|

市場調查報告書

商品編碼

1936498

農散貨船裝卸設備市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)Agri-bulk Ship Loading and Unloading Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

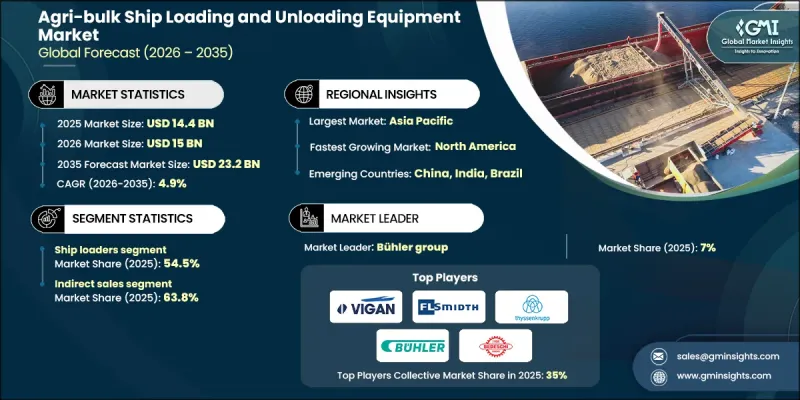

全球農產品散裝卸設備市場預計到 2025 年將達到 144 億美元,到 2035 年將達到 232 億美元,年複合成長率為 4.9%。

港口和散貨碼頭向自動化和機械化解決方案的轉型正在推動市場需求,傳統的人工和重力系統已無法滿足高吞吐量農產品出口的需求。現代化的連續船舶裝卸裝置(CSU)正作為一種環保解決方案嶄露頭角,它採用封閉式輸送系統、除塵技術和再生煞車技術,可降低高達30-40%的能耗,符合全球永續性目標。北美、歐洲和亞太地區對港口基礎設施、糧食轉運設施和工業海運樞紐的投資正在推動CSU的普及。技術升級是關鍵的市場趨勢,因為糧食貿易商和碼頭營運商越來越傾向於採用能夠提高生產效率、最大限度減少產品損失並簡化營運的高容量自動化系統。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始金額 | 144億美元 |

| 預測金額 | 232億美元 |

| 複合年成長率 | 4.9% |

2025年,船舶裝卸設備市場收入達78億美元,佔54.5%的市場。船舶裝卸設備因其能夠提高吞吐量、縮短船舶週轉時間並提升作業安全性而被廣泛採用。伸縮式溜槽、自動定位和抑塵技術等整合功能提高了效率和可靠性。該領域的領先地位反映了該行業正持續向高容量出口碼頭和先進的船舶貨物裝卸解決方案轉型,旨在最大限度地提高性能,同時最大限度地減少對環境的影響。

到2025年,間接銷售通路將佔市場佔有率的63.8%,凸顯了市場對區域經銷商和工程服務提供者的依賴。這種分銷模式有助於快速更換關鍵零件和簽訂本地維護契約,尤其是在收穫尖峰時段。透過這些管道,港口營運商可以獲得本地技術專長,從而確保其複雜設備的持續運作和及時支援。

預計到2025年,美國農產品散裝裝卸設備市場將佔據64.4%的市場佔有率,這主要得益於糧食出口基礎設施投資和港口物流現代化帶來的強勁需求。環保合規、粉塵控制和能源效率是影響採購決策的關鍵因素。隨著營運商在遵守日益嚴格的環保法規的同時,致力於提高營運吞吐量,美國市場將持續成長。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段的附加價值

- 影響價值鏈的因素

- 產業影響因素

- 成長促進因素

- 全球糧食安全與糧食貿易擴張

- 智慧港口概念及自動化

- 環境法規和粉塵控制

- 產業潛在風險與挑戰

- 高昂的初始資本支出(CAPEX)和基礎設施成本

- 現有泊位維修的複雜性

- 機會

- 數位雙胞胎和預測性維護

- 數位雙胞胎和預測性維護

- 成長促進因素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 按類型

- 監管環境

- 標準和合規要求

- 區域法規結構

- 認證標準

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章 按類型分類的市場估算與預測,2022-2035年

- 手動的

- 自動的

- 半自動

第6章 按分銷管道分類的市場估算與預測,2022-2035年

- 直接地

- 間接

第7章 2022-2035年各地區市場估算與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第8章:公司簡介

- AGI(Ag Growth International)

- AUMUND Group

- Bedeschi Spa

- Buhler Group

- Cargotec(MacGregor)

- Ems-tech Inc.

