|

市場調查報告書

商品編碼

1885795

人工智慧病理分析系統市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)AI-Powered Pathology Analysis System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

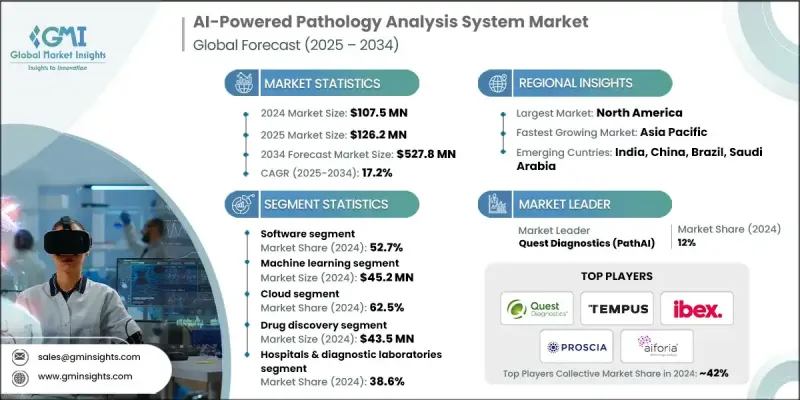

2024 年全球人工智慧病理分析系統市值為 1.075 億美元,預計到 2034 年將以 17.2% 的複合年成長率成長至 5.278 億美元。

市場擴張的促進因素包括數位病理學和遠端病理學的日益普及、對更快更準確診斷結果的需求不斷成長、慢性病患病率的上升以及人工智慧演算法的持續進步。熟練病理學家的短缺促使人們採用自動化解決方案,而人工智慧與基因組學和多組學資料的整合則創造了先進的診斷能力。數位病理學能夠遠端存取高解析度切片影像,促進跨地域協作;遠端病理學則允許專家在異地會診病例。人工智慧平台增強了影像分析能力,支援決策制定,並在專家審核前提供即時品質控制。這些系統利用人工智慧分析醫學影像,檢測疾病模式,並幫助病理學家實現更快、更一致、更準確的診斷。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 1.075億美元 |

| 預測值 | 5.278億美元 |

| 複合年成長率 | 17.2% |

預計到2024年,軟體領域將佔據52.7%的市場佔有率,這主要得益於藥物研發和臨床試驗領域軟體應用的不斷成長。醫院和實驗室正擴大部署軟體解決方案,以實現工作流程自動化並與電子健康記錄(EHR)系統整合,從而提高效率和生產力。

2024 年,機器學習領域的估值達到 4,520 萬美元,因為包括卷積神經網路 (CNN) 和生成對抗網路 (GAN) 在內的機器學習演算法能夠分析複雜的組織病理學模式,從而支持疾病的早期檢測。

預計到2024年,北美人工智慧病理分析系統市佔率將達到47.7%。該地區受益於先進的醫療基礎設施、數位病理學的廣泛應用以及對人工智慧研究的大量投入。包括TEMPUS、PHILIPS和PROSCIA在內的美國主要公司正與醫院和製藥公司合作,在診斷、生物標記開發和臨床試驗中部署人工智慧解決方案。監管政策的明確以及與電子病歷系統的整合進一步推動了該地區人工智慧技術的應用和部署。

人工智慧病理分析系統市場的主要企業包括IBEX、HOLOGIC、QRITIVE、Tribune Health、aiforia、Aiosyn、Mindpeak、VISIOPHARM、PathAI、Roche、Quest Diagnostics、PHILIPS、TEMPUS、Deep Bio、KFBIO和Indica Labs。市場參與者正透過加大研發投入來提升演算法準確性並擴展診斷能力,從而鞏固自身市場地位。他們與醫院、實驗室和製藥公司建立策略合作夥伴關係,同時擴大軟體部署規模,並將人工智慧整合到臨床工作流程中。地理擴張、收購和合作也是其核心策略,此外,他們還將平台與電子病歷系統整合,以提高互通性。各公司致力於推出先進的分析工具、基於機器學習的解決方案以及人工智慧驅動的工作流程自動化,以鞏固其市場地位,並加速其在診斷、藥物開發和臨床研究領域的應用。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 產業影響因素

