|

市場調查報告書

商品編碼

1892648

智慧物流平台市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Smart Logistics Platforms Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

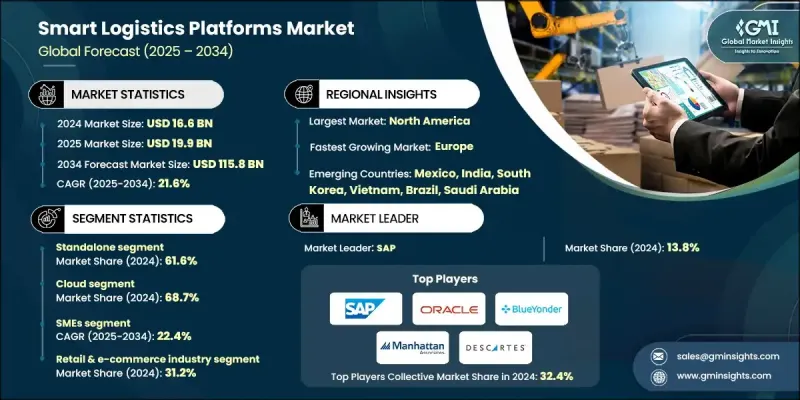

2024 年全球智慧物流平台市場價值為 166 億美元,預計到 2034 年將以 21.6% 的複合年成長率成長至 1,158 億美元。

全球貿易的擴張推動了對先進物流解決方案的需求,包括車隊管理、即時追蹤、路線最佳化、庫存控制和倉庫管理。企業正擴大採用這些平台來簡化營運、提高效率並增強複雜供應鏈的透明度。企業可以選擇整合解決方案(在單一平台上提供多種功能)或獨立解決方案(專注於根據營運需求量身定做的特定任務)。人工智慧和機器學習透過最佳化路線、改善預測分析、加強安全性和防範網路威脅,進一步加速了市場成長。由於對全球出口的大量投資,北美和歐洲預計將繼續保持領先地位,而亞太地區在出口導向經濟體擴張的推動下,正崛起為成長最快的市場。中國、美國和德國在全球貿易中佔據主導地位,因此對能夠有效管理國際供應鏈的創新物流解決方案有著強勁的需求。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 166億美元 |

| 預測值 | 1158億美元 |

| 複合年成長率 | 21.6% |

2024年,獨立式物流解決方案佔了61.6%的市佔率。其受歡迎的原因在於部署速度更快、初始成本更低,並且無需完全系統整合即可處理特定的物流功能,例如路線最佳化、車隊監控和倉庫視覺化。這些解決方案可客製化、易於實施,是需要快速獲得明確結果的企業的理想選擇。

到2024年,雲端部署領域將佔據68.7%的市場。雲端平台因其即時追蹤、可擴展營運和人工智慧驅動的分析功能而廣受歡迎。它們能夠實現合作夥伴之間的無縫協作,增強供應鏈的透明度,並使物流供應商能夠在無需龐大本地基礎設施的情況下有效應對需求波動。

2024年,美國智慧物流平台市場規模達69億美元。高昂的物流成本佔國民生產總值的8-10%以上,推動了人工智慧平台的普及,這些平台可以最佳化路線、減少資源浪費並提高營運效率。

