|

市場調查報告書

商品編碼

1913398

汽車輪胎充氣機市場:市場機會、成長促進因素、產業趨勢分析及預測(2026-2035)Automotive Tire Inflator Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

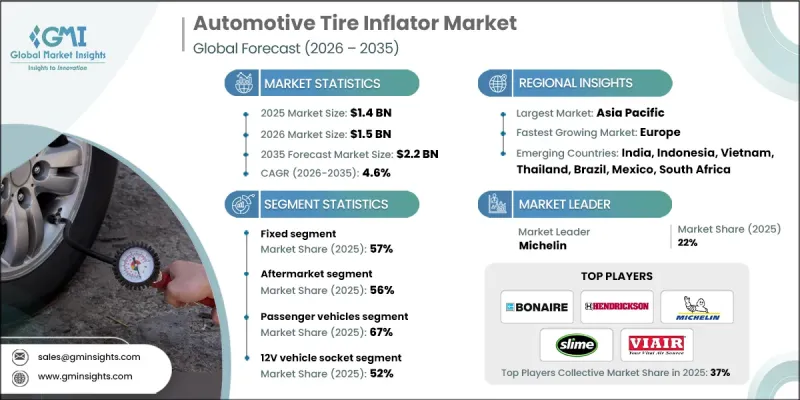

全球汽車輪胎充氣機市場預計到 2025 年將達到 14 億美元,到 2035 年將達到 22 億美元,年複合成長率為 4.6%。

汽車輪胎充氣裝置在維持適當的輪胎氣壓方面發揮著至關重要的作用,這直接關係到車輛的效率、行駛安全性和整體性能。該市場涵蓋固定式和攜帶式解決方案,可透過車輛電源插座、可充電電池系統或直接電源連接供電。產品種類繁多,從基本的充氣裝置到具有自動壓力調節和監控功能的攜帶式控制系統,應有盡有。技術進步正在重塑市場格局,數位化介面、自動斷電功能和智慧壓力控制等技術的進步提高了易用性和精度。成長趨勢反映了成熟市場(以替換需求為主導)與新興市場(車輛保有量不斷成長,持續創造新機會)之間的對比。不斷變化的消費者期望、日益嚴格的安全標準以及零售通路的數位化程度不斷提高,都在影響消費者的購買行為。這些因素共同作用,持續重塑全球汽車生態系統中的產品創新、可近性和普及性。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 14億美元 |

| 市場規模預測 | 22億美元 |

| 複合年成長率 | 4.6% |

預計到2025年,固定式充氣機市佔率將達57%,2026年至2035年複合年成長率將達4.2%。這些系統專為連續、高強度使用而設計,通常安裝在專業和工業環境中。其性能穩定,不受功率限制,並且能夠承受嚴苛的運行要求,這些優勢使其在市場上佔據主導地位。

預計到2025年,售後市場將佔據56%的市場佔有率,並在2035年之前以4.8%的最高複合年成長率成長。消費者對替換件和產品升級的強勁需求,以及線上銷售管道的拓展,持續推動市場成長。此細分市場滿足了用戶對更高功能性、更強便攜性或多輛車用充氣幫浦的需求。

預計到2025年,中國汽車輪胎充氣機市場將佔全球38%的佔有率,市場規模達5.417億美元。新興經濟體汽車保有量的成長、消費者在汽車配件上的支出增加、零售網路的擴張以及汽車保養意識的提高,都支撐了中國在該地區主導地位。

目錄

第1章:分析方法和範圍

第2章執行摘要

第3章業界考察

- 產業生態系分析

- 供應商情況

- 利潤率分析

- 成本結構

- 每個階段的附加價值

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 促進要素

- 提高輪胎安全意識

- 對攜帶式和緊湊型解決方案的需求

- 冒險和越野活動的興起

- 隨著汽車擁有量的增加,對輪胎充氣幫浦的需求也隨之增加。

- 電子商務的發展提高了產品供應量和市場覆蓋範圍。

- 產業潛在風險與挑戰

- 先進型號的初始成本較高

- 替代輪胎維修解決方案的競爭格局

- 市場機遇

- 對智慧數位輪胎充氣泵的需求日益成長

- 無線和可充電充氣幫浦越來越受歡迎

- 新興市場汽車銷售上升

- 適用於沒有備胎的車輛的原廠配套產品

- 拓展電子商務和直接面向銷售管道

- 促進要素

- 成長潛力分析

- 監管環境

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 生產統計

- 生產基地

- 消費基礎

- 進出口

- 定價分析

- 按地區

- 依產品

- 成本細分分析

- 專利分析

- 永續性和環境方面

- 永續努力

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

- 未來展望與投資機會

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 主要企業的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 主要趨勢

- 企業合併(M&A)

- 商業夥伴關係與合作

- 新產品發布

- 企業擴張計畫和資金籌措

第5章 按產品分類的市場估算與預測(2022-2035 年)

- 固定式

- 攜帶式的

第6章 依車輛類型分類的市場估計與預測(2022-2035 年)

- 搭乘用車

- 掀背車

- 轎車

- SUV

- 商用車輛

- 輕型商用車(LCV)

