|

市場調查報告書

商品編碼

1928982

二手卡車市場機會、成長要素、產業趨勢分析及2026年至2035年預測Used Trucks Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

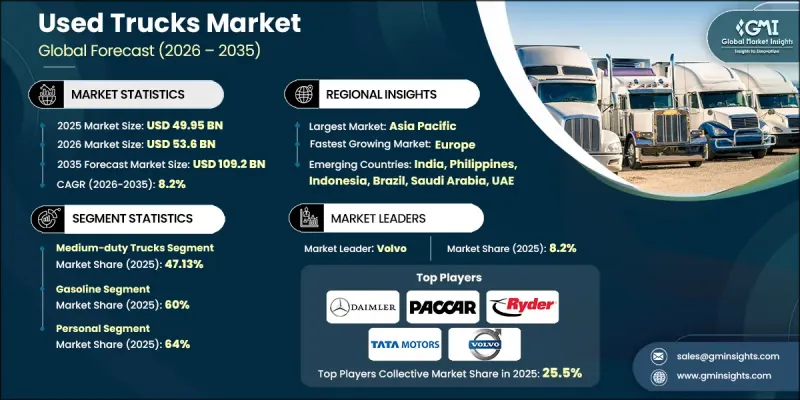

全球二手卡車市場預計到 2025 年將達到 499.5 億美元,到 2035 年將達到 1,092 億美元,年複合成長率為 8.2%。

車輛價格上漲、OEM交付週期延長以及對資本保全的重視,正促使車隊營運商轉向次市場,以維持業務永續營運和保障利潤率。二手卡車曾經被視為剩餘資產,如今已成為物流、建築、市政服務、採礦、農業、公共產業等行業車隊最佳化策略的重要組成部分。車隊經理優先考慮擁有完整服務記錄、符合排放氣體標準且能夠進行數位化改裝的車輛。遠端資訊處理、預測性維護、ADAS改裝和動力傳動系統監控等技術的應用,能夠延長車輛使用壽命、降低總擁有成本,並支援基於數據驅動的決策,從而最佳化燃油效率、駕駛員表現和資產重新部署。這種以生命週期為導向的策略,而非僅僅關注首次購車成本,正在改變市場動態,使二手卡車成為注重成本控制、尋求在都市區和區域交通網路中實現運營柔軟性和效率的車隊運營商的戰略選擇。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 499.5億美元 |

| 預測金額 | 1092億美元 |

| 複合年成長率 | 8.2% |

預計到2025年,中型卡車市佔率將達到47.13%,並在2035年之前以8.1%的複合年成長率成長。總重在10,001至26,000磅(約4,536至11,814公斤)之間的中型卡車具有多功能性、燃油效率高和購置成本低等優點,是城市物流、最後一公里配送、建築支援和市政服務的理想選擇。其有效載荷能力和營運成本效益的平衡使其尤其受到中小車隊營運商的青睞。

預計到2025年,汽油卡車市佔率將達到60%,並在2026年至2035年間以8.3%的複合年成長率成長。汽油卡車易於取得、購買成本低廉且維護簡便,使其對車隊營運商、中小企業和區域配送服務供應商極具吸引力。完善的服務網路和充足的零件供應進一步提升了汽油卡車的吸引力,尤其是在新興市場。

預計到2025年,中國二手卡車市場將佔據全球65.5%的市場佔有率,市場規模達229.6億美元。電子商務、物流、跨區域運輸和基礎設施計劃的快速發展推動了這一成長。新車價格上漲使得二手車對中小企業更具吸引力,從而帶動了對中重型二手卡車的需求。

目錄

第1章調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率分析

- 成本結構

- 每個階段的附加價值

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 促進要素

- 全球對電動和混合動力重型卡車的需求不斷成長

- 北美貨運活動不斷擴大

- 中小企業數量呈現成長趨勢

- 亞太地區基礎建設活動投資增加

- 產業潛在風險與挑戰

- 景氣衰退和低經濟成長

- 監理合規與政府法規

- 市場機遇

- 擴展認證二手(CPO) 和製造商保固二手卡車計劃

- 小型企業和自僱人士對經濟高效的車隊解決方案的需求日益成長

- 已開發國家向新興市場跨境二手貿易日益成長

- 數位再行銷、線上競標和數據驅動定價的日益普及

- 促進要素

- 成長潛力分析

- 監管環境

- 北美洲

- NEVI/IIJA,先進清潔卡車 (ACT) 法規

- 歐洲

- 德國:《電動車法案》(EmoG)

