|

市場調查報告書

商品編碼

1936573

運輸管理系統市場機會、成長要素、產業趨勢分析及預測(2026-2035年)Traffic Management System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

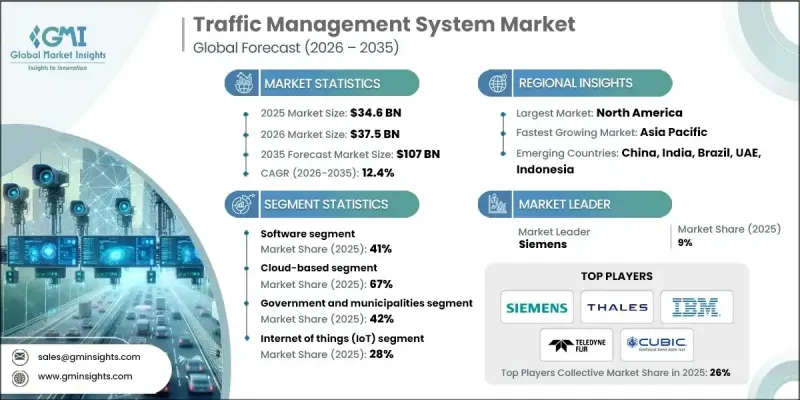

全球交通管理系統市場預計到 2025 年將達到 346 億美元,到 2035 年將達到 1,070 億美元,年複合成長率為 12.4%。

現代都市區高度依賴交通管理系統,透過整合硬體、軟體和服務來改善交通出行、緩解擁塞並提昇道路安全。快速的都市化、基礎設施現代化以及日益成長的交通堵塞經濟成本(根據國際能源總署 (IEA) 估計,已開發經濟體的交通堵塞成本佔年度 GDP 的 2% 至 4%)是推動這一市場發展的因素。交通管理系統正擴大利用人工智慧 (AI)、物聯網 (IoT)、雲端運算和巨量資料,以實現即時監控、預測分析和智慧交通解決方案。基於雲端的部署能夠實現集中管理、可擴展的城市級部署,並與車聯網 (V2X) 等聯網汽車技術整合。分階段部署通常從訊號最佳化和即時監控開始,逐步發展到預測分析、自動駕駛車輛協調和多模態交通管理。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 346億美元 |

| 預測金額 | 1070億美元 |

| 複合年成長率 | 12.4% |

到 2025 年,雲端部署模式將佔 67% 的市場佔有率,到 2035 年將以 12.7% 的複合年成長率成長。雲端解決方案提供彈性可擴展性、即時處理大量感測器資料流以及無縫的第三方整合,同時將對高成本的本地基礎設施的依賴性降低 40-60%。

預計到2025年,軟體解決方案領域將佔據41%的市場佔有率,並在2035年之前以11.5%的複合年成長率成長,這主要得益於人工智慧驅動的分析、自適應交通號誌控制和自動事件偵測技術。這些平台利用機器學習演算法進行交通預測,利用電腦視覺進行即時監控,並利用最佳化引擎改善城市交通流量。

預計從 2026 年到 2035 年,美國交通管理系統市場將以 11.9% 的複合年成長率成長。聯邦舉措,例如撥款 1,100 億美元用於交通基礎設施現代化的《基礎設施投資和就業法案》,以及美國運輸部智慧型運輸系統聯合計畫辦公室的指導,正在加速美國各地交通管理系統的普及。

