|

市場調查報告書

商品編碼

1892903

汽車側簾式氣囊市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)Automotive Curtain Airbags Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

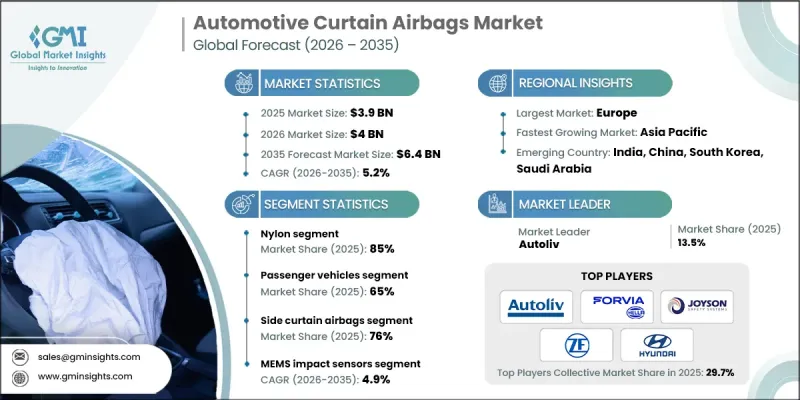

2025 年全球汽車側簾式安全氣囊市場價值為 39 億美元,預計到 2035 年將以 5.2% 的複合年成長率成長至 64 億美元。

SUV和跨界車銷售的穩定成長是主要驅動力,因為更寬敞的座艙和更高的車頂線條增加了對頭部保護系統的需求。汽車製造商正逐步將側簾式氣囊作為標準配置,使全球消費者都能以具競爭力的價格獲得先進的安全解決方案。電動車滑板式平台的演進正在重塑車輛架構,影響感測器和安全系統的佈局。這種轉變使得側簾式氣囊能夠更好地整合,促使供應商設計更輕巧、更緊湊的充氣式氣囊,並採用更先進的紡織材料,以便在日益狹小的座艙空間內提供強力的保護。隨著全球多個地區法規的日益嚴格,汽車製造商幾乎必須在所有車型級別中提供側面碰撞保護。消費者對車輛安全的日益關注也促使汽車製造商透過配備符合地區標準的先進被動安全系統來打造差異化產品線,從而吸引那些優先考慮全面乘員保護的消費者。

| 市場範圍 | |

|---|---|

| 起始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 39億美元 |

| 預測值 | 64億美元 |

| 複合年成長率 | 5.2% |

到2025年,尼龍材料市佔率將達到85%,預計到2035年將以4.2%的複合年成長率成長。未來,尼龍-聚酯混紡織物、新一代尼龍配方以及生物基聚醯胺的研發有望在提升性能的同時,協助實現永續發展目標。纖維化學的進步正不斷縮小尼龍與其他替代材料之間的性能差距。

2025年,乘用車細分市場佔據65%的市場佔有率,預計2026年至2035年將以5.5%的複合年成長率成長。不同車型等級的應用模式有所不同:高階車型普遍採用側簾式氣囊系統,而中階車型則迅速普及。入門級市場仍面臨成本限制,但隨著監管要求的加強以及全球消費者對安全性的日益重視,整體應用率正在上升。

預計到2025年,美國汽車側簾式氣囊市場規模將達8.715億美元。監管機構不斷提高側面碰撞和彈射保護測試的要求,鼓勵製造商採用更先進的側簾式氣囊,這些氣囊針對大型SUV和皮卡進行了最佳化。與早期設計相比,這些升級後的系統覆蓋範圍更廣,翻滾保護性能更佳。

