|

市場調查報告書

商品編碼

1936515

汽車傳動軸市場機會、成長要素、產業趨勢分析及2026年至2035年預測Automotive Drive Shaft Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

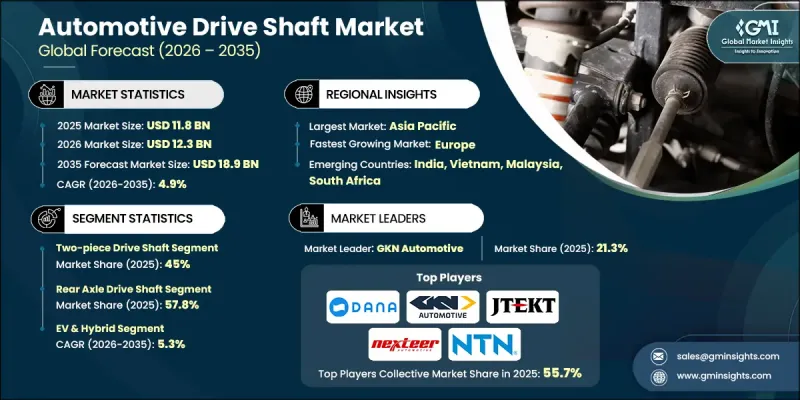

全球汽車傳動軸市場預計到 2025 年將達到 118 億美元,到 2035 年將達到 189 億美元,年複合成長率為 4.9%。

市場成長與全球乘用車和商用車產量的成長密切相關。隨著汽車產量的增加,對關鍵傳動系統零件的需求也隨之成長,這使得傳動軸成為現代汽車製造的關鍵要素。這些部件在動力傳輸中發揮著至關重要的作用,是車輛傳動系統和變速系統不可或缺的一部分。汽車產業電氣化程度的不斷提高進一步推動了市場成長動能。電動和混合動力汽車平台需要專門設計的傳動軸來適應其獨特的扭力特性和緊湊的動力傳動系統佈局。傳統汽車和電動車產量的持續成長正在增強長期需求。為應對監管壓力和效率目標,汽車製造商優先考慮輕量化,這加速了傳動系統零件的技術創新。同時,售後市場也為市場擴張做出了重大貢獻。老舊車輛的替換零件需求維持了對傳統和先進傳動軸解決方案的需求。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 118億美元 |

| 預測金額 | 189億美元 |

| 複合年成長率 | 4.9% |

製造商正加速向輕量化結構轉型,採用能夠提升效率和車輛動態性能的替代材料。減輕零件重量有助於提高燃油經濟性和性能,同時也有助於滿足排放氣體法規的要求。在對效率要求嚴格的地區,這些尖端材料的應用尤其普遍。隨著車輛使用壽命的延長,售後市場也持續受益,推動了各種材料類型的零件的穩定更換需求。

截至2025年,兩段式傳動軸市佔率達45%,市場規模達53億美元。這種設計廣泛應用於需要較長傳動軸的車輛,尤其是在高需求的實用型和商用車領域。其模組化設計使其易於安裝、操作簡單、維護高效,進而在全球市場廣受歡迎。

預計到2025年,後軸傳動軸細分市場將佔據57.8%的市場佔有率,到2035年市場規模將達到103億美元。後輪驅動和全輪驅動架構在多個車型類別中的廣泛應用持續支撐著市場需求。後軸結構具有結構優勢,設計複雜度更低,使其成為重型車輛的首選,尤其是在對實用型交通工具需求旺盛的地區。

預計到2025年,美國汽車傳動軸市場規模將達到12.8億美元。美國本土製造商持續採用尖端材料和精密生產技術,以提高傳動軸的強度重量比和整體效率。燃油效率和減排的監管壓力仍然是影響零件設計和材料選擇的關鍵因素。