目錄

第1章調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率分析

- 成本結構

- 每個階段的附加價值

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 促進要素

- 全球都市化進程

- 政府投資和監管支持

- 交通管理系統的技術進步

- 對高效率交通運輸的需求日益成長

- 先進分析技術和巨量資料的廣泛應用

- 產業潛在風險與挑戰

- 高昂的初始投資和營運成本

- 隱私和資料安全問題

- 市場機遇

- 智慧城市計劃推動TMS(交通管理系統)的普及

- 都市區汽車數量的增加正在推動需求成長。

- 與聯網汽車自動駕駛車輛的整合

- 緊急服務和公共支持

- 更合理的交通流可以減少排放和燃料消耗。

- 成長潛力分析

- 監管環境

- 北美洲

- 美國聯邦智慧交通系統標準與聯網汽車指南

- 加拿大—國家智慧交通系統策略與省級交通法規

- 歐洲

- 德國——道路交通法和歐盟智慧交通系統指令

- 英國—交通管理法與城市交通框架

- 法國——國家智慧交通系統最佳化策略

- 義大利-智慧交通系統行動計畫和道路安全義務

- 亞太地區

- 中國—國家智慧交通系統標準與智慧城市交通指南

- 印度—機動車法和智慧城市計劃

- 日本——交通政策與道路交通法

- 澳洲 - ADR 和 ITS 交通管制指南

- LATAM

- 墨西哥 - 交通監控和智慧交通系統解決方案的 NOM 標準

- 阿根廷 - 國家交通法與智慧型運輸系統 (ITS) 框架

- 中東和非洲

- 南非共和國 - 道路交通法與智慧運輸政策

- 沙烏地阿拉伯—交通法規與2030願景智慧交通系統舉措

- 北美洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利分析

- 用例和成功案例

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

- 未來前景與機遇

- 經營模式和定價框架

- 前期硬體投資成本(CAPEX)與持續軟體營運成本(OPEX)

- 基於授權和基於訂閱的軟體定價

- 託管服務和經常性收入模式

- 基於績效的合約(KPI、擁塞緩解服務水準協議)

- PPP和基於績效的支付結構

- 成本經濟學:初始成本與持續費用

- 互通性和標準合規性

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 企業擴張計畫和資金籌措

第5章 按技術分類的市場估算與預測,2022-2035年

- 人工智慧和機器學習

- 物聯網 (IoT)

- 基於雲端的

- 巨量資料分析

- 其他

第6章 按組件分類的市場估算與預測,2022-2035年

- 硬體

- 交通號誌及控制設備

- 感應器

- 攝影機和監視器系統

- 可變訊息顯示螢幕

- 軟體

- 交通分析

- 智慧型訊號系統

- 路線引導

- 交通監控

- 服務

- 諮詢

- 部署與整合

- 支援與維護

第7章 按應用領域分類的市場估算與預測,2022-2035年

- 城市交通管理

- 公路交通管理

- 公共運輸管理

- 停車場管理

- 事件管理

- 綜合走廊管理(ICM)

- 其他

第8章 依實施類型分類的市場估算與預測,2022-2035年

- 本地部署

- 基於雲端的

9. 依最終用途分類的市場估計與預測,2022-2035 年

- 政府和地方政府

- 運輸

- 私人組織

- 其他

第10章 2022-2035年各地區市場估計與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 比荷盧經濟聯盟

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 新加坡

- 泰國

- 印尼

- 越南

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥倫比亞

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章 公司簡介

- 世界公司

- Cisco

- Huawei Technologies

- IBM

- Intel

- Siemens

- Swarco

- Teledyne FLIR

- Thales

- TomTom International

- 區域玩家

- Cubic

- Iteris

- Jenoptik

- Kapsch

- Metro Infrasys

- Omnitec Systems

- Q-Free

- TransCore

- 新興科技創新者

- Acyclica

- Cohda Wireless

- Miovision

- Radwin

- Sensys Networks

- Sick

- Sumitomo

- Vayyar Imaging

The Global Traffic Management System Market was valued at USD 34.6 billion in 2025 and is estimated to grow at a CAGR of 12.4% to reach USD 107 billion by 2035.

Modern urban centers rely heavily on traffic management systems to improve mobility, reduce congestion, and enhance road safety by integrating hardware, software, and services. The market is driven by rapid urbanization, infrastructure modernization, and rising economic costs of traffic congestion, which the International Energy Agency estimates to be 2-4% of GDP in developed economies annually. Traffic management systems increasingly leverage AI, IoT, cloud computing, and big data to enable real-time monitoring, predictive analytics, and intelligent transport solutions. Cloud-based deployments allow centralized control, scalable citywide implementation, and integration with connected vehicle technologies such as vehicle-to-everything (V2X) communication. Phased implementations typically begin with signal optimization and real-time monitoring and evolve to predictive analytics, autonomous vehicle coordination, and multi-modal transport management.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $34.6 Billion |

| Forecast Value | $107 Billion |

| CAGR | 12.4% |

The cloud deployment model accounted for 67% share in 2025 and is growing at a CAGR of 12.7% through 2035. Cloud solutions provide elastic scalability, real-time processing of massive sensor data streams, and seamless third-party integration while reducing reliance on costly on-premises infrastructure by 40-60%.

