|

市場調查報告書

商品編碼

1913437

衛星通訊市場機會、成長要素、產業趨勢分析及2026年至2035年預測Satellite Communication (SATCOM) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

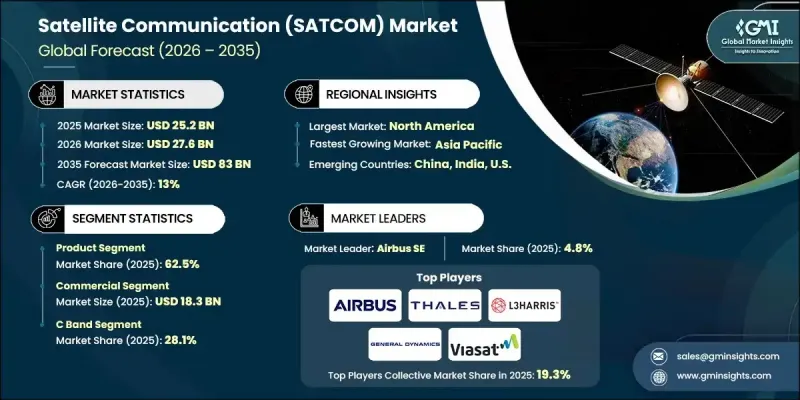

全球衛星通訊(SATCOM)市場預計到 2025 年將達到 252 億美元,到 2035 年將達到 830 億美元,年複合成長率為 13%。

市場成長的驅動力來自對不間斷連接日益成長的需求、緊湊型衛星網路的快速部署以及在地理環境惡劣地區對通訊存取日益成長的需求。連網設備和機器間通訊的日益普及持續推動著跨多個領域安全、即時資料傳輸的需求。由於僅靠地面網路無法提供穩定的覆蓋範圍,衛星通訊正成為全球數位基礎設施的關鍵組成部分。衛星平台正日益與下一代行動網路相融合,從而在傳統網路覆蓋受限的地區實現無縫連接。衛星架構和地面系統的持續技術創新正在提升容量、彈性和傳輸效率。此外,為了滿足機構和企業用戶等群體不斷變化的需求,人們越來越關注安全、高吞吐量的通訊能力。這些因素共同鞏固了衛星通訊作為擴展全球連結基礎技術的地位。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 252億美元 |

| 預測金額 | 830億美元 |

| 複合年成長率 | 13% |

預計到2025年,服務業規模將達到95億美元,並在2026年至2035年間以13.5%的複合年成長率成長。對持續高速通訊日益成長的依賴以及衛星服務的廣泛應用,正推動商業和機構用戶對衛星解決方案的依賴程度不斷提高。衛星技術的進步正在擴大其全球覆蓋範圍,從而推動對基於服務的產品和服務的需求。

2025年,C波段市佔率達28.1%。其強勁表現得益於其訊號傳輸穩定、覆蓋範圍廣、抗環境干擾能力強等優勢。隨著市場對可靠衛星廣播和連接解決方案的需求不斷成長,C波段在通訊網路中的廣泛應用將繼續鞏固其市場主導地位。

預計到2025年,北美衛星通訊(SATCOM)市佔率將達到45.6%。政府持續投資、服務不足地區對衛星寬頻需求的成長、對衛星緊急系統日益依賴,以及衛星平台與先進的無線技術的整合程度不斷提高,都是推動該地區成長的因素。對太空基礎設施的持續投資將鞏固該地區的長期主導。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段的附加價值

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 促進要素

- 對網路連線的需求不斷成長

- 開發小型衛星星系以增強通訊系統

- 偏遠地區對網路連結的需求日益成長

- 對物聯網和機器對機器(M2M)連接的需求日益成長

- 加強與5G網路的融合

- 產業潛在風險與挑戰

- 高成本和漫長的開發週期

- 太空碎片和軌道擁擠

- 市場機遇

- 對全球互聯互通的新需求

- 衛星小型化進展

- 促進要素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 新興經營模式

- 合規要求

- 國防預算分析

- 全球國防費用趨勢

- 區域國防預算分配

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 主要國防現代化項目

- 預算預測(2026-2035 年)

- 對產業成長的影響

- 各國國防預算

- 國防預算按部門分配

- 人員

- 運作/維護

- 採購

- 研究與發展、測試與評估

- 基礎設施和建築

- 技術與創新

- 供應鏈韌性

- 地緣政治分析

- 勞動力分析

- 數位轉型

- 併購和策略聯盟

- 風險評估與管理

- 重大合約授予(2022-2025)