目錄

第1章:方法論

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率

- 成本結構

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 電子商務成長與全通路履約需求

- 供應鏈可視性和韌性的必要性

- 勞動力短缺與自動化應用

- 雲端採用和數位轉型勢在必行

- 產業陷阱與挑戰

- 高昂的初始實施成本和總體擁有成本 (TCO) 問題

- 資料安全和隱私合規負擔

- 市場機遇

- 自主物流與人機混合網路

- 用於營運輔助的生成式人工智慧

- 最後一公里配送創新

- 內陸及最低度開發國家(LDC)物流數位化

- 成長促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 技術路線圖與演進

- 技術採納生命週期分析

- 價格趨勢

- 按地區

- 依產品

- 專利分析

- 網路安全與資料治理格局

- 客戶痛點及工作流程最佳化分析

- 可視性差距和即時追蹤挑戰

- 人工流程和資料輸入效率低下

- 承運能力限制和貨運採購

- 最後一公里配送成本與顧客體驗

- 庫存準確性和倉庫勞動生產力

- 個案研究和實施成功指標

- 最佳情況

- 數位轉型經濟學與總擁有成本分析

- 雲端遷移成本效益分析

- SaaS 與永久授權總體擁有成本比較

- 實施成本和專業服務

- 變革管理與培訓投資

- 網路安全架構與資料隱私框架

- 雲端安全和多租戶隔離

- 資料加密

- 身分與存取管理 (IAM)

- GDPR、CCPA 和跨境資料法規

- 供應鍊網路威脅及攻擊途徑

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃和資金

- 供應商選擇標準

- 供應鏈及合作夥伴生態系分析

第5章:市場估算與預測:依解法分類,2021-2034年

- 獨立版

- 融合的

第6章:市場估算與預測:依部署模式分類,2021-2034年

- 現場

- 雲

- 私有雲端

- 公共雲端

- 混合雲端

- 混合

第7章:市場估算與預測:依企業規模分類,2021-2034年

- 中小企業

- 大型企業

第8章:市場估算與預測:依最終用途分類,2021-2034年

- 零售與電子商務

- 製造業

- 第三方物流

- 食品和飲料

- 製藥

- 其他

第9章:市場估計與預測:依地區分類,2021-2034年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐

- 比荷盧經濟聯盟

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳新銀行

- 新加坡

- 馬來西亞

- 印尼

- 越南

- 泰國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥倫比亞

- MEA

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- 全球公司

- Manhattan Associates

- SAP

- Oracle

- Blue Yonder

- Uber Freight

- Kinaxis

- E2 open

- Infor

- Descartes Systems

- HighJump

- Magaya Supply Chain

- LogiNext Mile

- Alpega

- Honeywell

- 區域公司

- Project44

- FourKites

- CH Robinson Worldwide

- XPO Logistics

- JB Hunt Transport Services

- Transporeon

- Trimble Transportation

- Samsara

- 新興公司

- Flexport

- Convoy

- Waymo Via

- Starship Technologies

- Waabi

- Nuro

- Loadsmart

The Global Smart Logistics Platforms Market was valued at USD 16.6 billion in 2024 and is estimated to grow at a CAGR of 21.6% to reach USD 115.8 billion by 2034.

The expansion of global trade is fueling the need for advanced logistics solutions, including fleet management, live tracking, route optimization, inventory control, and warehouse management. Companies are increasingly adopting these platforms to streamline operations, enhance efficiency, and improve visibility across complex supply chains. Businesses can choose between integrated solutions, which offer multiple functionalities within a single platform, and standalone solutions, which focus on specific tasks tailored to operational requirements. Artificial intelligence and machine learning are further accelerating market growth by optimizing routes, improving predictive analytics, strengthening security, and preventing cyber threats. North America and Europe are expected to remain leaders due to substantial investments in global exports, while the Asia-Pacific region is emerging as the fastest-growing market, driven by the expansion of export-oriented economies. China, followed by the U.S. and Germany, dominates global trade, creating strong demand for innovative logistics solutions to manage international supply chains effectively.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $16.6 Billion |

| Forecast Value | $115.8 Billion |

| CAGR | 21.6% |

The standalone segment held a 61.6% share in 2024. Its popularity is attributed to faster deployment, lower initial costs, and the ability to handle specific logistics functions such as route optimization, fleet monitoring, and warehouse visibility without full system integration. These solutions are customizable, easy to implement, and ideal for businesses requiring quick, focused results.

