|

市場調查報告書

商品編碼

1934766

歐洲發電機組:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)Europe Generator Sets - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

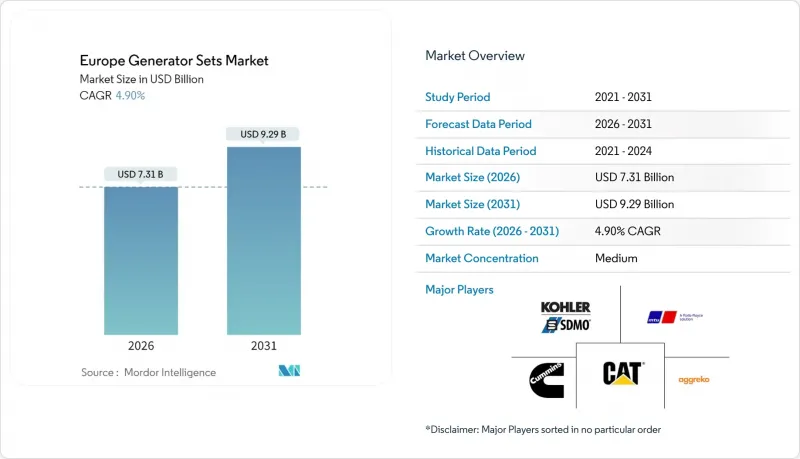

預計到 2026 年,歐洲發電機組市場價值將達到 73.1 億美元。

預計該產業規模將從 2025 年的 69.7 億美元成長到 2031 年的 92.9 億美元,2026 年至 2031 年的複合年成長率為 4.9%。

隨著資料中心、醫療機構和可再生能源計劃尋求低碳備用電源,市場需求正從純柴油產品轉向雙燃料、天然氣和氫燃料平台。企業永續發展計畫、第五階段排放法規以及大都會圈的電網擁塞正在加速這一轉型,而電池-發電機混合系統和模組化建築則正在改變採購趨勢。德國仍然是最大的單一國家市場,但西班牙快速的可再生能源部署和基礎設施規劃正推動最快的成長。在容量方面,75kVA至375kVA的容量仍佔據出貨量的主導地位,但超大規模資料中心正在推動750kVA至2000kVA機組的需求激增。競爭策略的重點是燃料獨立式引擎、氫燃料試點項目和數位化互聯的租賃車隊,這些都為微電網部署、孤島供電和建築工地開闢了新的機會。

歐洲發電機組市場趨勢與洞察

資料中心和醫療領域對可靠備用電源的需求日益成長

法蘭克福、阿姆斯特丹、巴黎和都柏林的資料中心營運商正在增設兆瓦級發電機組,以緩解電網壓力,滿足Tier III運作,並在頻率響應市場實現容量貨幣化。醫院正在升級到模組化、可並聯運轉的發電機組,以滿足EN 50172切換規則和24小時燃料儲備要求。康明斯預計2024年歐洲資料中心訂單將實現兩位數成長,其中3500 kVA QSK95成為首選平台。設備擴大被指定用於備用和尖峰用電調節,從而延長平均運作並推動對低氮氧化物燃氣機組的需求。醫療保健採購者更傾向於選擇具備遠距離診斷功能的設備,以支援預防性保養和ISO 22301業務連續性審核。

歐洲各地建築業蓬勃發展,基礎建設升級改造。

西班牙的太陽能和交通基礎設施擴建、波蘭的鐵路網路更新以及義大利的國家復甦和韌性計劃,都導致計劃工期延長,並促使行動電源租賃合約的期限也隨之延長。預計到2024年,歐洲建設產業的產值將達到1.6兆歐元,而對於缺乏固定現場電源的場所而言,100kVA至500kVA的可攜式發電機仍然至關重要。 Aggreko公司在2024年將其歐洲租賃設備規模擴大了12%,推出了符合歐V排放標準的柴油-電池混合動力發電機,這些發電機在低負載運轉時可降低30%的油耗。承包商擴大要求使用具備遙測功能的設備,以便即時監控運作時間、排放和油耗,並且擴大將發電機整合到更廣泛的現場管理儀錶板中。