目錄

第1章調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段的附加價值

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 促進要素

- 全球汽車產量和銷售成長

- 電池式電動車(BEV)中的電力驅動橋整合

- 採用輕量材料提高燃油效率

- 向後輪驅動和全輪驅動(AWD)SUV的轉變

- 產業潛在風險與挑戰

- 市場飽和和激烈的價格競爭

- 內燃機乘用車的銷量正在下降

- 市場機遇

- 為電動和混合動力汽車製化傳動軸

- 碳纖維複合材料技術的商業化

- 新興國家售後市場的成長

- 非洲和拉丁美洲尚未開發的市場

- 促進要素

- 成長潛力分析

- 監管環境

- 北美洲

- 美國國家公路交通安全管理局(NHTSA)

- 美國環保署(EPA)

- 美國汽車工程師協會(SAE International)

- 加拿大運輸部

- 職業安全與健康管理局(OSHA)

- 歐洲

- 歐盟委員會(EC)

- 歐洲汽車製造商協會 (ACEA)

- 歐洲標準化委員會(CEN)

- 亞太地區

- 國土交通省

- 中華人民共和國工業與資訊化部(工信部)

- 印度汽車研究協會(ARAI)

- 拉丁美洲

- 國家計量、品質和技術研究院(INMETRO)

- 墨西哥經濟部秘書處(SE)

- 阿根廷國家交通安全局(ANTSV)

- 中東和非洲

- 海灣合作理事會標準組織(GSO)

- 南非標準局 (SABS)

- 沙烏地阿拉伯標準、計量和品質組織(SASO)

- 北美洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 生產統計

- 生產基地

- 消費基礎

- 出口和進口

- 成本細分分析

- 永續性和環境影響

- 環境影響評估

- 社會影響力和社區服務

- 公司管治與企業社會責任

- 永續金融與投資趨勢

- 產品生命週期分析

- 傳動軸生命週期階段

- 按材料生命週期

- 失效模式和生命週期限制因素

- 預測性維護和生命週期延長

- 報廢車輛的處置與回收

- 電動車和混合動力汽車的影響分析

- 電動車動力傳動系統架構及其對傳動軸的影響

- 電動車專用傳動軸要求

- 混合動力汽車傳動軸的複雜性

- 不斷變化的競爭格局

- 案例研究

- OEM傳動系統架構映射

- 傳動系統部件的系統級交互

- NVH性能和車輛動力學的基準

- 售後市場故障模式及更換經濟性

- 未來前景與機遇

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 企業擴張計畫和資金籌措

第5章 市場估計與預測:依軸分類,2022-2035年

- 單驅動軸

- 兩段式傳動軸

- 滑入式管路驅動軸

第6章 按職位分類的市場估算與預測,2022-2035年

- 前橋驅動軸

- 後軸驅動軸

7. 按設計結構分類的市場估算與預測,2022-2035 年

- 中空傳動軸

- 剛性/實心驅動軸

第8章 按材料分類的市場估算與預測,2022-2035年

- 鋼材

- 鋁

- 碳纖維

第9章 依車輛類型分類的市場估計與預測,2022-2035年

- 搭乘用車

- SUV

- 轎車

- 掀背車

- 商用車輛

- 輕型商用車(LCV)

- MCV

- 重型商用車(HCV)

- 摩托車

第10章 2022-2035年按推進方式分類的市場估計與預測

- 內燃機(ICE)

- 電動車和混合動力汽車

- 電池式電動車(BEV)

- 混合動力電動車(HEV)

- 插電式混合動力車(PHEV)

第11章 依銷售管道分類的市場估計與預測,2022-2035年

- OEM

- 售後市場

第12章 2022-2035年各地區市場估算與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 捷克共和國

- 比利時

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 新加坡

- 馬來西亞

- 印尼

- 越南

- 泰國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥倫比亞

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第13章:公司簡介

- 世界玩家

- GKN Automotive

- Dana

- American Axle &Manufacturing(AAM)

- NTN

- Nexteer

- JTEKT

- Hyundai WIA

- IFA

- Neapco

- Schaeffler

- 本地製造商

- Wanxiang Qianchao

- Xuchang Yuandong Driveshaft

- 歐洲軌道交通

- EDS-ALL DRIVESHAFT

- GuangZhou JunChi AutoParts

- Drexler Automotive

- Dorman Products

- Quigley

- 新興製造商

- GSP Automotive

- The Timken

- Comer Industries

- GNA Drivelines

- Schaeffler

- Elbe

- Amalga Composites

The Global Automotive Drive Shaft Market was valued at USD 11.8 billion in 2025 and is estimated to grow at a CAGR of 4.9% to reach USD 18.9 billion by 2035.

