|

市場調查報告書

商品編碼

1936481

車載輔助系統市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)In-Vehicle Assistant Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

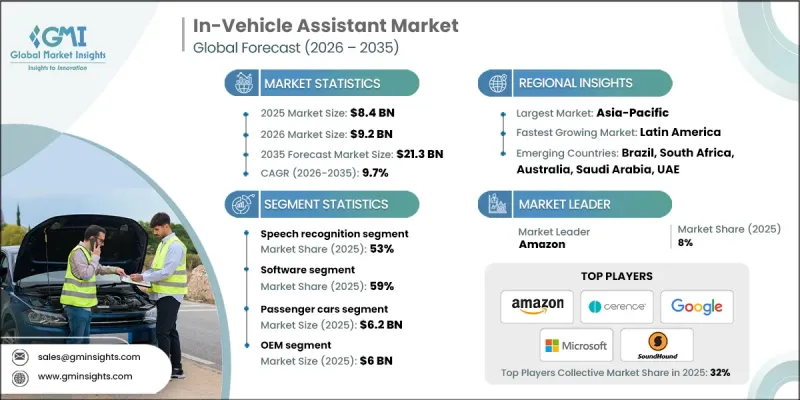

全球車載助手市場預計到 2025 年將達到 84 億美元,到 2035 年將達到 213 億美元,年複合成長率為 9.7%。

市場擴張的驅動力來自消費者對安全、便利、免手動駕駛的需求不斷成長,以及汽車製造商(OEM)大力推廣電動和自動駕駛汽車。隨著汽車製造商將語音、觸控手勢輸入整合到聯網汽車中,多模態人機介面(HMI)的出現正在推動產業轉型。大規模語言模型(LLM)協助開發更聰明的平台和設備,實現直覺的駕駛交互,並促進其在從豪華車到入門級車等各種車型中的應用。儘管新冠疫情暫時擾亂了汽車生產並推遲了新車上市,但對聯網汽車和智慧汽車技術的持續投資支撐了對整合語音助理和先進車載數位體驗的強勁長期需求。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始金額 | 84億美元 |

| 預測金額 | 213億美元 |

| 複合年成長率 | 9.7% |

預計到2025年,語音辨識市佔率將達到53%,並在2026年至2035年間以8.7%的複合年成長率成長。這項技術是車載輔助系統的核心,它透過自動語音辨識(ASR)演算法將麥克風擷取的語音訊號轉換為可執行的文字。收入來源包括汽車專用ASR軟體、波束成形麥克風以及專用於音訊處理的數位訊號處理(DSP)晶片的授權許可。

預計到2025年,軟體領域將佔據59%的市場佔有率,並在2035年之前以8.2%的複合年成長率成長。軟體平台包括基於雲端的自然語言處理、語音辨識引擎、軟體更新管理系統以及用於整合第三方應用程式的API。許可模式多種多樣,傳統供應商通常提供基於車輛的訂閱合約。

預計到2025年,中國車載助手市場規模將達26億美元。中國年產汽車超過3000萬輛,政府的「新基建政策」和「智慧城市規劃」等措施正在加速汽車互聯化進程。強制推行語音緊急呼叫系統以及為先進聯網汽車提供專款的法規,進一步鞏固了市場成長動能。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 零件供應商

- 技術平台提供者

- 系統整合商

- 汽車製造商

- 售後市場經銷商

- 最終用戶

- 成本結構

- 利潤率

- 在每個階段創造附加價值

- 垂直整合趨勢

- 顛覆者

- 供應商情況

- 影響因素

- 成長促進因素

- 聯網汽車和智慧汽車日益普及

- 消費者對安全性和免手動操作的需求日益成長

- 電動車和自動駕駛汽車(EV/AV)市場的擴張

- 售後軟體升級的成長

- 產業潛在風險與挑戰

- 高昂的OEM整合成本

- 隱私和資料安全問題

- 市場機遇

- 人工智慧助理整合

- 引入多模態人機交互

- 雲端連線和OTA更新

- 各地區智慧助理普及率

- 成長促進因素

- 技術趨勢與創新生態系統

- 目前技術

- 新興技術

- 成長潛力分析

- 監管環境

- 北美洲

- FMVSS駕駛分心預防指南

- 加州ACC/ZEV法規

- 加拿大運輸部連網車輛與資訊娛樂系統指南

- 歐洲

- 歐盟通用安全法規(GSR)

- 汽車資訊娛樂系統的CE認證

- 歐盟車輛類型認證指令

- 亞太地區

- 日本汽車電子設備安全標準

- 中國GB標準(適用於聯網汽車)