- 中型商用車(MCV)

- 重型商用車(HCV)

- 摩托車

- 電動車

- 越野車(ATV/UTV)

第7章 按銷售管道分類的市場估算與預測(2022-2035 年)

- OEM

- 固定式

- 攜帶式的

- 售後市場

- 固定式

- 攜帶式的

第8章 按應用領域分類的市場估算與預測(2022-2035 年)

- 家用

- 商業的

- 工業的

第9章 按組件分類的市場估計和預測(2022-2035 年)

- ECU

- 壓縮機

- 壓力感測器

- 其他

第10章 依能源類型分類的市場估算與預測(2022-2035 年)

- 12V汽車插座

- 可充電電池(鋰離子電池)

- 直流電源

- 其他

第11章 各地區市場估計與預測(2022-2035 年)

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 比荷盧經濟聯盟國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 新加坡

- 泰國

- 印尼

- 越南

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥倫比亞

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第12章:公司簡介

- 國際公司

- Berkshire Hathaway

- BLACK+DECKER

- CRAFTSMAN

- ITW Global Tire Repair

- Marmon Holdings

- MAT Industries

- Michelin

- Slime

- STEMCO Products

- VIAIR

- 本地公司

- Airtec

- BONAIRE Industries

- Coido

- Guangzhou Meitun Electronic Commerce

- Hendrickson USA

- Kensun

- Nova Gas Techniques

- Pressure Systems International

- PressureGuard

- TIRETEK

- 新興企業

- Alpha Catalyst Consulting

- Alto Ride

- Kstar New Energy

- Stealth Electric Outboards

- TEMO

The Global Automotive Tire Inflator Market was valued at USD 1.4 billion in 2025 and is estimated to grow at a CAGR of 4.6% to reach USD 2.2 billion by 2035.

Automotive tire inflators play an essential role in maintaining correct tire pressure, which directly supports vehicle efficiency, driving safety, and overall performance. The market includes both stationary and portable solutions designed to operate through vehicle power outlets, rechargeable battery systems, or direct electrical connections. Product offerings range from basic air inflation units to digitally controlled systems equipped with automated pressure regulation and monitoring capabilities. Technological progress has reshaped the market, with digital interfaces, automated shut-off functions, and intelligent pressure control improving usability and accuracy. Growth trends reflect a contrast between mature markets, where replacement demand is dominant, and developing regions, where rising vehicle ownership continues to create new opportunities. Shifting consumer expectations, tighter safety standards, and the increasing digitization of retail channels are influencing purchasing behavior. Together, these factors continue to redefine product innovation, accessibility, and adoption across global automotive ecosystems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.4 Billion |

| Forecast Value | $2.2 Billion |

| CAGR | 4.6% |

The fixed inflator segment accounted for 57% share in 2025 and is projected to grow at a CAGR of 4.2% from 2026 to 2035. These systems are designed for continuous, high-capacity usage and are commonly installed in professional and industrial environments. Their ability to deliver consistent performance without power limitations and withstand heavy operational demands supports their leading market position.

The aftermarket segment held 56% share in 2025 and is expected to grow at the fastest CAGR of 4.8% through 2035. Strong consumer demand for replacement units and product upgrades, combined with the expansion of online sales channels, continues to drive growth. This segment serves users seeking improved functionality, portability, or additional inflators for multiple vehicles.

China Automotive Tire Inflator Market held a 38% share in 2025, generating USD 541.7 million. Regional leadership is supported by rising vehicle ownership, increasing consumer spending on automotive accessories, expanding retail networks, and growing awareness of vehicle care across emerging economies.

Key companies active in the Global Automotive Tire Inflator Market include Michelin, VIAIR, Slime, ITW Global Tire Repair, Kensun, Marmon Holdings, BONAIRE Industries, Hendrickson USA, TIRETEK, and Guangzhou Meitun Electronic Commerce. Companies operating in the Global Automotive Tire Inflator Market strengthen their competitive position through continuous product innovation and portfolio expansion. Manufacturers focus on integrating digital controls, smart sensors, and automated features to improve accuracy and ease of use. Expanding presence across online and offline distribution channels helps brands reach a wider customer base. Strategic pricing across basic and premium product lines supports diverse consumer needs. Firms also emphasize product durability and compliance with safety standards to build long-term trust. Partnerships with automotive retailers and investments in brand visibility further enhance market penetration.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Vehicles

- 2.2.4 Application

- 2.2.5 Power Source

- 2.2.6 Component

- 2.2.7 Sales Channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1.1 Growth drivers

- 3.2.1.2 Rising awareness about tire safety

- 3.2.1.3 Demand for portable and compact solutions

- 3.2.1.4 Rise in adventure and off-road activities

- 3.2.1.5 Rising vehicle ownership is increasing demand for tire inflators

- 3.2.1.6 Growth of e-commerce is improving product availability and market reach