- 英國:清潔車輛改裝和認證計畫 (CVRAS)、超低排放氣體區 (ULEZ)

- 法國:流動性導向法(LOM 法)

- 義大利:國家綜合能源與氣候計畫(PNIEC)

- 亞太地區

- 中國:新能源汽車(NEV)強制政策

- 印度:FAME II計劃

- 日本:電動車(EV)與燃料電池汽車(FCV)引進戰略藍圖

- 澳洲:各州零排放車輛強制令

- 拉丁美洲

- 巴西:國家電動車政策(PNME)

- 墨西哥:都市區零排放車輛引進計劃

- 阿根廷:各州電動車獎勵政策(布宜諾斯艾利斯省)

- 中東和非洲

- 阿拉伯聯合大公國:電動車充電基礎設施法規(ADDM/DEWA)

- 沙烏地阿拉伯:電動車推廣法規結構(SASO)

- 南非:綠色交通戰略

- 北美洲

- 波特分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利分析

- 定價分析

- 按地區

- 按燃料

- 生產統計

- 生產基地

- 消費基礎

- 出口和進口

- 成本細分分析

- 永續性和環境影響分析

- 永續努力

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

- 未來前景與機遇

- 車隊採購與採購行為分析

- 購買二手卡車的決策標準

- OEM選擇與品牌偏好因素

- 燃料、負載容量和運作時間如何影響購買決策

- 二手卡車市場的殘值與市場動態

- 融資、租賃和卡車即服務 (TaaS) 的經濟學

- 售後市場、服務與零件經濟學

- 動力傳動系統轉型與燃料轉型路徑

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 企業擴張計畫和資金籌措

第5章 依燃料類型分類的市場估算與預測,2022-2035年

- 汽油

- 柴油引擎

- 電動車

- 混合

第6章 按類型分類的市場估算與預測,2022-2035年

- 小型卡車

- 中型卡車

- 大型卡車

7. 2022-2035年按銷售管道分類的市場估算與預測

- 特許經銷商

- 獨立零售商

- P2P

第8章 2022-2035年按規模分類的市場估算與預測

- 全尺寸

- 中號

- 袖珍的

第9章 依年齡分類的市場估計與預測,2022-2035年

- 最長3年

- 5至10歲

- 10歲以上

第10章 按驅動類型分類的市場估算與預測,2022-2035年

- 兩輪驅動

- 四輪驅動

第11章 按應用領域分類的市場估算與預測,2022-2035年

- 對於個人

- 商業的

- 建築和重型設備

- 農業和畜牧業

- 景觀美化和戶外服務

- 公共產業和市政應用

第12章 2022-2035年各地區市場估算與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 菲律賓

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第13章:公司簡介

- 世界玩家

- Copart

- Daimler

- Hino Motors

- Isuzu Motors

- Navistar International

- PACCAR

- Penske Used Trucks

- Ritchie Bros. Auctioneers

- Ryder System

- TATA Motors

- Volvo Trucks

- 區域玩家

- Arrow Truck Sales

- Enterprise Truck Rental

- International Used Trucks

- Knight-Swift Transportation

- Mascus

- Schneider National

- TruckPaper

- Werner Enterprises

- 新興企業

- JD Power

- Carvana

- Manheim

The Global Used Trucks Market was valued at USD 49.95 billion in 2025 and is estimated to grow at a CAGR of 8.2% to reach USD 109.2 billion by 2035.

