|

市場調查報告書

商品編碼

1936550

生物界面活性劑市場機會、成長要素、產業趨勢分析及預測(2026-2035年)Biosurfactants Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

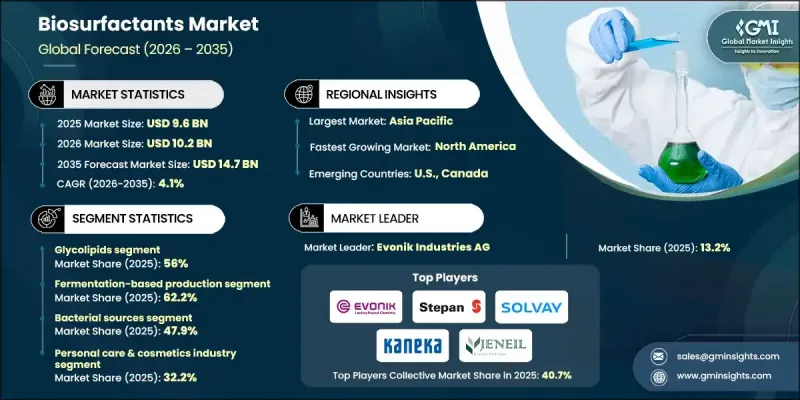

全球生物界面活性劑市場預計到 2025 年將達到 96 億美元,到 2035 年將達到 147 億美元,年複合成長率為 4.1%。

隨著全球各行各業向永續、環保的傳統化學界面活性劑替代品轉型,生物界面活性劑市場正蓬勃發展。生物界面活性劑是由細菌、真菌和酵母等微生物產生的生物來源化合物。它們能夠降低液體、固體和氣體之間的表面張力和界面張力。生物界面活性劑具有多種功能,可用作天然乳化劑、清潔劑、發泡劑和抗菌劑。其可生物分解、低毒性和可再生特性使其成為合成石油化學表面活性劑的理想替代品。生物界面活性劑能夠耐受極端pH值、溫度和鹽度,因此廣泛應用於各種工業領域。它們被廣泛用作製藥和化妝品行業的溫和清潔劑、食品行業的產品穩定劑以及石油和天然氣行業的提高採收率技術。日益增強的環保意識,加上全球監管壓力和永續性計劃,正在進一步加速生物表面活性劑在各地區的應用,尤其是在北美、歐洲和亞太地區。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 96億美元 |

| 預測金額 | 147億美元 |

| 複合年成長率 | 4.1% |

Glico產品在2025年佔據了56%的市場佔有率,預計到2035年將以4.1%的複合年成長率成長。醣脂類產品因其優異的乳化性、發泡和生物分解性而備受青睞,使其在環境修復和工業應用中展現出卓越的功效。這些生物生物界面活性劑由特定的微生物菌株產生,能夠促進生物修復過程,包括石油洩漏的分解,並因其環保高效的性能而備受推崇。醣脂類產品在各個工業領域的廣泛應用和功能可靠性持續推動著該細分市場的成長。

2025年,發酵法生產佔了62.2%的市場佔有率,預計2026年至2035年將以4.2%的複合年成長率成長。發酵法因其成本效益高、產品純度高且製程環境友好,仍是首選的生產方法。先進的生物技術,例如對念珠菌屬、芽孢桿菌屬和假單胞菌屬等微生物菌株的最佳化,提高了生物界面活性劑的產量、品質和穩定性。發酵製程的擴充性和經濟可行性使其成為全球生物界面活性劑供應鏈的基礎。

預計到2025年,北美生物界面活性劑市場將以29.2%的市佔率成為重要的區域領導者。市場成長的促進因素包括消費者對天然和永續產品的偏好、對合成化學品的嚴格監管,以及個人護理、家居和環境修復行業對生物表面活性劑日益成長的需求。主要行業參與者的存在、持續的研發投入以及技術主導的創新進一步鞏固了北美市場的地位,並鼓勵製造商投資先進的生產技術和環保配方。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段的附加價值

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 促進要素

- 產業潛在風險與挑戰

- 市場機遇

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 按類型

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利狀態

- 貿易統計(HS編碼)

(註:貿易統計數據僅涵蓋主要國家。)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續努力

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 考慮到碳足跡

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 依產品類型分類的市場估算與預測,2022-2035年

- 醣脂

- 鼠李醣脂

- 槐醣脂

- 海藻醣脂質

- 脂肽

- 磷脂

- 合成和半合成生物生物界面活性劑

- 甲酯磺酸鹽(MES)

