|

市場調查報告書

商品編碼

1913470

商用車座椅市場機會、成長要素、產業趨勢分析及2026年至2035年預測Commercial Vehicle Seat Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

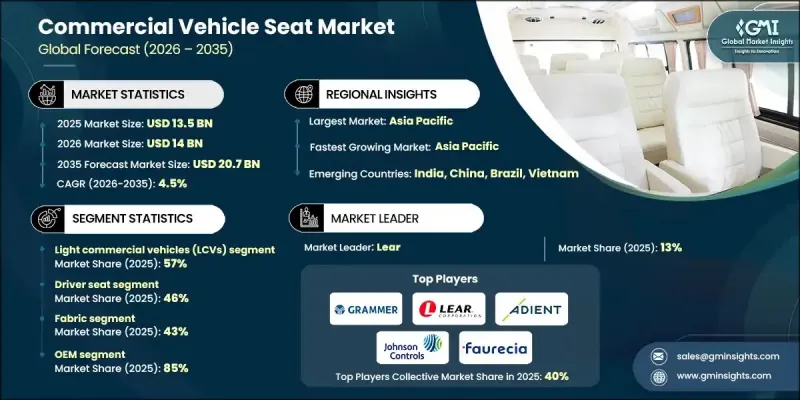

全球商用車座椅市場預計到 2025 年將達到 135 億美元,到 2035 年將達到 207 億美元,年複合成長率為 4.5%。

隨著車隊營運商將駕駛人的健康、效率和長期成本控制放在首位,市場發展日益受到以人體工學和舒適性為導向的座椅解決方案的驅動。座椅設計不佳被廣泛認為是導致身體不適和生產力下降的因素之一,因此,能夠提供姿勢支撐、減輕疲勞並改善日常駕駛體驗的座椅需求不斷成長。商用車座椅正從基本的舒適性發展成為與車輛電子設備和駕駛員監控平台整合的先進技術系統。電動調節、溫度控制、記憶設定和按摩功能等特性,反映了商用車內裝向高價值方向發展的趨勢。全球範圍內不斷加強的座椅性能、乘員保護和材料標準等安全標準也對市場產生了積極影響,促使製造商採用更先進的設計。同時,物流、貨運和配送服務的擴張持續推動全球商用車需求,並在新車生產和更換週期中帶動座椅安裝量的穩定成長。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 135億美元 |

| 預測金額 | 207億美元 |

| 複合年成長率 | 4.5% |

預計到2025年,輕型商用車市佔率將達到57%,並在2026年至2035年間以3.9%的複合年成長率成長。這一主導地位反映了其在配送服務、酒店服務和市政運營等領域的廣泛應用。此類車輛總重低於6000公斤(13228磅),需要具備耐用、耐磨的特性,並配備簡化的調節機構和經濟實惠的座椅,以滿足高使用率且注重預算的運營商的需求。

預計到2025年,駕駛室市佔率將達到46%,並在2026年至2035年間以4.8%的複合年成長率實現最快成長。駕駛室因其在安全、舒適性和員工留任方面發揮的關鍵作用而具有更高的價值。先進的人體工學設計、電動功能、氣候控制系統和優質材料不僅提升了駕駛室的價格,也有助於保障駕駛員的健康和持續提高生產力。

預計到2025年,亞太地區商用車座椅市佔率將達39%。該地區的領先地位得益於大規模的汽車製造、新興經濟體的基礎設施建設、成熟的汽車生產基地以及不斷成長的商務傳輸和出行服務需求的人口趨勢。都市區的成長推動了公共交通車隊和商用車投資的增加,從而持續帶動了全部區域對座椅系統的需求。

目錄

第1章調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率分析

- 成本結構

- 每個階段的附加價值

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 促進要素

- 對輕巧且符合人體工學的座椅的需求日益成長

- 嚴格的安全和排放氣體標準

- 電子商務和物流的成長

- 永續材料領域的進展

- 公共交通擴建與車隊現代化

- 產業潛在風險與挑戰

- 先進座椅技術高成本

- 供應鏈中斷

- 市場機遇

- 消費者對注重人體工學和舒適性的駕駛座的需求日益成長。

- 電動和自動駕駛商用車的普及率不斷提高

- 擴大公共交通和公車隊

- 模組化和折疊式座椅設計的興起

- 售後市場對替換零件的需求不斷成長

- 成長潛力分析

- 監管環境

- 北美洲

- 美國:FMVSS 207號-座椅系統

- 加拿大:CMVSS 208 - 正面碰撞中的乘員保護

- 歐洲

- 德國:ECE R17 - 座椅、座椅錨點、頭枕

- 英國:ECE R25 - 車輛座椅頭枕

- 法國:ECE R129 - 兒童限制系統(i-Size)