Increasing vehicle prices, long OEM delivery times, and a focus on capital preservation are driving fleet operators toward the secondary market to maintain operational continuity and protect profit margins. Once viewed as residual assets, used trucks are now integral to fleet optimization strategies across logistics, construction, municipal services, mining, agriculture, and utilities. Fleet managers are prioritizing vehicles with verified service histories, compliance with emission standards, and the ability to accommodate digital retrofits. The adoption of telematics, predictive maintenance, ADAS retrofits, and powertrain monitoring enhances vehicle longevity, reduces total cost of ownership, and enables data-driven decisions for fuel efficiency, driver performance, and asset redeployment. This lifecycle-oriented approach, rather than first-ownership economics, is reshaping demand dynamics, making used trucks a strategic choice for cost-conscious fleet operators seeking operational flexibility and efficiency in urban and regional transportation networks.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $49.95 Billion |

| Forecast Value | $109.2 Billion |

| CAGR | 8.2% |

The medium-duty segment held 47.13% share in 2025 and is projected to grow at a CAGR of 8.1% through 2035. Medium-duty trucks, with GVWR ranging from 10,001-26,000 lbs, offer versatility, fuel efficiency, and lower acquisition costs, making them ideal for urban logistics, last-mile deliveries, construction support, and municipal applications. These trucks are particularly favored by small and medium-sized fleet operators due to their balance of payload capacity and operational cost-effectiveness.

The gasoline trucks segment accounted for 60% share in 2025 and is expected to grow at a CAGR of 8.3% from 2026 to 2035. Their widespread availability, lower purchase price, and ease of maintenance make them highly appealing to fleet operators, small businesses, and local delivery services. Broad service networks and abundant spare parts further enhance the attractiveness of gasoline trucks, particularly in emerging markets.

China Used Trucks Market held 65.5% share, generating USD 22.96 billion in 2025. The growth is supported by rapid expansion in e-commerce, logistics, regional transportation, and infrastructure projects. Rising new truck prices have further increased the appeal of pre-owned vehicles among small- and medium-sized operators, fueling demand for medium- and heavy-duty used trucks.

Major players in the Global Used Trucks Market include Enterprise Truck Rental, PACCAR, Daimler, Penske Used Trucks, Ryder System, Schneider National, Ritchie Bros. Auctioneers, TATA Motors, Werner Enterprises, and Volvo Trucks. Companies in the Global Used Trucks Market strengthen their presence through strategic fleet acquisition, digital integration, and after-sales services. Emphasis on telematics, predictive maintenance, and vehicle certification ensures reliability and builds customer trust. Expanding geographic reach and diversifying inventory across duty classes meet regional demand. Partnerships with logistics, construction, and municipal operators enhance market penetration. Companies also focus on value-added services such as financing, warranty programs, and fleet management solutions to improve customer retention and increase total cost-of-ownership transparency.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Fuel

- 2.2.4 Sales Channel

- 2.2.5 Size

- 2.2.6 Age

- 2.2.7 Drive

- 2.2.8 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for electric & hybrid heavy-duty trucks across the globe

- 3.2.1.2 Growing freight transportation activities across North America

- 3.2.1.3 The rising number of small and medium-sized businesses

- 3.2.1.4 Rising investments in infrastructure development activities in Asia Pacific

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Economic downturns and low economic growth

- 3.2.2.2 Regulatory compliance and government regulations

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of certified pre-owned (CPO) and OEM-backed used truck programs

- 3.2.3.2 Growing demand for cost-effective fleet solutions among SME and owner-operators

- 3.2.3.3 Rising cross-border trade of used trucks from developed to emerging markets

- 3.2.3.4 Increasing adoption of digital remarketing, online auctions, and data-driven pricing

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 NEVI / IIJA, Advanced Clean Trucks (ACT) Regulation.