歐盟第五/六階段排放氣體法規將增加資本支出(CAPEX)和營運費用(OPEX)。

第五階段排放標準將於2024年全面實施,屆時功率超過56千瓦的柴油發電機必須配備柴油顆粒過濾器(DPF)、選擇性催化還原(SCR)和廢氣再循環(EGR)系統,將使購置成本增加高達18%。此外,柴油引擎廢氣處理液(DEF)的添加和過濾器再生維護成本將增加0.02至0.04歐元/kWh。功率在75千伏安至375千伏安之間的小規模用戶正在推遲升級或轉向燃氣發電機,阿特拉斯·科普柯公司200千伏安以下柴油發電機訂單下降9%,而燃氣和混合動力機組的出貨量成長14%,便印證了這一點。提案的第六階段排放標準將從2027年起進一步收緊氮氧化物(NOx)排放標準,提高30%。這將迫使原始設備製造商(OEM)採用氨逃逸催化劑,進一步增加成本並促使用戶轉向其他燃料。

細分市場分析

2025年,75kVA至375kVA功率等級的發電機組將佔據歐洲發電機組市場34.62%的佔有率,這得益於標準化的機殼、大規模生產和具有競爭力的價格。這些機組為零售連鎖店和商業建築的空調、冷凍和銷售點系統提供備用電源。隨著電池儲能技術在小規模併網負載中的滲透率不斷提高,市場成長速度有所放緩,但由於第五階段排放法規要求使用新型硬體,替換需求仍將持續存在。

750 kVA 至 2,000 kVA 容量段的複合年成長率將達到 6.25%,主要成長動力來自資料中心園區和大型製造廠部署的 N+1 模組化不間斷不斷電系統系統。康明斯 3,500 kVA QSK95 機組允許操作員在不重新設計開關設備的情況下增加 1 MW 的容量模組,從而縮短安裝時間。 2,000 kVA 以上的容量段,併網電力公司和獨立電力公司正在部署 Walsill 和 Caterpillar 的燃氣或雙燃料機組。 75 kVA 以下的容量段,在停電時間不超過四小時的地區,住宅和小規模商業用電需求正在下降,因此電池-逆變器組合更受歡迎。

到2025年,柴油將佔燃料結構的52.88%,這主要歸功於其大規模的裝機量和廣泛的供應。第五階段排放標準、都市區低排放區以及範圍2排放目標正在推動雙燃料引擎的普及,這類引擎可減少30%的二氧化碳排放和50%的顆粒物排放。天然氣引擎的需求量將佔約22%,主要集中在德國和荷蘭等天然氣管道密集的地區。同時,生質燃料車型的佔比將維持在3%以下,但隨著Neste公司氫化植物油(HVO)供應量的增加,其規模正在擴大。

康明斯、沃爾西爾和羅爾斯·羅伊斯的氫燃料引擎於2024年投入商業應用。目前氫燃料引擎的普及率仍低於1%,但隨著電解建設和管道基礎設施的成熟,預計普及率將會上升。丙烷、沼氣和垃圾掩埋沼氣引擎的應用則更為有限。預計到2031年,柴油引擎的市佔率將降至47.50%以下,但這主要是由於天然氣和混合動力產品的快速成長,而非柴油引擎將被完全取代。

歐洲發電機組市場報告按容量(小於 75KVA、75-375KVA、375-750KVA、750-2,000KVA、大於2,000KVA)、燃料類型(柴油、天然氣、雙燃料/混合動力、可再生/生質燃料、其他)、應用(緊急電源、市電/不間斷電源、其他)、最終用戶(住宅、商業建築、資料中心、其他)和地區(德國、英國、西班牙、其他)進行細分。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 市場定義與研究假設

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 資料中心和醫療領域對可靠備用電源的需求日益成長

- 歐洲各地的建築業蓬勃發展和基礎建設也在加速發展。

- 電網基礎設施老化和氣候變遷導致停電

- 在島嶼和礦區引進柴油-太陽能混合微電網

- 企業永續性目標推動了對天然氣和生質燃料發電機的需求

- 氫燃料電池發電機組的商業化進程開始

- 市場限制

- 歐盟第五/六階段排放標準增加了資本支出(CAPEX)和營運成本(OPEX)。

- 提高電網可靠性可降低備用需求

- 電池成本的急劇下降(超過200歐元/千瓦時)對小型柴油發電機構成了挑戰。

- 歐盟碳邊境調節機制導致出口成本增加

- 供應鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代產品和服務的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按產能

- 小於75千伏安

- 75~375kVA

- 375~750 kVA

- 750~2,000 kVA

- 2000千伏安或以上

- 按燃料類型

- 柴油引擎

- 天然氣

- 雙燃料和混合動力

- 可再生能源/生質燃料

- 其他

- 透過使用

- 應急電源

- 主電源/持續電源

- 尖峰用電調節

- 租賃/臨時電源

- 微電網和混合支持

- 最終用戶

- 住宅

- 商業建築

- 工業/製造業

- 資料中心

- 醫療設施

- 石油和天然氣

- 公共產業/電力

- 採礦和建設業

- 按地區

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 俄羅斯

- 其他歐洲地區

第6章 競爭情勢

- 市場集中度

- 策略性舉措(併購、夥伴關係、購電協議)

- 市場佔有率分析(主要企業的市場排名和佔有率)

- 公司簡介

- Cummins Inc.

