|

市場調查報告書

商品編碼

1928978

焊接設備及耗材市場機會、成長要素、產業趨勢分析及2026年至2035年預測Welding Equipment and Consumables Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

全球焊接設備和耗材市場預計到 2025 年將達到 147 億美元,到 2035 年將達到 243 億美元,年複合成長率為 5.2%。

快速的都市化和大規模基礎設施建設推動了焊接行業的擴張,這需要可靠、高強度的焊接解決方案。現代化基礎設施計劃需要先進的焊接技術,以確保橋樑、鐵路、公路和工業設施的耐久性和結構完整性。除了建築業之外,向永續建築方式的轉變也推動了對創新焊接技術的需求,這些技術能夠提高效率並最大限度地減少對環境的影響。公共和私營部門的基礎設施投資正在創造持續的成長機會。同時,隨著電動車和輕量化材料的應用,汽車和運輸業正在經歷轉型,這進一步推動了對能夠處理新型合金和複合材料的專用焊接設備和耗材的需求。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 147億美元 |

| 預測金額 | 243億美元 |

| 複合年成長率 | 5.2% |

預計到2025年,焊條市場規模將達到50億美元,並在2035年之前以4.6%的複合年成長率成長。焊條因其經濟高效、用途廣泛以及在戶外和惡劣環境下可靠運作而備受歡迎,使其成為建築、維修和維護應用中不可或缺的材料。其堅固耐用的設計使其能夠在其他焊材可能失效的環境中高效焊接,例如在風、雨和極端溫度下。此外,焊條還與多種金屬和合金相容,可在各種計劃中提供一致的焊接品質。

預計到2025年,電弧焊接市佔率將達到43.4%。電弧焊接的適應性和高效性使其成為汽車、建築和重工業等對焊接品質要求極高的行業的核心技術。手工電弧焊接(SMAW)、氣體保護金屬電弧焊接(GMAW)和電弧焊接(SAW)等技術被廣泛用於在各種金屬和合金上實現持久、精確的焊接。

美國焊接設備及耗材市場預計到2025年將達到27億美元,2026年至2035年的複合年成長率(CAGR)為5.7%。美國市場擁有強大的工業基礎和高度發展的製造業,汽車、航太和能源產業自動化和機器人焊接系統的普及推動了對精密設備的需求。為滿足嚴格的安全和品質標準,企業正加速投資尖端焊接技術和耗材,以支援先進的工業流程。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段的附加價值

- 影響價值鏈的因素

- 產業影響因素

- 促進要素

- 基礎設施建設和工業化

- 汽車和運輸業的擴張

- 焊接工藝的技術進步

- 挑戰與困難

- 較高的初始投資和維護成本

- 熟練勞動力短缺

- 機會

- 自動化和工業4.0的採用

- 可再生能源領域需求不斷成長

- 促進要素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 監管環境

- 北美洲

- 美國:消費品安全委員會(CPSC)聯邦法規(CFR)第16篇第1512部分

- 加拿大:國際標準化組織(ISO)4210

- 歐洲

- 德國:德國標準化協會 (DIN) 歐洲標準 (EN) ISO 4210

- 英國:歐洲標準 (EN) ISO 4210/英國合格評定 (UKCA)

- 法國:歐洲標準 (EN) ISO 4210

- 亞太地區

- 中國:國家標準(GB)3565

- 印度:印度標準 (IS) 10613

- 日本:日本工業標準(JIS)D 9110

- 拉丁美洲

- 巴西:巴西技術標準協會 (ABNT) 巴西標準 (NBR) ISO 4210

- 墨西哥:國際標準化組織(ISO)4210

- 中東和非洲

- 南非:南非國家標準 (SANS) 311

- 沙烏地阿拉伯:沙烏地阿拉伯標準、計量和品質組織 (SASO) 海灣標準組織 (GSO) ISO 4210

- 北美洲

- 貿易統計(HS編碼-8501)

- 主要進口國

- 主要出口國

- 波特分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章 按類型分類的市場估算與預測,2022-2035年

- 棒狀電極

- 單線

- 磁通繞組

- 縫紉線

- 其他(棒狀電極、保護氣體等)

第6章 按技術分類的市場估計與預測,2022-2035年

- 電弧焊接

- 電阻焊接

- 氧乙炔焊

- 固體焊接

- 其他(電子束等)

第7章 按應用領域分類的市場估算與預測,2022-2035年

- 車

- 建築/施工

- 船

- 航太/國防

- 石油和天然氣

- 其他(金屬、採礦等)

第8章 按分銷管道分類的市場估算與預測,2022-2035年

- 直銷

- 間接

第9章 2022-2035年各地區市場估算與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

第10章:公司簡介

- Ador Welding Ltd.