Market growth is tied to rising global vehicle production across passenger and commercial categories. As vehicle output increases, demand for essential drivetrain components continues to rise, positioning drive shafts as a critical element in modern automotive architecture. These components play a vital role in power transmission, making them indispensable to vehicle driveline and transmission systems. Expanding electrification across the automotive industry further supports market momentum, as electric and hybrid platforms require drive shafts engineered to manage distinct torque profiles and compact powertrain layouts. Continued growth in both conventional and electrified vehicle manufacturing reinforces long-term demand. Automakers are also responding to regulatory pressure and efficiency targets by prioritizing weight reduction, which is accelerating innovation across drivetrain components. In parallel, the aftermarket segment contributes significantly to market expansion as aging vehicles require replacement parts, sustaining consistent demand for both traditional and advanced drive shaft solutions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $11.8 Billion |

| Forecast Value | $18.9 Billion |

| CAGR | 4.9% |

Manufacturers are increasingly shifting toward lightweight construction by adopting alternative materials that improve efficiency and vehicle dynamics. Reduced component weight enhances fuel economy and performance while supporting compliance with emissions standards. Adoption of these advanced materials is particularly strong in regions with stringent efficiency requirements. The aftermarket continues to benefit from vehicle longevity, driving steady replacement demand across diverse material types.

The two-piece drive shafts segment held 45% share in 2025 and generated USD 5.3 billion. This configuration is widely adopted in vehicles requiring extended driveline lengths, particularly in higher-demand utility and commercial segments. Modular construction supports easier installation, simplified handling, and more efficient maintenance, contributing to its widespread acceptance across global markets.

The rear axle drive shafts segment accounted for 57.8% share in 2025 and is projected to reach USD 10.3 billion by 2035. Strong adoption of rear-wheel and all-wheel drive architectures across multiple vehicle categories continues to support demand. Rear axle configurations offer structural advantages and reduced engineering complexity, making them a preferred choice in larger vehicles, particularly in regions with strong demand for utility-focused transportation.

U.S. Automotive Drive Shaft Market reached USD 1.28 billion in 2025. Domestic manufacturers continue to adopt advanced materials and refined production techniques to enhance strength-to-weight ratios and overall efficiency. Regulatory pressure related to fuel efficiency and emissions reduction remains a key driver influencing component design and material selection.

Major companies operating in the Global Automotive Drive Shaft Market include GKN Automotive, Dana, American Axle & Manufacturing, NTN, Nexteer Automotive, Neapco, JTEKT, Hyundai WIA, Wanxiang Qianchao, and IFA. To strengthen their foothold, companies in the automotive drive shaft industry focus on material innovation, production efficiency, and strategic partnerships with vehicle manufacturers. Investment in lightweight engineering enables compliance with efficiency standards while improving performance. Portfolio diversification across vehicle types and drivetrain architectures allows suppliers to serve both conventional and electrified platforms. Expansion of aftermarket offerings supports recurring revenue streams. Manufacturers also prioritize automation and precision manufacturing to enhance quality and reduce costs.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Shaft

- 2.2.3 Position

- 2.2.4 Design Structure

- 2.2.5 Material

- 2.2.6 Vehicle

- 2.2.7 Propulsion

- 2.2.8 Sales Channel

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing global vehicle production & sales

- 3.2.1.2 E-axle integration in battery electric vehicles (BEVs)

- 3.2.1.3 Lightweight material adoption for fuel efficiency

- 3.2.1.4 Shift toward rear-wheel & all-wheel-drive (AWD) SUVs

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Market saturation & intense price competition