- Caterpillar Inc.

- Rolls-Royce Power Systems(MTU)

- Generac Holdings Inc.

- Kohler Co./SDMO

- Aggreko plc

- Wartsila Corp.

- Yanmar Holdings Co. Ltd.

- Mitsubishi Heavy Industries Ltd.

- Perkins Engines Company Ltd.

- FG Wilson

- HIMOINSA SL

- Volvo Penta

- Kirloskar Oil Engines Ltd.

- Pramac SpA

- Atlas Copco AB

- Doosan Portable Power

- DEUTZ AG

- Honda Power Products

- Briggs & Stratton

第7章 市場機會與未來展望

Europe Generator Sets market size in 2026 is estimated at USD 7.31 billion, growing from 2025 value of USD 6.97 billion with 2031 projections showing USD 9.29 billion, growing at 4.9% CAGR over 2026-2031.

Demand is shifting from diesel-only products to dual-fuel, gas and hydrogen-ready platforms as data centers, healthcare facilities, and renewable energy projects seek lower-carbon back-up power. Corporate sustainability programs, Stage V emissions rules, and grid congestion in metropolitan clusters are accelerating the transition, while battery-genset hybrids and modular architectures are reshaping procurement preferences. Germany remains the single-largest country market, but Spain's rapid renewable build-out and infrastructure programs are creating the fastest incremental growth. At the capacity level, the 75 kVA to 375 kVA segment still dominates shipments, yet hyperscale data centers are driving a swift rise in demand for 750 kVA to 2,000 kVA units. Competitive strategies center on fuel-agnostic engines, hydrogen pilots, and digitally connected rental fleets, which open up opportunities in microgrid deployments, island utilities, and construction sites.

Europe Generator Sets Market Trends and Insights

Growing Demand for Reliable Back-Up Power in Data Centers & Healthcare

Data-center operators in Frankfurt, Amsterdam, Paris, and Dublin are adding multi-megawatt generators to offset grid constraints, satisfy Tier III uptime, and monetize capacity in frequency-response markets. Hospitals are upgrading to modular, parallel-capable gensets to meet EN 50172 switchover rules and 24-hour fuel reserve requirements. Cummins logged a double-digit increase in European data-center orders in 2024, with its 3,500 kVA QSK95 emerging as a preferred platform. Equipment is increasingly specified for both standby and peak-shaving roles, lifting average runtime and driving demand for low-NOx gas units. Healthcare buyers favor units with remote diagnostics to support preventive maintenance and ISO 22301 business continuity audits.

Construction Boom & Infrastructure Upgrades Across Europe

Spain's solar and transport build-out, Poland's rail overhaul, and Italy's National Recovery and Resilience Plan are stretching project timelines and extending rental contracts for mobile power. The European construction sector generated EUR 1.6 trillion of output in 2024, and portable gensets between 100 kVA and 500 kVA remain essential where sites lack a permanent grid supply. Aggreko expanded its European rental fleet by 12% in 2024, with Stage V-compliant diesel-battery hybrids cutting fuel by 30% during low-load hours. Contractors increasingly demand telemetry-enabled sets to monitor runtime, emissions, and fuel use in real time, embedding gensets into broader site-management dashboards.

EU Stage V/VI Emission Norms Heighten CAPEX & OPEX

Stage V rules, fully effective from 2024, compel diesel gensets above 56 kW to add diesel particulate filters, SCR, and EGR, lifting capital cost by up to 18% and adding EUR 0.02-0.04 /kWh in maintenance for DEF replenishment and filter regeneration. Smaller buyers in the 75 kVA-375 kVA range are deferring replacements or shifting to gas units, evidenced by a 9% drop in diesel orders below 200 kVA at Atlas Copco and a 14% rise in gas and hybrid shipments. Proposed Stage VI limits would tighten NOx thresholds by an additional 30% after 2027, prompting OEMs to adopt ammonia-slip catalysts, which would drive further cost escalation and encourage fuel switching.