The software solutions segment held 41% share in 2025, with growth at a CAGR of 11.5% through 2035, driven by AI-powered analytics, adaptive signal control, and automated incident detection technologies. These platforms use machine learning algorithms for traffic prediction, computer vision for real-time monitoring, and optimization engines to improve urban traffic flow.

U.S. Traffic Management System Market will grow at a CAGR of 11.9% from 2026 to 2035. Federal initiatives such as the Infrastructure Investment and Jobs Act, which allocates USD 110 billion for modernizing transportation infrastructure, and guidance from the U.S. Department of Transportation's Intelligent Transportation Systems Joint Program Office, are accelerating TMS adoption across the country.

Key players in the Global Traffic Management System Market include Siemens, Iteris, Teledyne FLIR, Intel, Thales, Cubic, IBM, Jenoptik, Swarco, and Transcore. Companies in the traffic management system market strengthen their position by investing in AI-driven traffic analytics, expanding cloud-based service offerings, and developing modular, scalable solutions for urban deployments. Strategic collaborations with smart city projects, integration with connected vehicle and V2X technologies, and continuous R&D into predictive traffic optimization and real-time monitoring tools help firms expand their market footprint. Additionally, partnerships with government agencies and transportation authorities enable these companies to secure long-term contracts and maintain competitive advantage, while global expansion strategies and regional deployment customization support growth across emerging and mature markets.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 Research trail and confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Best estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Technology

- 2.2.3 Components

- 2.2.4 Application

- 2.2.5 Deployment Mode

- 2.2.6 End Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1.1 Growth drivers

- 3.2.1.2 Increasing global urbanization

- 3.2.1.3 Government investments and regulatory support

- 3.2.1.4 Technological advancements in traffic management systems

- 3.2.1.5 Increased demand for efficient transportation

- 3.2.1.6 Rising adoption of advanced analytics and big data

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial investment and operational costs

- 3.2.2.2 Privacy and data security concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Smart city projects drive TMS adoption

- 3.2.3.2 Rising urban vehicle populations increase demand

- 3.2.3.3 Integration with connected and autonomous vehicles

- 3.2.3.4 Support for emergency services and public safety

- 3.2.3.5 Reduce emissions and fuel consumption through smart traffic flow

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 US- Federal ITS standards and Connected Vehicle Guidelines

- 3.4.1.2 Canada - National ITS strategy and provincial traffic regulations

- 3.4.2 Europe

- 3.4.2.1 Germany- Road Traffic Act and EU ITS directives

- 3.4.2.2 UK- Traffic Management Act and urban mobility frameworks

- 3.4.2.3 France- National ITS strategy for traffic optimization

- 3.4.2.4 Italy- ITS action plans and road safety mandates

- 3.4.3 Asia Pacific

- 3.4.3.1 China- National ITS standards and smart city traffic guidelines

- 3.4.3.2 India- Motor vehicles act and smart city mission initiatives

- 3.4.3.3 Japan- i-Transportation policies and road traffic act

- 3.4.3.4 Australia- ADR and ITS guidelines for traffic control

- 3.4.4 LATAM

- 3.4.4.1 Mexico- NOM standards for traffic monitoring and ITS solutions

- 3.4.4.2 Argentina- National Traffic Law and ITS frameworks

- 3.4.5 MEA

- 3.4.5.1 South Africa- Road Traffic Act and smart mobility initiatives

- 3.4.5.2 Saudi Arabia- Traffic regulations and Vision 2030 ITS initiatives

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis

- 3.9 Use cases & success stories

- 3.10 Sustainability and environmental aspects

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly Initiatives

- 3.10.5 Carbon footprint considerations

- 3.11 Future outlook and opportunities

- 3.12 Business Model & Pricing Framework

- 3.12.1 One-time hardware CAPEX vs recurring software OPEX

- 3.12.2 License-based vs subscription-based software pricing

- 3.12.3 Managed services & annuity revenue models

- 3.12.4 Performance-based contracts (KPIs, congestion reduction SLAs)

- 3.12.5 PPP and outcome-based payment structures

- 3.13 Cost Economics: Upfront vs Recurring Spend

- 3.14 Interoperability & Standards Compliance

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Technology, 2022 - 2035 ($Bn)

- 5.1 Key trends

- 5.2 AI & ML

- 5.3 Internet of things (IoT)

- 5.4 Cloud-based

- 5.5 Big data analytics

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Component, 2022 - 2035 ($Bn)