- 3.2.2.2 Declining internal combustion engine (ICE) passenger car sales

- 3.2.3 Market opportunities

- 3.2.3.1 Electric & hybrid vehicle drive shaft customization

- 3.2.3.2 Carbon fiber composite technology commercialization

- 3.2.3.3 Aftermarket growth in emerging economies

- 3.2.3.4 White-space markets in Africa & Latin America

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 National Highway Traffic Safety Administration (NHTSA)

- 3.4.1.2 EPA (Environmental Protection Agency)

- 3.4.1.3 Society of Automotive Engineers (SAE International)

- 3.4.1.4 Transport Canada

- 3.4.1.5 Occupational Safety and Health Administration (OSHA)

- 3.4.2 Europe

- 3.4.2.1 European Commission (EC)

- 3.4.2.2 European Automobile Manufacturers’ Association (ACEA)

- 3.4.2.3 European Committee for Standardization (CEN)

- 3.4.3 Asia Pacific

- 3.4.3.1 Ministry of Land, Infrastructure, Transport and Tourism (MLIT), Japan

- 3.4.3.2 Ministry of Industry and Information Technology (MIIT), China

- 3.4.3.3 Automotive Research Association of India (ARAI)

- 3.4.4 Latin America

- 3.4.4.1 National Institute of Metrology, Quality and Technology (INMETRO)

- 3.4.4.2 Secretariat of Economy (SE), Mexico

- 3.4.4.3 National Traffic Safety Agency (ANTSV), Argentina

- 3.4.5 Middle East & Africa

- 3.4.5.1 GCC Standardization Organization (GSO)

- 3.4.5.2 South African Bureau of Standards (SABS)

- 3.4.5.3 Saudi Standards, Metrology and Quality Organization (SASO)

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Sustainability and environmental impact

- 3.11.1 Environmental impact assessment

- 3.11.2 Social impact & community benefits

- 3.11.3 Governance & corporate responsibility

- 3.11.4 Sustainable finance & investment trends

- 3.12 Product lifecycle analysis

- 3.12.1 Drive shaft lifecycle stages

- 3.12.2 Lifecycle by material

- 3.12.3 Failure modes & lifecycle limiting factors

- 3.12.4 Predictive maintenance & lifecycle extension

- 3.12.5 End-of-life disposal & recycling

- 3.13 Electric & Hybrid Vehicle Impact Analysis

- 3.13.1 EV Drivetrain Architecture & Drive Shaft Implications

- 3.13.2 EV-Specific Drive Shaft Requirements

- 3.13.3 Hybrid Vehicle Drive Shaft Complexity

- 3.13.4 Competitive Landscape Transformation

- 3.14 Case studies

- 3.15 OEM drivetrain architecture mapping

- 3.16 System-level driveline component interaction

- 3.17 NVH Performance & Vehicle Dynamics Benchmarking

- 3.18 Aftermarket Failure Modes & Replacement Economics

- 3.19 Future outlook & opportunities

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Shaft, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Single-Piece Drive Shaft

- 5.3 Two-Piece Drive Shaft

- 5.4 Slip-in-Tube Drive Shaft

Chapter 6 Market Estimates & Forecast, By Position, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Front Axle Drive Shaft

- 6.3 Rear Axle Drive Shaft

Chapter 7 Market Estimates & Forecast, By Design Structure, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Hollow Drive Shaft

- 7.3 Rigid/Solid Drive Shaft

Chapter 8 Market Estimates & Forecast, By Material, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Steel

- 8.3 Aluminum

- 8.4 Carbon Fiber

Chapter 9 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 Passenger cars

- 9.2.1 SUV

- 9.2.2 Sedan

- 9.2.3 Hatchback

- 9.3 Commercial vehicles

- 9.3.1 LCV

- 9.3.2 MCV

- 9.3.3 HCV

- 9.4 Two wheelers

Chapter 10 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 Internal Combustion Engine (ICE)

- 10.3 EV & Hybrid

- 10.3.1 Battery Electric Vehicle (BEV)