The cloud deployment segment held a 68.7% share in 2024. Cloud platforms are widely preferred for their real-time tracking, scalable operations, and AI-driven analytics. They enable seamless collaboration among partners, enhance supply chain visibility, and allow logistics providers to respond effectively to fluctuating demand without heavy on-premises infrastructure.

U.S. Smart Logistics Platforms Market reached USD 6.9 billion in 2024. High logistics costs, which account for more than 8-10% of the national GDP, have driven the adoption of AI-powered platforms that optimize routes, reduce resource waste, and improve operational efficiency.

Key players in the Smart Logistics Platforms Market include Blue Yonder, SAP, Oracle, Manhattan Associates, Descartes Systems, LogiNext Mile, Honeywell, Magaya Supply Chain, Alpega, and Infor. Companies in the Global Smart Logistics Platforms Market are focusing on AI and ML integration to enhance predictive analytics, optimize fleet management, and strengthen cybersecurity. Cloud-based platform development is prioritized to improve scalability, real-time collaboration, and global supply chain visibility. Strategic partnerships with logistics providers, manufacturers, and technology firms help expand market reach and foster innovation. Firms are investing in R&D to introduce customizable and modular solutions that meet diverse client needs. Market players are also emphasizing digital transformation, offering IoT-enabled platforms to track shipments, monitor inventory, and reduce operational inefficiencies.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Solution

- 2.2.3 Deployment model

- 2.2.4 Enterprise size

- 2.2.5 End use

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 E-Commerce growth & omnichannel Fulfilment demands

- 3.2.1.2 Supply chain visibility & resilience imperatives

- 3.2.1.3 Labor shortages & automation adoption

- 3.2.1.4 Cloud adoption & digital transformation mandates

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial implementation costs & TCO concerns

- 3.2.2.2 Data security & privacy compliance burden

- 3.2.3 Market opportunities

- 3.2.3.1 Autonomous logistics & hybrid human-robot networks

- 3.2.3.2 Generative AI for operational assistance

- 3.2.3.3 Last-mile delivery innovation

- 3.2.3.4 Landlocked & least developed country (LDC) logistics digitization

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.7.3 Technology roadmaps & evolution

- 3.7.4 Technology adoption lifecycle analysis

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Patent analysis

- 3.10 Cybersecurity & data governance landscape

- 3.11 Customer pain points & workflow optimization analysis

- 3.11.1 Visibility gap & real-time tracking challenges

- 3.11.2 Manual processes & data entry inefficiencies

- 3.11.3 Carrier capacity constraints & freight procurement

- 3.11.4 Last-Mile delivery cost & customer experience

- 3.11.5 Inventory accuracy & warehouse labor productivity

- 3.12 Case studies & implementation success metrics

- 3.13 Best case scenarios

- 3.14 Digital transformation economics & TCO analysis

- 3.14.1 Cloud migration cost-benefit analysis

- 3.14.2 SaaS vs perpetual license TCO comparison

- 3.14.3 Implementation costs & professional services

- 3.14.4 Change management & training investments

- 3.15 Cybersecurity architecture & data privacy framework

- 3.15.1 Cloud security & multi-tenant isolation

- 3.15.2 Data Encryption

- 3.15.3 Identity & access management (IAM)

- 3.15.4 GDPR, CCPA & cross-border data regulations

- 3.15.5 Supply chain cyber threats & attack vectors

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

- 4.7 Vendor selection criteria

- 4.8 Supply chain & partner ecosystem analysis

Chapter 5 Market Estimates & Forecast, By Solution, 2021 - 2034 ($Mn)

- 5.1 Key trends

- 5.2 Standalone

- 5.3 Integrated

Chapter 6 Market Estimates & Forecast, By Deployment Model, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 On-premises

- 6.3 Cloud

- 6.3.1 Private Cloud

- 6.3.2 Public Cloud

- 6.3.3 Hybrid Cloud

- 6.4 Hybrid

Chapter 7 Market Estimates & Forecast, By Enterprise Size, 2021 - 2034 ($Mn)