Other drivers and restraints analyzed in the detailed report include:

- Aging Grid Infrastructure & Climate-Driven Outages

- Hybrid Diesel-Solar Micro-Grids on Islands & Mine Sites

- Battery Storage Cost Plunge Challenges Small Diesel Sets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 75 kVA-375 kVA bracket accounted for 34.62% of the European generator sets market share in 2025, supported by standardized enclosures, high-volume production, and competitive pricing. These units back up HVAC, refrigeration, and point-of-sale systems in retail chains and commercial buildings. Growth is flattening as battery storage penetrates small, grid-connected loads, yet replacement demand persists because Stage V compliance mandates newer hardware.

The 750 kVA-2,000 kVA segment is on track for a 6.25% CAGR, propelled by data-center campuses and large-scale manufacturing that implement modular sets in N+1 layouts to achieve uninterrupted power. Cummins' 3,500 kVA QSK95 enables operators to add 1 MW blocks without re-engineering switchgear, reducing installation timelines. Above 2,000 kVA, applications include grid-balancing and island utilities deploying gas or dual-fuel units from Wartsila and Caterpillar. Below 75 kVA, residential and small commercial demand is shrinking as battery-inverter combinations gain favor in regions with outage durations of four hours or less.

Diesel held 52.88% of the 2025 fuel mix, mostly due to a large installed base and universal fuel availability. Stage V costs, urban low-emission zones, and Scope 2 targets are prompting buyers to adopt dual-fuel sets that emit 30% less CO2 and 50% less particulates. Natural-gas units represent roughly 22% of demand, concentrated in pipeline-dense regions such as Germany and the Netherlands, while bio-fuel-ready models remain below 3% but are scaling with HVO supply increases from Neste.

Hydrogen-ready engines from Cummins, Wartsila, and Rolls-Royce entered commercial portfolios in 2024; adoption is still under 1% but is expected to climb once electrolyzer build-outs and pipeline infrastructure mature. Propane, biogas, and landfill-gas engines serve tighter, niche sectors. Diesel's share is forecast to drop below 47.50% by 2031, not due to outright displacement, but rather because of faster growth in gas and hybrid offerings.

The Europe Generator Sets Market Report is Segmented by Capacity (Below 75 KVA, 75 To 375 KVA, 375 To 750 KVA, 750 To 2, 000 KVA, and Above 2, 000 KVA), Fuel Type (Diesel, Natural Gas, Dual-Fuel and Hybrid, Renewable/Bio-fuel, and Others), Application (Standby Power, Prime/Continuous Power, and More), End-User (Residential, Commercial Buildings, Data Centers, and More), and Geography (Germany, United Kingdom, Spain, and More).

List of Companies Covered in this Report:

- Cummins Inc.

- Caterpillar Inc.

- Rolls-Royce Power Systems (MTU)

- Generac Holdings Inc.

- Kohler Co. / SDMO

- Aggreko plc

- Wartsila Corp.

- Yanmar Holdings Co. Ltd.

- Mitsubishi Heavy Industries Ltd.

- Perkins Engines Company Ltd.

- FG Wilson

- HIMOINSA S.L.

- Volvo Penta

- Kirloskar Oil Engines Ltd.

- Pramac S.p.A.

- Atlas Copco AB

- Doosan Portable Power

- DEUTZ AG

- Honda Power Products

- Briggs & Stratton

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Market Definition & Study Assumptions

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for reliable back-up power in data centres & healthcare

- 4.2.2 Construction boom & infrastructure upgrades across Europe

- 4.2.3 Aging grid infrastructure & climate-driven outages

- 4.2.4 Hybrid diesel-solar microgrids adoption on islands & mine sites

- 4.2.5 Corporate sustainability targets boosting gas & biofuel gensets

- 4.2.6 Commercial launch of hydrogen-ready generator engines

- 4.3 Market Restraints

- 4.3.1 EU Stage V/VI emission norms heighten CAPEX & OPEX

- 4.3.2 Grid reliability improvements curb standby demand

- 4.3.3 Battery storage cost plunge (More Than EUR 200/kWh) challenges small diesel sets

