|

市場調查報告書

商品編碼

1885816

船用舷內機市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Inboard Boat Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

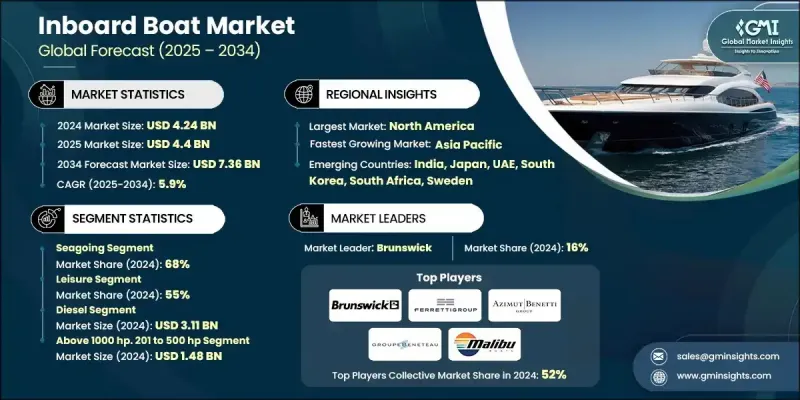

2024 年全球舷內船艇市場價值為 42.4 億美元,預計到 2034 年將以 5.9% 的複合年成長率成長至 73.6 億美元。

由於休閒船艇活動的增加、技術創新以及可支配收入的成長,市場正在擴張。包括先進的V型驅動和直驅系統在內的舷內引擎以其高性能、高效率和耐用性而聞名。現代舷內推進系統擴大與最佳化船體設計、燃油消耗、扭矩輸出和船舶整體性能的技術相結合。美國EPA Tier 3/4標準、國際海事組織MARPOL附則VI以及歐洲歐盟RCD2等監管框架正在推動原始設備製造商(OEM)採用低氮氧化物燃燒技術、閉迴路燃油控制和先進的催化處理系統。例如,將於2024年生效的EPA Tier 3標準規定,功率超過600馬力的引擎必須減少60%的氮氧化物排放和50%的顆粒物排放。新冠疫情嚴重擾亂了供應鏈,並在短期內影響了市場動態。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 42.4億美元 |

| 預測值 | 73.6億美元 |

| 複合年成長率 | 5.9% |

2024年,遠洋船舶市佔率達到68%,預計2025年至2034年將以5.6%的複合年成長率成長。遠洋內燃機船舶在沿海、近海和遠洋海域作業,對引擎的要求很高,必須能夠承受海水腐蝕、遠航作業和惡劣海況。這些船舶通常配備500-1000馬力的雙引擎運動釣魚系統,巡航艇和拖網漁船則配備200-600馬力的單台或雙台柴油引擎,以及高功率多引擎配置。

休閒船舶市場在2024年佔據55%的市場佔有率,預計到2034年將以5.1%的複合年成長率成長。該市場涵蓋用於巡航、釣魚和水上運動等活動的休閒船舶。這些船舶的年使用時間通常較低,為50-100小時,消費者的購買決策主要受營運成本、購買價格、生活方式和個人喜好等因素的影響。

2024年,美國舷內機船艇市場規模達18.9億美元。市場成長受到技術創新和監管因素的影響,其中包括旨在減少氮氧化物和顆粒物排放的美國環保署第三階段排放標準。汽油引擎需要三元觸媒轉換器,而功率超過600馬力的柴油引擎則採用選擇性催化還原(SCR)系統。墨西哥灣沿岸各州和佛羅裡達州對配備雙柴油舷內機、專為長時間作業而最佳化的近海漁船需求旺盛。

全球內燃機艇市場的主要參與者包括 Azimut-Benetti、BAVARIA Yachts、Fairline Yachts、Ferretti、Groupe Beneteau、Malibu Boats、MasterCraft Boat、Princess Yachts International、Sanlorenzo、Sunseeker International 和 Yamaha。市場領導者致力於引擎效率、推進系統和船體設計的創新,以提高燃油經濟性、扭力輸出和船舶整體性能。各公司大力投資研發,整合數位技術,包括引擎診斷、導航系統和物聯網性能監控。與碼頭營運商、分銷商和豪華遊艇製造商的策略合作有助於擴大市場覆蓋範圍並改善售後服務。區域擴張和製造設施升級使各公司能夠滿足不斷成長的市場需求並遵守嚴格的排放法規。行銷活動強調生活方式和休閒娛樂的吸引力,以吸引有抱負的消費者。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 原物料供應商

