|

市場調查報告書

商品編碼

1928995

拉伸膜及收縮膜市場機會、成長要素、產業趨勢分析及預測(2026年至2035年)Stretch and Shrink Films Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

全球拉伸收縮膜市場預計到 2025 年將達到 200 億美元,到 2035 年將達到 384 億美元,年複合成長率為 6.9%。

市場成長的驅動力來自循環經濟實踐的加速發展、回收活動的增加以及監管機構對永續包裝解決方案日益成長的關注。電子商務和物流活動的快速擴張顯著推動了對耐用、輕巧且經濟高效的包裝材料的需求,這些材料能夠在運輸和儲存過程中保護貨物。食品保鮮領域應用的不斷拓展,以及智慧包裝和薄膜製造技術的進步,進一步促進了市場擴張。日益增強的環保意識和更嚴格的塑膠廢棄物法規促使製造商採用可再生、可生物分解和環保的薄膜解決方案。此外,對本地採購的日益青睞以及對區域永續性政策的遵守,正在推動供應鏈的重組。這些趨勢在過去幾年中不斷增強,尤其是在歐洲和北美,監管壓力和消費者偏好的轉變正在加速環保包裝的普及。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 200億美元 |

| 預測金額 | 384億美元 |

| 複合年成長率 | 6.9% |

預計到2025年,包裝膜市佔率將達到49.1%。此細分市場的需求主要源自於對價格合理、防護性強的包裝解決方案的需求,以確保食品、零售和線上分銷通路的產品完整性。製造商越來越重視開發高性能、永續的包裝膜解決方案,力求在防護性、效率和環境影響之間取得平衡。

預計到2025年,聚乙烯產業的收入將達到59億美元。聚乙烯薄膜因其用途廣泛、經久耐用且成本優勢顯著,在多個終端應用產業中持續廣泛應用。生產商致力於提升薄膜質量,同時也開發可回收、可堆肥和環保材料。

預計到2025年,北美拉伸膜和收縮膜市佔率將達到30.2%。該地區的成長主要得益於蓬勃發展的電子商務、包裝作業自動化程度的提高以及鼓勵採用永續包裝的法規結構。消費者對環保包裝的需求也進一步推動了市場成長。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段的附加價值

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 促進要素

- 重點關注循環經濟和回收措施

- 不斷發展的電子商務和物流行業

- 在食品保藏領域不斷拓展的應用

- 智慧包裝解決方案的興起

- 薄膜製造技術的進步

- 產業潛在風險與挑戰

- 來自替代包裝材料的競爭

- 減少塑膠使用的監管壓力

- 市場機遇

- 永續包裝解決方案

- 引入可生物分解薄膜

- 促進要素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 新興經營模式

- 合規要求

- 永續性措施

- 消費者心理分析

- 地緣政治和貿易趨勢

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 按地區

- 市場集中度分析

- 主要企業的競爭標竿分析

- 財務績效比較

- 收入

- 利潤率

- 研究與開發

- 產品系列比較

- 產品線豐富

- 科技

- 創新

- 地理分佈比較

- 全球擴張分析

- 服務網路覆蓋範圍

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導企業

- 受讓人

- 追蹤者

- 小眾玩家

- 戰略展望矩陣

- 財務績效比較

- 2022-2025 年主要發展動態

- 併購

- 合作夥伴關係和合資企業

- 技術進步

- 擴張與投資策略

- 永續性措施

- 數位轉型計劃

新興企業/Start-Ups競爭趨勢

第5章 按材料分類的市場估算與預測,2022-2035年

- 聚乙烯(PE)

- 聚氯乙烯(PVC)

- 聚丙烯(PP)

- 可生物分解和可堆肥

- 其他

第6章 2022-2035年按產品分類的市場估算與預測

- 食物

- 封套和標籤

- 裹

第7章 依厚度類型分類的市場估計與預測,2022-2035年

- 超薄/膜(5-15μm)

- 標準商用膠片(15-25μm)

- 厚膜(25-50μm)

- 超厚/特殊規格薄膜(50微米或以上)

第8章 按應用領域分類的市場估算與預測,2022-2035年

- 消費品

- 食品/飲料

- 工業包裝

- 物流/運輸

- 製藥

- 其他

第9章 2022-2035年各地區市場估算與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- 主要企業

- Amcor plc

- Dow

- Sealed Air

- SABIC

- 按地區分類的主要企業

- 北美洲

- Intertape Polymer Group Inc.

- Film Source Packaging

- Sigma Plastics Group

- 亞太地區

- Scientex Berhad

- Shaktiman Packaging Pvt. Ltd.

- 歐洲

- Klockner Pentaplast

- Bollore Inc.

- 北美洲

- 小眾玩家/顛覆者

- Balcan Innovations Inc.