- 印度AIS/EMC指南

- 拉丁美洲

- 巴西 INMETRO 標準

- 哥倫比亞汽車互聯系統指南

- 阿根廷車載電子設備及資訊娛樂系統法規

- 中東和非洲

- 阿拉伯聯合大公國互聯語音汽車標準

- 阿曼汽車電子產品指南

- 南非SABS汽車音訊和資訊娛樂標準

- 北美洲

- 波特五力分析

- PESTEL 分析

- 價格趨勢

- OEM定價模式

- 售後市場價格趨勢

- 定期訂閱與單次購買模式

- 區域價格差異

- 專利分析

- 供應鏈分析

- 零件籌資策略

- 半導體晶片供應限制

- 對雲端基礎架構的依賴

- 區域供應鏈趨勢

- 打入市場策略

- 區域市場滲透策略

- 新參與企業需要考慮的關鍵監管因素

- 定價、服務和差異化策略

- 商業性可行性及部署

- 成本競爭力與高階音響產品提升銷售價值的比較

- OEM採購和平台擴充性的吸引力

- 售後升級可能性和經銷商安裝的經濟性

- 本地化、供應鏈彈性與物流可行性

- 永續性和環境方面

- 永續努力

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 競爭定位矩陣

- 戰略展望矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 企業擴張計畫和資金籌措

第5章 按技術分類的市場估算與預測,2022-2035年

- 語音辨識

- 自然語言處理(NLP)

- 人工智慧(AI)

第6章 按組件分類的市場估算與預測,2022-2035年

- 軟體

- 嵌入式軟體

- 基於雲端的軟體

- 人工智慧驅動的軟體

- 硬體

- 麥克風

- 揚聲器

- 控制單元

- 顯示面板

- 服務

- 整合與實施

- 維護和支援

- 諮詢服務

第7章 依車輛類型分類的市場估計與預測,2022-2035年

- 搭乘用車

- 轎車

- 掀背車車

- SUV

- 商用車輛

- 輕型商用車(LCV)

- 中型商用車(MCV)

- 重型商用車(HCV)

第8章 按應用領域分類的市場估算與預測,2022-2035年

- 導航

- 娛樂

- 溝通

- 其他

第9章 依銷售管道分類的市場估計與預測,2022-2035年

- OEM

- 售後市場

第10章 2022-2035年各地區市場估計與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 比利時

- 荷蘭

- 瑞典

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 新加坡

- 韓國

- 越南

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- Technology Giants &AI Platform Providers

- Amazon

- Apple

- Microsoft

- NVIDIA

- Cerence

- Nuance Communications

- SoundHound

- Tier 1 Automotive Suppliers

- Robert Bosch

- Continental

- Denso Corporation

- Samsung

- Aptiv PLC

- Panasonic Automotive Systems Company

- Visteon Corporation

- Automotive OEMs

- Mercedes-Benz Group

- Ford Motor Company

- Hyundai Motor Company

- BMW Group

- General Motors

- Tata Motors Limited

- 新興企業和專業公司

- Baidu

- Mihup Communications Private Limited

- Sensory

- NXP Semiconductors

The Global In-Vehicle Assistant Market was valued at USD 8.4 billion in 2025 and is estimated to grow at a CAGR of 9.7% to reach USD 21.3 billion by 2035.

Market expansion is driven by increasing consumer demand for safe, convenient, and hands-free vehicle interactions, alongside OEM commitments to introduce large numbers of electric and automated vehicles. The emergence of multimodal Human-Machine Interfaces (HMIs) is reshaping the industry, as automakers integrate voice, touch, and gesture-based inputs into connected vehicles. Large Language Models (LLMs) are enabling the development of smarter platforms and devices, allowing for more intuitive driver interactions and adoption across premium and entry-level vehicles alike. While the COVID-19 pandemic temporarily disrupted vehicle production and delayed new vehicle rollouts, the long-term demand for integrated voice assistants and advanced in-car digital experiences remains strong, supported by ongoing investments in connected and smart vehicle technologies.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $8.4 Billion |

| Forecast Value | $21.3 Billion |

| CAGR | 9.7% |

The speech recognition segment accounted for 53% share in 2025 and is expected to grow at a CAGR of 8.7% from 2026 to 2035. This technology forms the core of in-vehicle assistant systems, translating audio signals captured by microphones into actionable text via automatic speech recognition (ASR) algorithms. Revenue streams include specialized automotive ASR software licensing, beamforming microphones, and dedicated digital signal processor (DSP) chips for acoustic processing.

The software segment held a 59% share in 2025 and is anticipated to grow at a CAGR of 8.2% through 2035. Software platforms include cloud-based natural language processing, voice recognition engines, software update management systems, and APIs that integrate third-party applications. Licensing models vary, with traditional vendors often employing per-vehicle subscription arrangements.