目錄

第1章:方法論

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率分析

- 成本結構

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 越來越重視乘員安全合規性

- SUV和跨界車的普及率不斷上升

- 自適應安全氣囊系統的技術進步

- 新興汽車產業中心的生產擴張

- 轉向永續材料

- 產業陷阱與挑戰

- 高系統整合度和組件成本

- 新興市場安全監管有限

- 市場機遇

- 自動駕駛和半自動駕駛汽車的成長

- 售後市場更換和召回驅動的需求

- 拓展至商用車和車隊領域

- 以永續發展為導向的採購轉變

- 成長促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 美國-FMVSS 214側撞保護

- 加拿大 - CMVSS 214 側碰撞保護

- 歐洲

- 德國-聯合國第135號法規規定的桿側碰撞保護

- 英國-聯合國歐洲經濟委員會第95號法規側向衝擊保護

- 法國-歐盟通用安全法規 2019/2144

- 義大利-聯合國第21號法規室內配件安全

- 西班牙-歐盟法規 661/2009 通用車輛安全

- 亞太地區

- 中國GB 20071側撞保護

- 印度-AIS-099 側面碰撞法規

- 日本新車安全評鑑協會(JNCAP)側面撞擊安全性能測試規程

- 澳洲-ADR 72 側面碰撞保護

- 韓國KMVSS側撞保護

- 拉丁美洲

- 巴西-Contran 決議 518 側面碰撞保護

- 墨西哥-NOM-194-SCFI車輛安全標準

- 阿根廷-IRAM-AITA 1-20 側面碰撞標準

- 中東和非洲

- 南非-SANS 20079 側撞保護

- 沙烏地阿拉伯-SASO 2915車輛安全法規

- 阿拉伯聯合大公國-阿拉伯聯合大公國.S 5010-5 車輛碰撞保護

- 土耳其-聯合國歐洲經濟委員會第95號法規側面撞擊保護

- 北美洲

- 波特的分析

- PESTEL 分析

- 技術與創新格局

- 目前技術

- 新興技術

- 價格趨勢

- 依產品

- 按地區

- 生產統計

- 生產中心

- 消費中心

- 進出口

- 成本細分分析

- 專利分析

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

- 未來市場展望及機遇

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃和資金

第5章:市場估算與預測:依類型分類,2022-2035年

- 側簾式氣囊

- 尼龍

- 聚酯纖維

- 前側簾式氣囊

- 尼龍

- 聚酯纖維

- 後排側簾式氣囊

- 尼龍

- 聚酯纖維

第6章:市場估算與預測:依材料分類,2022-2035年

- 尼龍

- 聚酯纖維

第7章:市場估算與預測:依感測器類型分類,2022-2035年

- MEMS衝擊感測器

- 翻滾陀螺儀感應器

- 統一安全ECU

第8章:市場估算與預測:依車輛類型分類,2022-2035年

- 搭乘用車

- 掀背車

- 轎車

- SUV

- 商用車輛

- 輕型商用車(LCV)

- 中型商用車(MCV)

- 重型商用車輛(HCV)

第9章:市場估算與預測:依銷售管道分類,2021-2034年

- OEM

- 售後市場

第10章:市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐

- 葡萄牙

- 克羅埃西亞

- 比荷盧經濟聯盟

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 新加坡

- 泰國

- 印尼

- 越南

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

第11章:公司簡介

- 全球參與者

- Autoliv

- ZF Friedrichshafen

- Joyson Safety Systems

- Continental

- Hyundai

- Toyoda Gosei

- Daicel

- Bosch Passive Safety Systems

- Magna International

- Denso

- Valeo

- Delphi Automotive / BorgWarner

- 區域玩家

- Forvia Hella

- Kolon Industries

- Nihon Plast

- Porcher Industries

- Toray Industries

- Sumitomo

- SEIREN

- Toyota Boshoku

- Ashimori Industry

- U-Shin

- 新興及小眾玩家

- Yanfeng Automotive Trim Systems

- Wuhu Ruili Automobile Airbag

- ARC Automotive

- Tata AutoComp Systems

- Ningbo Joyson Electronic

- Changzhou Changrui

The Global Automotive Curtain Airbags Market was valued at USD 3.9 billion in 2025 and is estimated to grow at a CAGR of 5.2% to reach USD 6.4 billion by 2035.

Steady growth in SUV and crossover sales is a major driver, as wider cabins and taller rooflines increase the need for head protection systems. Automakers are progressively equipping more vehicles with curtain airbags as standard features, making advanced safety solutions available at competitive pricing worldwide. The evolution of EV skateboard platforms is reshaping vehicle architecture, influencing how sensors and safety systems are positioned. This shift enables better integration of curtain airbags, prompting suppliers to engineer lighter, compact inflatable designs and improved textile materials capable of providing strong protection in increasingly constrained cabin spaces. With global regulations tightening across multiple regions, OEMs are required to deliver side-impact protection across nearly all vehicle classes. Rising consumer focus on vehicle safety is also pushing automakers to differentiate their lineups with advanced passive safety systems that comply with regional standards and appeal to buyers who prioritize comprehensive occupant protection.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.9 Billion |

| Forecast Value | $6.4 Billion |

| CAGR | 5.2% |

The nylon material segment accounted for an 85% share in 2025 and is projected to grow at a CAGR of 4.2% through 2035. Future developments in nylon-polyester hybrids, next-generation nylon formulations, and bio-based polyamides are expected to improve performance while addressing sustainability goals. Advancements in fiber chemistry continue to narrow the performance gap between nylon and alternative materials.