- 成長促進因素

- 對更快診斷週轉時間和更高準確性的需求日益成長

- 慢性病盛行率上升

- 人工智慧演算法的進步

- 數位病理學和遠端病理學的應用日益廣泛

- 產業陷阱與挑戰

- 法規核准的複雜性

- 資料隱私和安全問題

- 市場機遇

- 越來越重視將人工智慧融入癌症篩檢和早期檢測項目

- 開發基於雲端的AI病理平台

- 成長促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 新興應用和用例

- 投資和融資環境

- 政策演變與變化

- 報銷方案

- 波特的分析

- PESTEL 分析

- 差距分析

- 未來市場趨勢

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 公司市佔率分析

- 全球的

- 北美洲

- 歐洲

- 亞太地區

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依組件分類,2021-2034年

- 主要趨勢

- 軟體

- 影像分析與模式識別

- 預測分析工具

- 工作流程自動化軟體

- 診斷決策支持

- 硬體

- 全切片影像(WSI)掃描儀

- 數位病理系統

- 顯微鏡

- 儲存系統

- 服務

- 實施與整合

- 諮詢與培訓

- 託管人工智慧服務

- 維護與支援

第6章:市場估計與預測:依技術分類,2021-2034年

- 主要趨勢

- 機器學習(ML)

- 卷積神經網路(CNN)

- 生成對抗網路(GAN)

- 循環神經網路(RNNS)

- 其他神經網路

- 基於電腦視覺的圖像分析

- 自然語言處理(NLP)

第7章:市場估算與預測:依部署模式分類,2021-2034年

- 主要趨勢

- 雲

- 本地部署

第8章:市場估算與預測:依應用案例分類,2021-2034年

- 主要趨勢

- 藥物發現

- 疾病診斷與預後

- 臨床工作流程

- 培訓與教育

第9章:市場估算與預測:依最終用途分類,2021-2034年

- 主要趨勢

- 醫院和診斷實驗室

- 生命科學公司

- 研究機構和學術中心

- 其他最終用途

第10章:市場估計與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- aetherAI

- aiforia

- Aiosyn

- deep bio

- HOLOGIC

- IBEX

- indica labs

- KFBIO

- mindpeak

- PHILIPS

- PROSCIA

- QRITIVE

- Quest Diagnostics (PathAI)

- Roche

- TEMPUS

- tribun HEALTH

- VISIOPHARM

The Global AI-Powered Pathology Analysis System Market was valued at USD 107.5 million in 2024 and is estimated to grow at a CAGR of 17.2% to reach USD 527.8 million by 2034.

The market expansion is driven by the rising adoption of digital pathology and telepathology, the growing need for faster and more accurate diagnostic results, the increasing prevalence of chronic diseases, and continuous advancements in AI algorithms. Shortages of skilled pathologists are encouraging the adoption of automated solutions, while integration of AI with genomic and multi-omics data is creating advanced diagnostic capabilities. Digital pathology enables remote access to high-resolution slide images, facilitating collaboration across geographies, and telepathology allows specialists to consult on cases from distant locations. AI-powered platforms enhance image analysis, support decision-making, and offer real-time quality control prior to expert review. These systems utilize artificial intelligence to analyze medical images, detect disease patterns, and assist pathologists in achieving faster, more consistent, and highly accurate diagnoses.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $107.5 Million |

| Forecast Value | $527.8 Million |

| CAGR | 17.2% |

The software segment held a 52.7% share in 2024, driven by rising adoption in drug discovery and clinical trials. Hospitals and laboratories are increasingly deploying software solutions to automate workflows and integrate with electronic health record (EHR) systems, enhancing efficiency and productivity.

The machine learning segment was valued at USD 45.2 million in 2024, as machine learning algorithms, including convolutional neural networks (CNNs) and generative adversarial networks (GANs), enable analysis of complex histopathological patterns, supporting early disease detection.

North America AI-Powered Pathology Analysis System Market held a 47.7% share in 2024. The region benefits from advanced healthcare infrastructure, high adoption of digital pathology, and substantial investments in AI research. Key US companies, including TEMPUS, PHILIPS, and PROSCIA, are collaborating with hospitals and pharmaceutical firms to deploy AI solutions in diagnostics, biomarker development, and clinical trials. Regulatory clarity and integration with EHR systems further support adoption and deployment in the region.

Leading companies in the AI-Powered Pathology Analysis System Market include IBEX, HOLOGIC, QRITIVE, Tribune Health, aiforia, Aiosyn, Mindpeak, VISIOPHARM, PathAI, Roche, Quest Diagnostics, PHILIPS, TEMPUS, Deep Bio, KFBIO, and Indica Labs. Market players are strengthening their position by investing in R&D to enhance algorithm accuracy and expand diagnostic capabilities. They are forming strategic partnerships with hospitals, laboratories, and pharmaceutical firms, while scaling software deployment and AI integration across clinical workflows. Geographic expansion, acquisitions, and collaborations are also central strategies, along with integrating platforms with EHR systems to improve interoperability. Companies focus on launching advanced analytics tools, machine learning-based solutions, and AI-powered workflow automation to solidify their market presence and accelerate adoption in diagnostics, drug development, and clinical research.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Component trends

