|

市場調查報告書

商品編碼

1892830

商業海藻市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)Commercial Seaweed Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

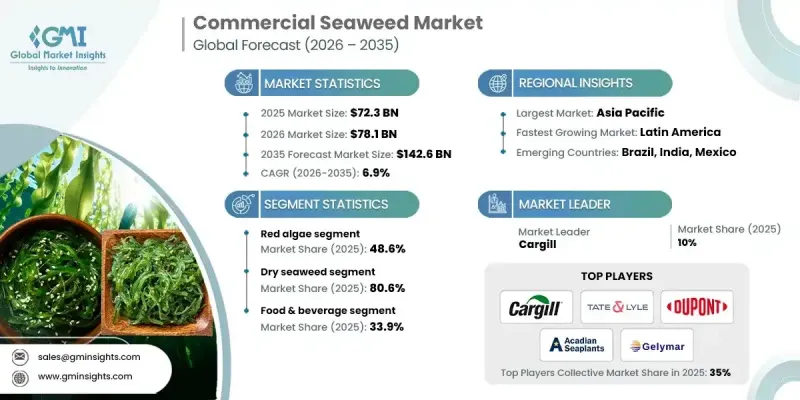

2025 年全球商業海藻市場價值為 723 億美元,預計到 2035 年將以 6.9% 的複合年成長率成長至 1,426 億美元。

隨著海藻功能多樣且永續性強,其在多條價值鏈中的應用日益廣泛,市場持續成長。需求成長與海藻衍生水膠體的應用日益普及密切相關,這些水膠體在食品、化妝品和工業配方中發揮重要的黏合、穩定和增稠作用。這些應用合計佔全球商業海藻收入的40%以上。同時,向環境友善農業實踐的轉型正在加速海藻基投入品的應用,使海藻成為與再生和低影響農業模式相契合的天然解決方案。全球政策與永續農業的協調一致進一步增強了需求。此外,海藻生物技術的創新正在拓展市場價值潛力,生產商投資於先進加工技術,以提取用於營養、健康和特殊應用的高價值化合物。這些發展正在重塑商業海藻產業,使其從以產量為主導的產業轉變為技術驅動、高價值的生態系統,擁有多元化的終端用途和強勁的長期成長前景。

| 市場範圍 | |

|---|---|

| 起始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 723億美元 |

| 預測值 | 1426億美元 |

| 複合年成長率 | 6.9% |

2025年,紅藻市佔率達到48.6%,預計到2035年將以6.8%的複合年成長率成長。其主導地位得益於其在水膠體生產中的廣泛應用,而水膠體仍然是食品、製藥和個人護理用品製造的基礎原料,從而鞏固了全球的穩定需求。

2025年,食品飲料應用領域佔33.9%的市場佔有率,預計2026年至2035年將以6.8%的複合年成長率成長。海藻作為一種天然功能性成分,繼續被廣泛應用,有助於提高包裝食品和加工食品的配方穩定性、增強營養價值,並實現清潔標籤定位。

北美商業海藻市場預計到2025年將佔據11%的市場佔有率,並呈現快速成長態勢。該地區受益於對永續水產養殖、氣候友善材料和替代飼料解決方案的投資不斷增加,從而推動了更廣泛的商業應用和下游創新。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 產業陷阱與挑戰

- 市場機遇

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 按類型

- 未來市場趨勢

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 專利格局

- 貿易統計(HS編碼)(註:僅提供重點國家的貿易統計資料)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依類型分類,2022-2035年

- 紅藻

- 褐藻

- 綠藻

第6章:市場估算與預測:依產品類型分類,2022-2035年

- 乾海藻

- 濕/新鮮海藻

第7章:市場估算與預測:依最終用途分類,2022-2035年

- 餐飲

- 乳製品

- 烘焙食品和糖果

- 加工肉類和海鮮

- 純素/植物性食品

- 功能飲料

- 可食用海藻零食

- 醬汁、湯料和調味料

- 動物飼料

- 牲畜飼料添加劑

- 家禽飼料

- 水產飼料

- 寵物食品補充劑

- 反芻動物的減甲烷飼料

- 醫藥及個人護理

- 傷口癒合軟膏

- 藥物輸送系統

- 護膚乳液和乳霜

- 洗髮精和護髮素

- 抗衰老和抗發炎產品

- 口腔護理產品

- 生物燃料

- 生物乙醇生產

- 沼氣發電

- 藻類生質能預處理投入

- 混合再生能源

- 其他

- 農業生物促效劑

- 土壤改良劑

- 水處理劑

- 紡織工業應用

- 生物塑膠和包裝材料

第8章:市場估算與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第9章:公司簡介

- Acadian Seaplants

- Algaia

- Cargill

- DuPont

- FMC Corporation

- Gelymar

- Indo Alginate

- Irish Seaweeds

- KIMICA Corporation

- Mara Seaweed

- MCPI (Marine Chemicals & Polymers Industries)

- Ocean Harvest Technology

- Qingdao Gather Great Ocean Algae Industry Group

- Qingdao Seawin Biotech Group

- Seasol

- Seaweed Energy Solutions

- Shaanxi Hongda Phytochemistry Co., Ltd.

- Tate & Lyle

- TBK Manufacturing Corporation (Philippines)

- W Hydrocolloids, Inc.

- Others

The Global Commercial Seaweed Market was valued at USD 72.3 billion in 2025 and is estimated to grow at a CAGR of 6.9% to reach USD 142.6 billion by 2035.

