|

市場調查報告書

商品編碼

1876636

汽車全像顯示半導體市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Automotive Holographic Display Semiconductors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

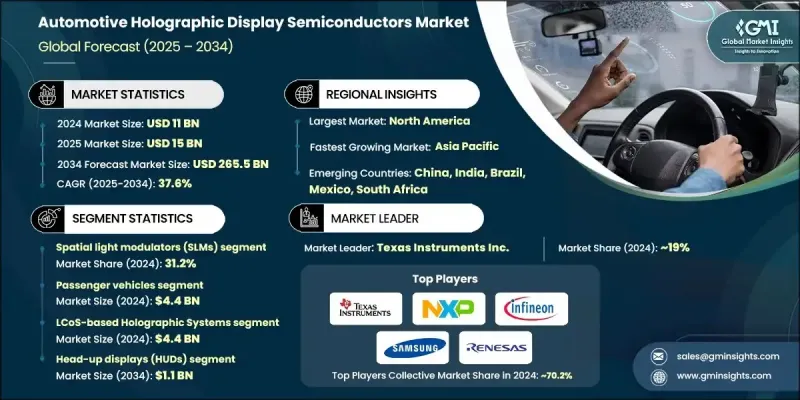

2024 年全球汽車全像顯示半導體市場價值為 110 億美元,預計到 2034 年將以 37.6% 的複合年成長率成長至 2655 億美元。

擴增實境和數位視覺化技術在汽車領域的快速普及,正加速推動對驅動下一代全像顯示系統的先進半導體的需求。汽車製造商日益專注於整合高性能晶片,以提供超清晰的即時影像,從而提升駕駛安全性和沈浸式資訊娛樂體驗。隨著汽車產業向互聯和自動駕駛汽車轉型,全像顯示器正被用於將關鍵資料直接投射到駕駛員的視線範圍內,從而提高駕駛員的態勢感知能力和整體安全性。這些創新的顯示系統依賴功能強大的半導體,能夠即時處理複雜的視覺訊息,並在動態條件下保持性能穩定。各國政府大力推廣智慧移動、永續發展和電動車技術,也推動了半導體技術的創新和應用。高階汽車和電動車產量的擴張,以及消費者對未來車載環境日益成長的需求,持續增強市場成長。技術供應商、半導體公司和汽車製造商之間的持續合作,正在加速先進全像顯示系統的商業化進程,從而重新定義數位座艙體驗。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 110億美元 |

| 預測值 | 2655億美元 |

| 複合年成長率 | 37.6% |

2024年,數位微鏡元件(DMD)市場規模達28億美元,預計2034年將以39.5%的複合年成長率成長。基於DMD的半導體裝置能夠提供卓越的影像精準度、亮度和對比度,使其成為高效能全像顯示器和抬頭顯示器不可或缺的一部分。這些系統採用數千個微型反射鏡來極其精確地操控光線,從而實現生動、高解析度的投影。它們在各種光照環境下保持清晰度和響應速度的能力,增強了駕駛員的視野和即時感知能力。隨著DMD支援高級駕駛輔助、導航視覺化和安全警報等功能,其在電動車和自動駕駛汽車中的應用正在迅速擴展,幫助製造商滿足消費者對下一代汽車顯示系統日益成長的需求。

2024年,乘用車市場規模預計將達44億美元。這一市場主導地位主要歸功於消費者對先進資訊娛樂系統、擴增實境介面和駕駛輔助技術的日益成長的興趣。電動車和豪華車產量的不斷增加,進一步提升了對能夠提供高效電源管理和優質視覺輸出的全像顯示半導體的需求。製造商正致力於開發專為乘用車設計的、經濟高效且節能的半導體解決方案,以兼顧性能和價格。車內沉浸式、互動式數位顯示器的需求持續成長,正在重塑整個汽車產業的使用者體驗標準。

2024年,北美汽車全像顯示半導體市場佔有率達到28.2%。該地區市場受益於快速的技術創新、電動車的強勁普及以及擴增實境抬頭顯示器的早期應用。研發投入龐大、政府大力推動互聯出行,以及眾多知名半導體生產商的存在,都為市場的穩定擴張提供了支撐。該地區的汽車產業正將全像顯示系統視為競爭優勢,致力於提升連網汽車的安全性、駕駛感知能力和娛樂功能。