- 零件製造商

- 船舶製造商和原始設備製造商

- 最終用戶及售後服務供應商

- 成本結構

- 利潤率

- 每個階段的價值增加

- 影響供應鏈的因素

- 科技顛覆因素

- 供應鏈脆弱性因素

- 顛覆者

- 科技驅動的顛覆

- 替代燃料供應中斷

- 數位轉型帶來的顛覆性影響

- 供應商格局

- 對力的影響

- 成長促進因素

- 嚴格的排放法規推動技術升級

- 疫情後休閒划船活動參與人數不斷成長

- 拖曳運動和水上運動的需求不斷成長

- 商用船舶船隊現代化要求

- 產業陷阱與挑戰

- 混合動力和電動船用系統的初始成本很高

- 排放合規和認證成本的複雜性

- 市場機遇

- 排放合規升級改造市場

- 替代燃料基礎設施開發

- 成長促進因素

- 技術趨勢與創新生態系統

- 目前技術

- 混合動力推進系統深度解析

- 全電池電力推進深潛

- 用於船舶應用的PEM燃料電池技術

- 氨作為船用燃料

- 新興技術

- 遠端診斷和無線更新

- 自主導航演算法

- 互聯船舶的網路安全架構

- 區塊鏈輔助供應鏈可追溯性

- 目前技術

- 成長潛力分析

- 監管環境

- IMO MARPOL 附錄 vi(i-iii 級,NOX ECAS)

- 歐盟休閒船艇指令及NRMM第五階段

- NMMA 和 ABYC 認證標準

- 零排放指令和綠色港口計劃

- 波特的分析

- PESTEL 分析

- 專利分析

- 成本細分分析

- 價格趨勢

- 按細分市場定價

- 船

- 地區

- 高階定價策略及理由

- 價值鏈成本結構分析

- 按應用和地區分類的價格敏感度

- 匯率波動導致的價格調整

- 按細分市場定價

- 生產統計

- 生產中心

- 消費中心

- 進出口

- 區域基礎設施和部署趨勢

- 電動船用引擎的充電基礎設施

- 替代燃料加註基礎設施

- 服務和維護基礎設施

- 製造基礎設施

- 專利分析

- 按技術領域分類的專利申請趨勢(2014-2024 年)

- 專利申請的地理分佈

- 主要專利持有者和創新領導者

- 新興技術專利(混合動力、電動、替代燃料)

- 專利到期分析及學名藥進入市場的機會

- 許可和技術轉移活動

- 專利訴訟與糾紛趨勢

- 對新進入者的自由運作分析

- 永續性和環境方面

- 減少實體原型製作和測試

- 提高能源效率

- 支援電氣化和減排技術

- 生命週期和電子垃圾管理

- 遵守環境法規

- 投資與融資分析

- 主要製造商的研發投入

- 電動船舶推進領域的創投

- 政府對清潔海洋技術的撥款和補貼

- 私募股權和策略投資活動

- 首次公開募股及公開市場活動

- 投資報酬率及退出分析

- 產品線及研發路線圖

- 產業研發格局概述

- 數位與自動駕駛技術路線圖(2024-2034)

- 按製造商分類的產品線

- 產品開發分析失敗

- 最佳情況

- 城市水道的全面電氣化

- 全球車隊預測性維護網路

- 船舶推動系統的循環經濟

- 監管驅動的市場轉型

- 數位孿生技術在船舶設計與營運的應用

- 風險評估與緩解策略

- 風險評估標準(可能性和影響)

- 風險監測和預警系統

- 保險與風險轉移

- 替代風險

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太

- 拉丁美洲

- 中東和非洲

- 競爭定位矩陣

- 戰略展望矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃和資金

- 高階定位策略

- 策略性OEM合作夥伴關係機會

- 競爭分析與獨特賣點

第5章:市場估算與預測:依水路分類,2021-2034年

- 主要趨勢

- 遠洋

- 內陸

第6章:市場估算與預測:以推進方式分類,2021-2034年

- 主要趨勢

- 汽油

- 柴油引擎

- 電的

第7章:市場估計與預測:依應用領域分類,2021-2034年

- 主要趨勢

- 閒暇

- 貨物運輸

- 人員運輸

- 釣魚

- 政府用途

第8章:市場估算與預測:依馬力分類,2021-2034年

- 主要趨勢

- 低於200馬力

- 201至500馬力

- 501至1000馬力

- 超過1000馬力

第9章:市場估算與預測:依船舶分類,2021-2034年

- 主要趨勢

- 中央控制台

- 快艇

- 浮橋

- 快艇弓形艇

- 其他

第10章:市場估計與預測:依地區分類,2021-2034年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 比利時