- FLSmidth

- Konecranes

- Liebherr-International AG

- NEUERO Industrietechnik GmbH

- PNM Bulk Handling

- Siwertell AB

- Thyssenkrupp AG

- VIGAN Engineering SA

- WAMGROUP SpA

The Global Agri-bulk Ship Loading and Unloading Equipment Market was valued at USD 14.4 billion in 2025 and is estimated to grow at a CAGR of 4.9% to reach USD 23.2 billion by 2035.

Demand is fueled by a shift toward automated and mechanized solutions in ports and bulk terminals, as traditional manual operations and gravity-fed systems become less viable for high-throughput agricultural exports. Modern continuous ship unloaders (CSUs) are emerging as a greener solution, incorporating closed conveyor systems, dust suppression, and regenerative braking technology, which can reduce energy consumption by up to 30-40%, aligning with global sustainability goals. Investment in port infrastructure, grain transfer facilities, and industrial maritime hubs is driving adoption across North America, Europe, and Asia-Pacific. Grain traders and terminal operators increasingly prefer high-capacity, automated systems that enhance productivity, minimize product loss, and streamline operations, making technological upgrades a central market trend.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $14.4 Billion |

| Forecast Value | $23.2 Billion |

| CAGR | 4.9% |

In 2025, the ship loaders segment generated USD 7.8 billion and capturing 54.5% share. Ship loaders are preferred for their ability to increase throughput, reduce vessel turnaround times, and enhance operational safety. Integration of features like telescopic chutes, automated positioning, and dust suppression technology has improved efficiency and reliability. The segment's dominance reflects the industry's ongoing shift toward high-capacity export terminals and advanced maritime handling solutions designed to maximize performance while minimizing environmental impact.

The indirect sales segment accounted for 63.8% share in 2025, highlighting the market's reliance on regional distributors and engineering service providers. This distribution model supports rapid replacement of critical components and on-site maintenance contracts, particularly during peak harvest seasons. Port operators rely on these channels to access localized technical expertise, ensuring uninterrupted operations and timely support for complex equipment.

U.S. Agri-bulk Ship Loading and Unloading Equipment Market held a 64.4% share in 2025, generating substantial demand through investments in grain export infrastructure and modernized port logistics. Environmental compliance, dust control measures, and energy efficiency are major factors shaping procurement decisions. The U.S. market continues to grow as operators focus on improving operational throughput while adhering to stricter environmental regulations.

Leading players in the Global Agri-bulk Ship Loading and Unloading Equipment Market include AGI (Ag Growth International), AUMUND Group, Bedeschi S.p.a., Buhler Group, Cargotec (MacGregor), Ems-tech Inc., FLSmidth, Konecranes, Liebherr-International AG, NEUERO Industrietechnik GmbH, PNM Bulk Handling, Siwertell AB, Thyssenkrupp AG, VIGAN Engineering S.A., and WAMGROUP S.p.A. Companies in Agri-bulk Ship Loading and Unloading Equipment Market are strengthening their presence through several strategies. They are investing in R&D to develop more energy-efficient, dust-free, and automated shiploader and unloader systems. Strategic partnerships with ports, grain terminals, and distributors enable better regional coverage and faster delivery of service contracts. Firms are expanding manufacturing capacities across Europe, North America, and Asia-Pacific to meet rising demand and reduce lead times. Additionally, companies are offering lifecycle services, predictive maintenance solutions, and modular system upgrades, which increase customer loyalty and reinforce long-term market positioning.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Distribution Channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Global food security and grain trade expansion

- 3.2.1.2 Smart port initiatives and automation

- 3.2.1.3 Environmental regulations and dust control

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High Initial CAPEX & infrastructure costs

- 3.2.2.2 Complexity of retrofitting existing berths

- 3.2.3 Opportunities

- 3.2.3.1 Digital twins and predictive maintenance

- 3.2.3.2 Digital twins and predictive maintenance

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By Type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Manual

- 5.3 Automatic

- 5.4 Semi-automatic

Chapter 6 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Direct

- 6.3 Indirect

Chapter 7 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Spain

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 AGI (Ag Growth International)

- 8.2 AUMUND Group

- 8.3 Bedeschi S.p.a.

- 8.4 Buhler Group

- 8.5 Cargotec (MacGregor)

- 8.6 Ems-tech Inc.

- 8.7 FLSmidth

- 8.8 Konecranes

- 8.9 Liebherr-International AG

- 8.10 NEUERO Industrietechnik GmbH

- 8.11 PNM Bulk Handling

- 8.12 Siwertell AB

- 8.13 Thyssenkrupp AG

- 8.14 VIGAN Engineering S.A.

- 8.15 WAMGROUP S.p.A