推動全球汽車全像顯示器半導體市場發展的關鍵企業包括:Synaptics Incorporated、三星電子有限公司、德州儀器公司、Himax Technologies, Inc.、恩智浦半導體公司、瑞薩電子株式會社、羅姆半導體公司、英飛凌科技股份公司、Magnachip Semiconductor Corporation、諾瓦姆半導體公司、Cemadepine 半導體公司Ltd.、FocalTech Systems Co., Ltd.、歐司朗股份公司、Valens Semiconductor Ltd.、Appotronics Co., Ltd.、Ceres Holographics Ltd. 和 Envisics Ltd.。這些領導企業正積極推行創新驅動型策略,致力於提升影像精準度、能源效率和整合能力。許多企業正大力投資研發,以開發針對擴增實境和即時3D視覺化最佳化的半導體架構。與汽車製造商和技術開發商的合作正在加速產品在下一代汽車中的測試和部署。為了滿足抬頭顯示器和全像顯示系統對高速、低功耗晶片日益成長的需求,各公司也正在擴大生產能力。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 產業影響因素

- 成長促進因素

- 擴增實境(AR)抬頭顯示器(HUD)在提高駕駛員安全性和導航視覺化方面的應用日益廣泛。

- 市場對配備先進數位系統的高階汽車和電動車的需求不斷成長。

- 半導體設計技術的不斷進步提高了顯示性能和能源效率。

- 消費者越來越偏愛沉浸式和未來感十足的車內體驗。

- 產業陷阱與挑戰

- 全像顯示半導體的高昂生產和整合成本。

- 緊湊型汽車儀錶板的熱管理和小型化問題。

- 市場機遇

- 開發用於下一代擴增實境和3D顯示系統的節能型半導體材料。

- 將人工智慧驅動的全像視覺化技術應用於預測導航和安全警報。

- 成長促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 美國

- 加拿大

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 北美洲

- 技術格局

- 當前趨勢

- 新興技術

- 管道分析

- 未來市場趨勢

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 全球的

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依半導體裝置類型分類,2021-2034年

- 主要趨勢

- 空間光調變器(SLM)

- 數位微鏡裝置(DMD)

- 半導體加工

- 驅動積體電路

- 電源管理積體電路

第6章:市場估價與預測:依車輛類型分類,2021-2034年

- 主要趨勢

- 搭乘用車

- 商用車輛

- 自動駕駛汽車

第7章:市場估算與預測:依全像技術類型分類,2021-2034年

- 主要趨勢

- 基於LCoS的全像系統

- 基於DLP的全像系統

- 基於超表面的系統

- 波導整合系統

第8章:市場估算與預測:依應用領域分類,2021-2034年

- 主要趨勢

- 抬頭顯示器(HUD)

- 儀表板顯示幕

- 資訊娛樂系統

第9章:市場估計與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- Texas Instruments Inc.

- NXP Semiconductors NV

- Renesas Electronics Corporation

- Samsung Electronics Co., Ltd.

- Himax Technologies, Inc.

- ROHM Semiconductor

- Infineon Technologies AG

- Synaptics Incorporated

- Magnachip Semiconductor Corporation

- Novatek Microelectronics Corp.

- ON Semiconductor Corporation

- Raydium Semiconductor Corporation

- LX Semicon Co., Ltd.

- FocalTech Systems Co., Ltd.

- ams OSRAM AG

- Valens Semiconductor Ltd.

- Ceres Holographics Ltd.

- Appotronics Co., Ltd.

- Envisics Ltd.

The Global Automotive Holographic Display Semiconductors Market was valued at USD 11 billion in 2024 and is estimated to grow at a CAGR of 37.6% to reach USD 265.5 billion by 2034.