- 荷蘭

- 瑞典

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 新加坡

- 韓國

- 越南

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- 全球參與者

- Azimut-Benetti

- Brunswick

- Ferretti

- Groupe Beneteau

- Malibu Boats

- Princess Yachts International

- Yamaha

- 區域玩家

- BAVARIA Yachts

- Chaparral Boats

- Cruisers Yachts

- Fairline Yachts

- Formula Boats

- MasterCraft Boat

- Regal Boats

- Sanlorenzo

- Sunseeker International

- Tiara Yachts

- 新興玩家

- Bertram Yachts

- Centurion Boats

- Correct Craft

- Damen Shipyards

- Everblue Marine

- Fincantieri

- Gulf Craft

- Hatteras Yachts

- Horizon Yachts

- Ocean Alexander

- Sanlian Marine

- Toyama Shipbuilding

- Viking Yachts

- Wauquiez

The Global Inboard Boat Market was valued at USD 4.24 billion in 2024 and is estimated to grow at a CAGR of 5.9% to reach USD 7.36 billion by 2034.

The market is expanding owing to increasing recreational boating, technological innovations, and rising disposable incomes. Inboard engines, including advanced V-drive and direct-drive systems, are known for their high performance, efficiency, and durability. Modern inboard propulsion is increasingly integrated with technologies that optimize hull designs, fuel consumption, torque output, and overall vessel performance. Regulatory frameworks such as the EPA Tier 3/4 in the United States, IMO MARPOL Annex VI globally, and EU RCD2 in Europe are pushing OEMs to adopt low-NOx combustion technologies, closed-loop fuel control, and advanced catalytic treatment systems. For example, the EPA Tier 3 standards, effective from 2024, mandate a 60% reduction in NOx emissions and a 50% reduction in particulate matter for engines exceeding 600 hp. The COVID-19 pandemic significantly disrupted supply chains, affecting market dynamics in the short term.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.24 Billion |

| Forecast Value | $7.36 Billion |

| CAGR | 5.9% |

The seagoing segment held a 68% share in 2024 and is expected to grow at a CAGR of 5.6% from 2025 to 2034. Seagoing inboard boats operate in coastal, offshore, and blue-water conditions that demand engines capable of withstanding saltwater corrosion, long-range operations, and rough waves. These vessels often feature dual-engine sport fishing systems between 500-1000 hp, single or dual diesel engines ranging from 200-600 hp for cruisers and trawlers, and high-powered multi-engine configurations.

The leisure segment held a 55% share in 2024 and is forecast to grow at a CAGR of 5.1% through 2034. This segment covers recreational vessels for activities such as cruising, fishing, and water sports. These boats generally experience low annual usage of 50-100 hours, with consumer decisions heavily influenced by operational costs, purchase price, lifestyle, and aspirational preferences.

U.S. Inboard Boat Market generated USD 1.89 billion in 2024. The market growth is influenced by technical innovations and regulatory drivers, including EPA Tier 3 standards that reduce NOx and particulate matter emissions. Gasoline engines require three-way catalytic converters, while diesel engines over 600 hp utilize selective catalytic reduction (SCR) systems. States along the Gulf Coast and Florida show high demand for offshore fishing boats equipped with twin diesel inboard engines optimized for extended operations.

Key players in the Global Inboard Boat Market include Azimut-Benetti, BAVARIA Yachts, Fairline Yachts, Ferretti, Groupe Beneteau, Malibu Boats, MasterCraft Boat, Princess Yachts International, Sanlorenzo, Sunseeker International, and Yamaha. Market leaders focus on innovation in engine efficiency, propulsion systems, and hull design to improve fuel economy, torque output, and overall vessel performance. Companies invest heavily in R&D to integrate digital technologies, including engine diagnostics, navigation systems, and IoT-enabled performance monitoring. Strategic collaborations with marina operators, distributors, and luxury yacht builders help expand market reach and improve after-sales services. Regional expansions and manufacturing facility upgrades enable companies to meet growing demand and comply with strict emission regulations. Marketing efforts emphasize lifestyle and leisure appeal to attract aspirational consumers.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast

- 1.4 Primary research and validation

- 1.5 Some of the primary sources

- 1.6 Data mining sources

- 1.6.1 Secondary

- 1.6.1.1 Paid Sources

- 1.6.1.2 Public Sources

- 1.6.1.3 Sources, by region

- 1.6.1 Secondary

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Waterways

- 2.2.3 Propulsion

- 2.2.4 Application

- 2.2.5 Horsepower

- 2.2.6 Boat

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material suppliers

- 3.1.1.2 Component manufacturers

- 3.1.1.3 Boat builders & OEMs

- 3.1.1.4 End use & after-sales service providers

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Factors impacting the supply chain

