- 10.10 Karma Pharmatech

- 10.11 Lupin

- 10.12 Microbix Biosystems

- 10.13 Novartis

- 10.14 Pfizer

- 10.15 Sanofi

- 10.16 Teva Pharmaceuticals

血栓症治療市場規模、佔有率和成長分析:按藥物類別、作用機制、應用、臨床適應症、分銷管道和地區分類-2026-2033年產業預測

血栓症治療市場規模、佔有率和成長分析:按藥物類別、作用機制、應用、臨床適應症、分銷管道和地區分類-2026-2033年產業預測 血栓症治療市場:2026年至2032年全球市場預測(依治療方法、給藥途徑、藥物類別、適應症和最終用戶分類)來替普拉市場:2026-2032年全球市場預測(依患者類型、治療領域、通路和最終用戶分類)溶栓藥物市場:2026-2032年全球市場預測(依藥物類別、適應症、給藥途徑、病患群體及最終使用者分類)

血栓症治療市場:2026年至2032年全球市場預測(依治療方法、給藥途徑、藥物類別、適應症和最終用戶分類)來替普拉市場:2026-2032年全球市場預測(依患者類型、治療領域、通路和最終用戶分類)溶栓藥物市場:2026-2032年全球市場預測(依藥物類別、適應症、給藥途徑、病患群體及最終使用者分類) 2026-2034年全球血栓症治療市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球血栓症治療市場規模、佔有率、趨勢和成長分析報告 全球血栓症藥物市場:市場規模、佔有率和趨勢分析(按疾病類型、藥物類別、分銷管道和地區分類),細分市場預測(2025-2033 年)

全球血栓症藥物市場:市場規模、佔有率和趨勢分析(按疾病類型、藥物類別、分銷管道和地區分類),細分市場預測(2025-2033 年) 溶栓藥物市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

溶栓藥物市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測