- Air Liquide Welding

- Arcon Welding Equipment

- Bohler Welding

- Denyo Co., Ltd.

- ESAB

- Fronius International GmbH

- Hyundai Welding Co., Ltd.

- Illinois Tool Works Inc.(ITW)

- Jasic Technology Co., Ltd.

- Kemppi Oy

- Lincoln Electric

- Miller Electric

- Panasonic Welding Systems

- Tianjin Golden Bridge Welding Materials Group

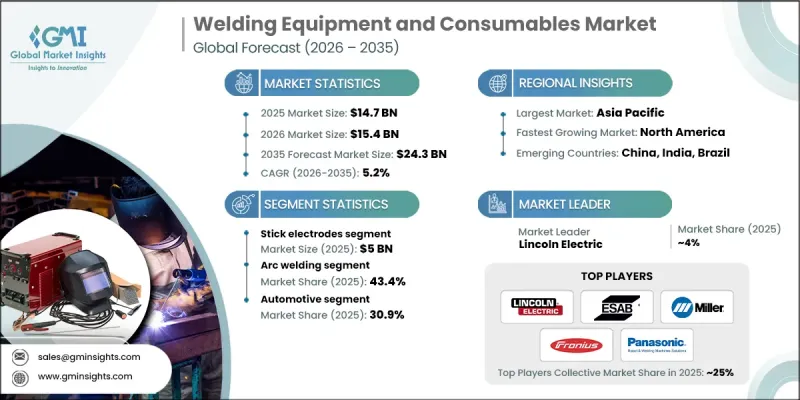

The Global Welding Equipment and Consumables Market was valued at USD 14.7 billion in 2025 and is estimated to grow at a CAGR of 5.2% to reach USD 24.3 billion by 2035.

The industry's expansion is fueled by rapid urbanization and large-scale infrastructure developments that demand reliable and high-strength welding solutions. Modern infrastructure projects require advanced welding techniques to ensure durability and structural integrity across bridges, railways, highways, and industrial facilities. Beyond construction, the shift toward sustainable building practices has increased the need for innovative welding technologies that improve efficiency and minimize environmental impact. Investments from both public and private sectors in infrastructure are creating consistent growth opportunities. At the same time, the automotive and transportation industries are undergoing transformation due to the adoption of electric vehicles and lightweight materials, further driving demand for specialized welding equipment and consumables capable of handling new alloys and composites.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $14.7 Billion |

| Forecast Value | $24.3 Billion |

| CAGR | 5.2% |

The stick electrodes segment accounted for USD 5 billion in 2025 and is expected to grow at a CAGR of 4.6% through 2035. These electrodes remain popular due to their cost-effectiveness, versatility, and ability to perform reliably in outdoor and challenging conditions, making them indispensable for construction, repair, and maintenance applications. Their robust design allows welders to work efficiently in environments with wind, rain, or extreme temperatures, where other consumables might fail. Stick electrodes also offer compatibility with a wide range of metals and alloys, providing consistent weld quality across diverse projects.

The arc welding segment held a 43.4% share in 2025. Arc welding's adaptability and efficiency make it central to industries requiring high-quality welds, including automotive, construction, and heavy engineering. Techniques such as shielded metal arc welding (SMAW), gas metal arc welding (GMAW), and submerged arc welding (SAW) are widely employed to achieve durable and precise welds across various metals and alloys.

U.S. Welding Equipment and Consumables Market generated USD 2.7 billion in 2025 and is projected to grow at a CAGR of 5.7% from 2026 to 2035. The U.S. market benefits from a robust industrial base and a highly developed manufacturing sector, where widespread adoption of automated and robotic welding systems in automotive, aerospace, and energy industries is driving demand for high-precision equipment. The focus on meeting stringent safety and quality standards has accelerated investments in cutting-edge welding technologies and consumables to support advanced industrial processes.