- HIPAC Spa

- Italdibipack SpA

- RKW Group

- LyondellBasell Industries NV

- AZ Packaging

- Paragon Films

- Coveris Holdings SA

- LUBAN PACK

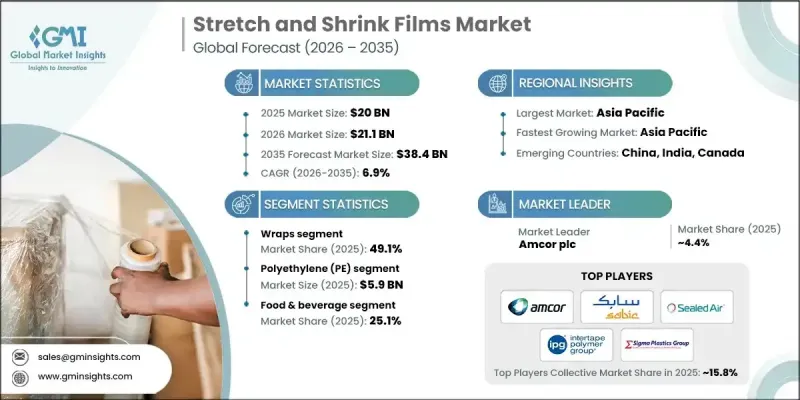

The Global Stretch and Shrink Films Market was valued at USD 20 billion in 2025 and is estimated to grow at a CAGR of 6.9% to reach USD 38.4 billion by 2035.

Market growth is driven by the accelerating adoption of circular economy practices, rising recycling initiatives, and increasing regulatory focus on sustainable packaging solutions. Rapid expansion of e-commerce and logistics activities is significantly boosting demand for durable, lightweight, and cost-efficient packaging materials that protect goods during transportation and storage. Growing applications in food preservation, combined with advancements in smart packaging and film manufacturing technologies, are further supporting market expansion. Heightened environmental awareness and stricter plastic waste regulations are encouraging manufacturers to introduce recyclable, biodegradable, and environmentally responsible film solutions. In addition, a growing preference for local sourcing and compliance with regional sustainability policies is reshaping supply chains. These trends have gained momentum over the past few years, particularly across Europe and North America, where eco-conscious packaging adoption has accelerated due to regulatory pressure and shifting consumer preferences.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $20 Billion |

| Forecast Value | $38.4 Billion |

| CAGR | 6.9% |

The wraps segment accounted for 49.1% share in 2025. Demand within this segment is being supported by the need for affordable and protective packaging solutions that maintain product integrity across food, retail, and online distribution channels. Manufacturers are increasingly prioritizing the development of high-performance and sustainable wrap solutions that balance protection, efficiency, and reduced environmental impact.

The polyethylene segment generated USD 5.9 billion in 2025. Polyethylene films continue to be widely adopted due to their versatility, durability, and cost advantages across multiple end-use industries. Producers are focusing on enhancing film quality while advancing recyclable, compostable, and lower-impact material options.

North America Stretch and Shrink Films Market held a 30.2% share in 2025. Regional growth is being driven by strong e-commerce activity, increasing automation in packaging operations, and regulatory frameworks that promote sustainable packaging adoption. Consumer demand for environmentally responsible packaging is further reinforcing market momentum.

Key companies operating in the Global Stretch and Shrink Films Market include Berry Global Inc., Amcor plc, Dow, LyondellBasell Industries N.V., Sealed Air, SABIC, Sigma Plastics Group, Paragon Films, RKW Group, Klockner Pentaplast, Intertape Polymer Group Inc., Coveris Holdings S.A., Bollore Inc, Balcan Innovations Inc, Scientex Berhad, HIPAC Spa, Italdibipack SpA, Film Source Packaging, A-Z Packaging, LUBAN PACK, and Shaktiman Packaging Pvt. Ltd. Companies in the Global Stretch and Shrink Films Market are strengthening their competitive position through sustainability-focused innovation, capacity expansion, and material optimization. Many players are investing in research to develop recyclable and bio-based films that comply with evolving environmental regulations. Enhancing production efficiency through automation and advanced manufacturing techniques is helping reduce costs and improve consistency. Strategic partnerships with e-commerce, food, and logistics companies are enabling long-term supply agreements.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry snapshot, 2022-2035

- 2.2 Key market trends

- 2.2.1 Material trends

- 2.2.2 Product trends

- 2.2.3 Thickness type trends

- 2.2.4 Application trends

- 2.2.5 Regional trends

- 2.3 TAM analysis, 2026-2035 (USD Million)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Focus on circular economy and recycling initiatives

- 3.2.1.2 Expansion of E-commerce and logistics sector

- 3.2.1.3 Increasing applications in food preservation

- 3.2.1.4 Emergence of smart packaging solutions

- 3.2.1.5 Advancements in film manufacturing technologies

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Competition of alternative packaging materials