- 2.2.3 Technology trends

- 2.2.4 Deployment mode trends

- 2.2.5 Use case trends

- 2.2.6 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for faster diagnostic turnaround time with improved accuracy

- 3.2.1.2 Rising prevalence of chronic diseases

- 3.2.1.3 Advancements in AI algorithms

- 3.2.1.4 Growing adoption of digital pathology and telepathology

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Regulatory approval complexities

- 3.2.2.2 Data privacy & security concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Increasing focus on AI integration in cancer screening and early detection programs

- 3.2.3.2 Development of cloud-based AI pathology platforms

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Emerging applications and use cases

- 3.7 Investment and funding landscape

- 3.8 Policy evolution and changes

- 3.9 Reimbursement scenario

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

- 3.12 Gap analysis

- 3.13 Future market trends

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Component, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Software

- 5.2.1 Image analysis & pattern recognition

- 5.2.2 Predictive analytics tools

- 5.2.3 Workflow automation software

- 5.2.4 Diagnostic decision support

- 5.3 Hardware

- 5.3.1 Whole slide imaging (WSI) scanners

- 5.3.2 Digital pathology systems

- 5.3.3 Microscopes

- 5.3.4 Storage systems

- 5.4 Services

- 5.4.1 Implementation & integration

- 5.4.2 Consulting & training

- 5.4.3 Managed AI services

- 5.4.4 Maintenance & support

Chapter 6 Market Estimates and Forecast, By Technology, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Machine learning (ML)

- 6.2.1 Convolutional neural networks (CNNS)

- 6.2.2 Generative adversarial networks (GANS)

- 6.2.3 Recurrent neural networks (RNNS)

- 6.2.4 Other neural networks

- 6.3 Computer vision-based image analysis

- 6.4 Natural language processing (NLP)

Chapter 7 Market Estimates and Forecast, By Deployment Mode, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Cloud

- 7.3 On-premise

Chapter 8 Market Estimates and Forecast, By Use Case, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Drug discovery

- 8.3 Disease diagnosis & prognosis

- 8.4 Clinical workflow

- 8.5 Training & education

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals & diagnostic laboratories

- 9.3 Life sciences companies

- 9.4 Research institutes & academic centers

- 9.5 Other end use

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East & Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 aetherAI

- 11.2 aiforia

- 11.3 Aiosyn

- 11.4 deep bio

- 11.5 HOLOGIC

- 11.6 IBEX

- 11.7 indica labs

- 11.8 KFBIO

- 11.9 mindpeak

- 11.10 PHILIPS

- 11.11 PROSCIA

- 11.12 QRITIVE

- 11.13 Quest Diagnostics (PathAI)

- 11.14 Roche

- 11.15 TEMPUS

- 11.16 tribun HEALTH

- 11.17 VISIOPHARM

3D步態和運動分析系統市場(按組件、最終用戶、技術、應用、部署模式和通路分類),全球預測(2026-2032)

3D步態和運動分析系統市場(按組件、最終用戶、技術、應用、部署模式和通路分類),全球預測(2026-2032) 心率監測器市場規模、佔有率和成長分析:按產品類型、最終用戶、應用和地區分類 - 2026-2033 年產業預測

心率監測器市場規模、佔有率和成長分析:按產品類型、最終用戶、應用和地區分類 - 2026-2033 年產業預測 人工智慧病理分析系統市場規模、佔有率和成長分析:按組件、技術、部署模式、用例、最終用途和地區分類-產業預測(2026-2033 年)

人工智慧病理分析系統市場規模、佔有率和成長分析:按組件、技術、部署模式、用例、最終用途和地區分類-產業預測(2026-2033 年) 2026年全球心率監測設備市場報告呼吸頻率監測儀市場按產品類型、最終用戶、技術、應用、連接方式和分銷管道分類,全球預測(2026-2032年)

2026年全球心率監測設備市場報告呼吸頻率監測儀市場按產品類型、最終用戶、技術、應用、連接方式和分銷管道分類,全球預測(2026-2032年) 全球心率監測器市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析以及未來預測(2026-2034)

全球心率監測器市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析以及未來預測(2026-2034) 穿戴式汗液分析設備市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)

穿戴式汗液分析設備市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年) 全球心率變異性監測市場:預測至 2032 年—按產品類型、訊號處理、連接方式、技術、應用、最終用戶和地區進行分析

全球心率變異性監測市場:預測至 2032 年—按產品類型、訊號處理、連接方式、技術、應用、最終用戶和地區進行分析 全球光學心率感測器市場

全球光學心率感測器市場