The rapid adoption of augmented reality and digital visualization technologies in vehicles is accelerating demand for advanced semiconductors that power next-generation holographic display systems. Automakers are increasingly focusing on integrating high-performance chips capable of delivering ultra-clear, real-time images for enhanced driver safety and immersive infotainment experiences. As the automotive industry transitions toward connected and autonomous vehicles, holographic displays are being used to project critical data directly within the driver's line of sight, improving situational awareness and overall safety. These innovative display systems rely on powerful semiconductors that process complex visual information instantly and maintain performance under dynamic conditions. Governments promoting smart mobility, sustainability, and electric vehicle technologies are also driving semiconductor innovation and adoption. The expansion of premium and electric vehicle production, combined with growing consumer demand for futuristic in-car environments, continues to strengthen market growth. Ongoing collaboration between technology providers, semiconductor companies, and automotive manufacturers is accelerating the commercialization of advanced holographic display systems that redefine the digital cockpit experience.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $11 Billion |

| Forecast Value | $265.5 Billion |

| CAGR | 37.6% |

The digital micromirror devices (DMDs) segment accounted for USD 2.8 billion in 2024 and is anticipated to grow at a CAGR of 39.5% through 2034. DMD-based semiconductors deliver exceptional image precision, brightness, and contrast, making them integral to high-performance holographic and head-up displays. These systems employ thousands of microscopic mirrors to manipulate light with extreme accuracy, resulting in vivid and high-resolution projections. Their ability to maintain clarity and responsiveness in diverse lighting environments enhances driver visibility and real-time awareness. The integration of DMDs into electric and autonomous vehicles is expanding rapidly as they support advanced driver assistance, navigation visualization, and safety alerts, helping manufacturers meet growing expectations for next-level automotive display systems.

The passenger vehicle segment generated USD 4.4 billion in 2024. This dominance is attributed to rising consumer interest in advanced infotainment, augmented reality interfaces, and driver assistance technologies. The increasing production of electric and luxury cars is further elevating the need for holographic display semiconductors that provide efficient power management and premium visual output. Manufacturers are emphasizing the development of cost-effective, energy-optimized semiconductor solutions specifically designed for passenger vehicles to balance performance and affordability. The demand for immersive, interactive digital displays inside vehicles continues to rise, reshaping user experience standards across the automotive industry.

North America Automotive Holographic Display Semiconductors Market held a share of 28.2% in 2024. The regional market benefits from rapid technological innovation, strong electric vehicle adoption, and early integration of augmented reality head-up displays. High investment in R&D, government initiatives promoting connected mobility, and the presence of prominent semiconductor producers are supporting steady market expansion. The region's automotive sector is leveraging holographic display systems as a competitive differentiator, focusing on enhancing safety, driver awareness, and entertainment capabilities within connected vehicles.

Key players shaping the Global Automotive Holographic Display Semiconductors Market include Synaptics Incorporated, Samsung Electronics Co., Ltd., Texas Instruments Inc., Himax Technologies, Inc., NXP Semiconductors N.V., Renesas Electronics Corporation, ROHM Semiconductor, Infineon Technologies AG, Magnachip Semiconductor Corporation, Novatek Microelectronics Corp., ON Semiconductor Corporation, Raydium Semiconductor Corporation, LX Semicon Co., Ltd., FocalTech Systems Co., Ltd., ams OSRAM AG, Valens Semiconductor Ltd., Appotronics Co., Ltd., Ceres Holographics Ltd., and Envisics Ltd. Leading companies in the Automotive Holographic Display Semiconductors Market are pursuing innovation-driven strategies focused on enhancing image precision, energy efficiency, and integration capabilities. Many are investing heavily in R&D to develop semiconductor architectures optimized for augmented reality and real-time 3D visualization. Collaborations with automakers and technology developers are accelerating product testing and deployment in next-generation vehicles. Companies are also expanding manufacturing capacity to meet growing demand for high-speed, low-power chips used in head-up and holographic display systems.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional Trends

- 2.2.2 Semiconductor Device Type Trends

- 2.2.3 Vehicle Type Trends

- 2.2.4 Holographic Technology Type Trends

- 2.2.5 Application Trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing Adoption of Reality (AR) Head-Up Displays (HUDs) for Improved Driver Safety and Navigation Visualization.

- 3.2.1.2 Rising Demand for Premium and Electric Vehicles Equipped with Advanced Digital Systems.

- 3.2.1.3 Continuous Technological Advancements in Semiconductor Design Enhancing Display Performance and Energy Efficiency.

- 3.2.1.4 Increasing Consumer Preference for Immersive and Futuristic In-Car Experiences.

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Production and Integration Costs Associated with Holographic Display Semiconductors.

- 3.2.2.2 Thermal Management and Miniaturization Issues in Compact Vehicle Dashboards.

- 3.2.3 Market opportunities

- 3.2.3.1 Development of Energy-efficient Semiconductor Materials for Next-Generation AR and 3D Display Systems.

