|

市場調查報告書

商品編碼

1936561

發電機組市場機會、成長要素、產業趨勢分析及2026年至2035年預測Generator Sets Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

全球發電機組市場預計到 2025 年將達到 487 億美元,到 2035 年將達到 1,076 億美元,年複合成長率為 8.2%。

全球電力需求不斷成長,這主要得益於工業的快速發展和商業活動的擴張,進而推動了各行業對發電機組的需求。工業、醫療、通訊和製造業等關鍵產業對持續供電的依賴性日益增強,進一步推動了對這些系統的需求。發電機組通常將柴油或天然氣燃氣引擎與發電機整合在一起,可在電網不穩定、不穩定或無法供電的地區提供可靠的電力源。新興市場頻繁的停電,加上都市化進程的加速和基礎設施的完善,正在加速備用電源解決方案的普及。燃油效率的提高、排放氣體的減少、噪音控制、數位化監控、基於物聯網的分析以及預測性維護等技術進步,正日益影響產品開發和客戶期望。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 487億美元 |

| 預測金額 | 1076億美元 |

| 複合年成長率 | 8.2% |

截至2025年,柴油發電機組市佔率達76.2%。隨著電力供應不穩定的地區對可靠備用電源的需求持續成長,柴油發電機組仍是工業、商業和基礎設施應用的首選。製造商正致力於減少排放氣體、提高燃油效率和降低運行噪音——這些都是柴油發電機組設計的關鍵挑戰。此外,緊急應變和關鍵公共服務對快速電力解決方案的需求日益成長,也進一步推動了柴油發電機組的應用。

預計2025年,主電源/連續發電機市場規模將達149億美元。需要穩定電壓和頻率以進行精密操作的工業領域,越來越依賴能夠應對長時間運作週期和重型機械負載的可靠主電源發電機。這些系統在滿足大規模工業和營運需求方面的可靠性,持續推動它們在能源密集產業的應用。

預計到2025年,美國發電機組市場將佔據85.8%的市場佔有率,市場規模將達到86億美元。颶風、洪水、冰暴和熱浪等極端天氣事件日益頻繁,推動了對可靠緊急備用電源系統的需求,以確保業務永續營運。企業、關鍵基礎設施和公共服務機構正優先部署彈性電力解決方案,以最大限度地減少停機時間,避免代價高昂的業務中斷。此外,商業設施、工業基地和大型城市開發的擴張也進一步加速了發電機組在美國的普及應用。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 原物料供應及採購分析

- 製造能力評估

- 供應鏈韌性與風險因素

- 配電網路分析

- 監管環境

- 產業影響因素

- 促進要素

- 產業潛在風險與挑戰

- 成長潛力分析

- 波特五力分析

- PESTEL 分析

- 發電機組成本結構分析

- 價格趨勢分析

- 額定功率

- 按地區

- 新的機會與趨勢

- 數位化和物聯網整合

第4章 競爭情勢

- 介紹

- 按地區分類的公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 中東

- 非洲

- 拉丁美洲

- 戰略儀錶板

- Key partnerships &collaborations

- Major M&A activities

- Product innovations &launches

- Market expansion strategies

- 策略舉措

- 競爭標竿分析

- 創新與科技趨勢

第5章 依功率等級分類的市場規模及預測(2022-2035年)

- ≤50 kVA

- 50千伏安至125千伏安

- 125千伏安至200千伏安

- 200千伏安至330千伏安

- 330千伏安至750千伏安

- 超過750千伏安

第6章 依燃料類型分類的市場規模及預測(2022-2035年)

- 柴油引擎

- 氣體

- 混合

7. 依最終用途分類的市場規模及預測(2022-2035年)

- 住宅

- 獨立式住宅

- 多用戶住宅

- 商業的

- 溝通

- 衛生保健

- 資料中心

- 教育機構

- 政府機構

- 飯店業

- 零售

- 房地產

- 商業設施

- 基礎設施

- 其他

- 工業的

- 石油和天然氣

- 製造業

- 建造

- 電力公司

- 礦業

- 運輸/物流

- 其他

第8章 依應用領域分類的市場規模及預測(2022-2035年)