The passenger vehicle segment held a 65% share in 2025 and is anticipated to grow at a CAGR of 5.5% from 2026 to 2035. Adoption patterns vary depending on vehicle class: high-end models have widespread use of curtain airbag systems, while mid-range vehicles have seen rapid integration. Entry-level markets still face cost limitations, but overall adoption is rising as regulatory requirements strengthen and as safety becomes a higher priority among consumers worldwide.

US Automotive Curtain Airbags Market reached USD 871.5 million in 2025. Regulatory authorities have been expanding requirements for side-impact and ejection mitigation testing, encouraging manufacturers to adopt more advanced curtain airbags optimized for larger SUVs and pickup trucks. These updated systems offer broader coverage and better rollover performance than earlier designs.

Key companies operating in the Automotive Curtain Airbags Market include Autoliv, Continental, Hella, Hyundai, Joyson Safety Systems, Kolon Industries, Neaton Auto Products Manufacturing, Toyoda Gosei, and ZF Friedrichshafen. Companies within the Automotive Curtain Airbags Market are strengthening their competitive presence by advancing material technology, reducing system weight, and developing compact inflators that improve deployment efficiency. Many manufacturers are collaborating closely with automakers to design airbag systems tailored to new EV platforms and evolving vehicle geometries. Investments in improved textile engineering, enhanced sensor integration, and high-performance inflator mechanisms form a major part of ongoing R&D. Firms are also prioritizing compliance with global regulatory updates to secure broader OEM adoption. Expanding production capacity in strategic regions, focusing on cost-efficient manufacturing, and ensuring consistent quality control help companies maintain strong international footprints.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2022-2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Material

- 2.2.4 Sensor

- 2.2.5 Vehicle

- 2.2.6 Sales channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing emphasis on occupant safety compliance

- 3.2.1.2 Rising adoption of SUVs and crossovers

- 3.2.1.3 Technological advancements in adaptive airbag systems

- 3.2.1.4 Production expansion in emerging automotive hubs

- 3.2.1.5 Shift toward sustainable materials

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High system integration and component costs

- 3.2.2.2 Limited safety regulations in emerging markets

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in autonomous and semi-autonomous vehicles

- 3.2.3.2 Aftermarket replacement and recall-driven demand

- 3.2.3.3 Expansion into commercial vehicles and fleets

- 3.2.3.4 Sustainability-driven procurement shifts

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 United States- FMVSS 214 side impact protection

- 3.4.1.2 Canada- CMVSS 214 side impact protection

- 3.4.2 Europe

- 3.4.2.1 Germany-UN regulation 135 pole side impact protection

- 3.4.2.2 United Kingdom-UNECE regulation 95 lateral impact protection

- 3.4.2.3 France-EU general safety regulation 2019/2144

- 3.4.2.4 Italy-UN regulation 21 interior fittings safety

- 3.4.2.5 Spain-EU regulation 661/2009 general vehicle safety

- 3.4.3 Asia Pacific

- 3.4.3.1 China-GB 20071 side impact protection

- 3.4.3.2 India-AIS-099 side impact regulation

- 3.4.3.3 Japan-JNCAP side impact crashworthiness protocol

- 3.4.3.4 Australia-ADR 72 side impact protection

- 3.4.3.5 South Korea-KMVSS side impact crash protection

- 3.4.4 Latin America

- 3.4.4.1 Brazil-Contran resolution 518 side impact protection

- 3.4.4.2 Mexico-NOM-194-SCFI vehicle safety standard

- 3.4.4.3 Argentina-IRAM-AITA 1-20 side impact standard

- 3.4.5 Middle East & Africa

- 3.4.5.1 South Africa-SANS 20079 side impact protection

- 3.4.5.2 Saudi Arabia-SASO 2915 vehicle safety regulation

- 3.4.5.3 UAE-UAE.S 5010-5 vehicle crash protection

- 3.4.5.4 Turkey-UNECE regulation 95 side impact protection

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technology

- 3.7.2 Emerging technology

- 3.8 Price trends

- 3.8.1 By Product

- 3.8.2 By region

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Future market outlook & opportunities

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Type, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 Side curtain airbags

- 5.2.1 Nylon

- 5.2.2 Polyester

- 5.3 Front curtain airbags

- 5.3.1 Nylon

- 5.3.2 Polyester

- 5.4 Rear curtain airbags

- 5.4.1 Nylon

- 5.4.2 Polyester

Chapter 6 Market Estimates & Forecast, By Material, 2022 - 2035 ($Mn, Units)