Major players in the Global Welding Equipment and Consumables Market include Ador Welding Ltd., Air Liquide Welding, Arcon Welding Equipment, Bohler Welding, Denyo Co., Ltd., ESAB, Fronius International GmbH, Hyundai Welding Co., Ltd., Illinois Tool Works Inc. (ITW), Jasic Technology Co., Ltd., Kemppi Oy, Lincoln Electric, Miller Electric, Panasonic Welding Systems, and Tianjin Golden Bridge Welding Materials Group. Companies in the Global Welding Equipment and Consumables Market are pursuing multiple strategies to strengthen their market presence and expand their foothold. They are investing in research and development to introduce advanced, high-efficiency welding solutions tailored for industrial, construction, and automotive applications. Partnerships and collaborations with infrastructure and automotive companies allow them to offer integrated solutions and secure long-term contracts. Many are focusing on expanding their geographic reach, particularly in emerging markets where infrastructure growth is rapid. The adoption of automation, robotic welding systems, and smart welding technologies helps enhance operational efficiency for clients, increasing brand loyalty.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Market estimates & forecasts parameters

- 1.4 Forecast Model

- 1.4.1 Key trends for market estimates

- 1.4.2 Quantified market impact analysis

- 1.4.2.1 Mathematical impact of growth parameters on forecast

- 1.4.3 Scenario analysis framework

- 1.5 Primary research and validation

- 1.5.1 Some of the primary sources (but not limited to)

- 1.6 Data mining sources

- 1.6.1 Paid Sources

- 1.7 Primary research and validation

- 1.7.1 Primary sources

- 1.8 Research Trail & confidence scoring

- 1.8.1 Research trail components

- 1.8.2 Scoring components

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market Definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Technology

- 2.2.4 Application

- 2.2.5 Distribution channels

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Infrastructure development and industrialization

- 3.2.1.2 Automotive and transportation sector expansion

- 3.2.1.3 Technological advancements in welding processes

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 High initial investment and maintenance costs

- 3.2.2.2 Shortage of skilled workforce

- 3.2.3 Opportunities

- 3.2.3.1 Adoption of automation and industry 4.0

- 3.2.3.2 Growing demand in renewable energy sector

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Regulatory landscape

- 3.7.1 North America

- 3.7.1.1 US: Consumer Product Safety Commission (CPSC) 16 Code of Federal Regulations (CFR) part 1512

- 3.7.1.2 Canada: International Organization for Standardization (ISO) 4210

- 3.7.2 Europe

- 3.7.2.1 Germany: Deutsches Institut fur Normung (DIN) European Norm (EN) ISO 4210

- 3.7.2.2 UK: European Norm (EN) ISO 4210 / United Kingdom Conformity Assessed (UKCA)

- 3.7.2.3 France: European Norm (EN) ISO 4210

- 3.7.3 Asia Pacific

- 3.7.3.1 China: Guobiao (GB) 3565

- 3.7.3.2 India: Indian Standard (IS) 10613

- 3.7.3.3 Japan: Japanese Industrial Standard (JIS) D 9110

- 3.7.4 Latin America

- 3.7.4.1 Brazil: Associacao Brasileira de Normas Tecnicas (ABNT) Norma Brasileira (NBR) ISO 4210

- 3.7.4.2 Mexico: International Organization for Standardization (ISO) 4210

- 3.7.5 Middle East & Africa

- 3.7.5.1 South Africa: South African National Standard (SANS) 311

- 3.7.5.2 Saudi Arabia: Saudi Standards, Metrology and Quality Organization (SASO) Gulf Standardization Organization (GSO) ISO 4210

- 3.7.1 North America

- 3.8 Trade statistics (HS Code - 8501)

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter';s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2022 - 2035, (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Stick electrodes

- 5.3 Solid wires

- 5.4 Flux coiled wires

- 5.5 Saw wires

- 5.6 Others (rod electrodes, shielding gas, etc.)