- 支援

- 尖峰用電調節

- 主運轉/連續運行

第9章 依銷售管道分類的市場規模及預測,2022-2035年

- 線上

- 經銷商

- 零售

第10章 2022-2035年各地區市場規模及預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 俄羅斯

- 英國

- 德國

- 法國

- 西班牙

- 奧地利

- 義大利

- 亞太地區

- 中國

- 澳洲

- 印度

- 日本

- 韓國

- 印尼

- 馬來西亞

- 泰國

- 越南

- 菲律賓

- 緬甸

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 卡達

- 土耳其

- 伊朗

- 阿曼

- 非洲

- 埃及

- 奈及利亞

- 阿爾及利亞

- 南非

- 安哥拉

- 肯亞

- 莫三比克

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 智利

第11章:公司簡介

- Aggreko

- American Honda Motor

- ASHOK LEYLAND

- Atlas Copco

- Briggs &Stratton

- Caterpillar

- Cummins

- Deere &Company

- FG Wilson

- Generac Power Systems

- Greaves Cotton

- HIMOINSA

- HUU TOAN GROUP

- JC Bamford Excavators

- Kirloskar

- MAHINDRA POWEROL

- Mitsubishi Heavy Industries

- Rehlko

- Rolls-Royce

- Sterling and Wilson

- Sudhir Power

- Supernova Genset

- Wartsila

- Yamaha Motor

- YANMAR HOLDINGS

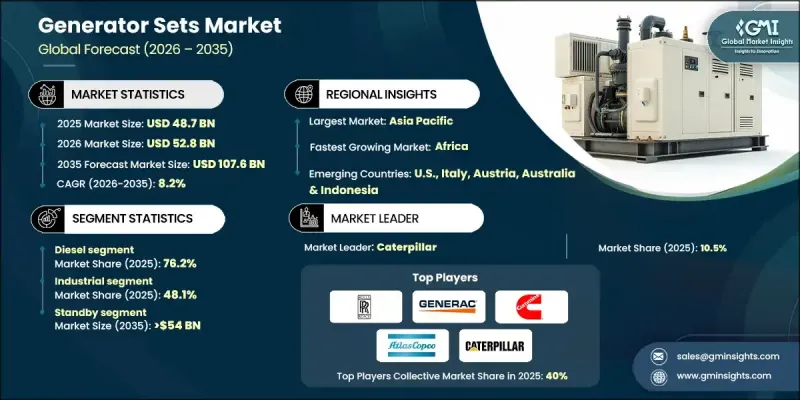

The Global Generator Sets Market was valued at USD 48.7 billion in 2025 and is estimated to grow at a CAGR of 8.2% to reach USD 107.6 billion by 2035.

Rising electricity demand worldwide, fueled by rapid industrial growth and expanding commercial activities, is driving the adoption of generator sets across various sectors. Increasing reliance on continuous power for critical operations in industries, healthcare, telecom, and manufacturing is boosting the demand for these systems. A generator set, which integrates an engine, usually diesel or natural gas, with an alternator, provides a dependable source of electricity where grid power is unreliable, unstable, or unavailable. The frequent power outages in emerging markets, coupled with growing urbanization and infrastructure development, are accelerating the installation of backup power solutions. Technological advancements such as improved fuel efficiency, emission reductions, noise control, digital monitoring, IoT-enabled analytics, and predictive maintenance are increasingly shaping product development and customer expectations.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $48.7 Billion |

| Forecast Value | $107.6 Billion |

| CAGR | 8.2% |

The diesel generator sets segment accounted for 76.2% share in 2025. As demand for dependable backup power continues to rise in regions with unstable electricity supply, diesel gensets remain the preferred choice for industrial, commercial, and infrastructure applications. Manufacturers are focusing on reducing emissions, improving fuel efficiency, and minimizing operational noise, which are key priorities in diesel genset design. There is also a growing need for rapid-response power solutions for emergency preparedness and critical public services, further driving the uptake of diesel units.

The prime/continuous generator segment reached USD 14.9 billion in 2025. Industries requiring consistent voltage and frequency stability for precision operations increasingly depend on robust prime-power gensets capable of handling long duty cycles and heavy mechanical loads. The reliability of these systems in supporting large-scale industrial and operational demands continues to strengthen their adoption across sectors with high energy needs.

