|

市場調查報告書

商品編碼

1885848

石油化學產品回收市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Petrochemical Recycling Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

2024 年全球石化回收市場價值為 185 億美元,預計到 2034 年將以 10.8% 的複合年成長率成長至 523 億美元。

市場的快速成長反映了對永續塑膠廢棄物管理解決方案日益成長的需求,以及先進化學回收技術的不斷改進。日益嚴峻的環境壓力和更嚴格的全球廢棄物法規正促使各行業和政府加快創新步伐,擴大回收能力。化學回收因其能夠將混合和受污染的塑膠廢棄物轉化為傳統機械系統無法有效處理的可用產品,而日益受到重視。隨著全球塑膠消費量的持續攀升,廢棄物產生量與回收能力之間的差距凸顯了對可擴展化學回收替代方案的迫切需求。主要地區的進展,加上強力的政策支持和大量的產業投資,正在重塑全球格局,並將石化回收定位為循環經濟的關鍵組成部分。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 185億美元 |

| 預測值 | 523億美元 |

| 複合年成長率 | 10.8% |

2024年,熱解技術市佔率達到43.5%,預計2034年將以10.4%的複合年成長率成長。其主導地位源自於其高度的商業化成熟度以及在無氧條件下分解複雜聚合物結構的能力,從而產生可精煉的碳氫化合物產品。該技術對混合和受污染塑膠的靈活性使其成為處理機械回收無法處理的廢棄物流的關鍵手段。其不斷擴展的設施網路和持續的投資支持也印證了其在業界的廣泛認可。

2024年,聚烯烴回收領域佔59.5%的市場佔有率,預計2025年至2034年將以10.5%的複合年成長率成長。聚乙烯和聚丙烯等材料因其在全球包裝生產中的廣泛應用而保持領先地位。它們的熱塑性使其與熱解和氣化等轉化技術高度相容,從而能夠高效地轉化為有價值的烴類衍生物。

2024年,北美石化回收市場佔24.8%的佔有率。該地區受益於可靠的廢棄物收集系統、產業投資以及鼓勵採用再生材料的扶持性監管措施。旨在加強生產者責任和減少垃圾掩埋的政策鞏固了市場成長,並刺激了對化學再生材料的長期需求。

石油化工回收市場的主要企業包括馬來西亞國家石油公司(PETRONAS Chemicals Group)、Quantafuel ASA、埃克森美孚公司(ExxonMobil Corporation)、Plastic Energy、利安德巴塞爾工業公司(LyondellBasell Industries)、Recycling Technologies Ltd.、巴斯夫公司(BASF SE)、伊士曼斯化學公司(Eastman Chem) Inc.、陶氏公司(Dow Inc.)、Carbios SA 和沙烏地基礎工業公司(SABIC)。這些企業透過投資先進的解聚技術、擴大工廠產能以及簽訂長期原料供應協議來確保穩定的原料供應,從而提升自身的競爭力。許多公司積極與包裝生產商和石油化學製造商合作,將回收產品直接整合到產品價值鏈中。策略合作夥伴關係能夠加速技術開發並支援大規模商業化。此外,各企業也加大研發投入,以提高製程效率、降低能耗並提升回收烴的純度。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 生產者延伸責任制(EPR)

- 再生材料含量要求及法規

- 塑膠垃圾危機與環境問題

- 產業陷阱與挑戰

- 高資本投資需求

- 技術挑戰與品質限制

- 市場機遇

- 政府資助和投資計劃

- 亞太地區新興市場擴張

- 成長促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 依技術類型

- 未來市場趨勢

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 專利格局

- 貿易統計(HS編碼)(註:僅提供重點國家的貿易統計資料)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依技術類型分類,2021-2034年

- 主要趨勢

- 熱解技術

- 傳統熱解系統

- 催化劑輔助的高級熱解

- 微波輔助熱解

- 解聚(化學分解)

- 溶劑分解過程

- PET回收的糖解作用

- 酵素解聚

- 催化解聚

- 氣化技術

- 空氣吹氣氣化系統

- 氧氣吹掃氣化

- 蒸氣氣化過程

- 電漿氣化技術

- 溶解和溶劑型回收

- 選擇性溶解技術

- 溶劑回收與純化

第6章:市場估算與預測:依原料類型分類,2021-2034年

- 主要趨勢

- 聚烯烴回收(PE/PP)

- 高密度聚乙烯(HDPE)回收

- 低密度聚乙烯(LDPE)回收

- 聚丙烯(PP)回收

- 混合聚烯烴流

- PET回收

- 瓶對瓶回收

- 光纖到光纖應用

- 食品級PET回收

- 彩色PET加工

- 混合塑膠垃圾回收

- 多層包裝材料

- 受污染的塑膠流

- 電子垃圾塑膠

- 汽車塑膠部件

- 特種聚合物回收

- 工程塑膠回收

- 熱固性塑膠加工

- 複合材料回收

- 生物基聚合物回收

第7章:市場估計與預測:依應用領域分類,2021-2034年

- 主要趨勢

- 化工原料生產

- 燃料生產應用

- 新型聚合物的生產

- 特種產品製造

第8章:市場估算與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第9章:公司簡介

- ExxonMobil Corporation

- Eastman Chemical Company

- Dow Inc.