- 6.1 Key trends

- 6.2 Hardware

- 6.2.1 Traffic signals and controllers

- 6.2.2 Sensors

- 6.2.3 Camera and surveillance systems

- 6.2.4 Variable message signs

- 6.3 Software

- 6.3.1 Traffic analytics

- 6.3.2 Smart signaling

- 6.3.3 Route guidance

- 6.3.4 Traffic monitoring

- 6.4 Services

- 6.4.1 Consulting

- 6.4.2 Deployment and integration

- 6.4.3 Support and maintenance

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn)

- 7.1 Key trends

- 7.2 Urban traffic management

- 7.3 Highway traffic management

- 7.4 Public transportation management

- 7.5 Parking management

- 7.6 Incident management

- 7.7 Integrated corridor management (ICM)

- 7.8 Others

Chapter 8 Market Estimates & Forecast, By Deployment Mode, 2022 - 2035 ($Bn)

- 8.1 Key trends

- 8.2 On-premises

- 8.3 Cloud-based

Chapter 9 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Bn)

- 9.1 Key trends

- 9.2 Government and municipalities

- 9.3 Transportation agencies

- 9.4 Private organizations

- 9.5 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.3.8 Benelux

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Singapore

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Colombia

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Cisco

- 11.1.2 Huawei Technologies

- 11.1.3 IBM

- 11.1.4 Intel

- 11.1.5 Siemens

- 11.1.6 Swarco

- 11.1.7 Teledyne FLIR

- 11.1.8 Thales

- 11.1.9 TomTom International

- 11.2 Regional Players

- 11.2.1 Cubic

- 11.2.2 Iteris

- 11.2.3 Jenoptik

- 11.2.4 Kapsch

- 11.2.5 Metro Infrasys

- 11.2.6 Omnitec Systems

- 11.2.7 Q-Free

- 11.2.8 TransCore

- 11.3 Emerging Technology Innovators

- 11.3.1 Acyclica

- 11.3.2 Cohda Wireless

- 11.3.3 Miovision

- 11.3.4 Radwin

- 11.3.5 Sensys Networks

- 11.3.6 Sick

- 11.3.7 Sumitomo

- 11.3.8 Vayyar Imaging

通訊流量管理市場預測至2034年-按組件、部署模式、網路類型、技術、應用、最終用戶和地區分類的全球分析

通訊流量管理市場預測至2034年-按組件、部署模式、網路類型、技術、應用、最終用戶和地區分類的全球分析 交通管理市場:按組件、技術、應用、最終用戶和部署模式分類-2026-2032年全球市場預測智慧交通管理系統市場預測至2034年-按解決方案、技術、最終用戶和區域分類的全球分析智慧交通管理與物聯網賦能道路市場預測:至2034年-按組件、部署模式、技術、應用和區域分類的全球分析智慧交通號誌市場按組件、連接方式、應用、安裝和最終用戶分類,全球預測(2026-2032年)

交通管理市場:按組件、技術、應用、最終用戶和部署模式分類-2026-2032年全球市場預測智慧交通管理系統市場預測至2034年-按解決方案、技術、最終用戶和區域分類的全球分析智慧交通管理與物聯網賦能道路市場預測:至2034年-按組件、部署模式、技術、應用和區域分類的全球分析智慧交通號誌市場按組件、連接方式、應用、安裝和最終用戶分類,全球預測(2026-2032年) 交通管理市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、設備、部署類型、最終用戶及解決方案分類

交通管理市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、設備、部署類型、最終用戶及解決方案分類 交通管理市場規模、佔有率和成長分析(按組件、系統、應用和地區分類)—產業預測(2026-2033 年)交通管理市場預測至2032年:按組件、系統、部署模式、應用、最終用戶和區域分類的全球分析

交通管理市場規模、佔有率和成長分析(按組件、系統、應用和地區分類)—產業預測(2026-2033 年)交通管理市場預測至2032年:按組件、系統、部署模式、應用、最終用戶和區域分類的全球分析 智慧交通管理系統市場-全球產業規模、佔有率、趨勢、機會和預測(按組件、按解決方案類型、按應用、按地區和按競爭分類,2020 年至 2030 年)

智慧交通管理系統市場-全球產業規模、佔有率、趨勢、機會和預測(按組件、按解決方案類型、按應用、按地區和按競爭分類,2020 年至 2030 年) 智慧交通管理的全球市場:2025-2030年

智慧交通管理的全球市場:2025-2030年