- 烷基聚葡萄糖苷(APG)

- 山梨糖醇酯

- 蔗糖酯

第6章 依生產方式分類的市場估算與預測,2022-2035年

- 基於發酵的生產

- 化學/酵素法合成

- 混合和新興方法

7. 2022-2035年按微生物來源分類的市場估計與預測

- 細菌來源

- 酵母和真菌來源

- 重組/基因改造菌株

第8章 依最終用途產業分類的市場估算與預測,2022-2035年

- 石油和天然氣產業

- 農業產業

- 農業化學品

- 作物保護

- 動物營養

- 化學製造

- 工業用清潔劑

- 油漆和塗料

- 金屬清洗和加工

- 食品飲料業

- 製藥和醫療保健產業

- 藥物用途

- 抗菌劑和抗病毒藥物

- 抗癌藥物應用

- 個人護理和化妝品行業

- 個人保健產品

- 口腔清潔用品

- 皮膚微生物組產品

- 家用清潔劑產業

- 家用清潔劑

- 硬表面清潔劑

- 特殊清潔劑

- 其他

第9章 2022-2035年各地區市場估算與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第10章:公司簡介

- Allied Carbon Solutions Co., Ltd.

- Evonik Industries AG

- Givaudan

- GlycoSurf LLC

- Jeneil Biotech, Inc.

- Kaneka Corporation

- Saraya Co., Ltd.

- Solvay SA

- Stepan Company

- Synthezyme LLC

The Global Biosurfactants Market was valued at USD 9.6 billion in 2025 and is estimated to grow at a CAGR of 4.1% to reach USD 14.7 billion by 2035.

The market is gaining momentum as industries worldwide shift toward sustainable and eco-friendly alternatives to traditional chemical surfactants. Biosurfactants are biologically derived compounds produced by microorganisms, including bacteria, fungi, and yeast, which reduce surface and interfacial tension between liquids, solids, and gases. They serve multiple functions, acting as natural emulsifiers, detergents, foaming agents, and antimicrobial agents. Their biodegradability, low toxicity, and renewable nature make them ideal replacements for synthetic, petrochemical-based surfactants. Biosurfactants are resilient under extreme pH, temperature, and salinity, making them versatile for diverse industrial applications. They are widely adopted in pharmaceuticals and cosmetics for gentle cleansing, in food for product stabilization, and in oil and gas for enhanced oil recovery. Rising environmental awareness, coupled with global regulatory pressure and sustainability initiatives, further accelerates their adoption across regions, particularly in North America, Europe, and Asia-Pacific.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $9.6 Billion |

| Forecast Value | $14.7 Billion |

| CAGR | 4.1% |

The glycolipids segment held a 56% in 2025 and is projected to grow at a CAGR of 4.1% by 2035. Glycolipids dominate due to their exceptional emulsifying, foaming, and biodegradability properties, making them highly effective in environmental remediation and industrial applications. These biosurfactants, produced by specific microbial strains, facilitate bioremediation processes, including oil spill degradation, and are highly valued for their eco-friendly and efficient performance. Their versatility and functional reliability across multiple industries continue to drive the glycolipids segment forward.

The fermentation-based production segment accounted for 62.2% share in 2025 and is expected to grow at a CAGR of 4.2% during 2026-2035. Fermentation remains the preferred manufacturing method due to its cost-effectiveness, high purity output, and environmentally safe processes. Advanced biotechnological techniques optimize microbial strains such as Candida, Bacillus, and Pseudomonas to enhance biosurfactant yields, quality, and consistency. The scalability and economic feasibility of fermentation processes make it a cornerstone of the global biosurfactants supply chain.

North America Biosurfactants Market held a 29.2% share in 2025, emerging as a key regional leader. The market growth is fueled by consumer preference for natural and sustainable products, stringent regulations on synthetic chemicals, and rising adoption across personal care, household, and environmental remediation industries. The presence of major industry players, continuous research and development, and technology-driven innovations further strengthen North America's market position, encouraging manufacturers to invest in advanced production techniques and eco-friendly formulations.