China In-Vehicle Assistant Market generated USD 2.6 billion in 2025. The country produces over thirty million vehicles annually, and government initiatives, such as the New Infrastructure Policy and Smart City programs, are accelerating vehicle connectivity. Regulations mandating voice-based emergency call systems and dedicated funding for intelligent connected vehicles further reinforce the market's growth trajectory.

Key players in the Global In-Vehicle Assistant Market include Microsoft, Apple, Amazon, Cerence, Continental, Google, Nuance, Panasonic Automotive, Samsung, and SoundHound. Companies in the in-vehicle assistant market are strengthening their position by investing in AI-driven voice recognition, multimodal HMI systems, and cloud platform integration. Strategic partnerships with OEMs ensure early adoption and long-term contracts. Continuous R&D in natural language processing, edge computing, and DSP optimization enhances performance and reliability. Expanding regional footprints, particularly in emerging automotive markets, allows companies to tap new customer bases. Licensing strategies, software subscriptions, and integration with third-party platforms further increase revenue streams while establishing brand presence and technological leadership.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Technology

- 2.2.3 Component

- 2.2.4 Vehicle

- 2.2.5 Application

- 2.2.6 Sales Channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Component suppliers

- 3.1.1.2 Technology platform providers

- 3.1.1.3 System integrators

- 3.1.1.4 Automotive OEMs

- 3.1.1.5 Aftermarket distributors

- 3.1.1.6 End-users

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Vertical integration trends

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Impact on forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing adoption of connected & smart vehicles

- 3.2.1.2 Rising consumer demand for safety & hands-free interaction

- 3.2.1.3 Expansion of electric and autonomous vehicle (EV/AV) market

- 3.2.1.4 Growth of aftermarket & software upgrades

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High OEM integration cost

- 3.2.2.2 Privacy & data security concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Integration of AI-driven assistants

- 3.2.3.2 Multimodal HMI adoption

- 3.2.3.3 Cloud connectivity and OTA updates

- 3.2.3.4 Regional adoption of smart assistants

- 3.2.1 Growth drivers

- 3.3 Technology trends & innovation ecosystem

- 3.3.1 Current technologies

- 3.3.2 Emerging technologies

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.1.1 FMVSS Driver Distraction Guidelines

- 3.5.1.2 California ACC & ZEV Regulations

- 3.5.1.3 Transport Canada Connected Vehicle & Infotainment Guidelines

- 3.5.2 Europe

- 3.5.2.1 EU General Safety Regulation (GSR)

- 3.5.2.2 CE Certification for Automotive Infotainment

- 3.5.2.3 EU Vehicle Type Approval Directive

- 3.5.3 Asia-Pacific

- 3.5.3.1 Japan Automotive Electronics Safety Standards

- 3.5.3.2 China GB Standards for Connected Vehicles

- 3.5.3.3 India AIS / EMC Guidelines

- 3.5.4 Latin America

- 3.5.4.1 Brazil INMETRO Standards

- 3.5.4.2 Colombia Automotive Connected Systems Guidelines

- 3.5.4.3 Argentina Vehicle Electronics & Infotainment Regulations

- 3.5.5 Middle East & Africa

- 3.5.5.1 UAE Standards for Connected & Voice-Enabled Vehicles

- 3.5.5.2 Oman Automotive Electronics Guidelines

- 3.5.5.3 South Africa SABS Automotive Voice & Infotainment Standards

- 3.5.1 North America

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Price trends

- 3.8.1 OEM Pricing models

- 3.8.2 Aftermarket pricing trends

- 3.8.3 Subscription vs one-time purchase models

- 3.8.4 Regional price variations

- 3.9 Patent analysis

- 3.10 Supply chain analysis

- 3.10.1 Component sourcing strategies

- 3.10.2 Semiconductor chip supply constraints

- 3.10.3 Cloud infrastructure dependencies

- 3.10.4 Regional supply chain dynamics

- 3.11 Go-to-market strategies

- 3.11.1 Region-specific market penetration strategies

- 3.11.2 Key regulatory considerations for new entrants

- 3.11.3 Pricing, service, and differentiation strategies

- 3.12 Commercial viability & deployment

- 3.12.1 Cost competitiveness vs. premium audio upsell value

- 3.12.2 OEM sourcing attractiveness and platform scalability

- 3.12.3 Aftermarket upgrade potential and dealer fitment economics

- 3.12.4 Localization, supply resilience, and logistics practicality

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.13.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia-Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Technology, 2022 - 2035 ($Bn)