- 義大利:ECE R17 - 座椅、座椅錨點、頭枕

- 亞太地區

- 中國:GB 15083 - 汽車座椅強度要求及試驗方法

- 印度:AIS-023 - 商用車輛座椅、固定裝置和頭枕

- 日本:JASO D 601-商用車輛座椅

- 拉丁美洲

- 巴西:CONTRAN 第 780 號決議案-商用車輛安全標準

- 中東和非洲

- 阿拉伯聯合大公國:GSO 2014 - 機動車輛安全要求

- 北美洲

- 波特五力分析

- PESTEL 分析

- 技術與創新展望

- 當前技術趨勢

- 新興技術

- 生產統計

- 生產基地

- 消費基礎

- 出口和進口

- 定價分析

- 成本細分分析

- 專利分析

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

- 未來展望與投資機會

- 智慧互聯和車輛系統整合

- 疲勞和注意力分散檢測系統(整合式)

- 支援遠端資訊處理功能的座椅感測器生態系統

- ADAS整合:乘員偵測與安全氣囊最佳化

- 駕駛員健康分析與預測性健康監測

- 基於雲端的車隊智慧平台和表格數據分析

- 車輛電氣化對座椅系統的影響

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 企業擴張計畫和資金籌措

第5章 依座位容量分類的市場估算與預測,2022-2035年

- 駕駛座

- 乘客座椅

- 後座

- 折疊式座椅

第6章 按材料分類的市場估算與預測,2022-2035年

- 織物

- 乙烯基塑膠

- 皮革

- 合成材料

第7章 依車輛類型分類的市場估計與預測,2022-2035年

- 輕型商用車(LCV)

- 重型商用車(HCV)

- 公車和長途客車

第8章 按技術分類的市場估算與預測,2022-2035年

- 標準/傳統座位

- 電動座椅

- 加熱和通風座椅

- 記憶座椅

- 按摩座椅

第9章 依銷售管道分類的市場估計與預測,2022-2035年

- OEM

- 售後市場

第10章 2022-2035年各地區市場估計與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 比荷盧經濟聯盟

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 新加坡

- 泰國

- 印尼

- 越南

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥倫比亞

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章 公司簡介

- 世界玩家

- Adient

- Brose Fahrzeugteile

- Faurecia

- GRAMMER

- Hyundai Dymos

- Johnson Controls

- Lear

- Magna International

- RECARO Automotive Seating

- TS TECH

- Daimler

- Iveco

- 主要製造商(按地區分類)

- Dongfeng Auto Seating

- GRM Seating Solutions

- Kongsberg Automotive

- Seoyon E-Hwa

- Sogefi

- Sumitomo Riko

- Sundaram Clayton

- Tachi-S

- Toyota Boshoku

- Zhejiang Panyu-Jeep Vehicle

- 新興製造商

- Autofurn International

- Blitz

- Bostrom Seating Systems

- Firth Seating Technologies

- King Long Commercial Vehicle Seating

The Global Commercial Vehicle Seat Market was valued at USD 13.5 billion in 2025 and is estimated to grow at a CAGR of 4.5% to reach USD 20.7 billion by 2035.

Market development is increasingly influenced by the shift toward ergonomic, comfort-oriented seating solutions, as fleet operators prioritize driver well-being, efficiency, and long-term cost control. Poor seating design is widely recognized as a contributor to physical discomfort and reduced productivity, which has accelerated demand for seats that support posture, reduce fatigue, and improve daily driving conditions. Commercial vehicle seating has evolved beyond basic comfort to become a technology-enabled system integrated with vehicle electronics and driver monitoring platforms. Features such as powered adjustments, temperature-controlled seating, memory settings, and massage functions reflect a broader move toward higher-value interiors in commercial vehicles. The market is also benefiting from tighter global safety requirements covering seating performance, occupant protection, and material standards, which are pushing manufacturers toward more advanced designs. In parallel, the expansion of logistics, freight movement, and delivery services continues to stimulate demand for commercial vehicles worldwide, reinforcing steady growth in seating installations across new vehicle production and replacement cycles.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $13.5 Billion |

| Forecast Value | $20.7 Billion |

| CAGR | 4.5% |

The light commercial vehicles segment held a 57% share in 2025 and is expected to grow at a CAGR of 3.9% from 2026 to 2035. This leadership reflects their widespread use across delivery services, service-oriented businesses, and municipal operations. Vehicles in this category, with gross vehicle weights below 6,000 kilograms or 13,228 pounds, require seating that balances durability, resistance to wear, simplified adjustment mechanisms, and cost efficiency to meet the expectations of high-usage and budget-conscious operators.