Major companies operating in the Global Biosurfactants Market include GlycoSurf LLC, Solvay S.A., Stepan Company, Allied Carbon Solutions Co., Ltd., Jeneil Biotech, Inc., Kaneka Corporation, Evonik Industries AG, Synthezyme LLC, Givaudan, and Saraya Co. Ltd. Companies in the biosurfactants market are focusing on several key strategies to strengthen their market position and expand global presence. They are investing heavily in R&D to develop high-performance, sustainable biosurfactant formulations tailored for different industrial applications. Strategic partnerships with manufacturers in pharmaceuticals, cosmetics, food, and oil and gas enhance market reach and technology adoption. Companies are also expanding production capacities, optimizing fermentation processes, and introducing multi-functional biosurfactants with improved efficiency and stability.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Production method

- 2.2.4 Microbial sources

- 2.2.5 End use industry

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Glycolipids

- 5.2.1 Rhamnolipids

- 5.2.2 Sophorolipids

- 5.2.3 Trehalolipids

- 5.3 Lipopeptides

- 5.4 Phospholipids

- 5.5 Synthetic & semi-synthetic biosurfactants

- 5.5.1 Methyl ester sulfonates (MES)

- 5.5.2 Alkyl polyglucosides (APG)

- 5.5.3 Sorbitan esters

- 5.5.4 Sucrose esters

Chapter 6 Market Estimates and Forecast, By Production Method, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Fermentation-based production

- 6.3 Chemical & enzymatic synthesis

- 6.4 Hybrid & emerging methods

Chapter 7 Market Estimates and Forecast, By Microbial Source, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Bacterial sources

- 7.3 Yeast & fungal sources

- 7.4 Engineered & recombinant strains

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Oil & gas industry

- 8.3 Agriculture industry

- 8.3.1 Agricultural chemicals

- 8.3.2 Crop protection

- 8.3.3 Animal nutrition

- 8.4 Chemical manufacturing

- 8.4.1 Industrial cleaners

- 8.4.2 Paints & coatings

- 8.4.3 Metal cleaning & processing

- 8.5 Food & beverage industry

- 8.6 Pharmaceutical & healthcare industry

- 8.6.1 Pharmaceutical applications

- 8.6.2 Antimicrobial/antiviral agents

- 8.6.3 Anticancer applications

- 8.7 Personal care & cosmetics industry

- 8.7.1 Personal care products

- 8.7.2 Oral care

- 8.7.3 Skin microbiome products

- 8.8 Household cleaning industry

- 8.8.1 Household detergents

- 8.8.2 Hard surface cleaners

- 8.8.3 Specialty cleaners

- 8.9 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Allied Carbon Solutions Co., Ltd.

- 10.2 Evonik Industries AG

- 10.3 Givaudan

- 10.4 GlycoSurf LLC

- 10.5 Jeneil Biotech, Inc.

- 10.6 Kaneka Corporation

- 10.7 Saraya Co., Ltd.

- 10.8 Solvay S.A.

- 10.9 Stepan Company

- 10.10 Synthezyme LLC

微生物生物界面活性劑市場:按類型、原料、形態、通路和應用分類-2026-2032年全球市場預測

微生物生物界面活性劑市場:按類型、原料、形態、通路和應用分類-2026-2032年全球市場預測 生物界面活性劑市場:依類型(醣脂、脂肽、磷脂質、聚合物生物界面活性劑)、應用和來源(微生物來源、植物來源) - 全球預測(~2036年)

生物界面活性劑市場:依類型(醣脂、脂肽、磷脂質、聚合物生物界面活性劑)、應用和來源(微生物來源、植物來源) - 全球預測(~2036年) 生物表面活性劑:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

生物表面活性劑:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 全球生物表面活性劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球生物表面活性劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球植物來源生物界面活性劑市場報告2026年全球生物界面活性劑市場報告

2026年全球植物來源生物界面活性劑市場報告2026年全球生物界面活性劑市場報告 生物界面活性劑市場-全球產業規模、佔有率、趨勢、機會及按類型、應用、地區和競爭格局分類的預測(2021-2031年)

生物界面活性劑市場-全球產業規模、佔有率、趨勢、機會及按類型、應用、地區和競爭格局分類的預測(2021-2031年) 生物界面活性劑市場規模、佔有率及成長分析(按產品類型、原料、應用及地區分類)-2026-2033年產業預測

生物界面活性劑市場規模、佔有率及成長分析(按產品類型、原料、應用及地區分類)-2026-2033年產業預測 全球可生物分解界面活性劑市場預測(至2032年):依產品類型、原料、應用、最終用戶及地區分類

全球可生物分解界面活性劑市場預測(至2032年):依產品類型、原料、應用、最終用戶及地區分類 日本生物界面活性劑市場報告:按產品、原料、應用和地區分類(2026-2034年)

日本生物界面活性劑市場報告:按產品、原料、應用和地區分類(2026-2034年)