|

市場調查報告書

商品編碼

1936532

罕見疾病治療市場機會、成長要素、產業趨勢分析及2026年至2035年預測Rare Disease Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

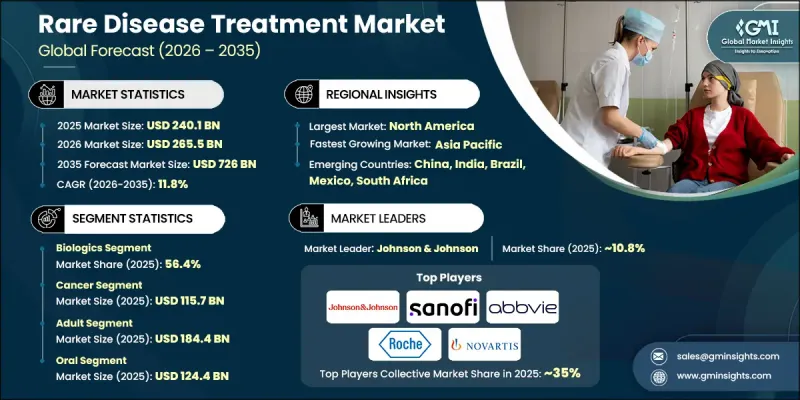

全球罕見疾病治療市場預計到 2025 年將達到 2,401 億美元,到 2035 年將達到 7,260 億美元,年複合成長率為 11.8%。

該市場專注於開發和商業化針對患者群體有限且存在顯著未滿足醫療需求的疾病的治療方法。罕見疾病治療涵蓋了在專門的監管路徑下開發的各種先進治療方法,並得到有利的政策獎勵和報銷體系的支持。精準醫療的持續進步和鼓勵創新的監管支持計劃不斷推動市場擴張。該行業越來越注重針對潛在生物學機制的緩解疾病和根治性療法,而不僅僅是症狀管理。分子科學和治療工程領域的創新正在改變治療效果和長期疾病管理。科學進步、以患者為中心的開發策略以及有利的法規環境的融合,持續推動全球醫藥和醫療保健市場的需求和投資。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 2401億美元 |

| 預測金額 | 7260億美元 |

| 複合年成長率 | 11.8% |

市場的一個顯著變化是向分子標靶和基因指導療法的轉變。先進的治療方法因其能夠提供持久的臨床療效並有可能改變疾病進展而備受關注。在基因組研究和精準診斷技術進步的支持下,個人化治療的開發日益普及。這些客製化療法在提高療效的同時,降低了副作用的風險,從而推動了罕見疾病整體管理到個人化護理模式的轉變。

2025年,生物製劑市佔率佔比達到56.4%,預計2026年至2035年將以11.7%的複合年成長率成長。由於其特異性和強大的治療效果,生物治療方法在應對複雜的生物學疾病方面發揮核心作用。標靶干預和安全性提升是推動生物製劑廣泛應用的關鍵因素。生物製藥研發的持續創新,包括基於患者個別數據的個人化治療,將進一步支持該領域的持續成長,並與精準醫療主導的醫療保健模式的更廣泛轉型相契合。

預計到2025年,成人患者市場規模將達到1,844億美元,到2035年將以11.7%的複合年成長率成長。由於疾病進展模式和診斷時機的特殊性,成人是全球最大的治療目標族群。雖然兒童市場規模相對小規模,但診斷技術的進步和早期檢測的普及正在推動其成長,對這兩個領域的持續投資確保了治療格局的不斷發展。

預計到2025年,北美將佔據罕見疾病治療市場41.1%的佔有率,憑藉其先進的醫療保健體系、強力的監管獎勵以及創新治療方法的快速普及,繼續保持主導地位。該地區受益於完善的研究基礎設施、精準醫療的早期應用以及對生物技術研發的大量投資。此外,支持性的健保報銷制度和積極的病患權益計劃也促進了全部區域持續的需求和市場的成熟。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 產業影響因素

- 促進要素

- 罕見病患疾病率不斷上升

- 精準醫療和生物技術的進步

- 支持性的法規結構和獎勵

- 提高公眾意識和早期診斷率

- 產業潛在風險與挑戰

- 高成本和有限的負擔能力

- 患者數量少且臨床試驗複雜

- 市場機遇

- 拓展至醫療基礎設施正在改善的新興市場

- 協作與數位健康整合

- 促進要素

- 成長潛力分析

- 科技趨勢

- 當前技術趨勢

- 新興技術

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 管道分析

- 未來市場趨勢

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章 依藥物類型分類的市場估算與預測,2022-2035年