- 3.2.3.2 Integration of AI-driven Holographic Visualization for Predictive Navigation and Safety Alerts.

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S.

- 3.4.1.2 Canada

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.4.1 North America

- 3.5 Technology landscape

- 3.5.1 Current trends

- 3.5.2 Emerging technologies

- 3.6 Pipeline analysis

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.2.5 Latin America

- 4.2.6 Middle East and Africa

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Semiconductor Device Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Spatial Light Modulators (SLMs)

- 5.3 Digital Micromirror Devices (DMDs)

- 5.4 Processing Semiconductors

- 5.5 Driver Integrated Circuits

- 5.6 Power Management ICs

Chapter 6 Market Estimates and Forecast, By Vehicle Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Passenger Vehicles

- 6.3 Commercial Vehicles

- 6.4 Autonomous Vehicles

Chapter 7 Market Estimates and Forecast, By Holographic Technology Type, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 LCoS-based Holographic Systems

- 7.3 DLP-based Holographic Systems

- 7.4 Metasurface-based Systems

- 7.5 Waveguide-integrated Systems

Chapter 8 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Head-Up Displays (HUDs)

- 8.3 Instrument Cluster Displays

- 8.4 Infotainment Systems

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Texas Instruments Inc.

- 10.2 NXP Semiconductors N.V.

- 10.3 Renesas Electronics Corporation

- 10.4 Samsung Electronics Co., Ltd.

- 10.5 Himax Technologies, Inc.

- 10.6 ROHM Semiconductor

- 10.7 Infineon Technologies AG

- 10.8 Synaptics Incorporated

- 10.9 Magnachip Semiconductor Corporation

- 10.10 Novatek Microelectronics Corp.

- 10.11 ON Semiconductor Corporation

- 10.12 Raydium Semiconductor Corporation

- 10.13 LX Semicon Co., Ltd.

- 10.14 FocalTech Systems Co., Ltd.

- 10.15 ams OSRAM AG

- 10.16 Valens Semiconductor Ltd.

- 10.17 Ceres Holographics Ltd.

- 10.18 Appotronics Co., Ltd.

- 10.19 Envisics Ltd.

汽車半導體市場:按組件、應用、車輛類型和最終用戶分類-2026-2032年全球市場預測

汽車半導體市場:按組件、應用、車輛類型和最終用戶分類-2026-2032年全球市場預測 汽車功率半導體市場:策略性洞察與預測(2026-2031年)

汽車功率半導體市場:策略性洞察與預測(2026-2031年) 汽車半導體市場分析及預測(至2035年):依類型、產品類型、技術、組件、應用、材質、裝置、最終使用者、功能及安裝類型分類

汽車半導體市場分析及預測(至2035年):依類型、產品類型、技術、組件、應用、材質、裝置、最終使用者、功能及安裝類型分類 2026年全球汽車半導體市場報告汽車用碳化矽元件市場:2026-2032年全球預測(依元件類型、應用、額定電壓和封裝類型分類)汽車用碳化矽功率元件市場:2026-2032年全球預測(依元件類型、車輛型態、電壓等級、額定功率、銷售管道和應用分類)汽車用碳化矽功率模組市場:按車輛類型、配置、額定功率、冷卻方式和應用分類,全球預測(2026-2032年)

2026年全球汽車半導體市場報告汽車用碳化矽元件市場:2026-2032年全球預測(依元件類型、應用、額定電壓和封裝類型分類)汽車用碳化矽功率元件市場:2026-2032年全球預測(依元件類型、車輛型態、電壓等級、額定功率、銷售管道和應用分類)汽車用碳化矽功率模組市場:按車輛類型、配置、額定功率、冷卻方式和應用分類,全球預測(2026-2032年) 汽車半導體市場:驅動智慧(2025)

汽車半導體市場:驅動智慧(2025) 乘用車半導體市場-全球產業規模、佔有率、趨勢、機會和預測,按組件類型、應用類型、地區和競爭格局分類,2020-2030年預測

乘用車半導體市場-全球產業規模、佔有率、趨勢、機會和預測,按組件類型、應用類型、地區和競爭格局分類,2020-2030年預測 汽車功率半導體及模組(SiC、GaN)產業(2025)

汽車功率半導體及模組(SiC、GaN)產業(2025)