Chapter 6 Market Estimates & Forecast, By Technology, 2022 - 2035, (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Arc welding

- 6.3 Resistance welding

- 6.4 Oxy-fuel welding

- 6.5 Solid state welding

- 6.6 Others (electron beam, etc.)

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035, (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Automotive

- 7.3 Building and construction

- 7.4 Marine

- 7.5 Aerospace & defense

- 7.6 Oil & gas

- 7.7 Others (metal, mining, etc.)

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Direct

- 8.3 Indirect

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 Saudi Arabia

- 9.6.2 UAE

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Ador Welding Ltd.

- 10.2 Air Liquide Welding

- 10.3 Arcon Welding Equipment

- 10.4 Bohler Welding

- 10.5 Denyo Co., Ltd.

- 10.6 ESAB

- 10.7 Fronius International GmbH

- 10.8 Hyundai Welding Co., Ltd.

- 10.9 Illinois Tool Works Inc. (ITW)

- 10.10 Jasic Technology Co., Ltd.

- 10.11 Kemppi Oy

- 10.12 Lincoln Electric

- 10.13 Miller Electric

- 10.14 Panasonic Welding Systems

- 10.15 Tianjin Golden Bridge Welding Materials Group

焊接設備市場:按類型、技術、材料類型、電源、用戶類型、應用和分銷管道分類-2026-2032年全球預測旋轉焊接機市場:依焊接技術、機器類型、電源、喉深、行動類型和終端用戶產業分類-2026-2032年全球預測高速網片焊接機市場:依產品類型、焊接製程、產量、銷售管道及應用分類-全球預測,2026-2032年固定電阻點焊機市場:依機器類型、自動化程度、額定功率、焊接電流和終端用戶產業分類,全球預測,2026-2032年高速自動焊絲焊接機市場:依機器類型、焊接工藝類型、自動化程度、功率等級、終端用戶產業及銷售管道,全球預測,2026-2032年攜帶式電阻點焊機市場:按機器類型、功率輸出、焊接模式、電極材料和終端用戶產業分類,全球預測,2026-2032年旋轉焊接變位機市場:按類型、負載能力、軸類型、動力系統、最終用戶分類,全球預測(2026-2032年)焊接工作台煙塵收集器市場:依產品類型、機械結構、過濾方式、安裝方式、應用、終端用戶產業分類,全球預測(2026-2032年)

焊接設備市場:按類型、技術、材料類型、電源、用戶類型、應用和分銷管道分類-2026-2032年全球預測旋轉焊接機市場:依焊接技術、機器類型、電源、喉深、行動類型和終端用戶產業分類-2026-2032年全球預測高速網片焊接機市場:依產品類型、焊接製程、產量、銷售管道及應用分類-全球預測,2026-2032年固定電阻點焊機市場:依機器類型、自動化程度、額定功率、焊接電流和終端用戶產業分類,全球預測,2026-2032年高速自動焊絲焊接機市場:依機器類型、焊接工藝類型、自動化程度、功率等級、終端用戶產業及銷售管道,全球預測,2026-2032年攜帶式電阻點焊機市場:按機器類型、功率輸出、焊接模式、電極材料和終端用戶產業分類,全球預測,2026-2032年旋轉焊接變位機市場:按類型、負載能力、軸類型、動力系統、最終用戶分類,全球預測(2026-2032年)焊接工作台煙塵收集器市場:依產品類型、機械結構、過濾方式、安裝方式、應用、終端用戶產業分類,全球預測(2026-2032年) 日本工業焊接機市場規模、佔有率、趨勢及預測(依焊接技術、自動化程度、電源類型、銷售管道、終端用戶產業及地區分類,2026-2034年)日本智慧焊接設備市場規模、佔有率、趨勢及預測(按組件、材料類型、焊接技術、自動化程度、最終用途產業及地區分類),2026-2034年

日本工業焊接機市場規模、佔有率、趨勢及預測(依焊接技術、自動化程度、電源類型、銷售管道、終端用戶產業及地區分類,2026-2034年)日本智慧焊接設備市場規模、佔有率、趨勢及預測(按組件、材料類型、焊接技術、自動化程度、最終用途產業及地區分類),2026-2034年