- 生物製藥

- 非生物製藥

第6章 依治療領域分類的市場估計與預測,2022-2035年

- 癌症

- 血液相關疾病

- 中樞神經系統

- 呼吸系統疾病

- 肌肉骨骼疾病

- 循環系統疾病

- 其他治療領域

7. 按病患類型分類的市場估計與預測,2022-2035 年

- 成人版

- 兒童

8. 依行政途徑分類的市場估計與預測,2022-2035 年

- 口服

- 注射

- 其他給藥途徑

9. 依最終用途分類的市場估計與預測,2022-2035 年

- 醫院和診所

- 居家醫療環境

- 其他最終用戶

第10章 2022-2035年各地區市場估計與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- AbbVie

- Alexion Pharmaceuticals

- Amgen

- AstraZeneca

- Baxter International

- Bayer

- Bristol-Myers Squibb

- Eli Lilly and Company

- F. Hoffmann La Roche

- GlaxoSmithKline

- Johnson &Johnson

- Merck &Co.

- Novartis

- Novo Nordisk

- Pfizer

- Sanofi

- Takeda Pharmaceutical

- Vertex Pharmaceutical

The Global Rare Disease Treatment Market was valued at USD 240.1 billion in 2025 and is estimated to grow at a CAGR of 11.8% to reach USD 726 billion by 2035.

The market focuses on the development and commercialization of therapies designed to address conditions affecting limited patient populations but characterized by substantial unmet clinical needs. Rare disease treatments span a broad range of advanced therapeutic modalities developed under specialized regulatory pathways, supported by favorable policy incentives and reimbursement structures. Continued progress in precision medicine, along with regulatory support programs that encourage innovation, continues to accelerate market expansion. The industry is increasingly centered on disease-modifying and curative approaches that target underlying biological mechanisms rather than symptom management alone. Innovations in molecular science and therapeutic engineering are transforming treatment outcomes and long-term disease control. The convergence of scientific advancements, patient-focused development strategies, and supportive regulatory ecosystems continues to strengthen global demand and investment across pharmaceutical and healthcare markets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $240.1 Billion |

| Forecast Value | $726 Billion |

| CAGR | 11.8% |

A notable transformation within the market is the shift toward molecularly targeted and genetically informed therapies. Advanced therapeutic approaches are gaining traction as they offer durable clinical benefits and the potential to alter disease progression. Personalized treatment development has become increasingly prevalent, supported by advancements in genomic research and diagnostic precision. These tailored therapies enhance treatment effectiveness while reducing the risk of adverse reactions, reinforcing the transition toward individualized care models across rare disease management.

The biologics segment held 56.4% share in 2025 and is projected to grow at a CAGR of 11.7% during 2026-2035. These therapies play a central role in addressing complex biological conditions due to their specificity and strong therapeutic performance. Their ability to deliver targeted intervention with improved safety profiles has driven widespread adoption. Continued innovation in biologic development, including customization based on patient-level data, further supports sustained segment growth and aligns with the broader shift toward precision-driven healthcare.

The adult patient population generated reached USD 184.4 billion in 2025 and is expected to grow at a CAGR of 11.7% throughout 2035. Adults represent the largest treatment group globally due to disease progression patterns and diagnosis timelines. While the pediatric segment remains smaller in comparison, it continues to experience accelerated growth, supported by expanded diagnostic capabilities and earlier disease identification. The evolving treatment landscape ensures continued investment across both population segments.

North America Rare Disease Treatment Market accounted for 41.1% share in 2025, maintaining its leadership position due to advanced healthcare systems, strong regulatory incentives, and rapid adoption of innovative therapies. The region benefits from extensive research infrastructure, early integration of precision medicine, and substantial investment in biotechnology development. Supportive reimbursement structures and active patient advocacy further contribute to sustained demand and market maturity across the region.

Key companies operating in the Global Rare Disease Treatment Market include Novartis, Pfizer, Sanofi, Vertex Pharmaceutical, Takeda Pharmaceutical, Bristol-Myers Squibb, AstraZeneca, Merck & Co., AbbVie, Bayer, Novo Nordisk, GlaxoSmithKline, Eli Lilly and Company, Johnson & Johnson, Amgen, Alexion Pharmaceuticals, Baxter International, and F. Hoffmann La Roche. These organizations maintain strong positions through innovation-driven pipelines and long-term investment strategies. To reinforce their foothold, companies in the rare disease treatment sector are prioritizing sustained investment in research and development focused on high-value, disease-modifying therapies. Strategic collaborations, licensing agreements, and acquisitions are widely used to expand therapeutic pipelines and accelerate commercialization timelines. Firms are also leveraging precision medicine platforms to develop targeted treatments that address specific patient subgroups.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Drug type trends