United States Generator Sets Market held an 85.8% share, generating USD 8.6 billion in 2025. The increasing frequency of extreme weather events, such as hurricanes, floods, ice storms, and heatwaves, is driving the demand for dependable emergency backup power systems to ensure uninterrupted operations. Businesses, critical infrastructure, and public service facilities are prioritizing resilient power solutions to minimize downtime and avoid costly disruptions. Moreover, the growth of commercial complexes, industrial hubs, and large-scale urban developments is further accelerating the adoption of generator sets across the country.

Key players in the Global Generator Sets Market include Briggs & Stratton, Cummins, YANMAR HOLDINGS, Sterling and Wilson, Atlas Copco, Aggreko, Rehlko, Caterpillar, HIMOINSA, American Honda Motor, Generac Power Systems, Rolls-Royce, FG Wilson, Mahindra Powerol, Deere & Company, Supernova Genset, HUU TOAN GROUP, Kirloskar, Ashok Leyland, Greaves Cotton, Yamaha Motor, Mitsubishi Heavy Industries, and Sudhir Power. To strengthen their position, companies in the generator sets industry are adopting several strategic approaches. They are investing in research and development to deliver energy-efficient, low-emission, and quieter genset models. Strategic partnerships, mergers, and acquisitions are helping them expand their geographical presence and enter new markets. Firms are also integrating smart technologies, including IoT-enabled monitoring and predictive maintenance solutions, to meet evolving customer expectations. Additionally, a strong focus on after-sales service, digital platforms for real-time performance tracking, and customization options for industrial and commercial clients enhances brand loyalty and ensures sustained market growth.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates & forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Power rating trends

- 2.4 Fuel trends

- 2.5 End use trends

- 2.6 Application trends

- 2.7 Sales channel trends

- 2.8 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of generator sets

- 3.8 Price trend analysis

- 3.8.1 By power rating

- 3.8.2 By region

- 3.9 Emerging opportunities & trends

- 3.10 Digitalization and IoT integration

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East

- 4.2.5 Africa

- 4.2.6 Latin America

- 4.3 Strategic dashboard

- 4.3.1 Key partnerships & collaborations

- 4.3.2 Major M&A activities

- 4.3.3 Product innovations & launches

- 4.3.4 Market expansion strategies

- 4.4 Strategic initiatives

- 4.5 Competitive benchmarking

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Power Rating, 2022 - 2035 (USD Million & ‘000 Units)

- 5.1 Key trends

- 5.2 ≤ 50 kVA

- 5.3 > 50 kVA - 125 kVA

- 5.4 > 125 kVA - 200 kVA

- 5.5 > 200 kVA - 330 kVA

- 5.6 > 330 kVA - 750 kVA

- 5.7 > 750 kVA

Chapter 6 Market Size and Forecast, By Fuel, 2022 - 2035 (USD Million & ‘000 Units)

- 6.1 Key trends

- 6.2 Diesel

- 6.3 Gas

- 6.4 Hybrid

Chapter 7 Market Size and Forecast, By End Use, 2022 - 2035 (USD Million & ‘000 Units)

- 7.1 Key trends

- 7.2 Residential

- 7.2.1 Single family

- 7.2.2 Multi family

- 7.3 Commercial

- 7.3.1 Telecom

- 7.3.2 Healthcare

- 7.3.3 Data centers

- 7.3.4 Educational institutions

- 7.3.5 Government centers

- 7.3.6 Hospitality

- 7.3.7 Retail sales

- 7.3.8 Real estate

- 7.3.9 Commercial complex

- 7.3.10 Infrastructure

- 7.3.11 Others

- 7.4 Industrial

- 7.4.1 Oil & gas

- 7.4.2 Manufacturing

- 7.4.3 Construction

- 7.4.4 Electric utilities

- 7.4.5 Mining

- 7.4.6 Transportation & logistics

- 7.4.7 Others

Chapter 8 Market Size and Forecast, By Application, 2022 - 2035 (USD Million & ‘000 Units)

- 8.1 Key trends

- 8.2 Standby

- 8.3 Peak shaving

- 8.4 Prime/continuous

Chapter 9 Market Size and Forecast, By Sales Channel, 2022 - 2035 (USD Million & ‘000 Units)