The market continues to gain momentum as seaweed becomes increasingly integrated into multiple value chains, supported by its functional versatility and sustainability profile. Demand growth is strongly linked to the rising use of seaweed-derived hydrocolloids that perform essential binding, stabilizing, and thickening functions across food, cosmetics, and industrial formulations. These applications collectively account for more than 40% of global commercial seaweed revenue. At the same time, the transition toward environmentally responsible agricultural practices is accelerating the adoption of seaweed-based inputs, positioning seaweed as a natural solution aligned with regenerative and low-impact farming models. Global policy alignment with sustainable agriculture has further strengthened demand. In parallel, innovation across seaweed biotechnology is expanding the market's value potential, as producers invest in advanced processing to extract high-value compounds for nutrition, health, and specialty applications. These developments are reshaping the commercial seaweed industry from a volume-driven sector into a technology-enabled, high-value ecosystem with diversified end uses and strong long-term growth visibility.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $72.3 Billion |

| Forecast Value | $142.6 Billion |

| CAGR | 6.9% |

The red algae segment held a 48.6% share in 2025 and is expected to grow at a CAGR of 6.8% through 2035. This dominance is supported by its widespread use in hydrocolloid production, which remains a foundational input across food, pharmaceutical, and personal care manufacturing, reinforcing steady global demand.

The food & beverage applications segment held 33.9% share in 2025 and is forecast to grow at a CAGR of 6.8% from 2026 to 2035. Seaweed continues to be widely incorporated as a natural functional ingredient, supporting formulation stability, nutritional enhancement, and clean-label positioning across packaged and processed food categories.

North America Commercial Seaweed Market accounted for 11% share in 2025 and is showing rapid growth. The region benefits from increasing investment in sustainable aquaculture, climate-aligned materials, and alternative feed solutions, driving broader commercial adoption and downstream innovation.

Key companies operating in the Global Commercial Seaweed Market include Cargill, Tate & Lyle, DuPont, FMC Corporation, Algaia, Gelymar, Acadian Seaplants, Irish Seaweeds, KIMICA Corporation, Qingdao Seawin Biotech Group, Ocean Harvest Technology, Seasol, Seaweed Energy Solutions, Indo Alginate, TBK Manufacturing Corporation, W Hydrocolloids, Inc., MCPI, Mara Seaweed, Qingdao Gather Great Ocean Algae Industry Group, and Shaanxi Hongda Phytochemistry. Companies in the Global Commercial Seaweed Market are strengthening their market position by expanding vertically across cultivation, processing, and formulation to secure supply consistency and improve margins. Significant investment is directed toward research and development to unlock high-value extracts and improve processing efficiency. Strategic partnerships with food, agriculture, and wellness manufacturers are helping accelerate commercialization and application development. Firms are also scaling production capacity in high-growth regions to reduce logistics costs and meet rising demand.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Form

- 2.2.4 End use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code)(Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Red algae

- 5.3 Brown algae

- 5.4 Green algae

Chapter 6 Market Estimates and Forecast, By Form, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Dry seaweed

- 6.3 Wet/Fresh seaweed

Chapter 7 Market Estimates and Forecast, By End use, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Food & beverage

- 7.2.1 Dairy products

- 7.2.2 Bakery & confectionery

- 7.2.3 Processed meats & seafood

- 7.2.4 Vegan/plant-based foods

- 7.2.5 Functional beverages

- 7.2.6 Edible seaweed snacks

- 7.2.7 Sauces, soups & seasonings

- 7.3 Animal feed

- 7.3.1 Livestock feed additives

- 7.3.2 Poultry feed

- 7.3.3 Aquaculture feed

- 7.3.4 Pet food supplements

- 7.3.5 Methane-reducing feed for ruminants

- 7.4 Pharmaceutical & personal care

- 7.4.1 Wound healing ointments

- 7.4.2 Drug delivery systems

- 7.4.3 Skin care lotions & creams

- 7.4.4 Shampoos & conditioners

- 7.4.5 Anti-aging & anti-inflammatory products

- 7.4.6 Oral care products

- 7.5 Biofuels

- 7.5.1 Bioethanol production

- 7.5.2 Biogas generation

- 7.5.3 Algal biomass pre-treatment inputs

- 7.5.4 Hybrid renewable energy blends

- 7.6 Others

- 7.6.1 Agricultural biostimulants

- 7.6.2 Soil conditioners

- 7.6.3 Water treatment agents

- 7.6.4 Textile industry applications

- 7.6.5 Bioplastics & packaging materials

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Acadian Seaplants

- 9.2 Algaia

- 9.3 Cargill

- 9.4 DuPont

- 9.5 FMC Corporation

- 9.6 Gelymar

- 9.7 Indo Alginate

- 9.8 Irish Seaweeds

- 9.9 KIMICA Corporation

- 9.10 Mara Seaweed

- 9.11 MCPI (Marine Chemicals & Polymers Industries)

- 9.12 Ocean Harvest Technology

- 9.13 Qingdao Gather Great Ocean Algae Industry Group

- 9.14 Qingdao Seawin Biotech Group

- 9.15 Seasol

- 9.16 Seaweed Energy Solutions

- 9.17 Shaanxi Hongda Phytochemistry Co., Ltd.

- 9.18 Tate & Lyle

- 9.19 TBK Manufacturing Corporation (Philippines)

- 9.20 W Hydrocolloids, Inc.

- 9.21 Others