The driver seat segment accounted for 46% share in 2025 and is forecast to register the fastest growth, with a CAGR of 4.8% from 2026 to 2035. Driver seats command a higher value due to their critical role in safety, comfort, and workforce retention. Advanced ergonomics, powered functionality, climate features, and premium materials contribute to stronger pricing while supporting operator health and sustained productivity.

Asia Pacific Commercial Vehicle Seat Market held a 39% share in 2025. The region's dominance is supported by large-scale vehicle manufacturing, infrastructure development across emerging economies, established automotive production bases, and demographic trends that are increasing demand for commercial transportation and mobility services. Rising urban populations are driving greater investment in public transport fleets and commercial vehicles, which continues to boost demand for seating systems across the region.

Key participants in the Global Commercial Vehicle Seat Market include Lear, Adient, GRAMMER, Faurecia, TS TECH, RECARO Automotive Seating, Hyundai Dymos, Johnson Controls, Daimler, and Iveco. Companies operating in the Global Commercial Vehicle Seat Market are reinforcing their market position through a combination of innovation, strategic partnerships, and global expansion. Manufacturers are investing heavily in research and development to enhance ergonomic performance, integrate smart features, and improve material durability while meeting evolving safety standards. Many players are aligning closely with vehicle OEMs to secure long-term supply agreements and participate early in platform development cycles. Expansion into high-growth regions and localization of production are being used to reduce costs and improve responsiveness to regional demand.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Seat

- 2.2.4 Material

- 2.2.5 Technology

- 2.2.6 Sales Channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1.1 Growth drivers

- 3.2.1.2 Rising demand for lightweight and ergonomic seating

- 3.2.1.3 Stringent safety and emission regulations

- 3.2.1.4 Growth in e-commerce and logistics

- 3.2.1.5 Advancements in sustainable materials

- 3.2.1.6 Expansion of public transportation and fleet modernization

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced seating technologies

- 3.2.2.2 Supply chain disruptions

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand for ergonomic and comfort-focused driver seats

- 3.2.3.2 Rising adoption of electric and autonomous commercial vehicles

- 3.2.3.3 Expansion of public transport and bus fleets

- 3.2.3.4 Increasing use of modular and folding seating designs

- 3.2.3.5 Strong aftermarket replacement demand

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 US: FMVSS No. 207 - seating systems

- 3.4.1.2 Canada: CMVSS 208 - occupant protection in frontal impacts

- 3.4.2 Europe

- 3.4.2.1 Germany: ECE R17 - seats, seat anchorages and head restraints

- 3.4.2.2 UK: ECE R25 - head restraints for vehicle seats

- 3.4.2.3 France: ECE R129 - Child Restraint Systems (i-Size)

- 3.4.2.4 Italy: ECE R17 - seats, seat anchorages and head restraints

- 3.4.3 Asia Pacific

- 3.4.3.1 China: GB 15083 - strength requirement and test of motor vehicle seats

- 3.4.3.2 India: AIS-023 - seats, their anchorages and head restraints for commercial vehicles

- 3.4.3.3 Japan: JASO D 601 - commercial vehicle seats

- 3.4.4 Latin America

- 3.4.4.1 Brazil: CONTRAN Resolution 780 - commercial vehicle safety standards

- 3.4.5 MEA

- 3.4.5.1 UAE: GSO 2014 - motor vehicle safety requirements

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Production statistics

- 3.8.1 Production hubs

- 3.8.2 Consumption hubs

- 3.8.3 Export and import

- 3.9 Pricing analysis

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Future outlook & investment opportunities

- 3.14 Smart Connectivity & Vehicle System Integration

- 3.14.1 Fatigue & distraction detection systems ( integration)

- 3.14.2 Telematics-enabled seat sensor ecosystems

- 3.14.3 ADAS Co-Integration: occupancy sensing & airbag optimization

- 3.14.4 Driver wellness analytics & predictive health monitoring

- 3.14.5 Cloud-based fleet intelligence platforms & seat data analytics

- 3.15 Vehicle electrification impact on seating systems

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Seat, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Driver seat