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial cost of advanced models

- 3.2.2.2 Competition of alternative tire repair solutions

- 3.2.3 Market opportunities

- 3.2.3.1 Rising demand for smart and digital tire inflators

- 3.2.3.2 Growing adoption of cordless and rechargeable inflators

- 3.2.3.3 Increasing vehicle sales in emerging markets

- 3.2.3.4 OEM fitment in vehicles without spare tires

- 3.2.3.5 Expansion of e-commerce and direct-to-consumer channels

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Production statistics

- 3.8.1 Production hubs

- 3.8.2 Consumption hubs

- 3.8.3 Export and import

- 3.9 Pricing analysis

- 3.9.1 By region

- 3.9.2 By product

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Future outlook & investment opportunities

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Product, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Fixed

- 5.3 Portable

Chapter 6 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger vehicles

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUVS

- 6.3 Commercial vehicles

- 6.3.1 Light commercial vehicles (LCV)

- 6.3.2 Medium commercial vehicles (MCV)

- 6.3.3 Heavy commercial vehicles (HCV)

- 6.4 Two-wheelers

- 6.5 Electric vehicles

- 6.6 Off-Road Vehicles (ATV/UTV)

Chapter 7 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 OEM

- 7.2.1 Fixed

- 7.2.2 Portable

- 7.3 Aftermarket

- 7.3.1 Fixed

- 7.3.2 Portable

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Household

- 8.3 Commercial

- 8.4 Industrial

Chapter 9 Market Estimates & Forecast, By Component, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 ECU

- 9.3 Compressor

- 9.4 Pressure sensor

- 9.5 Others

Chapter 10 Market Estimates & Forecast, By Power Source, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 12V Vehicle Socket

- 10.3 Rechargeable Battery (Li-ion)

- 10.4 Direct AC Power

- 10.5 Other

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.3.8 Benelux

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Singapore

- 11.4.7 Thailand

- 11.4.8 Indonesia

- 11.4.9 Vietnam

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Colombia

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global Players

- 12.1.1 Berkshire Hathaway

- 12.1.2 BLACK+DECKER

- 12.1.3 CRAFTSMAN

- 12.1.4 ITW Global Tire Repair

- 12.1.5 Marmon Holdings

- 12.1.6 MAT Industries

- 12.1.7 Michelin

- 12.1.8 Slime

- 12.1.9 STEMCO Products

- 12.1.10 VIAIR

- 12.2 Regional Players

- 12.2.1 Airtec

- 12.2.2 BONAIRE Industries

- 12.2.3 Coido

- 12.2.4 Guangzhou Meitun Electronic Commerce

- 12.2.5 Hendrickson USA

- 12.2.6 Kensun

- 12.2.7 Nova Gas Techniques

- 12.2.8 Pressure Systems International

- 12.2.9 PressureGuard

- 12.2.10 TIRETEK

- 12.3 Emerging Players

- 12.3.1 Alpha Catalyst Consulting

- 12.3.2 Alto Ride

- 12.3.3 Kstar New Energy

- 12.3.4 Stealth Electric Outboards

- 12.3.5 TEMO

全球汽車自動輪胎壓力調節系統(ATIS)市場

全球汽車自動輪胎壓力調節系統(ATIS)市場 自動輪胎充氣系統市場:按車輛類型、技術、系統類型、最終用戶和分銷管道分類-2026-2032年全球市場預測

自動輪胎充氣系統市場:按車輛類型、技術、系統類型、最終用戶和分銷管道分類-2026-2032年全球市場預測 自動輪胎充氣系統市場:按類型、車輛類型、銷售管道和地區分類汽車自動胎壓調節系統市場:按類型、組件、輪胎類型、車輛類型、最終用戶和分銷管道分類 - 全球預測 2026-2032

自動輪胎充氣系統市場:按類型、車輛類型、銷售管道和地區分類汽車自動胎壓調節系統市場:按類型、組件、輪胎類型、車輛類型、最終用戶和分銷管道分類 - 全球預測 2026-2032 汽車自動胎壓調節系統市場規模、佔有率及成長分析(依車輛類型、類型、銷售管道及地區分類)-2026-2033年產業預測

汽車自動胎壓調節系統市場規模、佔有率及成長分析(依車輛類型、類型、銷售管道及地區分類)-2026-2033年產業預測 汽車自動輪胎充氣系統市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、銷售管道、車輛類型、地區和競爭格局分類,2020-2030 年預測全球汽車輪胎充氣機市場

汽車自動輪胎充氣系統市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、銷售管道、車輛類型、地區和競爭格局分類,2020-2030 年預測全球汽車輪胎充氣機市場 汽車自動輪胎充氣系統:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)

汽車自動輪胎充氣系統:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年) 自動輪胎充氣系統市場(按類型、組件、車輛類型和地區)2026 年至 2032 年

自動輪胎充氣系統市場(按類型、組件、車輛類型和地區)2026 年至 2032 年 汽車自動輪胎充氣系統市場規模、佔有率、趨勢分析報告:按類型、按車輛、按組件、按銷售管道、按地區、細分市場預測,2024-2030年

汽車自動輪胎充氣系統市場規模、佔有率、趨勢分析報告:按類型、按車輛、按組件、按銷售管道、按地區、細分市場預測,2024-2030年