- 5.1 Key trends

- 5.2 Speech Recognition

- 5.3 Natural Language Processing (NLP)

- 5.4 Artificial Intelligence (AI)

Chapter 6 Market Estimates & Forecast, By Component, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Software

- 6.2.1 Embedded software

- 6.2.2 Cloud-based software

- 6.2.3 Ai-powered software

- 6.3 Hardware

- 6.3.1 Microphones

- 6.3.2 Speakers

- 6.3.3 Control units

- 6.3.4 Display panels

- 6.4 Service

- 6.4.1 Integration and deployment

- 6.4.2 Maintenance and support

- 6.4.3 Consulting services

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger Cars

- 7.2.1 Sedans

- 7.2.2 Hatchbacks

- 7.2.3 SUVs

- 7.3 Commercial Vehicles

- 7.3.1 Light commercial vehicles (LCV)

- 7.3.2 Medium commercial vehicles (MCV)

- 7.3.3 Heavy commercial vehicles (HCV)

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn)

- 8.1 Key trends

- 8.2 Navigation

- 8.3 Entertainment

- 8.4 Communication

- 8.5 Others

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 10.1 North America

- 10.1.1 US

- 10.1.2 Canada

- 10.2 Europe

- 10.2.1 UK

- 10.2.2 Germany

- 10.2.3 France

- 10.2.4 Italy

- 10.2.5 Spain

- 10.2.6 Belgium

- 10.2.7 Netherlands

- 10.2.8 Sweden

- 10.2.9 Russia

- 10.3 Asia Pacific

- 10.3.1 China

- 10.3.2 India

- 10.3.3 Japan

- 10.3.4 Australia

- 10.3.5 Singapore

- 10.3.6 South Korea

- 10.3.7 Vietnam

- 10.3.8 Indonesia

- 10.4 Latin America

- 10.4.1 Brazil

- 10.4.2 Mexico

- 10.4.3 Argentina

- 10.5 MEA

- 10.5.1 South Africa

- 10.5.2 Saudi Arabia

- 10.5.3 UAE

Chapter 11 Company Profiles

- 11.1 Technology Giants & AI Platform Providers

- 11.1.1 Amazon

- 11.1.2 Google

- 11.1.3 Apple

- 11.1.4 Microsoft

- 11.1.5 NVIDIA

- 11.1.6 Cerence

- 11.1.7 Nuance Communications

- 11.1.8 SoundHound

- 11.2 Tier 1 Automotive Suppliers

- 11.2.1 Robert Bosch

- 11.2.2 Continental

- 11.2.3 Denso Corporation

- 11.2.4 Samsung

- 11.2.5 Aptiv PLC

- 11.2.6 Panasonic Automotive Systems Company

- 11.2.7 Visteon Corporation

- 11.3 Automotive OEMs

- 11.3.1 Mercedes-Benz Group

- 11.3.2 Ford Motor Company

- 11.3.3 Hyundai Motor Company

- 11.3.4 BMW Group

- 11.3.5 General Motors

- 11.3.6 Tata Motors Limited

- 11.4 Emerging Players & Specialists

- 11.4.1 Baidu

- 11.4.2 Mihup Communications Private Limited

- 11.4.3 Sensory

- 11.4.4 NXP Semiconductors

汽車語音辨識系統市場:按類型、組件、技術、連接方式、應用、車輛類型和銷售管道分類-2026-2032年全球市場預測

汽車語音辨識系統市場:按類型、組件、技術、連接方式、應用、車輛類型和銷售管道分類-2026-2032年全球市場預測 2026年全球車載語音助理市場報告

2026年全球車載語音助理市場報告 汽車音響產業(2026 年)

汽車音響產業(2026 年) 2026-2034年全球汽車語音辨識市場規模、佔有率、趨勢與成長分析報告2026年全球汽車語音辨識系統市場報告

2026-2034年全球汽車語音辨識市場規模、佔有率、趨勢與成長分析報告2026年全球汽車語音辨識系統市場報告 汽車語音辨識系統市場-全球產業規模、佔有率、趨勢、機會及預測(依車輛類型、最終用戶、地區及競爭格局分類,2021-2031年)

汽車語音辨識系統市場-全球產業規模、佔有率、趨勢、機會及預測(依車輛類型、最終用戶、地區及競爭格局分類,2021-2031年) 全球汽車語音辨識市場

全球汽車語音辨識市場 汽車語音辨識市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

汽車語音辨識市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 汽車語音辨識系統:市場佔有率分析、產業趨勢/統計、成長預測(2024-2029)

汽車語音辨識系統:市場佔有率分析、產業趨勢/統計、成長預測(2024-2029)