- 5.3 Passenger seat

- 5.4 Rear seat

- 5.5 Folding seat

Chapter 6 Market Estimates & Forecast, By Material, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Fabric

- 6.3 Vinyl

- 6.4 Leather

- 6.5 Synthetic materials

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Light commercial vehicles (LCV)

- 7.3 Heavy commercial vehicles (HCV)

- 7.4 Buses & coaches

Chapter 8 Market Estimates & Forecast, By Technology, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Standard/conventional seats

- 8.3 Powered/electric seats

- 8.4 Heated & ventilated seats

- 8.5 Memory seats

- 8.6 Massage seats

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.3.8 Benelux

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Singapore

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Colombia

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Adient

- 11.1.2 Brose Fahrzeugteile

- 11.1.3 Faurecia

- 11.1.4 GRAMMER

- 11.1.5 Hyundai Dymos

- 11.1.6 Johnson Controls

- 11.1.7 Lear

- 11.1.8 Magna International

- 11.1.9 RECARO Automotive Seating

- 11.1.10 TS TECH

- 11.1.11 Daimler

- 11.1.12 Iveco

- 11.2 Regional Players

- 11.2.1 Dongfeng Auto Seating

- 11.2.2 GRM Seating Solutions

- 11.2.3 Kongsberg Automotive

- 11.2.4 Seoyon E-Hwa

- 11.2.5 Sogefi

- 11.2.6 Sumitomo Riko

- 11.2.7 Sundaram Clayton

- 11.2.8 Tachi-S

- 11.2.9 Toyota Boshoku

- 11.2.10 Zhejiang Panyu-Jeep Vehicle

- 11.3 Emerging Players

- 11.3.1 Autofurn International

- 11.3.2 Blitz

- 11.3.3 Bostrom Seating Systems

- 11.3.4 Firth Seating Technologies

- 11.3.5 King Long Commercial Vehicle Seating

防撞飛機座椅市場規模、佔有率和成長分析:按平台類型、固定翼飛機座椅類型、固定翼飛機類型、固定翼飛機最終用戶和地區分類-2026-2033年產業預測

防撞飛機座椅市場規模、佔有率和成長分析:按平台類型、固定翼飛機座椅類型、固定翼飛機類型、固定翼飛機最終用戶和地區分類-2026-2033年產業預測 防撞飛機座椅市場報告:趨勢、預測與競爭分析(至2035年)

防撞飛機座椅市場報告:趨勢、預測與競爭分析(至2035年) 飛機座椅市場:2026-2032年全球市場預測(依座椅類型、飛機類型、材料類型、規格、飛機類型和最終用戶分類)

飛機座椅市場:2026-2032年全球市場預測(依座椅類型、飛機類型、材料類型、規格、飛機類型和最終用戶分類) 2026-2030年全球商用飛機座椅市場全球飛機睡衣市場(依材質、風格和通路分類)預測(2026-2032)

2026-2030年全球商用飛機座椅市場全球飛機睡衣市場(依材質、風格和通路分類)預測(2026-2032) 全球飛機座椅市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球飛機座椅市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 抗衝擊飛機座椅市場-全球產業規模、佔有率、趨勢、機會、預測:按產品、最終用戶、平台、地區和競爭對手分類,2021-2031年飛機座椅市場 - 全球產業規模、佔有率、趨勢、機會及預測(按飛機類型、艙位等級、座椅類型、銷售管道類型、地區和競爭格局分類,2021-2031年)

抗衝擊飛機座椅市場-全球產業規模、佔有率、趨勢、機會、預測:按產品、最終用戶、平台、地區和競爭對手分類,2021-2031年飛機座椅市場 - 全球產業規模、佔有率、趨勢、機會及預測(按飛機類型、艙位等級、座椅類型、銷售管道類型、地區和競爭格局分類,2021-2031年) 商用飛機客艙座椅市場規模、佔有率和成長分析(按艙位、座椅類型、組件和地區分類)-2026-2033年產業預測

商用飛機客艙座椅市場規模、佔有率和成長分析(按艙位、座椅類型、組件和地區分類)-2026-2033年產業預測 飛機座椅市場規模、佔有率和成長分析(按型號、組件、最終用戶和地區分類):產業預測(2026-2033 年)

飛機座椅市場規模、佔有率和成長分析(按型號、組件、最終用戶和地區分類):產業預測(2026-2033 年)