- 9.1 Key trends

- 9.2 Online

- 9.3 Dealer

- 9.4 Retail

Chapter 10 Market Size and Forecast, By Region, 2022 - 2035 (USD Million & ‘000 Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Russia

- 10.3.2 UK

- 10.3.3 Germany

- 10.3.4 France

- 10.3.5 Spain

- 10.3.6 Austria

- 10.3.7 Italy

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Australia

- 10.4.3 India

- 10.4.4 Japan

- 10.4.5 South Korea

- 10.4.6 Indonesia

- 10.4.7 Malaysia

- 10.4.8 Thailand

- 10.4.9 Vietnam

- 10.4.10 Philippines

- 10.4.11 Myanmar

- 10.5 Middle East & Africa

- 10.5.1 Saudi Arabia

- 10.5.2 UAE

- 10.5.3 Qatar

- 10.5.4 Turkey

- 10.5.5 Iran

- 10.5.6 Oman

- 10.6 Africa

- 10.6.1 Egypt

- 10.6.2 Nigeria

- 10.6.3 Algeria

- 10.6.4 South Africa

- 10.6.5 Angola

- 10.6.6 Kenya

- 10.6.7 Mozambique

- 10.7 Latin America

- 10.7.1 Brazil

- 10.7.2 Mexico

- 10.7.3 Argentina

- 10.7.4 Chile

Chapter 11 Company Profiles

- 11.1 Aggreko

- 11.2 American Honda Motor

- 11.3 ASHOK LEYLAND

- 11.4 Atlas Copco

- 11.5 Briggs & Stratton

- 11.6 Caterpillar

- 11.7 Cummins

- 11.8 Deere & Company

- 11.9 FG Wilson

- 11.10 Generac Power Systems

- 11.11 Greaves Cotton

- 11.12 HIMOINSA

- 11.13 HỮU TOAN GROUP

- 11.14 J C Bamford Excavators

- 11.15 Kirloskar

- 11.16 MAHINDRA POWEROL

- 11.17 Mitsubishi Heavy Industries

- 11.18 Rehlko

- 11.19 Rolls-Royce

- 11.20 Sterling and Wilson

- 11.21 Sudhir Power

- 11.22 Supernova Genset

- 11.23 Wartsila

- 11.24 Yamaha Motor

- 11.25 YANMAR HOLDINGS

發電機組市場:依燃料類型、型號、相數、額定輸出功率及最終用戶分類-2026-2032年全球市場預測防水發電機組市場:依燃料類型、額定功率、應用、便攜性、相數、冷卻方式和機殼類型分類,全球預測,2026-2032年

發電機組市場:依燃料類型、型號、相數、額定輸出功率及最終用戶分類-2026-2032年全球市場預測防水發電機組市場:依燃料類型、額定功率、應用、便攜性、相數、冷卻方式和機殼類型分類,全球預測,2026-2032年 尖峰用電調節發電機組市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測重油發電機組市場(依引擎類型、額定功率、安裝方式、冷卻方式、燃油管理系統及最終用途分類),全球預測(2026-2032)2026 年至 2035 年商用發電機市場機會、成長要素、產業趨勢分析及預測。

尖峰用電調節發電機組市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測重油發電機組市場(依引擎類型、額定功率、安裝方式、冷卻方式、燃油管理系統及最終用途分類),全球預測(2026-2032)2026 年至 2035 年商用發電機市場機會、成長要素、產業趨勢分析及預測。 歐洲發電機組:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)發電機組:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

歐洲發電機組:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)發電機組:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 2026年全球發電機組市場報告

2026年全球發電機組市場報告 發電機市場-全球產業規模、佔有率、趨勢、機會、預測:按燃料類型、功率輸出、便攜性、應用、地區和競爭格局分類,2021-2031年發電機組市場 - 全球產業規模、佔有率、趨勢、機會及預測(按容量、應用、最終用戶、燃料、地區和競爭格局分類),2021-2031年

發電機市場-全球產業規模、佔有率、趨勢、機會、預測:按燃料類型、功率輸出、便攜性、應用、地區和競爭格局分類,2021-2031年發電機組市場 - 全球產業規模、佔有率、趨勢、機會及預測(按容量、應用、最終用戶、燃料、地區和競爭格局分類),2021-2031年