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 市場集中度分析

- 按地區

- 主要企業的競爭標竿分析

- 財務績效比較

- 收入

- 利潤率

- 研究與開發

- 產品系列比較

- 產品線的廣度

- 科技

- 創新

- 地理分佈比較

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導企業

- 受讓人

- 追蹤者

- 小眾玩家

- 戰略展望矩陣

- 財務績效比較

- 重大進展

- 併購

- 夥伴關係與合作

- 技術進步

- 擴張與投資策略

- 永續發展計劃

- 數位轉型計劃

- 新興/Start-Ups競賽的趨勢

第5章 依解決方案分類的市場估算與預測,2022-2035年

- 產品

- 天線

- 相位陣列

- 主動電子掃描陣列(AESA)

- 數位波束形成(DBF)陣列

- 其他

- 收發器

- 發送器

- 接收器

- 功率放大器

- 轉換器

- 數據機/路由器

- 其他部分

- 天線

- 服務

- 工程與整合

- 安裝

- 物流和維護

第6章 2022-2035年各平台市場估算與預測

- 可攜式的

- 背負式

- 手持式

- 可部署/可飛行

- 陸地車輛

- 商用車輛/運輸

- 軍用車輛

- 無人地面車輛

- 固定於陸地

- 指揮控制中心

- 地球站/地面站

- 直播衛星電視

- 企業系統

- 機載

- 民航機

- 軍用機

- 無人駕駛飛行器(UAV)

- 海

- 商船

- 軍艦

第7章 依頻率分類的市場估計與預測,2022-2035年

- C波段

- S波段

- L波段

- X波段

- Ka波段

- Ku波段

- VHF/ UHF頻段

- EHF/SHF頻段

- 其他

第8章 2022-2035年各產業市場估算與預測

- 商業的

- 電信/蜂窩回程傳輸

- 媒體與娛樂

- 運輸/物流

- 科學研究與開發

- 航空

- 海上

- 零售和消費品

- 其他

- 政府/國防

第9章 2022-2035年各地區市場估算與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- 主要企業

- Airbus SE

- Intelsat SA

- Space Exploration Technologies Corp.

- SES SA

- 按地區分類的主要企業

- 北美洲

- General Dynamics Mission Systems

- L3Harris Technologies

- Viasat

- EchoStar Mobile

- 亞太地區

- China Aerospace Science and Technology Corporation(CASC)

- SKY Perfect JSAT Holdings Inc.

- Intellian Technologies

- 歐洲

- Thales

- Gilat Satellite Networks

- SES SA

- 北美洲

- 小眾玩家/顛覆者

- AvL Technologies

- Cobham Satcom

- Maxar Technologies Inc.

- Honeywell

- Viking Satcom

- Thuraya Telecommunications Company(Yashat)

- Iridium Communications

- Telesat Corporation

- Holkirk Communications

The Global Satellite Communication (SATCOM) Market was valued at USD 25.2 billion in 2025 and is estimated to grow at a CAGR of 13% to reach USD 83 billion by 2035.

Market momentum is supported by the accelerating need for uninterrupted connectivity, the rapid deployment of compact satellite networks, and rising demand for communication access in geographically challenging regions. Increasing adoption of connected devices and machine-based communication continues to elevate demand for secure, real-time data transmission across multiple sectors. Satellite communication is becoming a critical component of global digital infrastructure as terrestrial networks alone are unable to provide consistent coverage. Integration between satellite platforms and next-generation mobile networks is gaining traction, enabling seamless connectivity where traditional networks remain limited. Ongoing innovation within satellite architecture and ground systems is improving capacity, resilience, and transmission efficiency. The industry is also witnessing heightened focus on secure and high-throughput communication capabilities, particularly to meet the evolving requirements of institutional and enterprise users. These combined factors continue to reinforce satellite communication as a foundational technology for global connectivity expansion.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $25.2 Billion |

| Forecast Value | $83 Billion |

| CAGR | 13% |

The services segment was valued at USD 9.5 billion in 2025 and is expected to grow at a CAGR of 13.5% during 2026-2035. Rising dependence on continuous, high-speed communication and broader accessibility of satellite-enabled services are increasing reliance on satellite-based solutions across commercial and institutional users. Advancements in satellite technology have expanded global reach, strengthening demand for service-based offerings.