- 6.1 Key trends

- 6.2 Nylon

- 6.3 Polyester

Chapter 7 Market Estimates & Forecast, By Sensor, 2022 - 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 MEMS Impact Sensors

- 7.3 Rollover Gyro Sensors

- 7.4 Unified Safety ECUs

Chapter 8 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 Passenger vehicles

- 8.2.1 Hatchback

- 8.2.2 Sedan

- 8.2.3 SUVs

- 8.3 Commercial vehicles

- 8.3.1 Light commercial vehicles (LCVs)

- 8.3.2 Medium commercial vehicles (MCVs)

- 8.3.3 Heavy commercial vehicles (HCVs)

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.3.8 Portugal

- 10.3.9 Croatia

- 10.3.10 Benelux

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Singapore

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Turkey

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Autoliv

- 11.1.2 ZF Friedrichshafen

- 11.1.3 Joyson Safety Systems

- 11.1.4 Continental

- 11.1.5 Hyundai

- 11.1.6 Toyoda Gosei

- 11.1.7 Daicel

- 11.1.8 Bosch Passive Safety Systems

- 11.1.9 Magna International

- 11.1.10 Denso

- 11.1.11 Valeo

- 11.1.12 Delphi Automotive / BorgWarner

- 11.2 Regional Players

- 11.2.1 Forvia Hella

- 11.2.2 Kolon Industries

- 11.2.3 Nihon Plast

- 11.2.4 Porcher Industries

- 11.2.5 Toray Industries

- 11.2.6 Sumitomo

- 11.2.7 SEIREN

- 11.2.8 Toyota Boshoku

- 11.2.9 Ashimori Industry

- 11.2.10 U-Shin

- 11.3 Emerging & Niche Players

- 11.3.1 Yanfeng Automotive Trim Systems

- 11.3.2 Wuhu Ruili Automobile Airbag

- 11.3.3 ARC Automotive

- 11.3.4 Tata AutoComp Systems

- 11.3.5 Ningbo Joyson Electronic

- 11.3.6 Changzhou Changrui

安全氣囊市場:按車輛類型、驅動方式、技術、銷售管道和最終用戶分類-2026-2032年全球預測軟袋光檢機市場:按技術、額定功率、應用和分銷管道分類,全球預測(2026-2032年)

安全氣囊市場:按車輛類型、驅動方式、技術、銷售管道和最終用戶分類-2026-2032年全球預測軟袋光檢機市場:按技術、額定功率、應用和分銷管道分類,全球預測(2026-2032年) 安全氣囊控制單元感測器市場分析及預測(至2035年):按類型、產品類型、技術、組件、應用、材質、安裝方法、最終用戶、功能和安裝類型分類

安全氣囊控制單元感測器市場分析及預測(至2035年):按類型、產品類型、技術、組件、應用、材質、安裝方法、最終用戶、功能和安裝類型分類 全球安全氣囊電子市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球安全氣囊電子市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 商用車汽車安全氣囊市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、銷售管道、地區和競爭格局分類,2021-2031年)安全氣囊感知器市場 - 全球產業規模、佔有率、趨勢、機會及預測(按車輛類型、地點、動力類型、地區和競爭格局分類,2021-2031年)汽車側簾式氣囊市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、車輛類型、需求類別、地區和競爭格局分類,2021-2031年

商用車汽車安全氣囊市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、銷售管道、地區和競爭格局分類,2021-2031年)安全氣囊感知器市場 - 全球產業規模、佔有率、趨勢、機會及預測(按車輛類型、地點、動力類型、地區和競爭格局分類,2021-2031年)汽車側簾式氣囊市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、車輛類型、需求類別、地區和競爭格局分類,2021-2031年 汽車安全氣囊市場機會、成長要素、產業趨勢分析及2026年至2035年預測輕型汽車安全氣囊市場 - 全球產業規模、佔有率、趨勢、機會及預測(按車輛類型、安全氣囊類型、需求類別、紗線類型、地區和競爭格局分類,2021-2031年)主動式安全氣囊套件市場按類型、驅動方式、安裝階段、車輛類型和分銷管道分類,全球預測(2026-2032年)

汽車安全氣囊市場機會、成長要素、產業趨勢分析及2026年至2035年預測輕型汽車安全氣囊市場 - 全球產業規模、佔有率、趨勢、機會及預測(按車輛類型、安全氣囊類型、需求類別、紗線類型、地區和競爭格局分類,2021-2031年)主動式安全氣囊套件市場按類型、驅動方式、安裝階段、車輛類型和分銷管道分類,全球預測(2026-2032年)