- 7.1 Key trends

- 7.2 SME

- 7.3 Large Enterprises

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn)

- 8.1 Key trends

- 8.2 Retail & E-commerce

- 8.3 Manufacturing

- 8.4 Third party logistics

- 8.5 Food & Beverage

- 8.6 Pharmaceuticals

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.3.8 Benelux

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Singapore

- 9.4.7 Malaysia

- 9.4.8 Indonesia

- 9.4.9 Vietnam

- 9.4.10 Thailand

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Colombia

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global companies

- 10.1.1 Manhattan Associates

- 10.1.2 SAP

- 10.1.3 Oracle

- 10.1.4 Blue Yonder

- 10.1.5 Uber Freight

- 10.1.6 Kinaxis

- 10.1.7. E2 open

- 10.1.8 Infor

- 10.1.9 Descartes Systems

- 10.1.10 HighJump

- 10.1.11 Magaya Supply Chain

- 10.1.12 LogiNext Mile

- 10.1.13 Alpega

- 10.1.14 Honeywell

- 10.2 Regional companies

- 10.2.1 Project44

- 10.2.2 FourKites

- 10.2.3 C.H. Robinson Worldwide

- 10.2.4 XPO Logistics

- 10.2.5 J.B. Hunt Transport Services

- 10.2.6 Transporeon

- 10.2.7 Trimble Transportation

- 10.2.8 Samsara

- 10.3 Emerging companies

- 10.3.1 Flexport

- 10.3.2 Convoy

- 10.3.3 Waymo Via

- 10.3.4 Starship Technologies

- 10.3.5 Waabi

- 10.3.6 Nuro

- 10.3.7 Loadsmart

全球物流和運輸市場按收入、貨運方式、地區、業務場景和應用案例分類-預測至2035年

全球物流和運輸市場按收入、貨運方式、地區、業務場景和應用案例分類-預測至2035年 2025年全球風力發電機運輸物流市場報告

2025年全球風力發電機運輸物流市場報告 全球智慧城市物流市場:未來預測(至2032年)-按交付類型、運輸方式、物流模式、技術、最終用戶和區域進行分析電動車物流市場預測至2032年:按車輛類型、電池類型、充電基礎設施、動力傳動系統配置、應用、最終用戶和地區分類的全球分析

全球智慧城市物流市場:未來預測(至2032年)-按交付類型、運輸方式、物流模式、技術、最終用戶和區域進行分析電動車物流市場預測至2032年:按車輛類型、電池類型、充電基礎設施、動力傳動系統配置、應用、最終用戶和地區分類的全球分析 全球裝卸整平機市場(依產品類型、終端用戶產業、操作模式、安裝方式及容量分類)-2025-2032年預測按貨物類型、貨櫃類型、服務類型、港口類型、船隊所有權類型和客戶類型分類的短途運輸服務市場 - 2025-2032 年全球預測中哩物流市場(按服務、運輸方式、距離段、貨物類型和最終用戶分類)-2025-2030 年全球預測按類型、服務類型、車隊規模、最終用戶類型和垂直行業分類的零擔物流市場 - 2025-2030 年全球預測物流市場:按類型、功能、運輸類型、運輸方式和行業 - 2025-2030 年全球預測

全球裝卸整平機市場(依產品類型、終端用戶產業、操作模式、安裝方式及容量分類)-2025-2032年預測按貨物類型、貨櫃類型、服務類型、港口類型、船隊所有權類型和客戶類型分類的短途運輸服務市場 - 2025-2032 年全球預測中哩物流市場(按服務、運輸方式、距離段、貨物類型和最終用戶分類)-2025-2030 年全球預測按類型、服務類型、車隊規模、最終用戶類型和垂直行業分類的零擔物流市場 - 2025-2030 年全球預測物流市場:按類型、功能、運輸類型、運輸方式和行業 - 2025-2030 年全球預測 全球製造業物流市場

全球製造業物流市場