- SABIC (Saudi Basic Industries Corporation)

- BASF SE

- LyondellBasell Industries

- PETRONAS Chemicals Group

- Plastic Energy

- Agilyx Corporation

- Pyrowave Inc.

- Recycling Technologies Ltd

- Brightmark LLC

- Quantafuel ASA

- Carbios SA

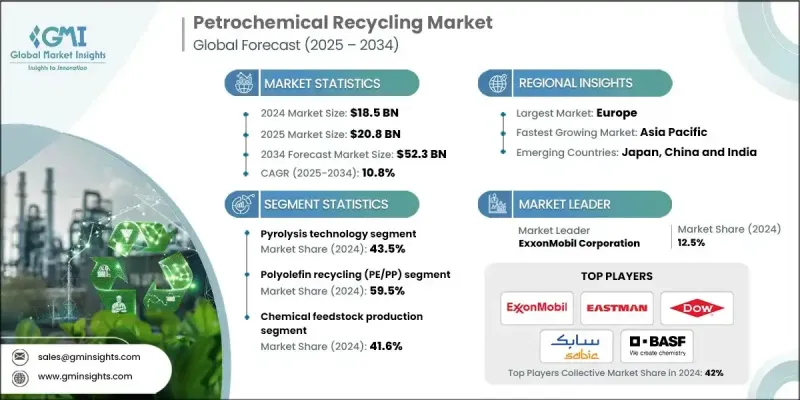

The Global Petrochemical Recycling Market was valued at USD 18.5 billion in 2024 and is estimated to grow at a CAGR of 10.8% to reach USD 52.3 billion by 2034.

The market's rapid rise reflects the growing need for sustainable solutions to manage plastic waste and the increasing refinement of advanced chemical recycling technologies. Rising environmental pressures and stricter global waste regulations are pushing industries and governments to accelerate innovation and expand recycling capacity. Chemical recycling is gaining traction as it provides a viable pathway for converting mixed and contaminated plastic waste into usable outputs that traditional mechanical systems cannot process effectively. As plastic consumption continues to climb worldwide, the gap between waste generation and recycling capacity highlights the urgent demand for scalable chemical recycling alternatives. Progress across major regions, combined with strong policy backing and substantial industrial investments, is reshaping the global landscape and positioning petrochemical recycling as a critical component of the circular economy.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $18.5 Billion |

| Forecast Value | $52.3 Billion |

| CAGR | 10.8% |

The pyrolysis technology segment held 43.5% share in 2024 and is anticipated to grow at a CAGR of 10.4% through 2034. Its dominance stems from its high commercial readiness and ability to break down complex polymer structures under oxygen-free conditions, yielding hydrocarbon products that can be refined. Its flexibility with mixed and contaminated plastics makes it essential for processing waste streams that mechanical recycling cannot accommodate. Its growing network of facilities and consistent investment support confirm its strong industry acceptance.

The polyolefin recycling segment accounted for a 59.5% share in 2024 and is expected to grow at a CAGR of 10.5% from 2025 to 2034. Materials such as polyethylene and polypropylene maintain a leading position due to their heavy use in global packaging production. Their thermoplastic properties make them highly compatible with conversion technologies such as pyrolysis and gasification, facilitating efficient transformation into valuable hydrocarbon derivatives.

North America Petrochemical Recycling Market held a 24.8% share in 2024. This region benefits from reliable waste collection systems, industry investments, and supportive regulatory measures that encourage recycled content adoption. Policies aimed at strengthening producer responsibility and reducing landfill waste reinforce market growth and stimulate long-term demand for chemically recycled materials.

Key companies in the Petrochemical Recycling Market include PETRONAS Chemicals Group, Quantafuel ASA, ExxonMobil Corporation, Plastic Energy, LyondellBasell Industries, Recycling Technologies Ltd., BASF SE, Eastman Chemical Company, Agilyx Corporation, Brightmark LLC, Pyrowave Inc., Dow Inc., Carbios SA, and SABIC (Saudi Basic Industries Corporation). Companies in the Petrochemical Recycling Market enhance their competitive standing by investing in advanced depolymerization technologies, expanding plant capacity, and forming long-term feedstock agreements to ensure stable input supply. Many firms pursue collaborations with packaging producers and petrochemical manufacturers to integrate recycled outputs directly into product value chains. Strategic partnerships accelerate technology development and support commercialization at scale. Organizations also increase R&D spending to improve process efficiency, reduce energy consumption, and enhance the purity of recycled hydrocarbons.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Technology type

- 2.2.3 Feedstock type

- 2.2.4 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Extended producer responsibility (EPR) mandates

