|

市場調查報告書

商品編碼

1936546

乳房超音波市場機會、成長要素、產業趨勢分析及2026年至2035年預測Breast Ultrasound Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

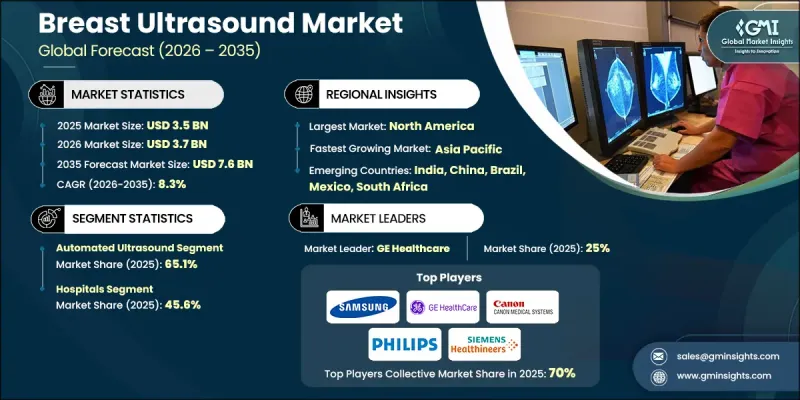

全球乳房超音波市場預計到 2025 年將達到 35 億美元,到 2035 年將達到 76 億美元,年複合成長率為 8.3%。

全球乳癌負擔日益加重、篩檢意識不斷提高、公共衛生政策支持以及超音波影像技術的持續創新,共同推動了市場成長。全球乳癌發生率的上升凸顯了早期檢測和精準診斷工具的重要性,直接增加了對乳房超音波系統的需求。這些系統因其非侵入性影像、無輻射暴露且適用於重複篩檢和後續觀察被廣泛採用。不斷擴大的宣傳活動和支持性醫療政策提高了常規篩檢的參與率,進一步增強了市場需求。對乳房健康的深入了解,以及診斷服務的日益普及,持續推動乳房超音波在醫療機構的應用。影像清晰度、自動化程度和診斷準確性的技術進步提高了臨床可靠性,並促進了乳房超音波在標準診斷流程中的廣泛應用。隨著醫療系統日益重視早期診斷和患者安全,乳房超音波仍然是支撐市場長期成長的關鍵影像解決方案。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 35億美元 |

| 預測金額 | 76億美元 |

| 複合年成長率 | 8.3% |

預計到2025年,自動化超音波市場規模將達到23億美元,佔市佔率的65.1%。自動化乳房超音波技術透過標準化掃描提供全面的影像,從而實現一致的影像品質和乳房組織的精細可視化。減少對操作者的依賴性以及提高診斷信心,並持續推動自動化系統在臨床應用中的普及。

醫院仍將是乳房超音波檢查的主要醫療場所,到 2024 年將佔 45.6% 的市場佔有率。這些機構提供先進的影像設備和綜合診斷服務,有助於在單一的醫療保健環境中進行準確的檢測、評估和後續觀察。

預計到2025年,北美乳腺超音波市場佔有率將達到34%。疾病盛行率上升、篩檢檢測普及率提高以及技術持續整合正在推動全部區域的需求成長。醫療機構越來越依賴先進的超音波解決方案來提高診斷準確性並減少解讀差異。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 產業影響因素

- 促進要素

- 全球乳癌發生率不斷上升

- 乳房超音波診斷設備的技術進步

- 對乳癌的認知提高以及政府的有利政策

- 改善美國乳房超音波篩檢的保險報銷

- 產業潛在風險與挑戰

- 自動乳房超音波設備高成本

- 發展中和低度開發地區缺乏技術熟練或訓練有素的勞動力

- 市場機遇

- 與遠端醫療的合作

- 促進要素

- 成長潛力分析

- 監管環境

- 技術進步

- 當前技術趨勢

- 新興技術

- 2024年定價分析

- 未來市場趨勢

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 重大進展

- 併購

- 合作夥伴關係和合資企業

- 新產品發布

- 擴張計劃

第5章 按類型分類的市場估算與預測,2022-2035年

- 常規超音波

- 自動超音波設備

6. 依最終用途分類的市場估計與預測,2022-2035 年

- 醫院

- 診斷檢查室

- 其他最終用戶

第7章 2022-2035年各地區市場估算與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第8章 公司簡介

- CapeRay

- Delphinus Medical Technologies, Inc.

- GE Healthcare

- Koninklijke Philips NV

- Siemens Healthineers AG

- Canon Medical Systems Corporation

- Fukuda Denshi

- Hologic, Inc.

- Seno Medical Instruments Inc.

- Shenzhen Mindray Bio-Medical Electronics Co., Ltd.

- Samsung Electronics Co. Ltd.

- FujiFilm Holdings Corporation

The Global Breast Ultrasound Market was valued at USD 3.5 billion in 2025 and is estimated to grow at a CAGR of 8.3% to reach USD 7.6 billion by 2035.