- 10.3.2 Hybrid Electric Vehicle (HEV)

- 10.3.3 Plug-in Hybrid Electric Vehicle (PHEV)

Chapter 11 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Bn, Units)

- 11.1 Key trends

- 11.2 Original Equipment Manufacturer (OEM)

- 11.3 Aftermarket

Chapter 12 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 US

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Russia

- 12.3.7 Czech Republic

- 12.3.8 Belgium

- 12.3.9 Netherlands

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 South Korea

- 12.4.5 Australia

- 12.4.6 Singapore

- 12.4.7 Malaysia

- 12.4.8 Indonesia

- 12.4.9 Vietnam

- 12.4.10 Thailand

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.5.4 Colombia

- 12.6 MEA

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 Global players

- 13.1.1 GKN Automotive

- 13.1.2 Dana

- 13.1.3 American Axle & Manufacturing (AAM)

- 13.1.4 NTN

- 13.1.5 Nexteer

- 13.1.6 JTEKT

- 13.1.7 Hyundai WIA

- 13.1.8 IFA

- 13.1.9 Neapco

- 13.1.10 Schaeffler

- 13.2 Regional players

- 13.2.1 Wanxiang Qianchao

- 13.2.2 Xuchang Yuandong Driveshaft

- 13.2.3 TrakMotive Europe

- 13.2.4 EDS - ALL DRIVESHAFT

- 13.2.5 GuangZhou JunChi AutoParts

- 13.2.6 Drexler Automotive

- 13.2.7 Dorman Products

- 13.2.8 Quigley

- 13.3 Emerging players

- 13.3.1 GSP Automotive

- 13.3.2 The Timken

- 13.3.3 Comer Industries

- 13.3.4 GNA Drivelines

- 13.3.5 Schaeffler

- 13.3.6 Elbe

- 13.3.7 Amalga Composites

全球汽車傳動軸市場:市場規模、佔有率、趨勢和成長分析(2026-2034)

全球汽車傳動軸市場:市場規模、佔有率、趨勢和成長分析(2026-2034) 汽車傳動軸市場 - 全球產業規模、佔有率、趨勢、機會、預測:按設計類型、位置類型、車輛類型、地區和競爭格局分類,2021-2031年

汽車傳動軸市場 - 全球產業規模、佔有率、趨勢、機會、預測:按設計類型、位置類型、車輛類型、地區和競爭格局分類,2021-2031年 汽車傳動軸市場:按車輛類型、材質、應用和最終用戶分類-2026-2032年全球市場預測

汽車傳動軸市場:按車輛類型、材質、應用和最終用戶分類-2026-2032年全球市場預測 汽車傳動軸市場規模、佔有率、趨勢和預測:按傳動軸類型、設計類型、安裝位置、材質、車輛類型、銷售管道和地區分類,2026-2034年

汽車傳動軸市場規模、佔有率、趨勢和預測:按傳動軸類型、設計類型、安裝位置、材質、車輛類型、銷售管道和地區分類,2026-2034年 2026年全球汽車傳動軸市場報告

2026年全球汽車傳動軸市場報告 汽車傳動軸市場:依驅動系統、車輛類型、銷售管道和地區分類。

汽車傳動軸市場:依驅動系統、車輛類型、銷售管道和地區分類。 汽車傳動軸:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)電機軸市場按應用、類型、材料、直徑範圍、塗層、銷售管道和最終用途行業分類,全球預測(2026-2032年)

汽車傳動軸:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)電機軸市場按應用、類型、材料、直徑範圍、塗層、銷售管道和最終用途行業分類,全球預測(2026-2032年) 汽車傳動軸市場規模、佔有率和成長分析(按設計類型、地點類型、車輛類型、銷售管道和地區分類)-2026-2033年產業預測軸帶式發電機市場-2025年至2030年預測

汽車傳動軸市場規模、佔有率和成長分析(按設計類型、地點類型、車輛類型、銷售管道和地區分類)-2026-2033年產業預測軸帶式發電機市場-2025年至2030年預測