- 3.4.2 Europe

- 3.4.2.1 Germany: Electric Mobility Act (EmoG)

- 3.4.2.2 UK: Clean Vehicle Retrofit Accreditation Scheme (CVRAS), Ultra-Low Emission Zone (ULEZ)

- 3.4.2.3 France: Mobility Orientation Law (LOM Act)

- 3.4.2.4 Italy: National Integrated Plan for Energy and Climate (PNIEC)

- 3.4.3 Asia Pacific

- 3.4.3.1 China: New Energy Vehicle (NEV) Mandate

- 3.4.3.2 India: FAME II Scheme

- 3.4.3.3 Japan: Strategic Roadmap for EV/FCV Deployment

- 3.4.3.4 Australia: State-Level Zero-Emission Vehicle Mandates

- 3.4.4 Latin America

- 3.4.4.1 Brazil: National Electric Mobility Policy (PNME)

- 3.4.4.2 Mexico: Urban Zero-Emission Fleet Programs

- 3.4.4.3 Argentina: Provincial EV Incentive Regulations (Buenos Aires)

- 3.4.5 MEA

- 3.4.5.1 UAE: EV Charging Infrastructure Regulation (ADDM/DEWA)

- 3.4.5.2 Saudi Arabia: EV Deployment Regulatory Framework (SASO)

- 3.4.5.3 South Africa: Green Transport Strategy

- 3.4.1 North America

- 3.5 Porter';s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis

- 3.9 Pricing Analysis

- 3.9.1 By region

- 3.9.2 By fuel

- 3.10 Production statistics

- 3.10.1 Production hubs

- 3.10.2 Consumption hubs

- 3.10.3 Export and import

- 3.11 Cost breakdown analysis

- 3.12 Sustainability and environmental impact analysis

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Future outlook & opportunities

- 3.14 Fleet procurement & buying behavior analysis

- 3.14.1 Purchase decision criteria for Used trucks

- 3.14.2 OEM selection and brand preference factors

- 3.14.3 Impact of fuel, payload, and uptime on buying decisions

- 3.15 Residual value & used truck market dynamics

- 3.16 Financing, leasing & Truck-as-a-Service (TaaS) economics

- 3.17 Aftermarket, service & parts economics

- 3.18 Powertrain transition & fuel migration pathways

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Fuel, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Gasoline

- 5.3 Diesel

- 5.4 Electric

- 5.5 Hybrid

Chapter 6 Market Estimates & Forecast, By Type, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Light-duty truck

- 6.3 Medium-duty truck

- 6.4 Heavy-duty truck

Chapter 7 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Franchised Dealer

- 7.3 Independent Dealer

- 7.4 Peer-to-peer

Chapter 8 Market Estimates & Forecast, By Size, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Full-size

- 8.3 Mid-size

- 8.4 Compact

Chapter 9 Market Estimates & Forecast, By Age, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 Up to 3 years

- 9.3 5-10 years

- 9.4 Above 10 years

Chapter 10 Market Estimates & Forecast, By Drive, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 Two-wheel drive

- 10.3 Four-wheel drive

Chapter 11 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn, Units)

- 11.1 Key trends

- 11.2 Personal

- 11.3 Commercial

- 11.3.1 Construction and heavy equipment

- 11.3.2 Agriculture and farming

- 11.3.3 Landscaping and outdoor services

- 11.3.4 Utility and municipal use

Chapter 12 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 US

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Russia

- 12.3.7 Nordics

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 Australia

- 12.4.5 South Korea

- 12.4.6 Philippines

- 12.4.7 Indonesia

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.6 MEA

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 Global Players

- 13.1.1 Copart

- 13.1.2 Daimler

- 13.1.3 Hino Motors

- 13.1.4 Isuzu Motors

- 13.1.5 Navistar International

- 13.1.6 PACCAR

- 13.1.7 Penske Used Trucks

- 13.1.8 Ritchie Bros. Auctioneers

- 13.1.9 Ryder System

- 13.1.10 TATA Motors

- 13.1.11 Volvo Trucks

- 13.2 Regional Players

- 13.2.1 Arrow Truck Sales

- 13.2.2 Enterprise Truck Rental

- 13.2.3 International Used Trucks

- 13.2.4 Knight-Swift Transportation

- 13.2.5 Mascus

- 13.2.6 Schneider National

- 13.2.7 TruckPaper

- 13.2.8 Werner Enterprises

- 13.3 Emerging Players

- 13.3.1 J.D. Power

- 13.3.2 Carvana

- 13.3.3 Manheim