- 3.1.5.1 Technology disruption factors

- 3.1.5.2 Supply chain vulnerability factors

- 3.1.6 Disruptors

- 3.1.6.1 Technology-driven disruptions

- 3.1.6.2 Alternative fuel disruptions

- 3.1.6.3 Digital transformation disruptions

- 3.1.1 Supplier landscape

- 3.2 Impact on forces

- 3.2.1 Growth drivers

- 3.2.1.1 Stringent emission regulations driving technology upgrades

- 3.2.1.2 Growing recreational boating participation post-pandemic

- 3.2.1.3 Rising demand for tow-sport & watersports activities

- 3.2.1.4 Commercial vessel fleet modernization requirements

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial cost of hybrid & electric inboard systems

- 3.2.2.2 Complexity of emission compliance & certification costs

- 3.2.3 Market opportunities

- 3.2.3.1 Retrofit market for emission compliance upgrades

- 3.2.3.2 Alternative fuel infrastructure development

- 3.2.1 Growth drivers

- 3.3 Technology trends & innovation ecosystem

- 3.3.1 Current technologies

- 3.3.1.1 Hybrid-electric propulsion deep dive

- 3.3.1.2 Full battery-electric propulsion deep dive

- 3.3.1.3 Pem fuel cell technology for marine applications

- 3.3.1.4 Ammonia as marine fuel

- 3.3.2 Emerging technologies

- 3.3.2.1 Remote diagnostics & over-the-air updates

- 3.3.2.2 Autonomous navigation algorithms

- 3.3.2.3 Cybersecurity architecture for connected vessels

- 3.3.2.4 Blockchain for supply chain traceability

- 3.3.1 Current technologies

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 IMO MARPOL annex vi (tier i-iii, NOX ECAS)

- 3.5.2 EU recreational craft directive & NRMM stage v

- 3.5.3 NMMA & ABYC certification standards

- 3.5.4 Zero-emission mandates & green port initiatives

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Patent analysis

- 3.9 Cost breakdown analysis

- 3.10 Price trends

- 3.10.1 Pricing by segment

- 3.10.1.1 Boat

- 3.10.1.2 Region

- 3.10.2 Premium pricing strategies and justification

- 3.10.3 Cost structure analysis across value chain

- 3.10.4 Price sensitivity by application and region

- 3.10.5 Price adjustments for currency fluctuations

- 3.10.1 Pricing by segment

- 3.11 Production statistics

- 3.11.1 Production hubs

- 3.11.2 Consumption hubs

- 3.11.3 Export and import

- 3.12 Regional infrastructure & deployment trends

- 3.12.1 Charging infrastructure for electric inboards

- 3.12.2 Alternative fuel bunkering infrastructure

- 3.12.3 Service & maintenance infrastructure

- 3.12.4 Manufacturing infrastructure

- 3.13 Patent analysis

- 3.13.1 Patent filing trends by technology area (2014-2024)

- 3.13.2 Geographic distribution of patent filings

- 3.13.3 Key patent holders & innovation leaders

- 3.13.4 Emerging technology patents (hybrid, electric, alternative fuels)

- 3.13.5 Patent expiration analysis & generic entry opportunities

- 3.13.6 Licensing & technology transfer activity

- 3.13.7 Patent litigation & dispute trends

- 3.13.8 Freedom-to-operate analysis for new entrants

- 3.14 Sustainability and environmental aspects

- 3.14.1 Reducing physical prototyping and testing

- 3.14.2 Energy efficiency improvements

- 3.14.3 Support for electrification and emission reduction technologies

- 3.14.4 Lifecycle and e-waste management

- 3.14.5 Compliance with environmental regulations

- 3.15 Investment & funding analysis

- 3.15.1 R&D investment by major manufacturers

- 3.15.2 Venture capital in electric marine propulsion

- 3.15.3 Government grants & subsidies for clean marine technology

- 3.15.4 Private equity & strategic investment activity

- 3.15.5 IPO & public market activity

- 3.15.6 Investment returns & exit analysis

- 3.16 Product pipeline & R&D roadmap

- 3.16.1 Industry R&D landscape overview

- 3.16.2 Digital & autonomous technology roadmap (2024-2034)

- 3.16.3 Product pipeline by manufacturer

- 3.16.4 Failed product development analysis

- 3.17 Best case scenarios

- 3.17.1 Full electrification of urban waterways

- 3.17.2 Predictive maintenance network across global fleets

- 3.17.3 Circular economy for marine propulsion

- 3.17.4 Regulatory-driven market transformation

- 3.17.5 Digital twin integration in vessel design and operations

- 3.18 Risk assessment & mitigation strategies

- 3.18.1 Risk assessment criteria (likelihood & impact)