- 2.2.3 Therapeutic area trends

- 2.2.4 Patient trends

- 2.2.5 Route of administration trends

- 2.2.6 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of rare diseases

- 3.2.1.2 Advancements in precision medicine and biotechnology

- 3.2.1.3 Supportive regulatory frameworks and incentives

- 3.2.1.4 Growing awareness and early diagnosis rates

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost and limited affordability

- 3.2.2.2 Small patient populations and clinical trial complexity

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into emerging markets with improving healthcare infrastructure

- 3.2.3.2 Collaborations and digital health integration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.2 Europe

- 3.5.3 Asia Pacific

- 3.6 Pipeline analysis

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Drug Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Biologics

- 5.3 Non-biologics

Chapter 6 Market Estimates and Forecast, By Therapeutic Area, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Cancer

- 6.3 Blood-related disorders

- 6.4 Central nervous system

- 6.5 Respiratory disorders

- 6.6 Musculoskeletal disorders

- 6.7 Cardiovascular disorders

- 6.8 Other therapeutic areas

Chapter 7 Market Estimates and Forecast, By Patient, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Adult

- 7.3 Pediatric

Chapter 8 Market Estimates and Forecast, By Route of Administration, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Oral

- 8.3 Injectable

- 8.4 Other routes of administration

Chapter 9 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals and clinics

- 9.3 Homecare settings

- 9.4 Other end users

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 AbbVie

- 11.2 Alexion Pharmaceuticals

- 11.3 Amgen

- 11.4 AstraZeneca

- 11.5 Baxter International

- 11.6 Bayer

- 11.7 Bristol-Myers Squibb

- 11.8 Eli Lilly and Company

- 11.9 F. Hoffmann La Roche

- 11.10 GlaxoSmithKline

- 11.11 Johnson & Johnson

- 11.12 Merck & Co.

- 11.13 Novartis

- 11.14 Novo Nordisk

- 11.15 Pfizer

- 11.16 Sanofi

- 11.17 Takeda Pharmaceutical

- 11.18 Vertex Pharmaceutical

罕見疾病治療市場:依治療方法、治療領域、給藥途徑、疾病、最終用戶、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測

罕見疾病治療市場:依治療方法、治療領域、給藥途徑、疾病、最終用戶、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測 α-甘露醣儲積症症市場:2026年至2032年全球市場預測(依治療方法、適應症、診斷方法及最終用戶分類)Lennox-Gastaut症候群治療市場:依給藥途徑、治療方法、患者年齡層、藥物類別及最終用戶分類-2026-2032年全球市場預測犬庫欣氏症治療市場依藥物類別、治療類型、給藥途徑及通路分類,全球預測(2026-2032年)

α-甘露醣儲積症症市場:2026年至2032年全球市場預測(依治療方法、適應症、診斷方法及最終用戶分類)Lennox-Gastaut症候群治療市場:依給藥途徑、治療方法、患者年齡層、藥物類別及最終用戶分類-2026-2032年全球市場預測犬庫欣氏症治療市場依藥物類別、治療類型、給藥途徑及通路分類,全球預測(2026-2032年) 罕見疾病治療市場分析及預測(至2035年):依類型、產品類型、服務、技術、應用、最終使用者、設備、流程、解決方案及階段分類

罕見疾病治療市場分析及預測(至2035年):依類型、產品類型、服務、技術、應用、最終使用者、設備、流程、解決方案及階段分類 罕見疾病治療市場規模、佔有率和成長分析(按治療領域、藥物類型、給藥途徑、患者類型、分銷管道和地區分類)-2026-2033年產業預測

罕見疾病治療市場規模、佔有率和成長分析(按治療領域、藥物類型、給藥途徑、患者類型、分銷管道和地區分類)-2026-2033年產業預測 全球罕見疾病治療市場:預測至2032年-依藥物類型、治療類型、給藥途徑、治療領域、通路、最終使用者和地區進行分析

全球罕見疾病治療市場:預測至2032年-依藥物類型、治療類型、給藥途徑、治療領域、通路、最終使用者和地區進行分析 酸性鞘神經磷脂酶缺乏症市場 - 全球及區域 - 分析與預測(2025-2035)愛德華茲症候群治療市場預測(至 2032 年):按治療類型、類型、最終用戶和地區進行的全球分析罕見疾病治療市場,按治療領域、按藥物類型、按給藥方式、按配銷通路、按患者年齡層、按國家/地區 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率及預測

酸性鞘神經磷脂酶缺乏症市場 - 全球及區域 - 分析與預測(2025-2035)愛德華茲症候群治療市場預測(至 2032 年):按治療類型、類型、最終用戶和地區進行的全球分析罕見疾病治療市場,按治療領域、按藥物類型、按給藥方式、按配銷通路、按患者年齡層、按國家/地區 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率及預測