Market growth is supported by the rising global burden of breast cancer, increasing screening awareness, supportive public health initiatives, and continuous innovation in ultrasound imaging technologies. The growing incidence of breast cancer worldwide has intensified the need for early-stage detection and accurate diagnostic tools, directly increasing demand for breast ultrasound systems. These systems are widely adopted because they enable non-invasive imaging without radiation exposure, making them suitable for repeated screenings and follow-up evaluations. Expanded awareness programs and favorable healthcare policies have encouraged higher participation in routine screening, further strengthening market demand. Improved understanding of breast health, combined with broader access to diagnostic services, continues to drive adoption across healthcare settings. Technological improvements in image clarity, automation, and diagnostic accuracy are enhancing clinical confidence and supporting wider integration of breast ultrasound into standard diagnostic workflows. As healthcare systems place greater emphasis on early diagnosis and patient safety, breast ultrasound remains a critical imaging solution supporting long-term market growth.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.5 Billion |

| Forecast Value | $7.6 Billion |

| CAGR | 8.3% |

The automated ultrasound segment generated USD 2.3 billion in 2025 and accounted for a share of 65.1%. Automated breast ultrasound technology provides comprehensive imaging through standardized scanning, enabling consistent image quality and detailed visualization of breast tissue. Reduced operator dependency and enhanced diagnostic reliability continue to support strong adoption of automated systems in clinical practice.

The hospitals segment accounted for 45.6% share in 2024 and remains the leading care setting for breast ultrasound procedures. These facilities offer access to advanced imaging equipment and integrated diagnostic services, supporting accurate detection, evaluation, and follow-up within a single care environment.

North America Breast Ultrasound Market represented 34% share in 2025. Rising disease prevalence, strong screening adoption, and continuous technology integration are driving demand across the region. Healthcare providers increasingly rely on advanced ultrasound solutions to improve diagnostic confidence and reduce interpretation variability.

Key companies operating in the Global Breast Ultrasound Market include GE Healthcare, Siemens Healthineers AG, Koninklijke Philips N.V., Canon Medical Systems Corporation, Samsung Electronics Co. Ltd., Hologic, Inc., Fujifilm Holdings Corporation, Shenzhen Mindray Bio-Medical Electronics Co., Ltd., Delphinus Medical Technologies, Inc., CapeRay, Seno Medical Instruments Inc., Fukuda Denshi, and others. Companies in the breast ultrasound market strengthen their competitive position by investing in advanced imaging innovation, automation, and diagnostic accuracy. Many players focus on developing systems with improved resolution, workflow efficiency, and reduced operator variability. Strategic partnerships with healthcare providers and research institutions support clinical validation and market expansion. Firms also emphasize integration with digital health platforms and AI-assisted diagnostics to enhance detection capabilities. Expanding global distribution networks and offering comprehensive service and training programs help improve adoption.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Type trends

- 2.2.3 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing prevalence of breast cancer worldwide

- 3.2.1.2 Rising technological advancements in breast ultrasound systems

- 3.2.1.3 Rising awareness and favourable government initiatives regarding breast cancer

- 3.2.1.4 Increased reimbursement for breast ultrasound in the U.S.

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of the automated breast ultrasound system devices

- 3.2.2.2 Lack of skilled or trained personnel in the developing and underdeveloped region

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with Telemedicine

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis, 2024

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Conventional ultrasound

- 5.3 Automated ultrasound

Chapter 6 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Hospitals

- 6.3 Diagnostic Laboratories

- 6.4 Other end users

Chapter 7 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 CapeRay

- 8.2 Delphinus Medical Technologies, Inc.

- 8.3 GE Healthcare

- 8.4 Koninklijke Philips N.V.

- 8.5 Siemens Healthineers AG

- 8.6 Canon Medical Systems Corporation

- 8.7 Fukuda Denshi

- 8.8 Hologic, Inc.

- 8.9 Seno Medical Instruments Inc.

- 8.10 Shenzhen Mindray Bio-Medical Electronics Co., Ltd.

- 8.11 Samsung Electronics Co. Ltd.

- 8.12 FujiFilm Holdings Corporation

乳房超音波市場:按產品、檢查方法、技術、探頭類型、應用和最終用戶分類-2026-2032年全球市場預測自動化乳房超音波系統市場:按產品、影像技術、應用和最終用戶分類-2026-2032年全球市場預測

乳房超音波市場:按產品、檢查方法、技術、探頭類型、應用和最終用戶分類-2026-2032年全球市場預測自動化乳房超音波系統市場:按產品、影像技術、應用和最終用戶分類-2026-2032年全球市場預測 乳房超音波市場規模、佔有率和成長分析:按產品類型、技術、應用、最終用戶和地區分類-2026-2033年產業預測

乳房超音波市場規模、佔有率和成長分析:按產品類型、技術、應用、最終用戶和地區分類-2026-2033年產業預測 2026年全球乳房超音波市場報告

2026年全球乳房超音波市場報告 全球自動化乳房超音波系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球自動化乳房超音波系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 按產品類型、應用和地區分類的自動乳房超音波系統(ABUS)市場

按產品類型、應用和地區分類的自動乳房超音波系統(ABUS)市場 2026-2030年全球自動化乳房超音波系統(ABUS)市場

2026-2030年全球自動化乳房超音波系統(ABUS)市場 推車式傳統乳房超音波系統的全球市場

推車式傳統乳房超音波系統的全球市場 自動乳房超音波系統市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

自動乳房超音波系統市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 乳房自動超音波市場規模、佔有率、趨勢分析報告:按產品、最終用途、地區、細分市場預測,2024-2030 年

乳房自動超音波市場規模、佔有率、趨勢分析報告:按產品、最終用途、地區、細分市場預測,2024-2030 年