The C-band segment held a 28.1% share in 2025. Its strong performance is supported by stable signal transmission, long-range coverage, and reduced sensitivity to environmental interference. Established adoption across communication networks continues to support its dominance as demand rises for dependable satellite broadcasting and connectivity solutions.

North America Satellite Communication (SATCOM) Market accounted for 45.6% share in 2025. Regional growth is driven by sustained government investment, expanding satellite broadband demand in underserved areas, increasing reliance on satellite-enabled emergency systems, and growing integration between satellite platforms and advanced wireless technologies. Continued investment in space infrastructure supports long-term regional leadership.

Key companies operating in the Global Satellite Communication (SATCOM) Market include Viasat, Thales, SES S.A., Iridium Communications, Airbus SE, Honeywell, Intelsat S.A., L3Harris Technologies, Space Exploration Technologies Corp., Telesat Corporation, Gilat Satellite Networks, Maxar Technologies Inc., General Dynamics Mission Systems, Intellian Technologies, Cobham Satcom, SKY Perfect JSAT Holdings Inc., Thuraya Telecommunications Company (Yashat), Viking Satcom, AvL Technologies, EchoStar Mobile, ASELSAN, Holkirk Communications, and China Aerospace Science and Technology Corporation (CASC). Companies in the Global Satellite Communication (SATCOM) Market strengthen their market position through continuous investment in advanced satellite architectures and next-generation network integration. Firms focus on expanding high-capacity satellite constellations to improve coverage, resilience, and data throughput. Strategic partnerships with network operators and government agencies support long-term contract stability.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Solution trends

- 2.2.2 Platform trends

- 2.2.3 Frequency trends

- 2.2.4 Industrial vertical trends

- 2.2.5 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of internet connectivity demand

- 3.2.1.2 Development of small satellite constellations to enhance communication systems

- 3.2.1.3 Increase demand for connectivity in remote areas

- 3.2.1.4 Rising demand for IoT and M2M connectivity

- 3.2.1.5 Growing integration with 5G networks

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High costs and long development cycles

- 3.2.2.2 Space debris and orbital congestion

- 3.2.3 Market opportunities

- 3.2.3.1 Emerging demand for global connectivity

- 3.2.3.2 Advancements in satellite miniaturization

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging business models

- 3.9 Compliance requirements

- 3.10 Defense Budget Analysis

- 3.11 Global Defense Spending Trends

- 3.12 Regional Defense Budget Allocation

- 3.12.1 North America

- 3.12.2 Europe

- 3.12.3 Asia Pacific

- 3.12.4 Middle East and Africa

- 3.12.5 Latin America

- 3.13 Key Defense Modernization Programs

- 3.14 Budget Forecast (2026-2035)

- 3.14.1 Impact on Industry Growth

- 3.14.2 Defense Budgets by Country

- 3.14.3 Defense Budget Allocation by Segment

- 3.14.3.1 Personnel

- 3.14.3.2 Operations and Maintenance

- 3.14.3.3 Procurement

- 3.14.3.4 Research, Development, Test and Evaluation

- 3.14.3.5 Infrastructure and Construction

- 3.14.3.6 Technology and Innovation

- 3.15 Supply Chain Resilience

- 3.16 Geopolitical Analysis

- 3.17 Workforce Analysis

- 3.18 Digital Transformation

- 3.19 Mergers, Acquisitions, and Strategic Partnerships Landscape

- 3.20 Risk Assessment and Management

- 3.21 Major Contract Awards (2022-2025)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market Concentration Analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Solution, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Product

- 5.2.1 Antennas

- 5.2.1.1 Phased arrays

- 5.2.1.2 Active electronically scanned array (AESA)

- 5.2.1.3 Digital beam forming (DBF) array

- 5.2.1.4 Others

- 5.2.2 Transceivers

- 5.2.2.1 Transmitters

- 5.2.2.2 Receivers

- 5.2.2.3 Power amplifiers

- 5.2.2.4 Converters

- 5.2.2.5 Modem & routers

- 5.2.2.6 Other component

- 5.2.1 Antennas

- 5.3 Services

- 5.3.1 Engineering & integration

- 5.3.2 Installation

- 5.3.3 Logistics & maintenance

Chapter 6 Market Estimates and Forecast, By Platform, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Portable