- 3.18.2 Risk monitoring & early warning systems

- 3.18.3 Insurance & risk transfer

- 3.18.4 Substitution risk

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia-Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Premium positioning strategies

- 4.7 Strategic OEM partnership opportunities

- 4.8 Competitive analysis and USPs

Chapter 5 Market Estimates & Forecast, By Waterways, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Seagoing

- 5.3 Inland

Chapter 6 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Gasoline

- 6.3 Diesel

- 6.4 Electric

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Leisure

- 7.3 Transport of goods

- 7.4 Transport of people

- 7.5 Fishing

- 7.6 Government use

Chapter 8 Market Estimates & Forecast, By Horsepower, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Below 200 hp

- 8.3 201 to 500 hp

- 8.4 501 to 1000 hp

- 8.5 Above 1000 hp

Chapter 9 Market Estimates & Forecast, By Boat, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 Center console

- 9.3 Express cruiser

- 9.4 Pontoon

- 9.5 Runabout bowrider

- 9.6 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 10.1 North America

- 10.1.1 US

- 10.1.2 Canada

- 10.2 Europe

- 10.2.1 UK

- 10.2.2 Germany

- 10.2.3 France

- 10.2.4 Italy

- 10.2.5 Spain

- 10.2.6 Belgium

- 10.2.7 Netherlands

- 10.2.8 Sweden

- 10.2.9 Russia

- 10.3 Asia Pacific

- 10.3.1 China

- 10.3.2 India

- 10.3.3 Japan

- 10.3.4 Australia

- 10.3.5 Singapore

- 10.3.6 South Korea

- 10.3.7 Vietnam

- 10.3.8 Indonesia

- 10.4 Latin America

- 10.4.1 Brazil

- 10.4.2 Mexico

- 10.4.3 Argentina

- 10.5 MEA

- 10.5.1 South Africa

- 10.5.2 Saudi Arabia

- 10.5.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Azimut-Benetti

- 11.1.2 Brunswick

- 11.1.3 Ferretti

- 11.1.4 Groupe Beneteau

- 11.1.5 Malibu Boats

- 11.1.6 Princess Yachts International

- 11.1.7 Yamaha

- 11.2 Regional Players

- 11.2.1 BAVARIA Yachts

- 11.2.2 Chaparral Boats

- 11.2.3 Cruisers Yachts

- 11.2.4 Fairline Yachts

- 11.2.5 Formula Boats

- 11.2.6 MasterCraft Boat

- 11.2.7 Regal Boats

- 11.2.8 Sanlorenzo

- 11.2.9 Sunseeker International

- 11.2.10 Tiara Yachts

- 11.3 Emerging players

- 11.3.1 Bertram Yachts

- 11.3.2 Centurion Boats

- 11.3.3 Correct Craft

- 11.3.4 Damen Shipyards

- 11.3.5 Everblue Marine

- 11.3.6 Fincantieri

- 11.3.7 Gulf Craft

- 11.3.8 Hatteras Yachts

- 11.3.9 Horizon Yachts

- 11.3.10 Ocean Alexander

- 11.3.11 Sanlian Marine

- 11.3.12 Toyama Shipbuilding

- 11.3.13 Viking Yachts

- 11.3.14 Wauquiez

2026年全球船用引擎市場報告

2026年全球船用引擎市場報告 船內引擎市場規模、佔有率和成長分析(按引擎類型、功率輸出、應用、船舶類型、最終用戶和地區分類)-2026-2033年產業預測

船內引擎市場規模、佔有率和成長分析(按引擎類型、功率輸出、應用、船舶類型、最終用戶和地區分類)-2026-2033年產業預測 船用舷內機市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)

船用舷內機市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年) 全球船用舷內引擎(小於5MW)市場:市場佔有率和排名、總收入和需求預測(2025-2031)

全球船用舷內引擎(小於5MW)市場:市場佔有率和排名、總收入和需求預測(2025-2031) 舷內機市場,按引擎類型、按功率輸出、按燃料系統類型、按應用、按國家和地區 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測舷內機市場規模 - 按產品類型、功率、應用、點火、引擎和預測,2024 年至 2032 年

舷內機市場,按引擎類型、按功率輸出、按燃料系統類型、按應用、按國家和地區 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測舷內機市場規模 - 按產品類型、功率、應用、點火、引擎和預測,2024 年至 2032 年