- 3.2.2.2 Regulatory pressures for plastic use reduction

- 3.2.3 Market Opportunities

- 3.2.3.1 Sustainable packaging solutions

- 3.2.3.2 Adoption of biodegradable films

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter';s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging business models

- 3.9 Compliance requirements

- 3.10 Sustainability measures

- 3.11 Consumer sentiment analysis

- 3.12 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 MEA

- 4.2.2 Market Concentration Analysis

- 4.2.1 By region

- 4.3 Competitive Benchmarking of key Players

- 4.3.1 Financial Performance Comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit Margin

- 4.3.1.3 R&D

- 4.3.2 Product Portfolio Comparison

- 4.3.2.1 Product Range Breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic Presence Comparison

- 4.3.3.1 Global Footprint Analysis

- 4.3.3.2 Service Network Coverage

- 4.3.3.3 Market Penetration by Region

- 4.3.4 Competitive Positioning Matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche Players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial Performance Comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and Acquisitions

- 4.4.2 Partnerships and Collaborations

- 4.4.3 Technological Advancements

- 4.4.4 Expansion and Investment Strategies

- 4.4.5 Sustainability Initiatives

- 4.4.6 Digital Transformation Initiatives

Emerging/ Startup Competitors Landscape

Chapter 5 Market Estimates and Forecast, By Material, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Polyethylene (PE)

- 5.3 Polyvinyl chloride (PVC)

- 5.4 Polypropylene (PP)

- 5.5 Biodegradable and compostable

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Product, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Hoods

- 6.3 Sleeves and labels

- 6.4 Wraps

Chapter 7 Market Estimates and Forecast, By Thickness Type, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Very thin / downgauged films (5-15 μm)

- 7.3 Standard commercial films (15- 25 μm)

- 7.4 Heavy-duty films (25-50 μm)

- 7.5 Ultra-heavy / specialty gauges (50 μm and above)

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Consumer goods

- 8.3 Food & beverage

- 8.4 Industrial packaging

- 8.5 Logistics & transportation

- 8.6 Pharmaceuticals

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Amcor plc

- 10.1.2 Dow

- 10.1.3 Sealed Air

- 10.1.4 SABIC

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 Intertape Polymer Group Inc.

- 10.2.1.2 Film Source Packaging

- 10.2.1.3 Sigma Plastics Group

- 10.2.2 Asia Pacific

- 10.2.2.1 Scientex Berhad

- 10.2.2.2 Shaktiman Packaging Pvt. Ltd.

- 10.2.3 Europe

- 10.2.3.1 Klockner Pentaplast

- 10.2.3.2 Bollore Inc.

- 10.2.1 North America

- 10.3 Niche Players/Disruptors

- 10.3.1 Balcan Innovations Inc.

- 10.3.2 HIPAC Spa

- 10.3.3 Italdibipack SpA

- 10.3.4 RKW Group

- 10.3.5 LyondellBasell Industries N.V.

- 10.3.6 A-Z Packaging

- 10.3.7 Paragon Films

- 10.3.8 Coveris Holdings S.A.

- 10.3.9 LUBAN PACK

全球拉伸膜和收縮膜市場:市場規模、佔有率和趨勢分析(按材料、產品、應用和地區分類),細分市場預測(2026-2033 年)

全球拉伸膜和收縮膜市場:市場規模、佔有率和趨勢分析(按材料、產品、應用和地區分類),細分市場預測(2026-2033 年) 拉伸膜包裝市場-2026-2031年預測流延拉伸膜市場-2026-2031年預測

拉伸膜包裝市場-2026-2031年預測流延拉伸膜市場-2026-2031年預測 拉伸膜包裝市場:全球預測(2026-2032 年),按薄膜類型、材料、厚度、應用和最終用途產業分類

拉伸膜包裝市場:全球預測(2026-2032 年),按薄膜類型、材料、厚度、應用和最終用途產業分類 全球流延拉伸膜市場

全球流延拉伸膜市場 吹塑拉伸包裝膜市場機會、成長動力、產業趨勢分析及2025-2034年預測

吹塑拉伸包裝膜市場機會、成長動力、產業趨勢分析及2025-2034年預測 2032 年拉伸膜市場預測:按產品類型、品種、材料、厚度、應用和地區進行的全球分析拉伸和收縮套標市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

2032 年拉伸膜市場預測:按產品類型、品種、材料、厚度、應用和地區進行的全球分析拉伸和收縮套標市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 北美收縮和拉伸膜:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)全球透氣拉伸膜市場規模依材料類型、最終用途產業、厚度、地區、範圍和預測劃分

北美收縮和拉伸膜:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)全球透氣拉伸膜市場規模依材料類型、最終用途產業、厚度、地區、範圍和預測劃分