- 6.2.1 Manpack

- 6.2.2 Handheld

- 6.2.3 Deployable/flyaway

- 6.3 Land mobile

- 6.3.1 Commercial vehicles/transport

- 6.3.2 Military vehicles

- 6.3.3 Unmanned ground vehicles

- 6.4 Land fixed

- 6.4.1 Command & control centers

- 6.4.2 Earth stations/ground station

- 6.4.3 Direct to home (DTH)/satellite tv

- 6.4.4 Enterprise Systems

- 6.5 Airborne

- 6.5.1 Commercial aircraft

- 6.5.2 Military aircraft

- 6.5.3 Unmanned aerial vehicles (UAVs)

- 6.6 Maritime

- 6.6.1 Commercial ships

- 6.6.2 Military ships

Chapter 7 Market Estimates and Forecast, By Frequency, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 C Band

- 7.3 S Band

- 7.4 L Band

- 7.5 X Band

- 7.6 Ka Band

- 7.7 Ku Band

- 7.8 VHF/UHF Band

- 7.9 EHF/SHF Band

- 7.10 Others

Chapter 8 Market Estimates and Forecast, By Industry Vertical, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Commercial

- 8.2.1 Telecommunication & cellular backhaul

- 8.2.2 Media & entertainment

- 8.2.3 Transportation & logistics

- 8.2.4 Scientific research & development

- 8.2.5 Aviation

- 8.2.6 Marine

- 8.2.7 Retail & consumer

- 8.2.8 Others

- 8.3 Government & defense

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Airbus SE

- 10.1.2 Intelsat S.A.

- 10.1.3 Space Exploration Technologies Corp.

- 10.1.4 SES S.A.

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 General Dynamics Mission Systems

- 10.2.1.2 L3Harris Technologies

- 10.2.1.3 Viasat

- 10.2.1.4 EchoStar Mobile

- 10.2.2 Asia Pacific

- 10.2.2.1 China Aerospace Science and Technology Corporation (CASC)

- 10.2.2.2 SKY Perfect JSAT Holdings Inc.

- 10.2.2.3 Intellian Technologies

- 10.2.3 Europe

- 10.2.3.1 Thales

- 10.2.3.2 Gilat Satellite Networks

- 10.2.3.3 SES S.A.

- 10.2.1 North America

- 10.3 Niche Players/Disruptors

- 10.3.1 AvL Technologies

- 10.3.2 Cobham Satcom

- 10.3.3 Maxar Technologies Inc.

- 10.3.4 Honeywell

- 10.3.5 Viking Satcom

- 10.3.6 Thuraya Telecommunications Company (Yashat)

- 10.3.7 Iridium Communications

- 10.3.8 Telesat Corporation

- 10.3.9 Holkirk Communications

軍用商業衛星通訊:趨勢與預測(2024-2034)

軍用商業衛星通訊:趨勢與預測(2024-2034) 中東衛星通訊市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

中東衛星通訊市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年) 日本衛星通訊市場報告(按類型(地面設備、服務)、平台(攜帶式、陸地、海上、機載)、最終用戶垂直產業(海事、國防和政府、企業、媒體和娛樂及其他)以及地區分類,2026-2034 年)衛星通訊:物聯網部署與訂閱

日本衛星通訊市場報告(按類型(地面設備、服務)、平台(攜帶式、陸地、海上、機載)、最終用戶垂直產業(海事、國防和政府、企業、媒體和娛樂及其他)以及地區分類,2026-2034 年)衛星通訊:物聯網部署與訂閱 2025年極地衛星通訊全球市場報告2025年全球軟體定義衛星市場報告2025年立方衛星下行鏈路服務全球市場報告

2025年極地衛星通訊全球市場報告2025年全球軟體定義衛星市場報告2025年立方衛星下行鏈路服務全球市場報告 M2M衛星通訊市場:2025-2032年全球預測(依產業、應用、平台類型、頻寬及服務類型分類)

M2M衛星通訊市場:2025-2032年全球預測(依產業、應用、平台類型、頻寬及服務類型分類) 衛星IoT通訊的全球市場 - 第5版衛星通訊市場按組件、通訊類型、分析技術、衛星類型、頻段、應用和最終用戶分類-2025-2032年全球預測

衛星IoT通訊的全球市場 - 第5版衛星通訊市場按組件、通訊類型、分析技術、衛星類型、頻段、應用和最終用戶分類-2025-2032年全球預測