- 3.2.1.2 Recycled content requirements & regulations

- 3.2.1.3 Plastic waste crisis & environmental concerns

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High capital investment requirements

- 3.2.2.2 Technical challenges & quality constraints

- 3.2.3 Market opportunities

- 3.2.3.1 Government funding & investment programs

- 3.2.3.2 Emerging market expansion in Asia-Pacific

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By technology type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Technology Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Pyrolysis technology

- 5.2.1 Conventional pyrolysis systems

- 5.2.2 Advanced pyrolysis with catalysts

- 5.2.3 Microwave-assisted pyrolysis

- 5.3 Depolymerization (chemolysis)

- 5.3.1 Solvolysis processes

- 5.3.2 Glycolysis for PET recycling

- 5.3.3 Enzymatic depolymerization

- 5.3.4 Catalytic depolymerization

- 5.4 Gasification technology

- 5.4.1 Air-blown gasification systems

- 5.4.2 Oxygen-blown gasification

- 5.4.3 Steam gasification processes

- 5.4.4 Plasma gasification technology

- 5.5 Dissolution & solvent-based recycling

- 5.5.1 Selective dissolution technologies

- 5.5.2 Solvent recovery & purification

Chapter 6 Market Estimates and Forecast, By Feedstock Type, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Polyolefin recycling (PE/PP)

- 6.2.1 High-density polyethylene (HDPE) recycling

- 6.2.2 Low-density polyethylene (LDPE) recycling

- 6.2.3 Polypropylene (pp) recycling

- 6.2.4 Mixed polyolefin streams

- 6.3 PET recycling

- 6.3.1 Bottle-to-bottle recycling

- 6.3.2 Fiber-to-fiber applications

- 6.3.3 Food-grade PET recycling

- 6.3.4 Colored PET processing

- 6.4 Mixed plastic waste recycling

- 6.4.1 Multi-layer packaging materials

- 6.4.2 Contaminated plastic streams

- 6.4.3 Electronic waste plastics

- 6.4.4 Automotive plastic components

- 6.5 Specialty polymer recycling

- 6.5.1 Engineering plastics recycling

- 6.5.2 Thermoset plastic processing

- 6.5.3 Composite material recycling

- 6.5.4 Bio-based polymer recycling

Chapter 7 Market Estimates and Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Chemical feedstock production

- 7.3 Fuel production applications

- 7.4 New polymer production

- 7.5 Specialty product manufacturing

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 ExxonMobil Corporation

- 9.2 Eastman Chemical Company

- 9.3 Dow Inc.

- 9.4 SABIC (Saudi Basic Industries Corporation)

- 9.5 BASF SE

- 9.6 LyondellBasell Industries

- 9.7 PETRONAS Chemicals Group

- 9.8 Plastic Energy

- 9.9 Agilyx Corporation

- 9.10 Pyrowave Inc.

- 9.11 Recycling Technologies Ltd

- 9.12 Brightmark LLC

- 9.13 Quantafuel ASA

- 9.14 Carbios SA

生物分解滲透油市場按產品形式、包裝類型、應用、最終用戶和分銷管道分類-2026-2032年全球預測生物基滲透油市場按產品類型、終端用戶產業和分銷管道分類-2026-2032年全球預測生物基防銹油市場按產品類型、包裝、應用和銷售管道分類-2026-2032年全球預測生物基防霧劑市場按類型、來源、形態、應用、終端用戶產業和銷售管道分類-2026-2032年全球預測

生物分解滲透油市場按產品形式、包裝類型、應用、最終用戶和分銷管道分類-2026-2032年全球預測生物基滲透油市場按產品類型、終端用戶產業和分銷管道分類-2026-2032年全球預測生物基防銹油市場按產品類型、包裝、應用和銷售管道分類-2026-2032年全球預測生物基防霧劑市場按類型、來源、形態、應用、終端用戶產業和銷售管道分類-2026-2032年全球預測 生物基尼龍市場規模、佔有率、成長及全球產業分析:應用及區域洞察與預測(2026-2034)

生物基尼龍市場規模、佔有率、成長及全球產業分析:應用及區域洞察與預測(2026-2034) 大豆化學品市場規模、佔有率和成長分析(按化學品類型、大豆產品類型、功能、大豆來源、形態、萃取方法、應用和地區分類)-2026-2033年產業預測

大豆化學品市場規模、佔有率和成長分析(按化學品類型、大豆產品類型、功能、大豆來源、形態、萃取方法、應用和地區分類)-2026-2033年產業預測 生物基化學品市場規模、佔有率和成長分析(按類型、應用和地區分類)-2026-2033年產業預測全球生化市場,2024-2031年

生物基化學品市場規模、佔有率和成長分析(按類型、應用和地區分類)-2026-2033年產業預測全球生化市場,2024-2031年 生物基化學品市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)

生物基化學品市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年) 生物為基礎隔熱材料的全球市場(2026年~2036年)

生物為基礎隔熱材料的全球市場(2026年~2036年)