- 4.3.4 EU Carbon Border Adjustment Mechanism raises export costs

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products & Services

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Capacity

- 5.1.1 Below 75 kVA

- 5.1.2 75 to 375 kVA

- 5.1.3 375 to 750 kVA

- 5.1.4 750 to 2,000 kVA

- 5.1.5 Above 2,000 kVA

- 5.2 By Fuel Type

- 5.2.1 Diesel

- 5.2.2 Natural Gas

- 5.2.3 Dual-Fuel and Hybrid

- 5.2.4 Renewable/Bio-fuel

- 5.2.5 Others

- 5.3 By Application

- 5.3.1 Standby Power

- 5.3.2 Prime/Continuous Power

- 5.3.3 Peak-Shaving

- 5.3.4 Rental/Temporary Power

- 5.3.5 Micro-grid and Hybrid Support

- 5.4 By End-User

- 5.4.1 Residential

- 5.4.2 Commercial Buildings

- 5.4.3 Industrial and Manufacturing

- 5.4.4 Data Centers

- 5.4.5 Healthcare Facilities

- 5.4.6 Oil and Gas

- 5.4.7 Utilities and Power

- 5.4.8 Mining and Construction

- 5.5 By Geography

- 5.5.1 Germany

- 5.5.2 United Kingdom

- 5.5.3 France

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 NORDIC Countries

- 5.5.7 Russia

- 5.5.8 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Cummins Inc.

- 6.4.2 Caterpillar Inc.

- 6.4.3 Rolls-Royce Power Systems (MTU)

- 6.4.4 Generac Holdings Inc.

- 6.4.5 Kohler Co. / SDMO

- 6.4.6 Aggreko plc

- 6.4.7 Wartsila Corp.

- 6.4.8 Yanmar Holdings Co. Ltd.

- 6.4.9 Mitsubishi Heavy Industries Ltd.

- 6.4.10 Perkins Engines Company Ltd.

- 6.4.11 FG Wilson

- 6.4.12 HIMOINSA S.L.

- 6.4.13 Volvo Penta

- 6.4.14 Kirloskar Oil Engines Ltd.

- 6.4.15 Pramac S.p.A.

- 6.4.16 Atlas Copco AB

- 6.4.17 Doosan Portable Power

- 6.4.18 DEUTZ AG

- 6.4.19 Honda Power Products

- 6.4.20 Briggs & Stratton

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

商用發電機市場 - 全球產業規模、佔有率、趨勢、機會、預測:按燃料、便攜性、功率輸出、應用、地區和競爭格局分類,2021-2031年

商用發電機市場 - 全球產業規模、佔有率、趨勢、機會、預測:按燃料、便攜性、功率輸出、應用、地區和競爭格局分類,2021-2031年 發電機組市場:依燃料類型、型號、相數、額定輸出功率及最終用戶分類-2026-2032年全球市場預測防水發電機組市場:依燃料類型、額定功率、應用、便攜性、相數、冷卻方式和機殼類型分類,全球預測,2026-2032年

發電機組市場:依燃料類型、型號、相數、額定輸出功率及最終用戶分類-2026-2032年全球市場預測防水發電機組市場:依燃料類型、額定功率、應用、便攜性、相數、冷卻方式和機殼類型分類,全球預測,2026-2032年 尖峰用電調節發電機組市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測重油發電機組市場(依引擎類型、額定功率、安裝方式、冷卻方式、燃油管理系統及最終用途分類),全球預測(2026-2032)2026 年至 2035 年商用發電機市場機會、成長要素、產業趨勢分析及預測。

尖峰用電調節發電機組市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測重油發電機組市場(依引擎類型、額定功率、安裝方式、冷卻方式、燃油管理系統及最終用途分類),全球預測(2026-2032)2026 年至 2035 年商用發電機市場機會、成長要素、產業趨勢分析及預測。 發電機組:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

發電機組:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 2026年全球發電機組市場報告發電機市場-全球產業規模、佔有率、趨勢、機會、預測:按燃料類型、功率輸出、便攜性、應用、地區和競爭格局分類,2021-2031年發電機組市場 - 全球產業規模、佔有率、趨勢、機會及預測(按容量、應用、最終用戶、燃料、地區和競爭格局分類),2021-2031年

2026年全球發電機組市場報告發電機市場-全球產業規模、佔有率、趨勢、機會、預測:按燃料類型、功率輸出、便攜性、應用、地區和競爭格局分類,2021-2031年發電機組市場 - 全球產業規模、佔有率、趨勢、機會及預測(按容量、應用、最終用戶、燃料、地區和競爭格局分類),2021-2031年